.png)

Pan-American Life ranks among the strongest niche carriers for infinite banking in 2026, pairing 85 to 92% first-year cash value with the simplest whole life product on the market and a flexible paid-up additions rider. The tradeoff is a smaller balance sheet, a higher lapse ratio, and no PUA catch-up provision.

A focused, openly pro-IBC carrier with very high early cash value, flexible PUAs, and the simplest product we have reviewed. It trades the scale, financial ratings, and long-term return of the Big Four mutuals for that focus, which fits mid-size premiums on a long horizon.

Pros

- 85 to 92% first-year cash value, cashflow or front-load

- Simplest whole life product reviewed (2 out of 10 complexity)

- Flexible PUA rider, anytime payments, $100/yr minimum

- Loan request about 10 days after funding

- Openly pro-IBC, credits Nelson Nash, 110+ years of dividends

- Variable loan rate, dividend adjusted on borrowed funds

Cons

- Smallest mutual holding company reviewed; COMDEX 78

- Lapse ratio 6.7% (2020 to 2025), second highest in the series

- Long-term IRR tends to trail the larger mutuals

- No PUA catch-up provision

- Roughly $100,000 annual PUA cap limits large policies

- Loans started by fillable PDF only, no online portal initiation

- Not available in New York

Most carrier comparisons start with the dividend rate and stop there. That is the wrong input to lead with, especially for a company that does not publish its dividend rate at all. The harder questions are whether a carrier will still be paying as illustrated in thirty years, whether its loan mechanics fit how you actually use capital, and whether its product can be designed to push cash value to the limit without becoming a Modified Endowment Contract.

The carrier matters far less than the design of the policy and your discipline in funding it. Pan-American Life, the company that bought and merged with Mutual Trust Life (MTL) in 2015, is a smaller carrier than the names most people recognize. It is also one of the most aggressively pro-IBC carriers in the market, and its product behaves in ways that surprise people who write it off for size alone.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and Pan-American earns a place on the short list for a specific buyer. This review covers what the company actually is after the merger, how its Horizon Value product behaves under both a cashflow and a front-load design, the math that decides whether borrowing against it makes sense, and the four honest tradeoffs that come with a niche carrier this size. We will also tell you who Pan-American is not for.

- Pan-American is the carrier that merged with MTL in 2015, carrying roughly 110 years of uninterrupted dividends through the Mutual Trust heritage.

- First-year cash value runs 85 to 92% on both cashflow and front-load designs, among the highest we review.

- It uses a variable loan rate and adjusts the dividend on borrowed funds. Carrier materials label the recognition type inconsistently, so confirm it before you design around it.

- The And Asset rule still governs: only borrow when the deployed return clears Pan-American's loan cost.

- Its limits are a smaller balance sheet, a 6.7% lapse ratio, a roughly $100,000 PUA cap, and no PUA catch-up provision.

- Pan-American sells in 49 states and Washington DC, but not in New York.

If you want to see the actual Horizon Value illustrations behind these numbers, Alden walks through both the cashflow and front-load designs on screen, including the year-by-year cash value:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves for a handful of structural questions, not for the headline dividend rate. The real questions are whether the company will still be paying dividends in forty years, whether its policy loan mechanics support how you plan to use capital, and whether its product can be designed to push cash value to the limit without tipping into a Modified Endowment Contract.

Pan-American answers those questions differently than a Big Four mutual does. It is smaller, it is niche, and it has built its product specifically for this strategy. That focus is both the reason to consider it and the reason to read the tradeoffs carefully, which is where this review spends most of its time.

"The product, its design, and your understanding are what matter most. The carrier choice among top mutuals is secondary." This is the lens we apply to every carrier, Pan-American included.

02 / The frameworkWhat does it mean to run infinite banking with Pan-American?

Running infinite banking with Pan-American means using a properly structured Horizon Value whole life policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. Pan-American leans into that heritage directly. Its client materials reference Nash and the book, and the company markets its own play on the concept. We respect that foundation. The And Asset builds on it with one rule the broader marketing of IBC does not enforce.

