.png)

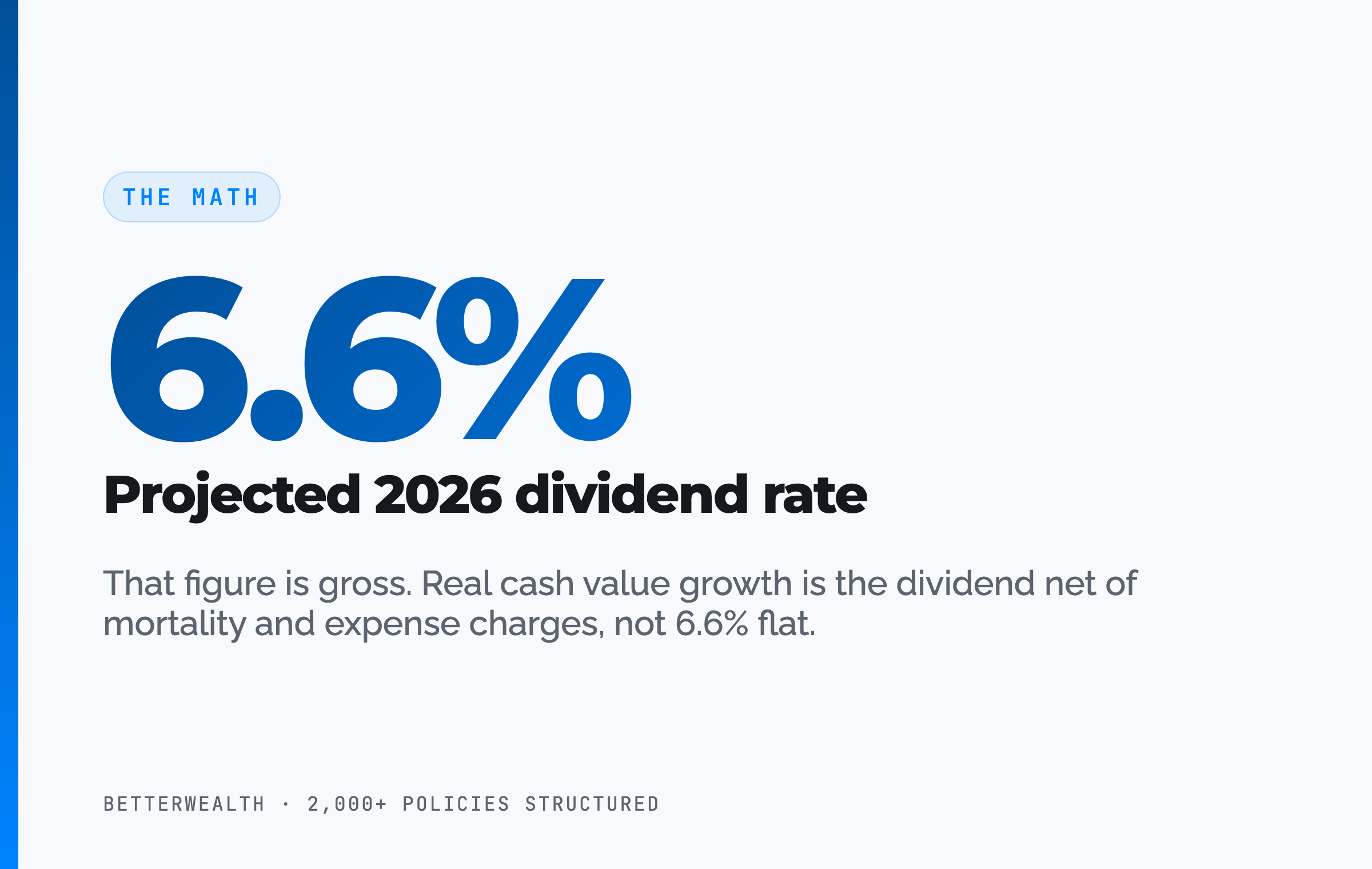

MassMutual is one of the most financially secure mutual carriers for infinite banking in 2026, with a 6.6% projected dividend rate, A++ strength, and a long dividend record. Its weaknesses are rigid paid-up additions riders, clunky illustration software, and a public anti-IBC marketing stance, so policy design and a skilled agent matter more here than elsewhere.

