.png)

The best companies for infinite banking in 2026 are mutual life insurers with long dividend histories, flexible paid-up additions, and a loan structure that supports disciplined borrowing. Penn Mutual, Guardian, MassMutual, and a handful of others lead, but the right carrier depends on your policy design and time horizon, not the dividend rate.

Most people choose an infinite banking carrier the way they shop for a savings account. They line up the dividend rates, pick the highest number, and assume they have made the right call. That single number tells you almost nothing about whether a policy will function as a capital base for the next thirty years, and the dividend rate is gross, before the internal costs that actually determine what compounds inside the policy.

The carrier matters far less than the design of the policy and your discipline in funding it. A well-designed policy at a strong carrier outperforms a poorly designed policy at the carrier with the flashiest dividend rate, every time. Carrier choice is real, and it matters, but it is the second decision, not the first.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we work with most of the carriers serious practitioners use. This guide covers what actually makes a life insurer good for this strategy, the difference between direct and non-direct recognition, how we evaluate a carrier against The And Asset framework, and an honest, name-by-name read on the ten carriers that come up most. We will also tell you which ones we would not lead with, and why.

- The best infinite banking carriers are mutual or member-owned, with decades of uninterrupted dividends and strong financial ratings.

- Policy design and paid-up additions flexibility drive early cash value more than the headline dividend rate does.

- Direct recognition adjusts the dividend on borrowed cash value; non-direct leaves it unchanged. Neither is automatically better.

- Penn Mutual, Guardian, and Pan-American Life are direct recognition; most others are non-direct; Ameritas lets you choose.

- Several leading carriers, including Penn Mutual, Lafayette Life, and OneAmerica, do not sell core whole life in New York.

- MassMutual is financially strong but has taken a public stance against infinite banking marketing.

01 / The problemWhy the highest dividend rate is the wrong place to start

Carrier choice solves for a handful of structural questions, and the headline dividend rate answers almost none of them. The real questions are whether the company will still be paying dividends in forty years, whether its loan mechanics support how you plan to deploy capital, and whether its product can be designed to push cash value to the limit without tipping into a Modified Endowment Contract.

The dividend interest rate is a gross number. Your cash value does not grow at the declared rate. It grows at the dividend net of mortality and expense charges, which is the figure that actually compounds inside the policy. A carrier can declare the largest dividend rate in the industry and still produce middling long-term growth once its internal costs and product design are accounted for. Comparing dividend rates across carriers is like comparing car horsepower without knowing the weight of the car.

We are not out here battling over who has the higher dividend rate. The question is which product is better for your situation, and how the designed illustration actually performs.

02 / The criteriaWhat makes a life insurance company good for infinite banking?

A good infinite banking carrier is mutual or member-owned, has paid dividends for decades, holds a strong financial rating, supports a heavy paid-up additions rider, and offers a loan structure that lets you borrow while the policy keeps compounding. Those five traits matter in that order, and the dividend rate is not on the list as a primary screen.

Here is what each one is doing for you.

- Mutual or member-owned structure. A mutual company is owned by its policyholders, not outside shareholders, so dividends flow to the people who hold the policies. Most top infinite banking carriers are full mutuals. A few, like Lafayette Life and OneAmerica, operate as stock companies under a mutual holding company. Foresters is a fraternal benefit society, member-owned but not a true mutual.

- Long dividend history. Uninterrupted dividends through depressions, wars, and rate cycles signal a company that manages for the long horizon this strategy requires. Several of these carriers have paid dividends for well over a century.

- Financial strength. An AM Best rating of A or better, ideally backed by a high COMDEX score, tells you the carrier can honor dividends and loans across decades. This is a stability screen, not a growth screen.

- Paid-up additions flexibility. The paid-up additions rider is the engine of early cash value. How much you can fund, whether payments are scheduled or anytime, and whether you can catch up a missed year all vary widely by carrier.

- Loan structure. How fast you can access a loan, the recognition type, and the loan-to-dividend spread determine how the policy behaves when you actually put it to work.