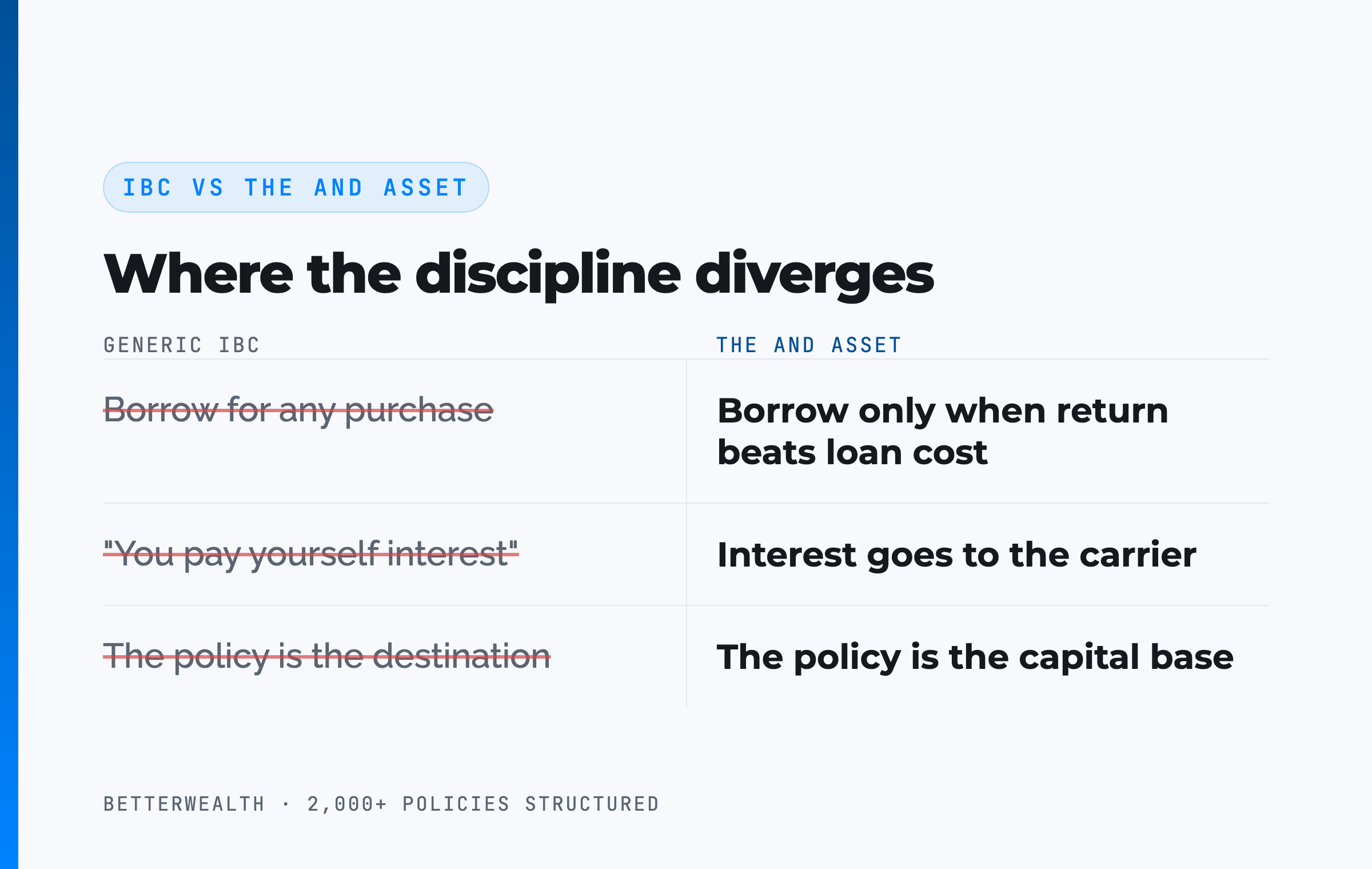

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to Pan-American. Your return is what your deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges.

