.png)

OneAmerica is an IBC-friendly, non-direct-recognition carrier whose Whole Life 95 pairs the most flexible paid-up additions rider in the field with fast loan access and a hybrid long-term care option. The tradeoff is below-average illustrated growth, which makes it a flexibility-and-service carrier rather than a performance-first one.

A solid, conservative workhorse that IBC practitioners reach for when flexibility, service, fast loan access, and a long-term care option matter more than headline cash value and IRR.

Pros

- Most flexible PUA rider in the field: anytime payments up to 3x base, $120/year minimum

- Non-direct recognition (dividend unaffected by loans)

- Loan access in about two weeks, among the fastest in the industry

- Industry-leading hybrid long-term care line (Asset Care, Annuity Care)

- Conservative, stable projections; lapse ratio of 4.7%, near the 5.1% industry average

Cons

- Below-average illustrated growth, roughly 2.9 to 3.5% long-term IRR

- Lower early cash value, 60 to 75% in year one on a cashflow design

- Max PUA caps the design near a 25/75 base-to-PUA ratio

- Conservative underwriting; can come in a rating class behind competitors

- Service strained by rapid growth, dated illustration software, no New York

Choosing a carrier for a multi-decade capital strategy is the wrong place to start, and it is exactly where most people start. They line up dividend rates the way shoppers line up APYs, pick the highest number, and assume they have made the right call. The dividend rate is one input, and OneAmerica does not even publish theirs. It tells you almost nothing about whether a policy will function as a capital base for the next thirty years.

The carrier matters far less than the design of the policy and your discipline in funding it. OneAmerica is a carrier IBC practitioners genuinely like, and the affection is earned: the team understands this kind of business, the paid-up additions rider is the most flexible in the field, and loan money moves fast. The numbers, though, run conservative, and an honest review has to say so.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we have watched OneAmerica go from a go-to front-load carrier to a workhorse we use selectively against the rest of the field. This review covers what the company actually is, how its Whole Life 95 product behaves under a cashflow and a front-load design, the math that decides whether borrowing against it makes sense, and the tradeoffs nobody puts in a sales deck. We will also tell you who OneAmerica is not for.

- OneAmerica is a non-direct-recognition carrier, so the dividend stays the same whether or not you have a loan outstanding.

- Its paid-up additions rider is the most flexible in the field, with anytime payments up to 3x the base premium.

- Its weakness is growth: long-term IRR runs near 2.9 to 3.5%, the bottom quarter among top mutuals.

- The And Asset rule still governs: only borrow when the deployed return clears OneAmerica's loan cost.

- OneAmerica leads the mutual market in hybrid long-term care through Asset Care and Annuity Care.

- OneAmerica sells in 49 states and Washington DC, but not in New York.

If you want to see the actual Whole Life 95 illustrations behind these numbers, Alden walks through both the cashflow and front-load designs on screen in the full review:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves a handful of structural questions, not the headline dividend rate. The real questions are whether the company will still pay dividends in forty years, whether its loan mechanics fit how you plan to use capital, and whether its product can be designed to push cash value to the limit without tipping into a Modified Endowment Contract.

OneAmerica answers the durability question well. A company with roots going back to 1864, a COMDEX of 95, and an AM Best rating of A+ is not a stability risk. The structure has a wrinkle worth knowing: the writing company, American United Life (AUL), operates as a stock insurer under the OneAmerica brand, owned by its policyholders through the American United Mutual Insurance Holding Company. So it is mutual at the holding level, which is what matters for dividends, even though the issuer underneath is a stock company. The harder questions are about mechanics, design, and growth, which is where this review spends most of its time.

"Dividend rate does not equate to internal rate of return. It does not directly translate to having the most efficient product." (Alden Armstrong)

02 / The frameworkWhat does it mean to run infinite banking with OneAmerica?

