.png)

Ameritas is a solid, IBC-friendly carrier for infinite banking in 2026, offering a rare choice between a 4% fixed loan and a variable loan, liberal underwriting, and coverage in all 50 states. The tradeoff is a lower COMDEX of 83 and a mandatory PUA step-down that makes it a short-pay carrier, not a long-term overfunding one.

A well-rounded mutual with genuinely useful flexibility, held back by a lower safety score and a paid-up additions schedule that punishes long-term funders. The 4% fixed loan and liberal underwriting are the reasons it makes our short list for the right client.

Pros

- Choice of a 4% fixed loan or a variable loan, switchable over time

- Liberal underwriting that often lands a better health rating

- All 50 states, including New York

- Care4Life: terminal, chronic, and critical illness riders

- Loans in roughly 21 days; 115 years of dividends

Cons

- Mandatory PUA step-down limits long-term overfunding

- Long-term IRR on the lower end at roughly 3.0 to 4.4%

- COMDEX of 83, below most carriers we use

- Does not publish total dividend dollars paid

- Dated illustration software; step-down can confuse buyers

Choosing an insurance carrier for a multi-decade capital strategy is the wrong place to start, and it is exactly where most people start. They line up dividend rates, pick the highest number, and assume they have made the right call. The dividend rate is one input. It tells you almost nothing about whether a policy will function as a capital base for the next thirty years.

With Ameritas, the carrier choice comes down to a funding-style question, not a dividend-rate question. Ameritas is a capable, IBC-aware mutual. It is also built around a paid-up additions rider that steps down on a fixed schedule, which makes it a different animal than a carrier you plan to overfund for decades.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and Ameritas earns a spot on the short list for a specific kind of funder. This review covers what the company actually is, how its Access Whole Life product behaves under both a cashflow and a front-load design, the unusual fixed-or-variable loan feature, the math that decides whether borrowing makes sense, and the real tradeoffs, including the ones that rule it out for some buyers. We will also tell you who Ameritas is not for.

