.png)

Foresters is a workable infinite banking carrier in 2026, offering industry-leading early cash value of 85 to 94%, fast loan access, and fraternal member benefits. Its tradeoff is lower long-term growth, with projected IRR near 3.1 to 3.8%, so it fits early-access and benefit-driven buyers more than pure performance seekers.

A 6% dividend rate is the first number most people see on Foresters, and often the only one. They assume it tracks one for one to cash value growth and stop reading. It does not, and it is only one input. The dividend rate says almost nothing about whether a contract will work as a capital base for the next thirty years, and with Foresters it hides a story that cuts both ways.

Foresters delivers some of the strongest early cash value in the market and some of the weakest long-term growth, which means the carrier only makes sense for a specific buyer doing a specific thing. It is also structurally unusual. Foresters is not a mutual insurance company. It is a fraternal benefit society, and that single fact changes the language, the legal wrapper, and the list of extra benefits attached to the contract.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we built this review as part of an ongoing series ranking the best life insurance companies for infinite banking. This piece covers what Foresters actually is, how its Advantage Plus II product behaves under both a cashflow and a front-load design, the math that decides whether borrowing against it makes sense, and the honest tradeoffs nobody puts in a sales deck. We will also tell you who Foresters is not for.

- Foresters is a fraternal benefit society, not a mutual insurer, and it issues a participating whole life certificate rather than a policy contract.

- Its strength is early cash value, reaching 93 to 94% in year one on a well-designed Advantage Plus II, which is industry leading.

- Its weakness is long-term growth, with projected IRR around 3.1 to 3.8%, lagging comparable US mutual carriers.

- The And Asset rule still governs: only borrow when the deployed return clears Foresters' loan cost.

- Foresters is non-direct recognition, so policy loans do not change your dividend, and loans are available about 10 days after funding.

- Membership adds fraternal benefits, including scholarships, an orphan benefit, and complimentary estate documents through Law Assure.

If you want to see the actual Advantage Plus II illustrations behind these numbers, Alden Armstrong walks through both the cashflow and front-load designs on screen, including the early cash value and the break-even points:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves for a handful of structural questions, not for the headline dividend rate. The real questions are whether the company will still be paying generously in forty years, whether its loan mechanics fit how you plan to use capital, and whether its product can be designed for high cash value without tipping into a Modified Endowment Contract. Foresters answers some of these well and one of them poorly.

On longevity, Foresters is convincing. A society founded in 1874, sharing profits with members for over 150 years, is not a stability risk. On performance, it is a different story. The early cash value is among the best in the market, but the projected long-term return trails the field, and that gap is the entire reason this review exists.

"Life insurance gives you multiple benefits by your contract, or in this case your certificate. Those all need to be factored in, because some of them never show up in an IRR calculator.", Caleb Guilliams

02 / The frameworkWhat does it mean to run infinite banking with Foresters?

Running infinite banking with Foresters means using a properly structured Foresters whole life certificate as a capital base you borrow against, while the contract keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset, and it matters more with Foresters than with almost any other carrier.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