What the carrier is actually being chosen for

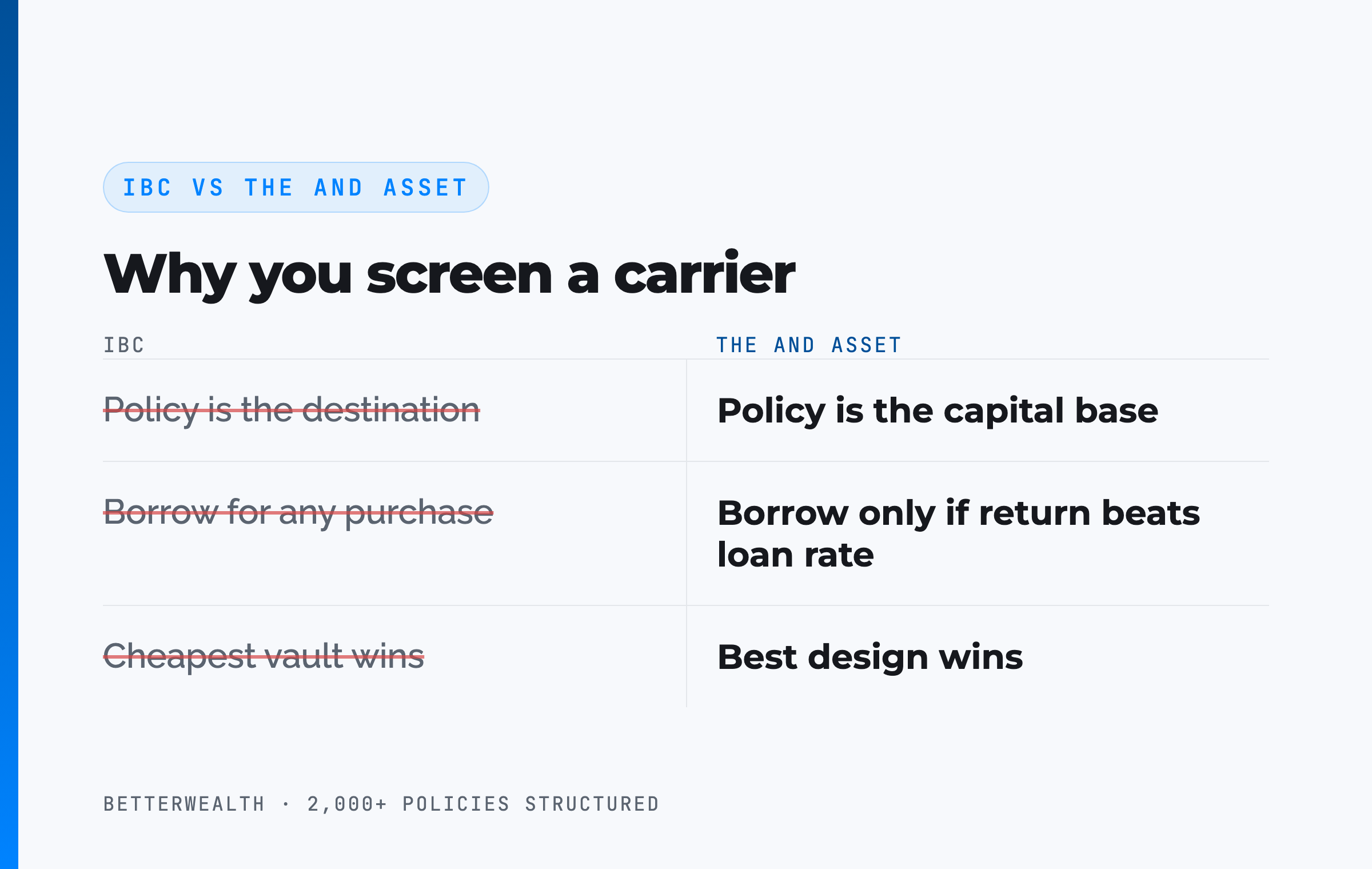

The carrier is the issuer of your capital base. It is not the strategy. The strategy is what we call The And Asset, and it determines why any of these traits matter in the first place. Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

IBC says you can use a whole life policy as a personal banking system for any purchase, and the carrier is just the vault. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. That distinction changes what you screen a carrier for. You are not shopping for the cheapest vault. You are shopping for the carrier whose design lets your dollars do two jobs at once: the policy compounding net of charges while the deployed capital earns its own return.