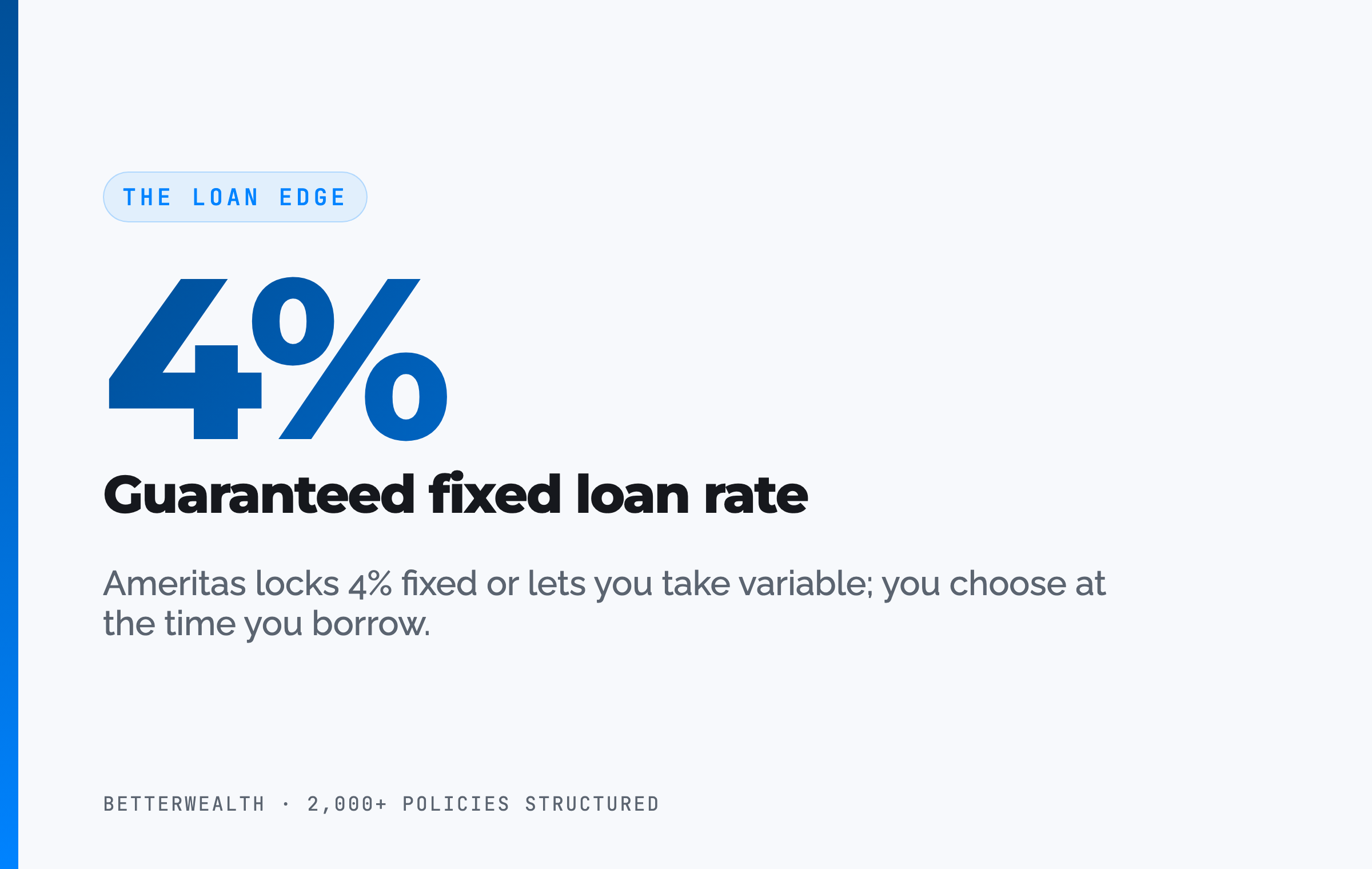

- Ameritas lets you choose a fixed-rate loan at a guaranteed 4% or a variable-rate loan, and switch between them over time.

- Its PUA rider steps down on a mandatory schedule, so it is built for short-pay funding, not decades of overfunding.

- Long-term IRR runs roughly 3.0 to 4.4%, on the lower end of the carriers we work with.

- Ameritas writes in all 50 states, including New York, and pays New York policyholders a separate dividend.

- Liberal underwriting often secures a better health rating than peers will offer the same applicant.

- The And Asset rule still governs: only borrow when the deployed return clears Ameritas's loan cost.

If you want to see the actual policy illustrations behind these numbers, Alden walks through both the cashflow and front-load designs on screen, including the PUA step-down that shapes the whole product:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves for a handful of structural questions, not for the headline dividend rate. The real questions are whether the company will still be paying dividends in forty years, whether its loan mechanics support how you plan to use capital, and whether its product can be designed to push cash value to the limit without tipping into a Modified Endowment Contract.

Ameritas answers the longevity question well. A company founded in 1887, fully mutual, with dividends paid every year since 1908, is not a fly-by-night operation. The harder questions are about mechanics and funding fit, which is where this review spends most of its time, because Ameritas has one design quirk that decides whether it belongs in your plan.

"We are not battling over who has the higher dividend rate. The product, its design, and your understanding are what matter most.", Alden Armstrong

02 / The frameworkWhat does it mean to run infinite banking with Ameritas?

Running infinite banking with Ameritas means using a properly structured Ameritas whole life policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