Running infinite banking with OneAmerica means using a properly structured Whole Life 95 policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

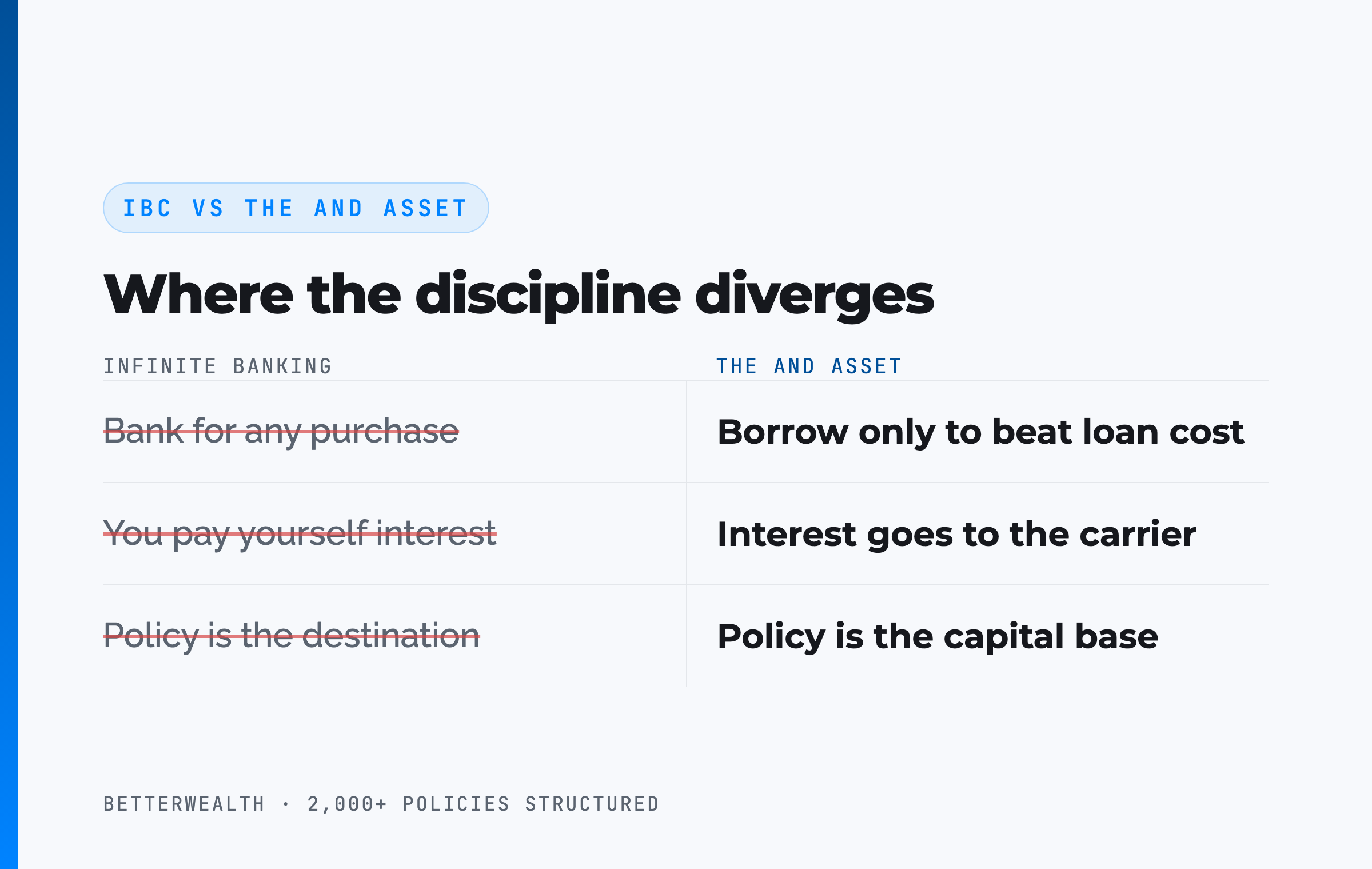

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to OneAmerica. Your return is what the deployed capital earns elsewhere while the policy compounds net of mortality and expense charges.

This distinction matters with OneAmerica specifically. The carrier's strengths are flexibility and access, which make casual spending easy. The discipline is on you, not the product.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the insurance company, and your return comes from what you deploy into.