The math has to work. The carrier just has to let it.

03 / RecognitionWhat does direct vs non-direct recognition actually mean?

Direct recognition means the carrier adjusts the dividend on the portion of cash value you have borrowed against; non-direct recognition means the dividend is unchanged whether or not you have a loan outstanding. This is the single most misunderstood carrier characteristic, and the marketing around it is mostly wrong in both directions.

The common fear about direct recognition is that borrowing drags your dividend down. Sometimes it does, and sometimes the carrier adjusts the dividend on borrowed funds up, depending on the rate environment. The point most people miss is that a direct-recognition carrier with a guaranteed spread removes a variable from your math. Penn Mutual, for example, guarantees a 0.65% spread between the loan rate and the dividend rate in policy years 1 through 10, and a 0% spread from year 11 onward. That fixed, known spread makes distribution-phase planning more predictable, not less.

Non-direct recognition has its own appeal. Your dividend is credited on the full cash value regardless of loans, so the math is simple: borrow, and the policy keeps crediting as if you had not. Neither structure is automatically superior. The right choice depends on how and when you plan to borrow, and what the rest of the design looks like.

Direct recognition is not the dirty word people think it is. With a guaranteed spread, it locks in your cost of borrowing, which makes retirement income math easier, not harder.

Which carriers are direct and which are non-direct

Among the carriers serious practitioners use, the split is clear. Penn Mutual, Guardian, and Pan-American Life are direct recognition. MassMutual, New York Life, Lafayette Life, OneAmerica, Foresters, and Security Mutual are non-direct recognition. Ameritas is the unusual one: it lets you choose a fixed direct-recognition loan or a variable non-direct loan, though only one at a time. Recognition type is a design input, not a verdict on the carrier.

04 / The methodHow do you evaluate a carrier for The And Asset?

You evaluate a carrier in five steps, and the order matters because each step screens out a different failure mode. This is the sequence we run before we recommend any carrier to a client.

- Confirm mutual ownership and dividend history. Start with a mutual or member-owned carrier with a long, uninterrupted dividend record. Ownership structure aligns the company with policyholders. A century of unbroken dividends shows it has managed through every kind of market.

- Check financial strength. Verify the AM Best rating, and the COMDEX score where one exists. The carrier must be able to pay dividends and honor loans across a multi-decade horizon. A small carrier with a thin balance sheet is a different risk than a top-rated mutual.

- Understand the recognition type and spread. Determine whether the carrier is direct or non-direct, and read the loan-to-dividend spread. This governs how borrowing affects your growth and how predictable your distribution math will be.

- Evaluate paid-up additions flexibility. Examine the PUA rider in detail: maximum funding, anytime versus scheduled payments, catch-up provisions, and rolling minimums. This is where carriers differ most, and where early cash value is won or lost.

- Match the carrier to your design and horizon. Choose the carrier whose product can be designed for your funding personality and time horizon. Someone who needs more early liquidity and someone funding for 25 years should not necessarily land at the same carrier.

Notice what is not on this list: picking the carrier with the highest dividend rate. That step does not exist, because the rate is an output of the design, not an input to the decision. For the design side of this equation, we go deep on how to structure a policy separately, because design is where most of the result is determined.

The right carrier depends on a specific person doing specific things.

This guide fits you if

- You have a long capital horizon (10+ years)

- You can name a use for capital that beats the loan cost

- You want to understand design before carrier

- You think in IRR and opportunity cost

It does not fit you if

- You are shopping purely on dividend rate

- You want a savings account, not a life insurance strategy

- You need the cash back in year one or two

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you which carrier and design fit your situation. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The carriersThe major infinite banking carriers, reviewed honestly

Below is a name-by-name read on the ten carriers that come up most when entrepreneurs and high-income earners build a policy for this strategy. Each one earns its place for a different reason, and each carries tradeoffs a sales deck will not show you. Dividend figures are projected or recently declared, gross of internal costs, and not guaranteed. We maintain a full individual review for each carrier, linked from this hub.