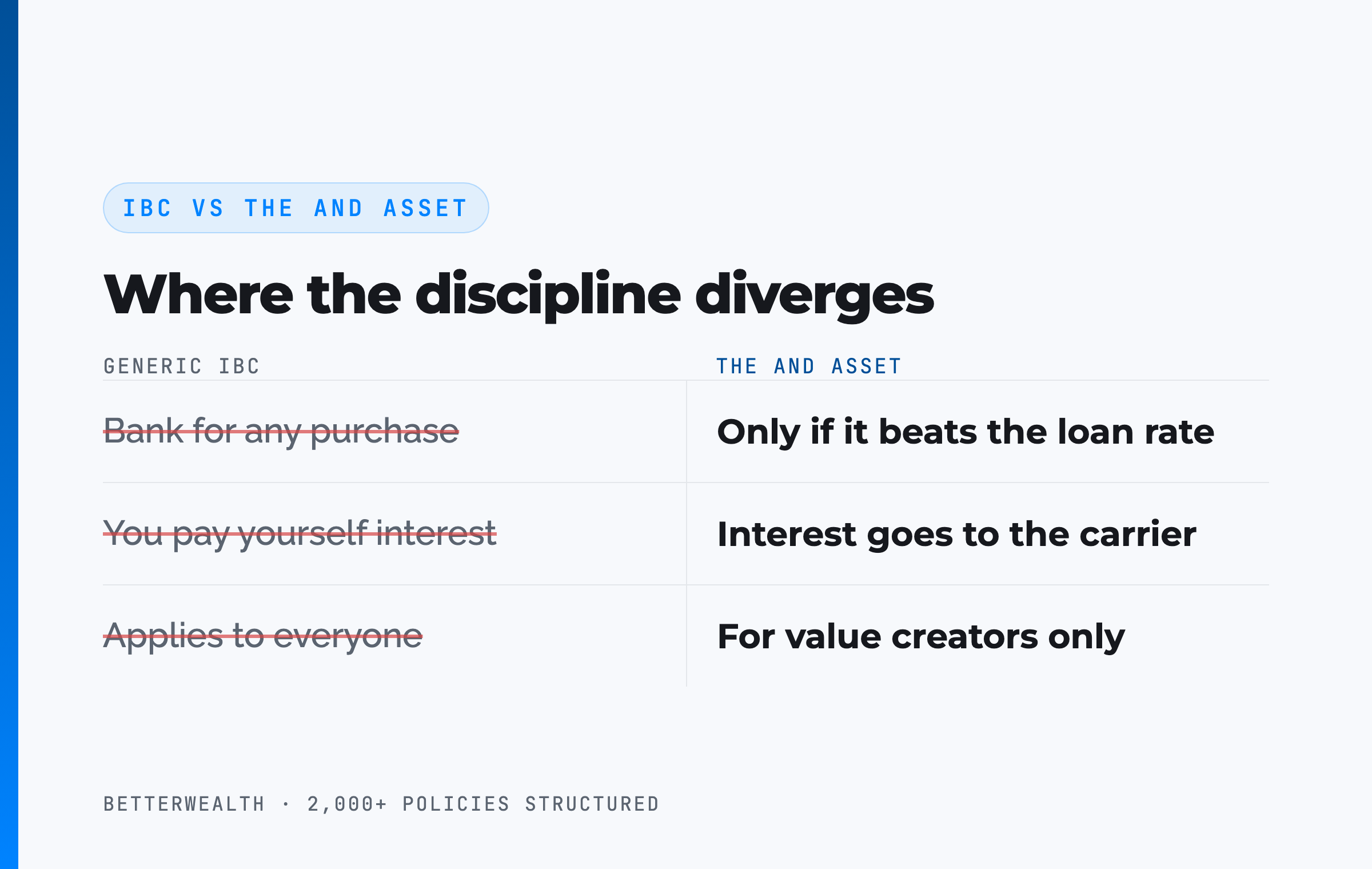

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to Ameritas. Your return is what the deployed capital earns elsewhere while the policy keeps compounding, net of mortality and expense charges.

The distinction matters here because Ameritas's 4% fixed loan changes the math. A guaranteed low loan cost widens the spread on a disciplined deployment, and it tempts the undisciplined into borrowing for things that never clear the bar.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the insurance company, and your return comes from what you deploy into.

03 / Financial strengthHow safe is Ameritas for a 30-year strategy?

Ameritas is financially sound but carries the lowest safety score of the carriers we regularly use, and that is worth saying plainly. Its AM Best rating is A (Excellent), and it is a 100% mutual owned by policyholders. Its COMDEX, the composite of five rating agencies scored out of 100, sits at 83. Most carriers in this series score 93 or higher.