Pros

- A++ (Superior) AM Best, COMDEX 98 (top 2% of carriers)

- $2.9 billion declared dividend at a 6.6% projected 2026 rate

- 2.5% lapse ratio versus a 5.1% industry average

- Available in all 50 states, including New York

- Traditional long-term-care rider available on whole life

- Fast loans, online portal, and a mobile app for loan initiation

Cons

- Least flexible PUA riders among major mutuals (ALIR and PALIR)

- Public anti-IBC-marketing stance since 2022; some agents removed

- Confusing supplemental-rider (LISR) annual statements

- Career-agent system rarely trained on high-cash-value design

- Cashflow design year-one cash value runs 75 to 85%

- Variable loan rate locked monthly by anniversary

- Outdated, clunky illustration software (8/10 complexity)

Most people choose an insurance carrier for a multi-decade strategy the way they pick a checking account: they find the biggest brand with the highest advertised rate and stop there. MassMutual rewards that instinct and punishes it at the same time. The dividend is high. The financial strength is A++, top 2% of carriers by COMDEX. And the fine print inside the paid-up additions riders can quietly undo a strategy that looked perfect on the illustration.

With MassMutual, the carrier is strong enough that the policy's design and your funding discipline decide whether it works, not the company logo. This is a legacy mutual that has paid dividends since 1869. It is also a company that came out, publicly, against the way infinite banking gets marketed. Both things are true, and both matter for how you use it.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and MassMutual lands on our short list of the best carriers for infinite banking for clients who arrive already knowing the name. This review covers what the company actually is, how its core products behave under both a cashflow and a front-load design, the ALIR and PALIR rider mechanics that trip people up, the math that decides whether borrowing makes sense, and the four honest tradeoffs that never appear on a sales slide. We will also tell you who MassMutual is wrong for.

- MassMutual is non-direct recognition, so your dividend is not adjusted when you borrow against the policy.

- It declared roughly $2.9 billion in dividends with a 6.6% projected 2026 rate.

- Its 2.5% lapse ratio, versus a 5.1% industry average, signals policies that perform close to illustration.

- Its weakness is rigid PUA riders: ALIR is all-or-nothing, and PALIR caps you at the highest amount paid in the prior two years with no backfill.

- The And Asset rule still governs: only borrow when the deployed return clears MassMutual's loan cost.

- MassMutual works in New York and offers a traditional long-term-care rider, both rare among carriers.

If you want to see the actual cashflow and front-load illustrations, plus Alden walking through how the two PUA riders behave on screen, watch the full carrier breakdown:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves for a handful of structural questions, not for the advertised dividend rate. The real questions are whether the company will still be paying healthy dividends in forty years, whether its loan mechanics fit how you plan to use capital, and whether its riders let you fund the policy the way your income actually flows.

MassMutual answers the first question as well as any carrier alive. Founded in 1851, paying dividends since 1869, a major US mutual, A++ from AM Best, and sitting on more than $380 billion in assets under management. Stability is not the concern. The concern is the rider mechanics and the company's posture toward how you use the policy, which is where this review spends most of its time.

"The product, its design, and your understanding of that product matter more than the carrier choice among top mutual insurance companies.", Alden Armstrong

02 / The frameworkWhat does it mean to run infinite banking with MassMutual?

Running infinite banking with MassMutual means using a properly structured MassMutual whole life policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