Penn Mutual

Penn Mutual is the carrier we reach for most often when long-term growth is the priority. Founded in 1847, fully mutual, it is the only US carrier with an AM Best rating of A or better for 98 consecutive years, currently A+ (Superior). It is direct recognition with a guaranteed 0.65% loan-to-dividend spread in years 1 to 10 and 0% from year 11 on. Its 2026 dividend is roughly $300 million declared at a projected 6.1% rate, and its paid-up additions are the most flexible in the group, with anytime payments and full catch-up. Its weakness is lower early cash value, running 7 to 12% behind some competitors in the first five years, and it does not sell in New York. It fits a long horizon, not a liquidity-first need.

Read the full Penn Mutual infinite banking review →

Guardian

Guardian is the financial-strength benchmark, holding a COMDEX of 100 and an AM Best rating of A++ (Superior). Mutual since 1925 and founded in 1860, it is direct recognition with a fixed 5% loan rate for the first 10 years, which makes borrowing costs predictable regardless of the rate environment. Its 2026 dividend is roughly $1.7 billion at a projected 6.25% rate, and its early cash value is among the strongest, particularly on a front-load design. The tradeoffs: its paid-up additions are less flexible without the term rider that accelerates funding, and getting an aggressive cash-value design approved can require an experienced agent. It is available in all 50 states, including New York.

Read the full Guardian infinite banking review →

MassMutual

MassMutual is one of the strongest mutuals in the country, with a COMDEX of 98 and an A++ rating, and it declares one of the largest dividends in the industry, roughly $2.9 billion at a projected 6.6% rate for 2026. We include it honestly: MassMutual has taken a public and private stance against infinite banking marketing, and its paid-up additions riders are among the least flexible in the industry. The policy can still be designed for high cash value, and the company is rock-solid, but it is not positioned as an infinite banking carrier, and that posture is worth knowing before you build around it.

Read the full MassMutual infinite banking review →

New York Life

New York Life is the largest of these mutuals, founded in 1841, with a COMDEX of 100 and an A++ rating. Its 2026 dividend is roughly $2.78 billion at a projected 6.4% rate. The brand and balance sheet are unmatched. The tradeoff for this strategy is fit: New York Life is a captive, career-agent carrier, its paid-up additions are inflexible with no catch-up provision, and the infinite banking use case is a rounding error in its book. For a conservative buyer who values the name and balance sheet above all, it is defensible. For maximum design flexibility, it is not the first call.

Ameritas

Ameritas is the flexible-loan specialist. Fully mutual since 1887, it is the only carrier in this group that lets you choose your recognition type: a fixed 4.00% direct-recognition loan that never increases, or a variable non-direct loan currently around 5.80%. Its 2026 dividend interest rate is 5.10%, and its AM Best rating is A (Excellent), with a COMDEX of 83, lower than the top mutuals. It is openly supportive of this strategy, offers good early cash value access, and is available in New York. The step-down PUA schedule makes it less ideal for aggressive long-term max-funding, so it fits designs with room to grow.

Read the full Ameritas infinite banking review →

Lafayette Life

Lafayette Life is the practitioner's quiet favorite for early cash value. Operating since 1905 as a stock company under the Western & Southern mutual holding company, it is non-direct recognition with an A+ rating and a COMDEX of 95. Its 2026 dividend is roughly $123.3 million at a projected 5.9% rate. Its underwriting is genuinely familiar with this strategy, and its early cash value is industry-leading, often 82 to 92% of premium in year one on a cashflow design. The tradeoffs: service and underwriting have strained under rapid growth, large policies can be difficult to approve, and it does not sell in New York.

Read the full Lafayette Life infinite banking review →

OneAmerica

OneAmerica is the hybrid long-term-care leader that also serves this strategy well. A stock company under a mutual holding structure dating to 1877, it is non-direct recognition with an A+ rating and a COMDEX of 95. It is well known and supportive in the infinite banking community, offers fast loan access in two to three weeks, and has unusually few paid-up additions restrictions. Its weaknesses are honest: long-term growth often runs in the bottom quartile of these mutuals, it does not publish a dividend interest rate, and it does not sell in New York. Its standout edge is its market-leading hybrid LTC products.