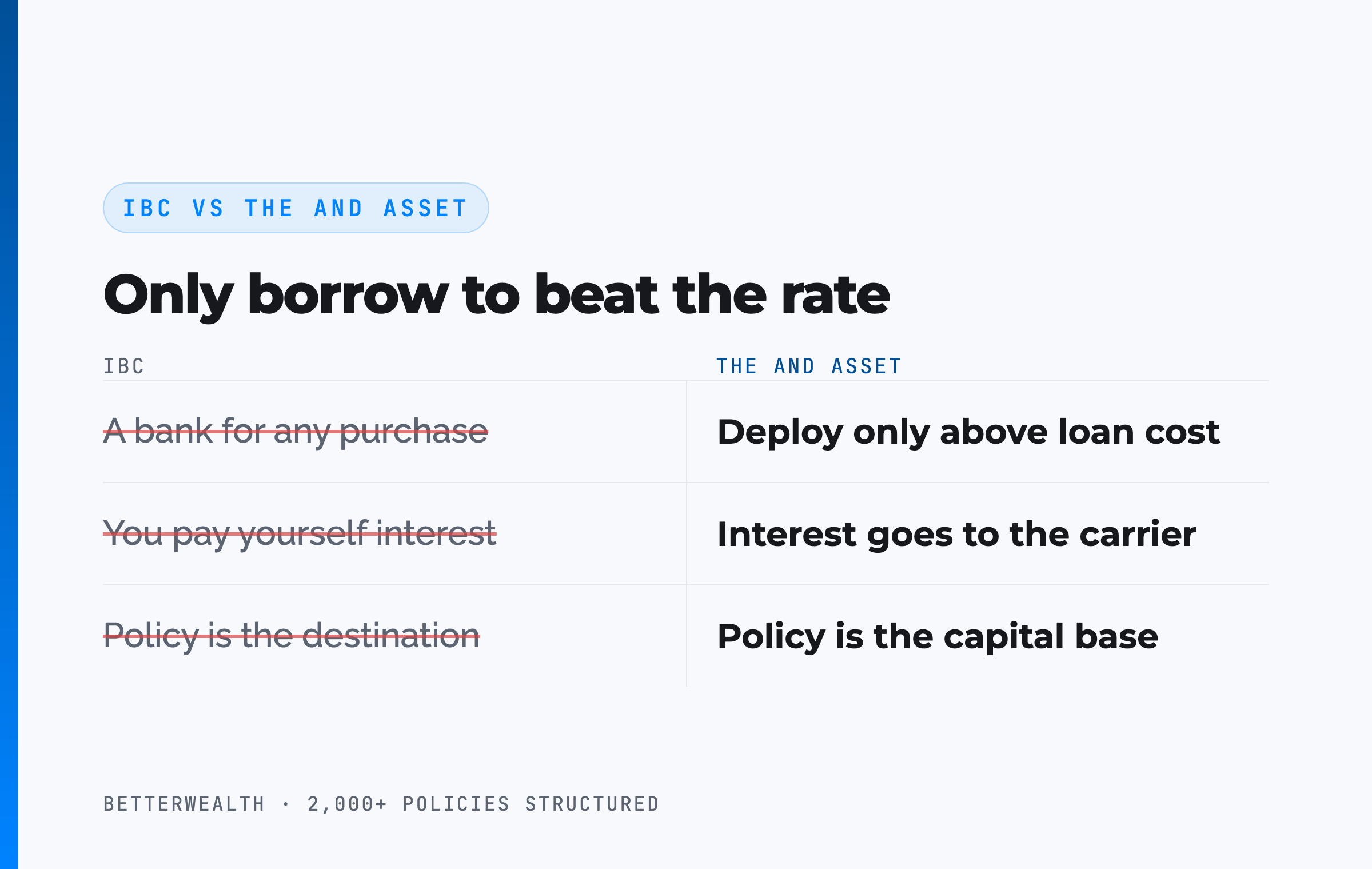

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the contract when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company, and your return is what your deployed capital earns elsewhere while the certificate keeps compounding net of internal costs.

This distinction is sharper with Foresters precisely because its projected long-term growth lags. When the contract grows slowly on its own, more of the value has to come from what you deploy the capital into, so a weak use of borrowed money costs you more here than at a higher-IRR carrier.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the carrier, and your return comes from what you deploy into.

03 / The structureWhy does it matter that Foresters is not a mutual?

It matters because the legal wrapper changes the vocabulary and adds a layer of member benefits, even though the contract behaves like participating whole life. Foresters, formally The Independent Order of Foresters, is a fraternal benefit society. You are not a policyholder with a policy contract. You are a certificate holder and a member of the society, and your participating whole life sits inside that membership.

In practice the certificate works the same way a participating whole life policy works. It earns dividends, builds cash value, and pays a death benefit. Foresters has only declared dividends for roughly the last 60 years. Across its full 150-plus-year history, it has shared profits with members in other forms, and it still does, paying over $15 million a year on average in fraternal benefits on top of the declared dividend. Foresters had not disclosed its 2026 dividend dollar amount at the time of writing; the most recent disclosed figure was $25.8 million paid to the US market in 2024.