The distinction matters with a carrier this pro-IBC, because the easiest mistake to make is to treat a policy that is good at early access as a reason to borrow casually.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the insurance company, and your return comes from what you deploy into.

03 / Financial strengthHow financially strong is Pan-American, and does its size matter?

Pan-American is financially sound but clearly smaller than the major mutuals, and the size matters for some buyers. It carries an AM Best rating of A (Excellent), a COMDEX score of 78, and a Weiss safety score of C (Fair). The Weiss scale is harsh, but a C still sits below New York Life's A-, the strongest Weiss mark in this series, so it belongs in the column of things to weigh, not wave away.

The merger shapes the picture. Mutual Trust was a niche IBC carrier with a loyal book. Pan-American brought a global footprint and a larger balance sheet. Neither company was in trouble. That said, a smaller mutual that runs a heavy IBC book carries a liquidity question worth asking, the same lens the carrier series applies to Security Mutual. Today 11.9% of Pan-American's portfolio is out on policy loans, a sign of its push into the IBC market and below Security Mutual's roughly 23%, but a number that rises as more policyholders borrow.

One figure deserves a flag. Pan-American's lapse ratio runs 6.7% from 2020 to 2025, against a 5.1% industry average, the second highest in the series. A merger usually lifts the lapse ratio for a stretch as policyholders react to the change in ownership. That context explains some of it, but the number is still above the field, and you should weigh it rather than dismiss it.

The company does not publish its dividend rate or its dividend dollars, which is frustrating for an analyst comparing carriers. The working estimate is roughly 6%, give or take 50 basis points. The dividend rate is gross. Your cash value grows at the dividend net of mortality and expense charges, which is the figure that actually compounds inside the policy. Any agent quoting a gross rate as your growth rate is either careless or selling.

04 / How it worksHow a Pan-American Horizon Value policy actually functions as an And Asset

A Pan-American policy functions as an And Asset through five mechanical steps, and the order matters. The product is Horizon Value, the simplest whole life chassis we have reviewed: plain whole life, simple term riders, and a paid-up additions rider with no gotchas. Here is the sequence we use when we structure one.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider toward its roughly $100,000 annual maximum. The PUA rider is the engine. Without it, this is an expensive death benefit. The base/PUA split is the single design decision that determines early cash value.

- Fund consistently. Choose a cashflow design (the same premium every year) or a front-load design (more in year one, then level). Pan-American supports long-pay funding, so a single product handles both early and later cash value well.

- Let the early years capitalize. First-year cash value lands at 85 to 92% of premium, which is high for the category. It climbs from there. The capitalization point, where a dollar of premium adds more than a dollar of cash value, arrives around years two to three.

- Borrow against the policy. A loan request can be made about 10 days after funding, collateralized by your cash value. Pan-American uses a variable loan rate and adjusts the dividend on the borrowed portion based on the outstanding loan. The death benefit and cash value still belong to you.

- Deploy and repay. Put the borrowed capital into an activity that beats Pan-American's loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

Because the early cash value is so high, the break-even point, where total cash value catches total contributions, arrives faster here than with most carriers, around year four to five on a well-designed cashflow policy for a healthy individual. Do not read that as a day-one break-even. Any illustration that shows cash value exceeding contributions in year one or two is selling you a fantasy.

Cashflow design versus front-load design

The two designs solve for different funding personalities. A cashflow design keeps the premium level. A front-load design front-ends a larger premium in year one, then drops to a level amount, buying more death benefit to stay under the MEC limit, which adds internal cost and pulls the front-load return slightly lower. On its best high-cash-value design, Pan-American's projected long-term IRR lands in the 3.4 to 4.7% range on current dividend projections, which trails the larger mutuals that lead the category long term. First-year cash value stays in the 85 to 92% range on both designs.