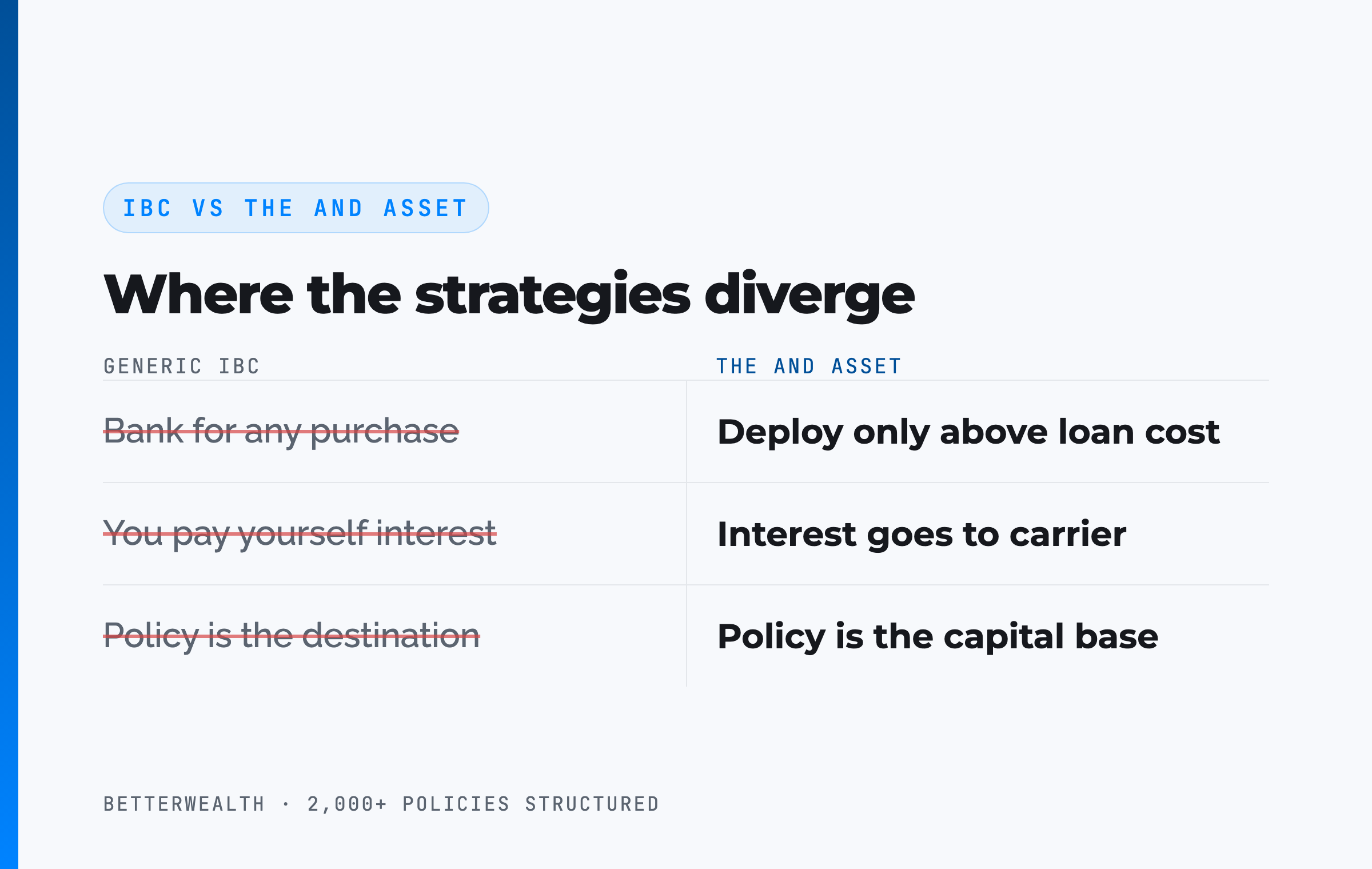

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to MassMutual. Your return is what the deployed capital earns elsewhere while the policy compounds uninterrupted.

The distinction is not academic here. The exact behavior MassMutual objects to, agents telling clients to "buy groceries" with policy loans and max-leverage early, is the casual spending The And Asset rules out. The disciplined version of this strategy is the version MassMutual has no problem with.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the insurance company, and your return comes from what you deploy into.

03 / The IBC stanceWhy does MassMutual publicly distance itself from infinite banking?

MassMutual distanced itself from infinite banking marketing because the marketing, not the strategy, created a problem it did not want its name attached to. Starting around 2022, the company took a stance, first privately among its agents and then more publicly, against IBC-style promotion.

The history matters. When dividend rates and loan rates both moved, some agents had encouraged clients to maximum-leverage policies very early. When loan costs ran above dividends on borrowed funds, those aggressively-loaned policies started to lapse. A company that prizes a low lapse ratio has every reason to discourage the behavior that drives lapses. MassMutual also runs a large career-agent system and treats the IBC marketing niche as more reputational downside than premium upside.

Two clarifications keep this honest. MassMutual is not anti-overfunding and not anti-loan. Some clients have been asked to verify loans against anti-money-laundering checks, a verification step, not an approval gate, and no client has been denied access to their own cash value. And BetterWealth still holds its contract and sells MassMutual products. The takeaway is narrow: market the strategy carefully, and do not treat the policy like a checking account.