Size the gap honestly. A score of 83 is above average, and a well-run smaller mutual can land below a giant partly because of scale. But the source carrier review flags the lower rating as a real consideration, not a footnote, and 83 is not the 95-to-100 range you get from Guardian or New York Life. For a thirty-year commitment, that difference deserves a conscious decision rather than a shrug.

Two other numbers round out the picture. Ameritas's lapse ratio runs 5.92% from 2020 to 2025, slightly above the 5.1% industry average AM Best reported as of 2023. A higher lapse ratio than the industry norm points to roughly average, arguably slightly below-average, policyholder persistency, not a standout. And Ameritas is unusual in that it publishes its dividend interest rate, 5.1% for 2026, but not the total dividend dollars it pays out, which some view as an unreasonable lack of transparency. The dividend rate is gross. Your cash value grows at the dividend net of mortality and expense charges, not the headline 5.1%.

04 / How it worksHow an Ameritas policy actually functions as an And Asset

An Ameritas policy functions as an And Asset through five mechanical steps, and the order matters. The product is Access Whole Life, designed for maximum cash value rather than maximum death benefit, typically on a 40/60 base-to-PUA split. Here is the sequence we use.

- Structure for cash value. Build a 40/60 design: 40% of premium toward base, 60% toward the paid-up additions rider. The PUA rider is the engine. Ameritas lets you fund up to 100% more PUA than illustrated under the MEC limit, which is real room to grow.

- Respect the step-down. Ameritas reduces PUA capacity on a fixed schedule, so the policy is built for a short-pay. Fund heavily in the early years rather than planning to overfund level for decades. The carrier will not even illustrate level long-term PUA.

- Let the early years capitalize. First-year cash value on a short-funded design lands around 80 to 90%, per Ameritas illustrations. Stretch the funding over more years and the early cash value drops, because the design needs a higher base premium. Do not expect to break even on day one.

- Choose your loan, then borrow. Loans are available about 21 days after funding. Choose a 4% fixed (direct) loan or a variable (non-direct) loan, decided at the time you borrow, not at issue. Smaller loans go through the portal, larger loans through your agent.

- Deploy and repay. Put the borrowed capital into an activity that beats the loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

On a well-designed Ameritas cashflow policy, the capitalization point, where a dollar of premium adds more than a dollar of cash value, arrives around year four or five. Break-even, where total cash value catches total contributions, typically lands around year eight. Any illustration showing year-two break-even is fiction.

Cashflow design versus front-load design

The two designs solve for different funding personalities, and with Ameritas they share the same constraint. A cashflow design keeps the premium level. A front-load design front-ends a larger premium in the first year or two, then settles into a lower ongoing premium. Both reach roughly 80 to 90% early cash value when you short-fund them, and stretching either over more years raises the base premium and pulls down that early cash value. The front-load typically capitalizes a touch sooner because the money goes in earlier, but the difference is modest.

Here is the catch that makes Ameritas different. Both designs run into the same PUA step-down, so neither is built for funding the same policy hard for decades. Short-pay is the carrier's native habitat.

Short and heavy, not long and level.

For a deeper walkthrough of how the base premium and PUA split drives early cash value, we broke down policy structure here:

Ameritas fits a specific person doing specific things.

It fits you if

- You will fund hard for a short window, then let it ride

- You want the 4% fixed loan or the fixed-or-variable choice

- A liberal underwriter could win you a better health rating

- You can name a use for capital that beats the loan cost

It does not fit you if

- You plan to overfund the same policy for 20-plus years

- You want the highest possible COMDEX safety score

- You want a savings account, not a capital strategy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether Ameritas or another carrier fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the return clear Ameritas's loan cost?

The return on whatever you deploy must exceed Ameritas's loan cost, or you should not borrow. This is the entire test. Ameritas is unusual because you can lock a 4% fixed loan rate, guaranteed never to increase on current products, or take a variable rate instead. Treat the 4% as illustrative of today's offering and verify it at the time you borrow, because loan terms vary by carrier and period.