On ratings, the fraternal structure means not every agency covers Foresters. It carries an AM Best rating of A (Excellent) and a DBRS Morningstar rating of A (Stable). It does not carry a COMDEX score, which is common for fraternal carriers. That is a gap in the data, not a red flag.

It is a certificate, not a policy contract, because Foresters is a fraternal benefit society. In reality it plays out the exact same way. It is just a different code in the insurance market.

04 / How it worksHow a Foresters certificate actually functions as an And Asset

A Foresters certificate functions as an And Asset through five mechanical steps, and the order matters. The product is Advantage Plus II, designed for maximum cash value rather than maximum death benefit. Here is the sequence we use when we structure one.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows. The PUA rider is the engine. Without it, this is an expensive death benefit. The base/PUA split is the single design decision that determines early cash value.

- Fund consistently. Choose a cashflow design (the same premium every year) or a front-load design (a larger first-year premium, then a level amount). Advantage Plus II is built to be funded long term, and it keeps accepting premium efficiently even after the term component falls off.

- Let the early years capitalize. Year-one cash value on a maximum-cash-value design lands around 93%, which is unusually strong. The capitalization point, where a dollar of premium adds more than a dollar of cash value, arrives around year three.

- Borrow against the certificate. As soon as 10 days after funding clears, you can take a policy loan collateralized by your cash value. Foresters is non-direct recognition, so the loan does not change your dividend.

- Deploy and repay. Put the borrowed capital into an activity that beats Foresters' loan cost, then repay from the cash flow that activity throws off. The certificate keeps compounding on its full value the entire time.

On a cashflow design funded at $50,000 per year, break-even, where total cash value catches total contributions, typically lands around year four to five for a healthy individual. Do not expect to break even on day one. You will not, and any illustration that shows it is fiction.

Cashflow design versus front-load design

The two designs solve for different funding personalities. A cashflow design keeps the premium level, year after year. On the illustration walked through in the video, $50,000 a year produces roughly 93% cash value in year one, a death benefit just above $1.3 million, and break-even around year four. A front-load design front-ends a larger premium, then drops to a level amount. To stay under the MEC limit it roughly doubles the death benefit, which adds internal cost and pushes break-even out to about year five.

Both designs share the same weak spot. Foresters projects a long-term IRR of roughly 3.2 to 3.8% on the cashflow design and 3.1 to 3.7% on the front-load design, both lower than comparable mutual carriers. You buy strong early access and accept slower long-term compounding. Neither design escapes that.

You trade long-term compounding for cash you can reach early.

Foresters fits a specific person doing specific things.

It fits you if

- You want maximum cash value in years 1 to 5

- You value the fraternal benefits and will actually use them

- You can name a use for capital that beats the loan cost

- You plan to deploy borrowed capital early and often

It does not fit you if

- You are optimizing purely for long-term IRR

- You want a top-rated "Big Four" mutual brand

- You want a savings account, not a life insurance strategy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether Foresters or another carrier fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the return clear Foresters' loan cost?

The return on whatever you deploy must exceed Foresters' loan cost, or you should not borrow. This is the entire test, and it is non-negotiable with a carrier whose own growth is modest. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with Foresters, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. Because Foresters is non-direct recognition, your dividend is unaffected by the loan, so the certificate keeps compounding on its full cash value net of mortality and expense charges. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the dollar has done two jobs. If it is lower, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

06 / Loan accessHow fast can you actually use the cash value?

Foresters offers some of the fastest loan access in this series, with loans available as soon as 10 days after funding clears, matching Security Mutual and Pan-American on speed. Practitioners have been told that once you can prove the initial check cleared, with a bank statement or a screenshot, the carrier will initiate a loan. If your plan depends on capital being ready when a deal shows up, that speed matters.

The loan system is non-direct recognition on a variable rate, like most carriers in this series. You can initiate loans through the online portal, by phone, or through your agent, and larger amounts may require additional verification. Repayments run through the portal, and interest accrues daily on the outstanding balance, visible to the day. That transparency is the cleanest way to see exactly what borrowing is costing you.