MassMutual is publicly cool on infinite banking, then names a product "High Early Cash Value" and ships a mobile app you can take a policy loan from. The company is more calculated than contradictory.

04 / How it worksHow a MassMutual policy actually functions as an And Asset

A MassMutual policy functions as an And Asset through five mechanical steps, and the product you start with shapes everything after. MassMutual sells a famously deep product shelf, but three products carry the cash-value work: Whole Life 100, the High Early Cash Value product, and the 10-pay. Here is the sequence we use.

- Pick the product to match the funding. Whole Life 100 is built for level, long-term cashflow funding. The High Early Cash Value product is built for a front-load. The 10-pay is for someone who wants to fund fast and stop. The product decision comes first because the rest depends on it.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows. The PUA rider is the engine. The base/PUA split, whether 10/90, 40/60, or somewhere between, is the single design decision that determines early cash value.

- Choose the PUA rider deliberately. MassMutual gives you ALIR or PALIR. They are not interchangeable, and picking the wrong one for your funding personality is the most common mistake we see on policy reviews. The next section breaks both down.

- Let the early years capitalize. First-year cash value on a Whole Life 100 cashflow design lands around 75 to 85% of premium. The capitalization point, where a dollar of premium adds more than a dollar of cash value, arrives around year four. Break-even, where total cash value catches total contributions, typically lands at year five or later. Any illustration showing year-two break-even on a cashflow design is fiction.

- Borrow, deploy, and repay. After about 30 days from funding, you can take a non-direct-recognition policy loan. Put the borrowed capital into an activity that beats MassMutual's loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

On a Whole Life 100 cashflow design funded as illustrated, the long-term internal rate of return tops out around 3.9 to 4.6% on current dividend projections. That figure is the dividend net of mortality and expense charges, not the gross 6.6% headline. Anyone quoting you the gross rate as your growth rate is careless or selling.

Cashflow design versus front-load design

The two designs solve for different funding personalities. A cashflow design keeps the premium level year after year on Whole Life 100, and it is the most efficient long-term structure for someone committing to fund for a decade or more. A front-load front-ends a larger premium, then drops to a smaller level amount, which fits someone repositioning idle capital from a business, a bank account, or a liquidation.

For front-loads, we lean on the High Early Cash Value product. On a tight design, it can put over 90% of a first-year premium into accessible cash value, reach its capitalization point in year two, and break even around year four. The trade is long-term growth: the front-load IRR runs slightly lower, roughly 3.8 to 4.5%, because more premium means more insurance to stay under the MEC limit, and more insurance means more internal cost. Neither design is "better." They fit different people.

Lower IRR, more volume working sooner. That is the front-load trade.

For a deeper walkthrough of how the PUA rider and base premium split drives all of this, see how to structure an And Asset policy.

MassMutual fits a specific person doing specific things.

It fits you if

- You will fund on a consistent, scheduled basis

- You value financial strength and a high dividend

- You want a traditional long-term-care rider built in

- You live in New York and need a carrier that writes there

It does not fit you if

- Your income is variable and you need PUA flexibility

- You plan to borrow heavily and early

- You want a carrier that openly supports the strategy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether MassMutual or another carrier fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The ridersHow do MassMutual's ALIR and PALIR PUA riders actually work?

MassMutual's two paid-up additions riders trade flexibility against discipline in opposite directions, and choosing the wrong one is the most expensive mistake on a MassMutual policy. The riders are the ALIR (Additional Life Insurance Supplement Rider) and the PALIR (Planned Additional Life Insurance Supplement Rider). They sound alike when spoken quickly, which is its own hazard.

ALIR: the all-or-nothing rider

The ALIR demands the full illustrated PUA premium on the anniversary, every year, or you pay zero. On a $5,000 base premium with a $25,000 ALIR premium, that $25,000 is due in full or not at all. You can take up to two $0 years; the rider cancels only if you skip more than two consecutive years, and then you have to re-underwrite to get it back. That rigidity is the cost. The payoff is the strongest backfill in the industry: after skipping, you can pay the current year plus the prior two years, so $25,000 three times over. Forced discipline, with a powerful catch-up if life interrupts.