Here is the structure of the decision. You borrow at the loan rate. Your policy keeps compounding on its full cash value, including the borrowed portion. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the policy has done two jobs with one dollar. If it is lower, you have borrowed money to lose money slowly.

The 4% fixed option is genuinely useful, with one honest caveat from the source review. The insurance company does not lose. If rates spike the way they did in the early 1980s and you are borrowing at a locked 4%, the carrier can adjust the dividend it pays on the loaned portion. The fixed loan rate is a real edge. It is not a free lunch.

If the deal does not clear the loan rate, do not borrow.

06 / Loan recognitionWhy does the fixed-or-variable choice matter?

Ameritas is the rare carrier that gives you both direct and non-direct recognition, and you decide which one at the time you take each loan. It does not use those labels. In practice, the fixed-rate loan, at 4%, behaves like direct recognition, and the variable-rate loan, currently 5.80% and tied to the Moody's Corporate Bond Yield Average, behaves like non-direct recognition. The only other carrier we work with that offers a fixed direct-recognition loan is Guardian, at 5% for the first ten years. Ameritas comes in lower at 4%.

The whole direct-versus-non-direct debate is, in our view, mostly a wash over a full rate cycle. If you could predict 30 years of interest rates, you could prove which one wins. Nobody can. When rates move, one method beats the other in a given year, and over time they tend to even out. What Ameritas does is hand you the choice instead of locking you into one.

The one rule on switching

You can move between fixed and variable year to year, but the loan types are exclusive: you cannot hold a fixed loan and open a variable one at the same time. Pay off the existing loan, then choose again. The practical version is simple. You do not commit at issue, and as long as you carry no outstanding loan, you pick the rate that fits the moment when you borrow.

Direct versus non-direct is not the holy war the forums make it. Ameritas just gives you both and lets you decide at the moment you borrow.

07 / Where it winsLiberal underwriting, Care4Life, and fast access

Ameritas's strongest features are the ones that rarely show up in an IRR comparison: forgiving underwriting, a triple set of living-benefit riders, and speed to cash. These shape your experience for thirty years, long after the dividend comparison is forgotten.

Liberal underwriting

Ameritas underwrites more liberally than most top mutuals. We have had clients declined or rated by one carrier and picked up by Ameritas at preferred. For a strategy that depends on actually getting the policy in force at a good rate, that matters. The flip side is real, and the source carrier review names it directly: Ameritas's overall financial stability paired with more liberal underwriting is exactly what gives some clients and agents pause, and a more liberal underwriter takes on risk other carriers pass on. That tradeoff is part of the same picture as the lower COMDEX. It is a genuine benefit when it wins a client a better rating, and a fair reason for caution if a top safety score is what you are after.

Care4Life living benefits

Ameritas is the only whole life carrier we work with that attaches all three accelerated death benefit riders: terminal illness, chronic illness, and critical illness. Most carriers offer the first one, many add the second. Ameritas adds critical illness on top, giving you three ways to access policy values under defined health circumstances. It is hard to price into an illustration. It is easy to value when you need it.

Fast access and the Ethos arm

Loans are available roughly 21 days after funding, faster than the 30 to 45 days common at larger carriers, with daily interest accrual you can track in the portal. Ameritas also owns Ethos Life, a simplified-issue arm that can issue whole life, term, and universal life with no medical exam and limited underwriting. Simplified issue costs more for the same rating, so it is a convenience trade, not a free upgrade. Ameritas is also one of only three carriers we work with whose disability waiver of premium can cover scheduled paid-up additions.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use when we compare carriers like Ameritas, Penn Mutual, and Guardian. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the honest tradeoffs

Every carrier has tradeoffs, and Ameritas's disqualify it for some buyers. Here they are, plainly.