Read the full OneAmerica infinite banking review →

Foresters Financial

Foresters is the member-benefits outlier. Founded in 1874, it is a fraternal benefit society rather than a true mutual, which means certificate holders become members with access to scholarships, grants, and other benefits beyond dividends. It is non-direct recognition with an A (Excellent) AM Best rating, a projected 6.00% dividend rate for 2026, fast 10-day loan access, and a standout 10-year paid-up additions catch-up window. The tradeoffs: projected long-term growth runs in the bottom quartile, and it does not sell in New York. The member benefits are a real differentiator for the right person.

Read the full Foresters infinite banking review →

Security Mutual

Security Mutual is the openly pro-IBC niche carrier. A mutual since 1886, it is non-direct recognition and markets directly to this strategy, with a flexible blended-term rider option and the fastest loan access in the group at 10 days. Its projected dividend rate is near 5.85%. The honest cautions are real: it is a small carrier with no COMDEX rating, an A- AM Best rating, a higher-than-average lapse ratio, and an unusually large share of its portfolio in policy loans. For a buyer who wants a carrier that fully embraces the strategy and has done the homework on the risk profile, it is an option. It is available in New York.

Read the full Security Mutual infinite banking review →

Pan-American Life

Pan-American Life is the carrier that most openly endorses the original concept, referencing Nelson Nash and Becoming Your Own Banker in its materials. It is direct recognition and offers some of the strongest early cash value in the industry, often in the 85 to 92% range on a front-load design. It is the natural fit for a buyer who wants maximum early access and a carrier that fully embraces the foundation of the strategy. As with every carrier here, the design and your horizon decide whether it belongs at the top of your list.

Read the full Pan-American Life infinite banking review →

06 / The mathDoes the return clear the carrier's loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow, and no carrier changes that test. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat any specific number as a variable to verify with the carrier, not a constant.

The decision structure is the same regardless of which company issued the policy. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, adjusted by the recognition spread if it is a direct-recognition carrier. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the same dollar has done two jobs. If it is lower, you have borrowed money to lose money slowly. The carrier's job is to make the spread as clean and predictable as possible. Your job is to only borrow when the deal clears.

If the deal does not clear the loan rate, do not borrow.

07 / Where people get this wrongThe mistakes that cost the most

The most expensive mistake is choosing a carrier on the dividend rate alone, and the second is treating carrier choice as the whole decision when it is the smaller half of it. Marketers have ruined how this strategy gets explained, and carrier selection is where the worst of it shows up.

You are not paying yourself interest, no matter which carrier you pick. The interest on a policy loan goes to the insurance company. Your return comes from what you deploy the borrowed capital into. Any agent who tells you that you are paying yourself back interest is either careless or selling, and that single misframe leads people to borrow for things that never clear the loan cost. The carrier does not save you from that error. Only the discipline does.

The other recurring mistake is buying the brand instead of the design. The largest, best-known mutual is not automatically the best fit for this strategy, and in several cases the carriers with the most flexible designs are the ones most people have never heard of. Read the honest pros and cons before you anchor on a name.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and carrier-comparison logic we use when we weigh companies like Penn Mutual, Guardian, and Lafayette Life against each other. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the real tradeoffs of carrier choice

Carrier choice brings real benefits, and every benefit comes with a tradeoff that disqualifies the carrier for some buyers. Pretending otherwise is how agents lose trust.

The benefits are concrete. A strong mutual gives you a century of dividend reliability, a balance sheet that will outlast you, and a loan you control. The right carrier's paid-up additions rider builds usable cash value early, and the right recognition structure makes your borrowing math predictable. Those are not small things over thirty years.

The tradeoffs are just as concrete. The carrier with the strongest long-term growth often has the weakest early cash value, which is the price of admission for the long-term result. The carrier with the most flexible loan access may run smaller and carry lower financial ratings. The carrier with the biggest brand may have the least flexible design. And geography is a hard constraint: several leading carriers, including Penn Mutual, Lafayette Life, OneAmerica, and Foresters, do not sell core whole life in New York, so New York residents work from a shorter list of Guardian, MassMutual, New York Life, Ameritas, and Security Mutual.

Strength, flexibility, growth, access. You rarely get all four.