Neither design is "better." The cashflow version suits a steady, predictable premium. The front-load version suits someone who can put a larger sum in early and wants more of the death benefit funded up front. The right one depends on your cash flow, not on a single headline number. Ask to see both illustrations side by side before you decide.

For a deeper walkthrough of how the PUA rider and base premium split drives all of this, our breakdown of how cash value actually works covers the mechanics step by step:

Read next: How Whole Life Insurance Cash Value Works and How to Structure a Whole Life Policy.

Pan-American fits a specific person doing specific things.

It fits you if

- You want high early cash value and a simple product

- Your premium fits comfortably under the PUA cap

- You can name a use for capital that beats the loan cost

- You value a carrier that openly supports this design

It does not fit you if

- You want to fund well above $100,000 of PUA per year

- You live in New York

- You prioritize the highest financial ratings above all

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether Pan-American or another carrier fits your design. If you are in the second, we will tell you that too.

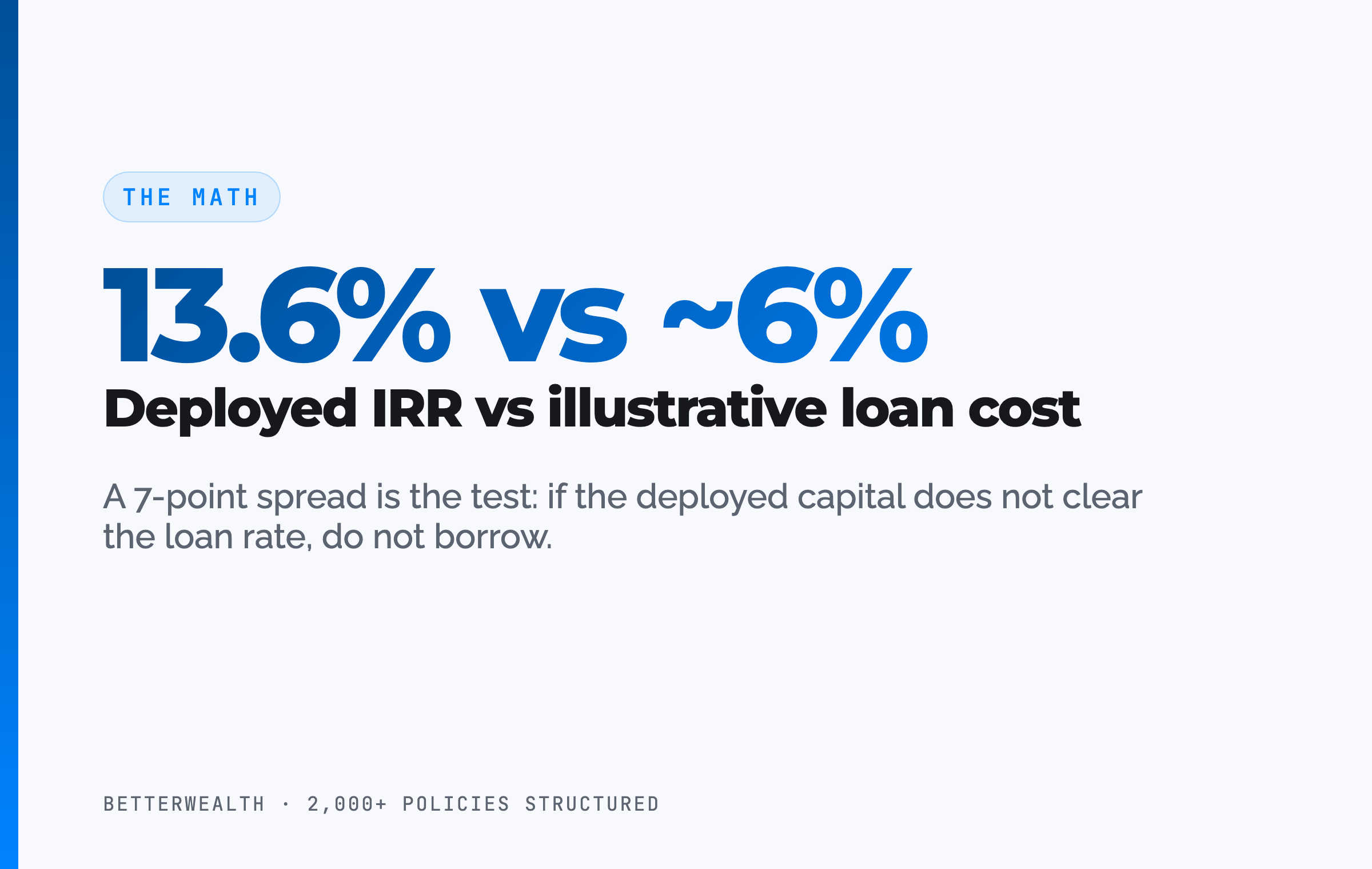

Book a Discovery Call05 / The mathDoes the return clear Pan-American's loan cost?

The return on whatever you deploy must exceed Pan-American's loan cost, or you should not borrow. This is the entire test. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with Pan-American, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. Your policy keeps compounding on its cash value, with the borrowed portion adjusted by Pan-American's variable loan rate. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread while the policy keeps growing. If it is lower, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

06 / Loan mechanicsHow Pan-American's loan recognition works

Pan-American uses a variable loan rate and adjusts the dividend it pays on the cash value you borrow against, rather than leaving it untouched. One note on labeling: the carrier's materials are not consistent. Some sources describe the system as non-direct recognition, while the product features describe a variable rate that adjusts the dividend based on outstanding loans, which is how direct recognition behaves. The classification matters less than the mechanism, so confirm the current label with the carrier before you design around it.