First, the PUA step-down. Capacity drops on a mandatory schedule: 25 times base premium in year one, 10 times through year five, 7.5 times through year ten, 5 times through year fifteen, and 2 times after year sixteen. Most carriers let you underwrite consistent PUA for as long as you want. Ameritas will not even illustrate it. If your plan is to overfund the same policy for decades, this is the wrong carrier. Second, long-term IRR runs roughly 3.0 to 4.4%, on the lower end of the field, below carriers like Penn Mutual. Third, the COMDEX of 83 sits below the 93-plus most of our carriers carry. Fourth, Ameritas does not publish its total dividend dollars, which some view as an unreasonable lack of transparency, and it pays New York clients a different dividend than the other 49 states.

Two more points of friction the sales pitch skips. The current declared dividend dollar amount is not disclosed or independently verifiable, so you are trusting the published rate without the full picture behind it. And from the agent side, Ameritas's illustration software is dated and a bit clunky, while the PUA step-down itself can confuse buyers who expected to fund level for life. None of this is disqualifying on its own, but it is part of an honest read.

This is a short-pay product, and the step-down is the proof.

If you want to overfund a single policy for as long as possible, this is not the right product. It was designed for short funding, and the step-down proves it.

09 / The fitWho is Ameritas right for, and who isn't it?

Ameritas is right for the entrepreneur or high-income earner who will fund a policy hard for a short window and values the 4% fixed loan, the fixed-or-variable choice, and liberal underwriting. It fits the value creator who wants living-benefit riders, who may need a forgiving underwriter to land a good rating, and who can identify productive uses for borrowed capital. It is also a sensible pick for a New York resident, since many strong carriers cannot write there.

It is the wrong carrier for someone who plans to overfund the same policy for 20-plus years, who wants the highest possible safety score, or who is looking for a savings vehicle rather than a capital base. If you cannot name an activity that beats the loan cost, no carrier is right for you, and Ameritas will not change that.

10 / Head to headAmeritas against Penn Mutual and Guardian

Against the two carriers it most often gets compared to, Ameritas trades long-term growth for a lower fixed loan rate and friendlier underwriting. The table sets it beside Penn Mutual and Guardian on the dimensions that decide a carrier for The And Asset. For the wider field, see our ranking of the best life insurance companies for infinite banking.

| Dimension | Ameritas | Penn Mutual | Guardian |

|---|---|---|---|

| Loan recognition | Both: 4% fixed (direct) or variable (non-direct), your choice | Direct, 0.65% spread yrs 1-10, 0% yrs 11+ | Direct, fixed 5% for 10 years |

| Year-1 cash value (cashflow) | 80 to 89% | 77 to 87% | 80 to 88% |

| Long-term IRR | ~3.0 to 4.4% | ~4.2 to 5.3% | ~3.5 to 4.5% |

| Long-term overfunding | Limited by mandatory PUA step-down | Strong, funds 10 to 35 years | Limited without Q-Term rider |

| New York | Yes (separate NY dividend) | No | Yes |

| Financial strength (COMDEX) | 83 | 93 | 100 |

Loan flexibility. Ameritas is the only one of the three that lets you pick fixed or variable at the time you borrow, and its 4% fixed beats Guardian's 5%. If a guaranteed low loan rate is your priority, Ameritas leads here.

Long-term growth. Penn Mutual, with a roughly 4.2 to 5.3% IRR and a decades-long funding window, beats Ameritas for anyone overfunding a single policy for the long haul. This is the gap that keeps Ameritas off the top of the list for long-term funders.

Access and underwriting. Ameritas writes in New York where Penn Mutual cannot, underwrites more liberally than either, and funds loans in about 21 days. The cost of that flexibility shows up in the lower COMDEX of 83.

An illustrative composite: the contractor who used the 4% fixed loan

Consider a 43-year-old contractor, preferred non-tobacco, funding an Ameritas Access Whole Life policy at $50,000 per year on a 40/60 cashflow design: $20,000 base and $30,000 PUA. This is a representative composite to show how the mechanics behave, not a single named client and not a guarantee. Your own numbers come from a real illustration run on your age, health, and funding.