There is no single best company for infinite banking. There is a best company for your design, your horizon, and your state. Anyone who names one universal winner is selling that carrier.

09 / The fitWho is each type of carrier right for?

The right carrier maps to the buyer, not to a leaderboard. The entrepreneur with a 20-year horizon who values long-term growth and can tolerate lower early liquidity leans toward Penn Mutual. The buyer who wants maximum financial strength and a recognizable brand leans toward Guardian or New York Life. The buyer who needs the most early cash value leans toward Lafayette Life, Guardian, or Pan-American Life. The buyer who wants loan flexibility and the choice of recognition type leans toward Ameritas. The buyer who wants a carrier that fully embraces the strategy leans toward Security Mutual or Pan-American Life.

It is the wrong decision for anyone who is shopping on dividend rate alone, who needs the cash back in the first year or two, or who cannot name an activity that beats the loan cost. If you cannot identify a productive use for borrowed capital, no carrier on this list is right for you, and the strongest mutual in the country will not change that.

10 / Head to headThe major carriers, side by side

Compared on the dimensions that actually decide fit, the carriers separate quickly. The table below sets the leading mutuals against each other on ownership, recognition type, 2026 dividend, financial strength, and the single trait each is known for. Dividend rates are projected or recently declared, gross of internal costs, and not guaranteed.

| Carrier | Ownership | Recognition | 2026 Dividend (illustrative) | AM Best | Known for |

|---|---|---|---|---|---|

| Penn Mutual | Full mutual (1847) | Direct (0.65% / 0% spread) | ~6.1%, ~$300M | A+ | Strongest long-term growth |

| Guardian | Mutual (1860) | Direct (fixed 5%, yrs 1-10) | ~6.25%, ~$1.7B | A++ | Top financial strength, early cash value |

| MassMutual | Full mutual (1851) | Non-direct | ~6.6%, ~$2.9B | A++ | Strength, but anti-IBC stance |

| New York Life | Full mutual (1841) | Non-direct | ~6.4%, ~$2.78B | A++ | Largest brand, inflexible PUAs |

| Ameritas | Full mutual (1887) | Direct or non-direct (choice) | ~5.10% | A | Loan flexibility, NY available |

| Lafayette Life | Mutual holding (1905) | Non-direct | ~5.9%, ~$123M | A+ | Early cash value, IBC-aware |

| OneAmerica | Mutual holding (1877) | Non-direct | Not published | A+ | Hybrid LTC, fast loans |

| Foresters | Fraternal society (1874) | Non-direct | ~6.00% | A | Member benefits, 10-yr catch-up |

| Security Mutual | Full mutual (1886) | Non-direct | ~5.85% | A- | Pro-IBC niche, fast loans |

| Pan-American Life | Mutual | Direct | Varies | A | Openly endorses IBC, early cash value |

Strength. Guardian, MassMutual, and New York Life sit at the top of the financial-strength tables with A++ ratings and COMDEX scores near 100. Penn Mutual's A+ and 98-year A-or-better streak put it a half-step behind on the rating, ahead on long-term performance. Smaller carriers like Security Mutual carry lower ratings, which is a real consideration over a 30-year horizon.

Recognition and flexibility. The direct-recognition carriers, Penn Mutual, Guardian, and Pan-American Life, give you a known spread. Ameritas uniquely lets you choose. The rest are non-direct, crediting the full cash value regardless of loans. None of this is a ranking. It is a set of design inputs.

Geography and posture. New York residents work from Guardian, MassMutual, New York Life, Ameritas, and Security Mutual. And MassMutual's stance against infinite banking marketing, despite its strength, is the kind of posture that belongs in the decision even though it never shows up in a dividend comparison.

A composite: choosing between two carriers for the same buyer

Consider a 47-year-old real estate investor, preferred non-tobacco, planning to fund a policy at $73,400 per year and deploy capital into rental property. This is a representative composite, not a single named client. Two carriers made the short list: a high-early-cash-value carrier and Penn Mutual, with its lower early value and stronger long-term curve.

Through the first three years, cash value trails cumulative contributions on both designs, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction, at any carrier.