Why non-direct recognition keeps the math simple

With non-direct recognition, your dividend does not move based on whether you have a loan outstanding. That removes a variable from the decision. You do not have to track how borrowing affects your credited rate, because it does not. For an entrepreneur who borrows often and repays on the cash flow a deal generates, that is one less thing to model on every loan.

Foresters' long-term growth is not as competitive as other companies we have shown. The pro is there are other things, the fraternal benefits, that do not show up in an IRR calculator and might still move the needle for you.

07 / Where it winsThe PUA catch-up provision nobody else has, plus the fraternal benefits

Foresters' standout features are a uniquely flexible paid-up additions rider and a set of member benefits no mutual carrier offers. These are the features that can tip the decision for the right buyer, and they rarely show up in a side-by-side rate comparison.

A 10-year PUA catch-up window

Foresters allows anytime PUA payments up to the maximum built into the certificate, with a minimum premium lower than the $100 to $120 many carriers require, and a high upper limit near $300,000 of annual premium into the rider. The standout is the catch-up provision. Most carriers, if they allow catch-up at all, let you backfill only the prior year. Foresters gives you a 10-year window from issue, so in year nine you can still fund a contribution you missed in year two, up to a $25,000 limit.

There is one caveat. Foresters readjusts the ceiling of your PUA rider at year five and again at year 10, based on the average you have actually funded. If you let your funding average drop, your future ceiling drops with it. Backfilling a missed year also repairs that average, which keeps your funding capacity intact. It is the only carrier we have reviewed with a look-back window this long. Lafayette Life does a similar look-back at year seven.

The fraternal benefits

This is where Foresters separates from every mutual carrier. As a certificate holder and member, you have access to competitive scholarships (over $2 million in annual tuition awards), an orphan scholarship for children left behind, an orphan benefit that can pay roughly $900 a month to a legal guardian for a child under 18, member discounts, wellness rewards, community grants, and Law Assure, which provides will, trust, power of attorney, and advance directive preparation. Foresters pays over $15 million a year on average across these benefits.

The honest question is how easy these are to actually claim. Many require qualification, and a small certificate may not justify chasing a $35 family-activity grant. We treat the fraternal benefits as a real but secondary consideration, not the reason to buy. Measure how much you value any one benefit, then weigh it against the performance you give up.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare carriers like Foresters, Penn Mutual, and Guardian. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the honest considerations

Foresters' benefits come with real considerations that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, lagging long-term growth. The projected 3.1 to 3.8% IRR trails comparable US mutuals, and over a multi-decade contract that gap compounds against you. If you are optimizing purely for performance, this is a genuine reason to look elsewhere. Second, the consumer complaint index. Foresters runs at 1.39 on the NAIC complaint index against a baseline of 1.00, so it draws more service complaints than an average-sized insurer, which likely ties to longer service times as a fast-growing carrier. Set expectations on response times up front. Third, geography. Foresters operates in 49 states plus Washington, DC, and does not sell in New York, so a New York resident is out from the start. Fourth, the structure itself. Foresters is not a true mutual, and it operates across the US, Canada, and the UK through separate subsidiaries, even though the product you buy is a US-regulated contract. For some buyers that is a non-issue. For others it is a reason to ask more questions.

There is also a distribution wrinkle worth naming. Foresters writes flexible contracts with large sales organizations and IMOs, which is part of why it reaches so many buyers. That breadth can mean a wider range of agent experience, which may feed the complaint numbers. The flip side is that a firm building out a structured organization can work with Foresters in ways stricter mutuals do not allow.

Against those considerations sit the strengths. Industry-leading early cash value, the longest PUA catch-up window we have seen, fast loan access, and a fraternal benefit package no mutual offers. The decision comes down to how you weigh early access and benefits against long-term compounding.

The early access is real, and so is the lower long-term return. You decide which one your plan needs.

If you are batting a thousand and you want the biggest IRR, this is probably not your carrier. But ask what other benefits you get, and whether you want to be part of the structure they have built.