Through the first three to four years, cash value trails cumulative contributions, exactly as a real policy should. Around year four, each premium dollar starts adding more than a dollar of cash value. Around year eight, total cash value crosses total contributions. Any illustration showing year-two break-even is marketing fiction.

Once the policy has meaningful accessible cash value, the contractor borrows against it at the 4% fixed rate to buy a piece of revenue-producing equipment. As long as the equipment's return clears that 4% cost, the spread works in the owner's favor and the policy keeps compounding on its full value the entire time, with repayment funded by the equipment's own cash flow.

The downside case matters just as much. If that equipment underperforms and returns less than the 4% loan cost, the spread runs the other way: the loan costs more than the deployment earns, and the right move is not to borrow at all. The strategy only works when the deployed return clears the loan rate, and no fixed loan rate, however low, changes that test.

One dollar doing two jobs is the whole point of the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether an Ameritas policy, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQAmeritas infinite banking questions

Is Ameritas good for infinite banking?

Ameritas is a solid carrier for infinite banking in 2026, with 115 years of dividends, a rare choice between a 4% fixed loan and a variable loan, liberal underwriting, and availability in all 50 states. Its weaknesses are a lower COMDEX of 83 and a PUA step-down that makes it best for short-pay funding rather than decades of overfunding.

Is Ameritas direct or non-direct recognition?

Ameritas is both. It lets you choose a fixed-rate loan (functioning like direct recognition) at a guaranteed 4% on its current whole life products, or a variable-rate loan (functioning like non-direct recognition) that does not change the declared dividend. You can switch between the two over time, but you can only have one loan type outstanding at once.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is Ameritas available in New York?

Yes. Ameritas operates in all 50 states, and Ameritas Life Insurance Corp. of New York can write policies for New York residents. Ameritas pays a separate dividend to New York policyholders than it pays in the other 49 states.

What is Ameritas's dividend rate for 2026?

Ameritas's 2026 dividend interest rate is 5.1%. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges, and dividends are declared annually and are not guaranteed. Ameritas is one of the few mutuals that publishes its dividend rate but not the total dollar amount paid.

What is Ameritas's best product for infinite banking?

Ameritas Access Whole Life, designed for maximum cash value on a 40/60 base-to-PUA split, is the product used for And Asset and infinite banking style designs. It pairs a heavy paid-up additions rider with a fixed loan option that few carriers offer.

What is the Ameritas PUA step-down?

Ameritas reduces how much you can pay into the paid-up additions rider on a fixed schedule: 25 times base premium in year one, 10 times through year five, 7.5 times through year ten, 5 times through year fifteen, and 2 times after year sixteen. Unlike most carriers, Ameritas mandates the step-down and will not even illustrate level long-term PUA, so it is built for short-pay funding.

How fast can you access cash from an Ameritas policy?

Ameritas allows policy loans roughly 21 days after initial funding, faster than the 30 to 45 days common at larger carriers. Smaller loans can be initiated through the online portal, larger loans go through your agent or the carrier, and interest accrues daily on the balance.

What is Care4Life from Ameritas?

Care4Life is Ameritas's set of accelerated death benefit riders. Ameritas is the only whole life carrier BetterWealth works with that attaches all three: terminal illness, chronic illness, and critical illness. These let you access policy values early under defined health circumstances.

Ameritas vs Penn Mutual or Guardian for infinite banking?

Ameritas offers a unique 4% fixed loan option and liberal underwriting but a lower COMDEX of 83 and long-term IRR of roughly 3.0 to 4.4%. Penn Mutual is direct recognition with stronger long-term IRR of 4.2 to 5.3%, and Guardian is direct recognition with a fixed 5% loan for the first 10 years and high early cash value. The right carrier depends on policy design and your funding horizon, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, Ameritas's A (Excellent) financial strength rating.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- Ameritas, declared dividend rate and product information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Specializes in policy structure and carrier comparisons across the IBC series, and walks through the Ameritas illustrations and PUA step-down in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether an Ameritas policy fits your plan, book a discovery call. We will tell you if it does not.