PALIR: flexible, but capped

The PALIR lets you fund anywhere from zero to your maximum year to year, which sounds like the flexible answer until you hit the limits. Your maximum resets to the highest amount paid in the last two years, so funding low for a stretch permanently lowers your ceiling. You get only three payments per policy year. And there is no backfill at all. You can skip one year; skip two consecutive years and the rider cancels. It is more flexible day to day, and less forgiving over time.

This is why MassMutual sits at the bottom of the industry for PUA flexibility. Neither rider gives an entrepreneur with variable income the yo-yo funding pattern other carriers allow. If we could marry the ALIR's backfill to the PALIR's annual flexibility, it would be a different conversation. We cannot.

The least flexible rider, the ALIR, carries the best backfill in the industry. The more flexible rider, the PALIR, takes that backfill away. MassMutual makes you choose your constraint.

The LISR escape hatch

One saving grace: the Level Indexed Supplement Rider (LISR), a blended term rider MassMutual lets you "flex" with extra premium up to the MEC limit. It buys out term and converts it to permanent insurance faster, which builds cash value when your PUA flexibility has run out. We do not recommend funding a policy primarily through blended term, and its annual statements confuse clients badly enough that explaining them is a recurring chore. But on a policy that lost PUA room, the LISR can keep capital flowing in.

06 / The mathDoes the return clear MassMutual's loan cost?

The return on whatever you deploy must exceed MassMutual's loan cost, or you should not borrow. This is the entire test. MassMutual is non-direct recognition, so borrowing does not change your dividend, and it uses a variable loan rate. The rate is set monthly and locks for a year on your policy anniversary, which means two policies in the same household can carry different loan rates. Policy loan rates vary by carrier and rate environment; at the time of writing many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, dividend unaffected by the loan because the recognition is non-direct. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the policy has done two jobs with one dollar. If it is lower, you have borrowed money to lose money slowly. Nelson Nash made a related point worth keeping: judge the strategy on the volume of capital working, not the rate alone.

If the deal does not clear the loan rate, do not borrow.

07 / Where it winsStrength, the long-term-care rider, and loan access

MassMutual's strongest features are the ones that have nothing to do with the dividend headline: financial strength, a rare long-term-care rider, and loan access that is genuinely convenient. These are the features that shape your experience for thirty years.

A++ strength and a healthy dividend

A 6.6% projected rate on roughly $2.9 billion declared, A++ from AM Best, COMDEX 98, and $380 billion in assets under management put MassMutual in the top tier of mutual carriers. The 2.5% lapse ratio against a 5.1% industry average is the quiet tell: policyholders keep these policies, which means the policies perform close to what the illustrations promised. Strength like this is what lets a long-horizon strategy survive forty years of rate environments.

A traditional long-term-care rider

MassMutual is one of the few carriers we work with that offers a true long-term-care accelerated death benefit rider on its whole life products. Most carriers offer a general accelerated death benefit rider; MassMutual's operates within the IRS definition of long-term care. For someone who wants LTC protection embedded in a cash-value policy rather than bought separately, this is a real edge. It is the kind of feature that closes the decision for a specific buyer.

Loan access and the LivingWell rider

Loans are available roughly 30 days after funding, sometimes 45 depending on premium size. Smaller loans often initiate through the online portal or the mobile app, with larger loans routed through your agent or the carrier for signature verification. Interest accrues daily at an annualized rate, which keeps the math clean. MassMutual also offers the LivingWell rider, which ties a Whoop, Apple Watch, or Garmin to the policy and can lower internal costs over time, improving cash value for the health-focused funder.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use when we compare carriers like MassMutual, Penn Mutual, and Guardian. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the four honest tradeoffs

MassMutual's benefits come with four tradeoffs that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, rigid PUA riders. Neither the ALIR nor the PALIR gives a variable-income entrepreneur the funding flexibility other carriers offer, and MassMutual sits at the bottom of the industry on this metric. Second, the anti-IBC stance. The company objects to aggressive infinite banking marketing, some agents were removed from distribution over it, and you have to be careful how the strategy is presented. Third, the LISR statements. The blended-term rider produces annual statements confusing enough that clients regularly believe they owe far more than they do. Fourth, the career-agent system: the majority of MassMutual policies are written by career agents who are not trained to design high-cash-value policies, so finding the right agent is genuinely hard.