Either way, the loan interest is charged in advance within the policy year, then credited back as you repay, similar to Guardian. As a hypothetical, a $100,000 loan at a 5% rate would post a $5,000 interest charge up front. Pan-American does not publish a fixed loan rate, so treat any specific number as a variable to verify, not a constant.

Recognition gets called a dirty word in the insurance world. The reality is less dramatic. Depending on the rate environment, the dividend adjustment can move for you or against you, and across a full policy life it tends to roughly net out. It is a structural feature to understand, not a reason to rule the carrier out on its own.

Loan recognition gets treated like a dirty word. We have reviewed plenty of carriers that adjust the dividend on borrowed funds, and over the life of a policy it tends to roughly net out.

07 / Where it winsPUA flexibility, fast loans, and a simple product

Pan-American's strongest features are paid-up additions flexibility, fast loan access, and a product simple enough that you can actually understand what you own. These are the things that shape your experience for decades, long after the dividend comparison is forgotten.

Paid-up additions flexibility

Pan-American's PUA rider allows anytime payments. As long as you pay at least the $100 annual minimum, you can fund the rider anywhere between that minimum and your underwritten maximum, at any point in the policy year, in any number of payments. The rider stays in force on the $100 minimum alone. The ceiling is roughly $100,000 of PUA per year without an underwritten exemption, which is why this is a mid-size-premium carrier rather than a large-case one. The one real gap is the lack of a catch-up provision: miss PUA premium, and you cannot backfill it later. That single feature is what keeps it from our top PUA spot.

Fast loan access

A loan request can be made about 10 days after funding, among the fastest in the series and tied with Security Mutual. The catch is the mechanics: loans are initiated by a fillable PDF form only, not through an online portal, though repayments do run through the portal. For a niche IBC carrier, an online loan request is the obvious next upgrade.