09 / The fitWho is Foresters right for, and who isn't it?

Foresters is right for the entrepreneur or value creator who wants maximum early cash value, will deploy borrowed capital early and often, and genuinely values the fraternal benefits attached to membership. It fits the buyer who treats the certificate as a capital base to borrow against rather than a long-term growth engine, and who can identify productive uses for that capital that clear the loan cost.

It is the wrong carrier for someone optimizing purely for long-term IRR, who wants a top-rated mutual brand, or who is looking for a savings vehicle rather than a life insurance strategy. If you cannot name an activity that beats the loan cost, no carrier is right for you, and Foresters makes that mistake more expensive because its own growth does less to bail you out.

10 / Head to headForesters against the alternatives

Compared to the capital tools entrepreneurs actually use, a Foresters And Asset certificate trades long-term growth for early access, control, and tax treatment. The table sets it against a HELOC, a 401(k), and a taxable brokerage account on the four dimensions that matter for life insurance strategy.

| Dimension | Foresters And Asset | HELOC | 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Growth | Compounds on full cash value, net of internal costs, even while borrowed against; long-term IRR is modest at ~3.1-3.8% | None (it is a credit line, not an asset) | Market growth, tax-deferred | Market growth, taxed annually on gains |

| Liquidity | High early cash value (85-94%); loans about 10 days after funding via portal, phone, or agent | Fast once approved, but can be frozen or called | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

| Tax treatment | Policy loans are not taxable income under IRC 7702 | Interest may be deductible in limited cases | Deferred now, taxed as ordinary income later | Capital gains and dividends taxed yearly |

| Control | Loan cannot be called; you set repayment terms; non-direct recognition keeps the math simple | Lender controls terms and can revoke access | Access rules set by Congress, not you | Full control, but no leverage feature built in |

Growth. A Foresters certificate keeps compounding on its full value while you borrow, which a HELOC cannot do because a credit line is not an asset. The catch is that Foresters compounds more slowly than top mutuals, which raises the bar on what you deploy borrowed capital into.

Liquidity. This is where Foresters shines. A HELOC is faster on paper, but a HELOC can be frozen exactly when you need it, as thousands of investors learned in 2020. Foresters combines high early cash value with loan access in about 10 days, and the loan cannot be called.

Tax and control. Policy loans are not taxable income under Section 7702, and the loan cannot be called. A 401(k) defers tax but restricts access until 59½ under rules set by Congress. The And Asset trades the highest possible long-term return for early access, control, and tax treatment you keep.

Foresters against the mutual carriers it competes with

The honest comparison is not Foresters versus a HELOC, it is Foresters versus the participating mutuals people actually weigh it against. This is where the tradeoff shows up: Foresters matches or beats the field on early cash value and loses to it on long-term IRR. Figures are typical ranges for high-cash-value designs and vary by age, health, and design.

| Carrier | 2026 dividend rate | Year-1 cash value | Long-term IRR | Loan recognition |

|---|---|---|---|---|

| Foresters | 6.00% | 85-94% | 3.1-3.8% | Non-direct |

| Penn Mutual | 6.10% | 77-87% | 4.2-5.3% | Direct |

| Guardian | 6.25% | 80-94% | 3.5-4.5% | Direct |

| Lafayette Life | 5.90% | 82-94% | 3.5-4.7% | Non-direct |

Read the IRR column and the case for Foresters narrows. Penn Mutual projects the strongest long-term return of the group, and Guardian and Lafayette Life both edge out Foresters on long-term compounding while landing close on early access. Foresters earns its place on year-one cash value, fast loans, the 10-year PUA catch-up window, and the fraternal benefits no mutual offers. If long-term IRR is your single priority, the table points elsewhere.

How the math plays out: a hypothetical contractor

The example below is hypothetical and built to show the mechanics. It is not a real client, not a quote, and not a guaranteed result. Actual numbers depend on age, health, design, and Foresters' future dividends, which are not guaranteed. Picture a 43-year-old general contractor, preferred non-tobacco, funding a Foresters Advantage Plus II certificate at $50,000 a year on a cashflow design.