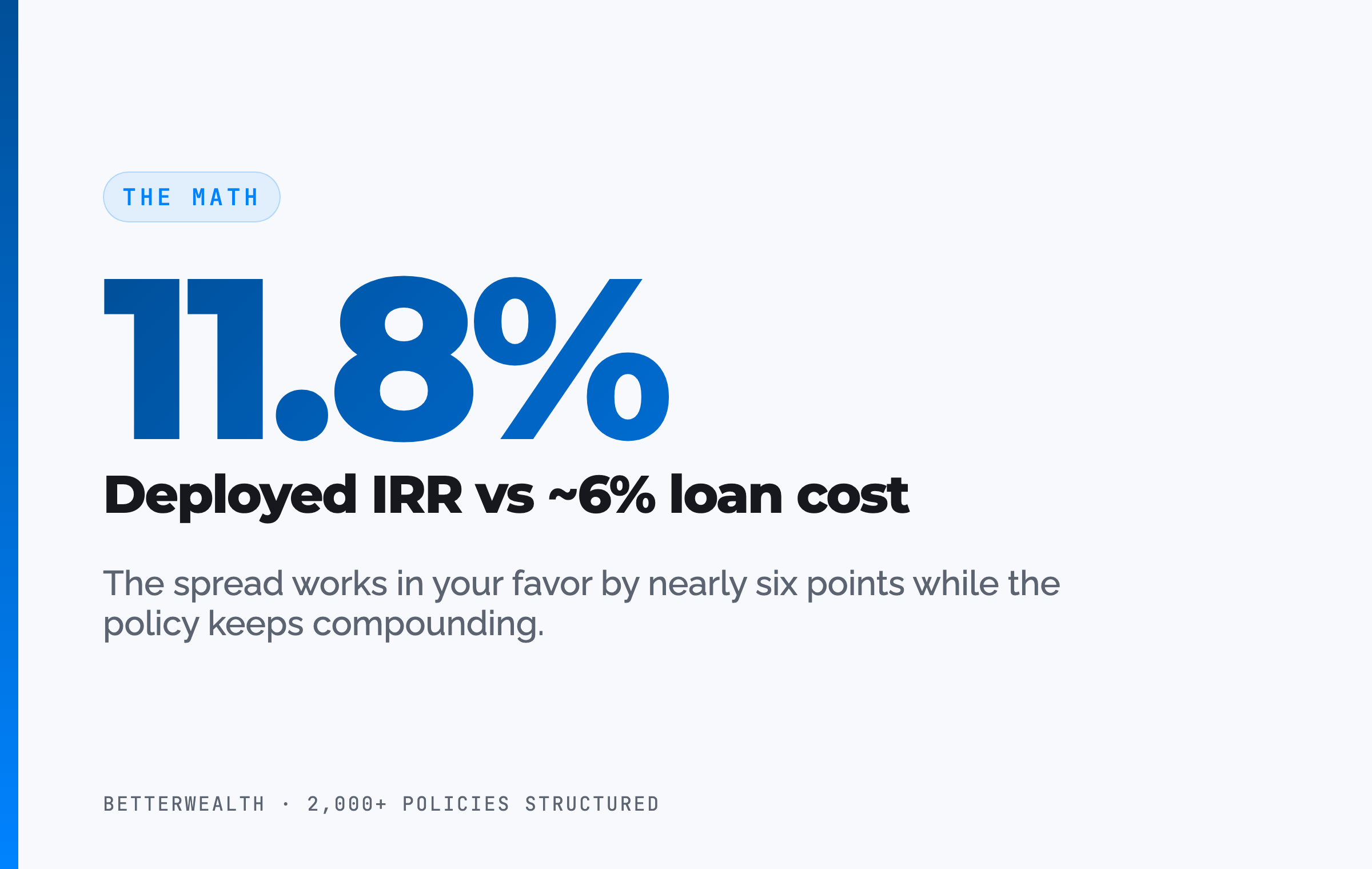

Because the investor's horizon was 20-plus years and the early liquidity was not needed until year six, we modeled Penn Mutual. In year six, with roughly $452,000 of accessible cash value, the investor borrowed $164,500 against the policy for a down payment on a duplex. The property returned an estimated 11.8% IRR. The loan cost was illustrative at around 6%, so the spread worked in the investor's favor by nearly six points, and the policy kept compounding on its full value the entire time. Repayment ran on a 38-month schedule funded by the property's own cash flow. Had the investor needed the cash in year two, the higher-early-value carrier would have been the right call instead. Same buyer, different horizon, different carrier.