Two operational frictions ride along with those four. MassMutual scores an 8 out of 10 on product complexity, driven by the PUA riders, LISR flexibility, and a deep product shelf, so the learning curve for an agent is steep. The illustration software is dated and clunky enough that many agents route illustrations through the home office, and compensation tracking on the carrier side can be cumbersome. None of this hits you directly as a policyholder, but it raises the odds of a botched design if your agent does not know the products cold.

Against those tradeoffs sits the company itself. A++ strength, a high dividend, a product shelf deep enough to solve almost any situation, and features like the long-term-care rider that few competitors match. For the right funder, the tradeoffs are acceptable. For the wrong one, the rider rigidity alone is a dealbreaker.

Strong company. Stiff riders. Know which you are buying.

The rider rigidity may be a feature, not a bug. MassMutual may be designing exactly so the flexibility-seekers self-select out. These companies are calculated, and the limits that do not show up on an illustration are the ones that matter most.

09 / The fitWho is MassMutual right for, and who isn't it?

MassMutual is right for the disciplined funder who values financial strength, a high dividend, and an embedded long-term-care option, and who will fund on a consistent schedule. It fits the entrepreneur or high-income earner who arrives wanting a household-name carrier they have seen sponsor a hockey team, who plans to fund steadily, and who can identify productive uses for borrowed capital. It is a frequent choice for someone using an annuity to fund the policy on a guaranteed schedule, or funding a short-pay on a child or grandchild through a trust, where the rider rigidity is irrelevant.

It is the wrong carrier for someone with variable income who needs to flex funding up and down, for someone who plans to borrow heavily in the first few years, or for someone who wants a carrier that endorses the strategy. When a client tells us they want to use cash value early and often, we usually steer them elsewhere, both because the rider flexibility is not there and because we want to place that business with a carrier that welcomes it.

10 / Head to headMassMutual against the alternatives

Compared to the capital tools entrepreneurs actually use, a MassMutual And Asset policy trades day-one access for control, tax treatment, and uninterrupted compounding. The table sets it against a HELOC, a 401(k), and a taxable brokerage account on the four dimensions that matter for capital strategy.

| Dimension | MassMutual And Asset | HELOC | 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Growth | Compounds on full cash value, net of internal costs, even while borrowed against; non-direct dividend unaffected by loans | None (it is a credit line, not an asset) | Market growth, tax-deferred | Market growth, taxed annually on gains |

| Liquidity | Loans after ~30 days; smaller loans via portal or app, larger via signed form | Fast once approved, but can be frozen or called | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

| Tax treatment | Policy loans are not taxable income under IRC 7702 | Interest may be deductible in limited cases | Deferred now, taxed as ordinary income later | Capital gains and dividends taxed yearly |

| Cost / contribution | $50,000/yr cashflow design, ~75-85% available in year one; loan rate variable, often 5-6% | No contribution; variable rate often 8-10%+ when open | $23,500 employee limit (2025); penalties to access early | No cap; brokerage fees plus annual tax drag |

Growth. A MassMutual policy keeps compounding on its full value while you borrow, and because the recognition is non-direct, the loan does not touch your dividend. A HELOC cannot do this because a credit line is not an asset. That uninterrupted compounding is the structural feature that makes the same dollar do two jobs.

Liquidity. A HELOC is faster on paper, but a HELOC can be frozen exactly when you need it, as thousands of investors learned in 2020. A MassMutual loan cannot be called. The roughly 30-day initial wait and the 75 to 85% first-year cash value on a cashflow design are the cost of access that does not disappear in a downturn.

Tax and control. Policy loans are not taxable income under Section 7702, and the loan cannot be called. A 401(k) defers tax but restricts access until 59½ under rules set by Congress. The And Asset trades the highest possible early liquidity for control and tax treatment you keep.

Against the other mutuals. The carrier comparison most readers actually want is MassMutual against its peers. MassMutual is non-direct recognition with A++ strength and a high dividend, held back by the least flexible PUA riders of the group. Penn Mutual is direct recognition and tends to show the strongest long-term growth. Guardian is direct recognition with strong high early cash value. If you specifically need New York coverage, MassMutual writes there, as do a handful of others like Ameritas and Security Mutual. The right answer depends on policy design and your time horizon, not the dividend rate alone. See the full carrier comparison for the side-by-side.