Even with Foresters' strong early cash value, the first years still trail cumulative contributions, exactly as a real certificate should. By around year three, each premium dollar adds more than a dollar of cash value. Break-even, where total cash value crosses total contributions, lands around year four to five. Any illustration showing year-two break-even is marketing fiction.

Once accessible cash value has built up, the contractor borrows against the certificate to buy used equipment that lets the crew take on site-prep work it used to subcontract out. The strategy only works if that equipment's added margin earns more than the loan cost. The certificate keeps compounding on its full value the entire time, and the loan is repaid from the equipment's own billings. If the deployed return cannot clear the loan rate, the right move is not to borrow.

When the deployed return beats the loan cost, the same dollar does two jobs.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a Foresters certificate, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQForesters infinite banking questions

Is Foresters good for infinite banking?

Foresters is a workable infinite banking carrier in 2026, with industry-leading early cash value of 85 to 94%, fast loan access, and a flexible paid-up additions rider. Its weakness is lower long-term growth, with projected IRR around 3.1 to 3.8%, so it fits buyers who value early access and fraternal benefits over maximum long-term performance.

Is Foresters a mutual insurance company?

No. Foresters, formally The Independent Order of Foresters, is a fraternal benefit society, not a mutual insurer. It issues a participating whole life certificate rather than a policy contract, and membership carries fraternal benefits in addition to the life insurance. Mechanically it functions like a participating whole life policy.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is Foresters direct or non-direct recognition?

Foresters is a non-direct recognition carrier on a variable-rate loan system. Dividends are not adjusted based on whether you have an outstanding policy loan, which keeps the borrowing math simple and predictable regardless of how often you borrow.

What is Foresters' dividend rate for 2026?

Foresters declares a 6% dividend interest rate, competitive with the larger mutuals. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges, and dividends are not guaranteed. Foresters has only paid dividends for roughly 60 years, though it has shared profits with members in other forms for over 150 years.

What is the Foresters Advantage Plus II?

Advantage Plus II is the Foresters participating whole life product used for And Asset and infinite banking style designs. Built for maximum cash value with a heavy paid-up additions rider, it can reach 93 to 94% cash value in year one, which is industry leading on early access.

How fast can you access cash from a Foresters policy?

Foresters allows policy loans as soon as 10 days after funding, once the initial payment clears. Loans can be requested through the online portal, by phone, or through your agent, and interest accrues daily with full transparency in the portal.

What fraternal benefits does Foresters offer?

As a fraternal benefit society, Foresters offers member benefits beyond the certificate, including competitive and orphan scholarships, an orphan monthly benefit, complimentary will and estate document preparation through Law Assure, member discounts, and community grants. Foresters has paid over $15 million in such benefits on average in recent years.

What is Foresters' long-term performance for infinite banking?

Foresters projects a long-term internal rate of return of roughly 3.1 to 3.8% on current dividend projections, which lags comparable US mutual carriers. The tradeoff is strong early cash value and fraternal benefits. For a buyer optimizing purely for long-term IRR, a top mutual carrier is usually a better fit.

Foresters vs Penn Mutual or Guardian for infinite banking?

Foresters leads on early cash value and fraternal benefits but trails on long-term IRR, projecting roughly 3.1 to 3.8% versus Penn Mutual's 4.2 to 5.3%. Penn Mutual is a direct recognition mutual with the strongest long-term growth. Guardian is a direct recognition mutual with strong early cash value. The right carrier depends on policy design and your priorities, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, Foresters' A (Excellent) financial strength rating, and DBRS Morningstar's A (Stable) rating.

- NAIC, the consumer complaint index (Foresters 1.39 versus a 1.00 baseline) referenced for carrier service comparisons.

- Foresters Financial, product, dividend, and fraternal benefit information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Specializes in policy structure and carrier comparisons across the IBC series, and walks through the Foresters Advantage Plus II illustrations in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a Foresters certificate fits your plan, book a discovery call. We will tell you if it does not.