A simple product and a useful rider

Horizon Value is the simplest whole life product we have reviewed, a 2 out of 10 on our complexity scale. Plain whole life, simple term riders, no traps on the PUA. Pan-American also offers a waiver of premium that can extend to the PUA rider, covering up to $15,000 of PUA per year if you become disabled, so the asset keeps building even when a paycheck stops. There is a Max Dividend Accumulation Option that scales the dividend back if a rapidly rising dividend would otherwise push a maximum-funded policy toward MEC. Simple chassis, real protections.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare carriers like Pan-American, Penn Mutual, and Guardian. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the four honest tradeoffs

Pan-American's benefits come with four tradeoffs that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, size. Pan-American is the smallest mutual holding company in this series, larger than Security Mutual but well behind Mass Mutual and New York Life, and its COMDEX of 78 reflects that. Second, the lapse ratio: 6.7% from 2020 to 2025, the second highest we have seen, softened but not erased by the post-merger context. Third, the roughly $100,000 PUA cap, which makes it the wrong carrier for anyone wanting to put millions of premium per year to work. Fourth, no PUA catch-up provision, so missed funding cannot be backfilled, where some other carriers do offer that option. A fifth point sits in the background: its long-term IRR tends to lag the larger mutuals, so the early-cash-value edge narrows the longer you hold.

Against those tradeoffs sits a competitive product for its size. Side by side with other small IBC carriers like Ameritas, OneAmerica, and Security Mutual, Pan-American's 85 to 92% first-year cash value holds up well. It runs close to the larger Lafayette Life, which edges it slightly on early cash value. For a carrier this size, that is a strong showing on day-one access.

Small company. Strong early-cash-value product.

Size does not always matter, but sometimes it should. If you want to put millions a year into PUAs, Pan-American is simply not the carrier you would consider.

09 / The fitWho is Pan-American right for, and who isn't it?

Pan-American is right for the entrepreneur or high-income earner funding a mid-size premium who wants high early cash value, a simple product, and a carrier that openly supports this design. It fits the value creator who can name a productive use for borrowed capital and who is comfortable with a smaller, niche mutual rather than a household name.

It is the wrong carrier for someone funding well above the PUA cap, someone who prioritizes the highest financial ratings above every other factor, or anyone in New York. And if you cannot name an activity that beats the loan cost, no carrier is right for you, and Pan-American will not change that.

10 / Head to headPan-American against the alternatives

Compared to the capital tools entrepreneurs actually use, a Pan-American And Asset policy trades day-one access for control, tax treatment, and uninterrupted compounding. The table sets it against a HELOC, a 401(k), and a taxable brokerage account on the four dimensions that matter for capital strategy.

| Dimension | Pan-American And Asset | HELOC | 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Growth | Compounds on cash value, net of internal costs, even while borrowed against | None (it is a credit line, not an asset) | Market growth, tax-deferred | Market growth, taxed annually on gains |

| Liquidity | Loan request about 10 days after funding; 85 to 92% of premium accessible early | Fast once approved, but can be frozen or called | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

| Tax treatment | Policy loans are not taxable income under IRC 7702 | Interest may be deductible in limited cases | Deferred now, taxed as ordinary income later | Capital gains and dividends taxed yearly |

| Control | Loan cannot be called; you set repayment terms | Lender controls terms and can revoke access | Access rules set by Congress, not you | Full control, but no leverage feature built in |

Growth. A Pan-American policy keeps compounding on its cash value while you borrow, which a HELOC cannot do because a credit line is not an asset. That uninterrupted compounding is the structural feature that lets the same dollar work in two places.

Liquidity. Pan-American's early cash value is its headline strength, with 85 to 92% of premium accessible in year one and a loan request available about 10 days after funding. A HELOC can be faster on paper, but a HELOC can be frozen exactly when you need it, as thousands of investors learned in 2020. The policy loan cannot be called.

Tax and control. Policy loans are not taxable income under Section 7702, and the loan cannot be called. A 401(k) defers tax but restricts access until 59½ under rules set by Congress. The And Asset trades the highest possible early liquidity for control and tax treatment you keep.

A composite: the business owner who deployed at year eight

Consider a 43-year-old business owner, preferred non-tobacco, funding a Pan-American Horizon Value policy at roughly $40,000 per year on a cashflow design. This is an illustrative composite to show the mechanics, not a single named client or a specific illustration on file. Treat the figures as round, directional, and dependent on the actual design.