A composite: the business owner who deployed at year nine

Consider a 43-year-old business owner, select preferred non-tobacco, funding a MassMutual Whole Life 100 policy at $50,000 per year on a cashflow design with a roughly 12/88 base/PUA split. The figures below are illustrative and hypothetical, drawn from the pattern we see across policies, not a single named client or a specific carrier illustration.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. The capitalization point arrives around year four, where each premium dollar starts adding more than a dollar of cash value. Break-even, where total cash value crosses total contributions, lands around year seven. No earlier. Any illustration showing year-two break-even on a cashflow design is marketing fiction.

Say that in year nine, with several hundred thousand dollars of accessible cash value, the owner borrows against the policy to buy revenue-producing equipment for the business. If the equipment earns a return above the loan cost, the spread works in the owner's favor. Because MassMutual is non-direct recognition, the dividend on the full cash value is untouched while the loan is outstanding, and the policy keeps compounding the entire time. Repayment runs on a schedule funded by the equipment's own cash flow.

The downside case is just as real. If that equipment underperforms and earns less than the loan cost, or sits idle, the spread inverts and the owner is borrowing to lose money slowly while interest accrues daily. The structure does not rescue a bad deployment. That is why The And Asset rule is non-negotiable: if the use of funds cannot clear the loan cost, you do not borrow.

One dollar doing two jobs only works when the deployment clears the loan rate.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a MassMutual policy, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQMassMutual infinite banking questions

Is Mass Mutual good for infinite banking?

MassMutual is a strong carrier for infinite banking in 2026, with A++ financial strength, a high dividend, and a low 2.5% lapse ratio. Its weaknesses are rigid paid-up additions riders, clunky illustration software, and an institutional anti-IBC marketing stance, so policy design and a skilled agent matter more here than with most carriers.

Is Mass Mutual direct or non-direct recognition?

MassMutual's current whole life products are non-direct recognition, which means your dividend is not adjusted when you borrow against the policy. Some legacy products offered both, but the products sold today are non-direct with a variable loan rate that locks for a year on your policy anniversary.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Why does Mass Mutual have an anti-IBC stance?

Starting around 2022, MassMutual distanced itself from infinite-banking-style marketing after some agents encouraged clients to over-leverage policies early, which contributed to lapses. MassMutual is not anti-overfunding or anti-loan. It objects to the aggressive marketing, and it still sells the products BetterWealth uses.

What is Mass Mutual's dividend rate for 2026?

MassMutual's projected dividend interest rate for 2026 is 6.6%, with roughly $2.9 billion declared to policyholders. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges, and dividends are declared annually and are not guaranteed.

What is the difference between MassMutual's ALIR and PALIR riders?

ALIR is an all-or-nothing PUA rider: the full illustrated amount is due on the anniversary or you pay zero, you can skip a maximum of two years, and it carries the strongest backfill in the industry. PALIR is more flexible year to year but caps your maximum at the highest amount paid in the last two years, allows only three payments per year, and offers no backfill.

Is Mass Mutual available in New York?

Yes. MassMutual is one of the few carriers BetterWealth works with that operates in New York, along with the rest of the 50 states. That nationwide reach, including New York, is one of its real advantages over smaller mutuals.

What is Mass Mutual's best product for infinite banking?

For level long-term funding, Whole Life 100 designed for maximum cash value is the workhorse. For a front-load, the High Early Cash Value product can put over 90% of a first-year premium into accessible cash value. The 10-pay is used when someone wants to fund quickly and stop.

How fast can you access cash from a MassMutual policy?

MassMutual allows policy loans roughly 30 days after funding, sometimes 45 depending on premium size. Smaller loans can often be initiated through the online portal or mobile app, while larger loans go through your agent or the carrier with a signed form, and interest accrues daily.

Mass Mutual vs Penn Mutual or Guardian for infinite banking?

MassMutual is non-direct recognition with A++ financial strength and a high dividend, but the least flexible PUA riders among major mutuals. Penn Mutual is direct recognition with strong long-term growth. Guardian is direct recognition with high early cash value. The right carrier depends on policy design and your time horizon, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, MassMutual's A++ (Superior) financial strength rating and the 5.1% industry lapse benchmark.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- MassMutual, declared dividend, product, and rider information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Specializes in policy structure and carrier comparisons across the IBC series, and walks through the MassMutual cashflow, front-load, and 10-pay illustrations in the source video. Co-author of the Ultimate 2026 IBC Carrier Comparison Guide.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a MassMutual policy fits your plan, book a discovery call. We will tell you if it does not.