One dollar. Two jobs. The carrier just has to let it happen.

The honest 30 minutes about which carrier fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you which carrier and design fit, or whether no policy fits at all. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQBest infinite banking companies, answered

What are the best companies for infinite banking?

The best companies for infinite banking are mutual or member-owned life insurers with long dividend histories, strong financial ratings, flexible paid-up additions, and a transparent loan structure. Penn Mutual, Guardian, MassMutual, New York Life, Ameritas, Lafayette Life, OneAmerica, Foresters, Security Mutual, and Pan-American Life are the carriers most often used. The right one depends on your policy design and time horizon, not the headline dividend rate.

What makes a life insurance company good for infinite banking?

A good infinite banking carrier is mutual or member-owned, has paid dividends for decades, holds a strong AM Best rating, supports a heavy paid-up additions rider so cash value builds early, and offers a loan structure that lets you borrow against the policy while it keeps compounding. Design flexibility matters more than the current dividend rate.

What is direct vs non-direct recognition?

Direct recognition means the carrier adjusts the dividend on the portion of cash value you have borrowed against. Non-direct recognition means the dividend is unchanged whether or not you have a loan outstanding. Neither is automatically better. Direct recognition with a guaranteed spread, like Penn Mutual's, can make distribution-phase math more predictable.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does the carrier with the highest dividend rate win?

No. The dividend rate is gross, before mortality and expense charges, and it is declared annually and not guaranteed. A carrier with a slightly lower dividend rate but better design flexibility, recognition structure, or long-term performance can outperform a higher headline rate. Compare designed illustrations, not dividend rates.

Which carriers are direct recognition and which are non-direct?

Penn Mutual, Guardian, and Pan-American Life are direct recognition. MassMutual, New York Life, Lafayette Life, OneAmerica, Foresters, and Security Mutual are non-direct recognition. Ameritas is unusual: it lets you choose a fixed direct-recognition loan or a variable non-direct loan, one at a time.

What are the best infinite banking companies in New York?

Several leading carriers do not sell their core whole life products in New York, including Penn Mutual, Lafayette Life, OneAmerica, and Foresters. Carriers available to New York residents include Guardian, MassMutual, New York Life, Ameritas, and Security Mutual.

Does MassMutual support infinite banking?

MassMutual is a strong mutual carrier, but it has taken a public and private stance against infinite banking marketing, and its paid-up additions riders are among the least flexible in the industry. It can still be designed for high cash value, but it is not positioned as an infinite banking carrier.

Does the carrier matter more than the policy design?

No. Policy design and funding discipline matter more than carrier choice. A well-designed policy at a strong carrier outperforms a poorly designed policy at the carrier with the highest dividend rate. Choose the carrier whose product can be designed for your horizon, then design it correctly.

How long until a whole life policy has usable cash value?

Cash value does not exceed cumulative contributions before year four on a healthy, well-designed policy, and break-even typically lands at year five or later. A heavily overfunded design with a strong paid-up additions rider has usable cash value to borrow against well before break-even.

- Nelson Nash, Becoming Your Own Banker. The origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law). The tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best. Financial strength ratings for every carrier referenced here.

- LIMRA. Life insurance industry data, including dividend and persistency benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states and works with every major carrier in this guide. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on which carrier and design fit your plan, book a discovery call. We will tell you if none of them do.

1. "What Is Infinite Banking?" (Pillar F3) → wired inline from the intro, the criteria section (H2 02), and the math context. Pillar must appear on every blog.

2. "How to Structure a Policy" (#9) → wired from the evaluation method section (H2 04).

3. "Paid-Up Additions (PUAs)" (#8) → wired from the criteria section (H2 02, the PUA bullet).

4. "Infinite Banking Pros and Cons" (#10) → wired from the "where people get this wrong" section (H2 07).

5. DOWN-LINKS: wire each of the ten carrier names in H2 05 to its individual carrier review once those URLs are live.