Through the first few years, cash value trails cumulative contributions, exactly as a real policy should, even on a high-early-cash-value carrier. Around year two to three, each premium dollar starts adding more than a dollar of cash value. Total cash value tends to cross total contributions around year four to five, not before. Any illustration showing a year-one or year-two break-even is marketing fiction.

Say the owner waits until year eight, when a meaningful balance has built, and borrows against the policy to buy revenue-producing equipment. If the equipment returns more than the policy loan cost, the spread works in the owner's favor, and the policy keeps compounding on its full cash value the entire time. If the deployed return cannot clear the loan rate, the right move is not to borrow. The exact dollars, rates, and repayment schedule depend on the design and the deal, so build the case off your own illustration, not a round number on a page.

One dollar doing two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. We have seen this strategy work exactly as designed, and we have seen it fail. On a discovery call, a practitioner looks at your specific situation and tells you whether a Pan-American policy, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQPan-American infinite banking questions

Is Pan-American good for infinite banking?

Pan-American Life is one of the strongest niche carriers for infinite banking in 2026, with 85 to 92% first-year cash value, a flexible paid-up additions rider, and the simplest whole life product on the market. Its limits are a smaller balance sheet, a higher lapse ratio, and no PUA catch-up provision, so it fits mid-size premiums on a long horizon.

Is Pan-American the same as MTL or Mutual Trust?

Pan-American Life is the company that bought and merged with Mutual Trust Life (MTL) in 2015. Pan-American dates to 1911 and Mutual Trust to 1904, and the combined book carries roughly 110 years of uninterrupted dividends. Many legacy MTL policies and producers now sit under the Pan-American banner.

Is Pan-American direct or non-direct recognition?

Carrier materials are not consistent on the label. Some Pan-American sources describe the loan system as non-direct recognition, while its product features describe a variable loan rate that adjusts the dividend based on outstanding loans, which is how direct recognition behaves. What is verifiable is the mechanism: a variable loan rate, with the dividend on borrowed funds adjusted. Confirm the current classification with the carrier before you design around it.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is Pan-American available in New York?

No. Pan-American does not sell its whole life products in New York. It operates in 49 states plus Washington DC. New York residents need a different carrier for an And Asset policy.

What is Pan-American's dividend rate for 2026?

Pan-American does not publicly disclose its 2026 dividend dollar amount or dividend interest rate. The rate is estimated at roughly 6%, give or take 50 basis points. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges, and dividends are not guaranteed.

What is Pan-American's best product for infinite banking?

Pan-American's Horizon Value whole life is the product used for And Asset and infinite banking style designs. It is the simplest whole life product reviewed in the carrier series, built with a flexible paid-up additions rider and simple term riders.

Does Pan-American have a PUA catch-up provision?

No. Pan-American's paid-up additions rider has no catch-up provision, so missed PUA premium cannot be backfilled in later years. The rider is otherwise flexible, with anytime payments between a $100 annual minimum and the underwritten maximum, up to roughly $100,000 of PUA per year.

How fast can you access cash from a Pan-American policy?

Pan-American allows a policy loan request about 10 days after funding, among the fastest in the industry. Loans are initiated by a fillable PDF form only, not yet through an online portal, while repayments go through the portal.

Pan-American vs Penn Mutual or Guardian for infinite banking?

Pan-American is a smaller, openly pro-IBC carrier with very high early cash value and the simplest product, but lower financial ratings and a $100,000 PUA cap. Penn Mutual leads long-term IRR, and Guardian leads financial strength at COMDEX 100. The right carrier depends on policy design and your time horizon, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept Pan-American references in its client materials.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, Pan-American's A (Excellent) financial strength rating.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- Pan-American Life, product and company information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Specializes in policy structure and carrier comparisons across the IBC series, and walks through the Pan-American Horizon Value illustrations in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a Pan-American policy fits your plan, book a discovery call. We will tell you if it does not.