03 / ConservatismWhy does a conservative carrier matter for a 30-year strategy?

Conservatism matters because The And Asset only works over a long horizon, and a long horizon rewards a carrier that prices honestly rather than chasing the illustration race. OneAmerica made a deliberate choice a few years ago to stop competing on illustrated numbers and stand behind conservative projections instead.

Two metrics frame the company. The first is the dividend: roughly $36.4 million declared in the most recent year, with no published dividend interest rate. Society of Actuaries data places the rate near 6.1%. That figure is gross. Your cash value does not grow at 6.1%. It grows at the dividend net of mortality and expense charges, which is the number that actually compounds inside the policy. We do not get caught up in the dividend hype, because we compare carriers on internal rate of return from the illustration, not on the headline rate.

The second metric is the lapse ratio, and almost nobody talks about it. OneAmerica sits at 4.7% from 2020 to 2025, just under the 5.1% industry average AM Best reported for 2023. That ratio tracks how many policies get surrendered, not how a policy performs against its illustration, so read it as a sign that policyholders tend to keep what they buy here. For a strategy you intend to hold for decades, retention like that is a quiet vote of confidence.

04 / How it worksHow does a OneAmerica policy actually function as an And Asset?

A OneAmerica policy functions as an And Asset through five mechanical steps, and the order matters. The product is Whole Life 95, designed for maximum cash value rather than maximum death benefit. Here is the sequence we use when we structure one.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as OneAmerica allows. The PUA rider is the engine. The carrier caps the maximum near a 25/75 base-to-PUA ratio, so the base premium will always be at least a quarter of total premium.

- Fund consistently. Choose a cashflow design (the same premium every year) or a front-load design (more in year one, then level). OneAmerica rewards long-term funding to the product limit, and a front-load under $100,000 gets you more early cash value than a larger one.

- Let the early years capitalize. First-year cash value on a cashflow design lands at 60 to 75% of premium. It climbs from there. Do not expect to break even on day one. You will not, and any illustration that shows it is fiction.

- Borrow against the policy. After about two weeks from initial funding, you can take a policy loan collateralized by your cash value. Because OneAmerica is non-direct recognition, the dividend stays the same whether or not the loan is outstanding.

- Deploy and repay. Put the borrowed capital into an activity that beats OneAmerica's loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

On the video's Whole Life 95 cashflow illustration, a 40-year-old male funding $50,000 a year reaches the capitalization point, where a year's growth exceeds the premium paid, around year four. Break-even, where total cash value catches total contributions, lands around year eight for a healthy individual. One detail worth flagging: the death benefit looks flat for about 13 years because a one-year renewable term rider sits on top, shrinking each year as permanent coverage grows underneath it.

Cashflow design versus front-load design

The two designs solve for different funding personalities. A cashflow design keeps the premium level year after year and produces a long-term IRR around 3 to 3.5% on current projections, with first-year cash value near 60 to 75%. A front-load front-ends a larger premium in year one, then drops to a level amount. With OneAmerica, the front-load behaves unusually: a front-load under $100,000 can push first-year cash value toward 90%, while a larger front-load pulls it back to that same 60 to 75% band.

That inversion is the tell. OneAmerica's design favors smaller policies. Most carriers reward more money with more efficiency. Here, under that $100,000 ceiling is where the front-load shines, with long-term IRR still in the 2.9 to 3.4% range. Neither design wins a growth race. They fit different cash-flow situations.

Smaller front-loads are where this carrier competes.

For a deeper walkthrough of how the PUA rider and base premium split drives all of this, we broke down policy structure here.

OneAmerica fits a specific person doing specific things.

It fits you if

- You value PUA flexibility and fast loan access over headline growth

- Your income is variable and you want catch-up room

- You want a long-term care option at the same carrier

- You can name a use for capital that beats the loan cost

It does not fit you if

- You want the highest possible cash value or IRR

- You live in New York

- You want a savings account, not a capital strategy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether OneAmerica or another carrier fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the return clear OneAmerica's loan cost?

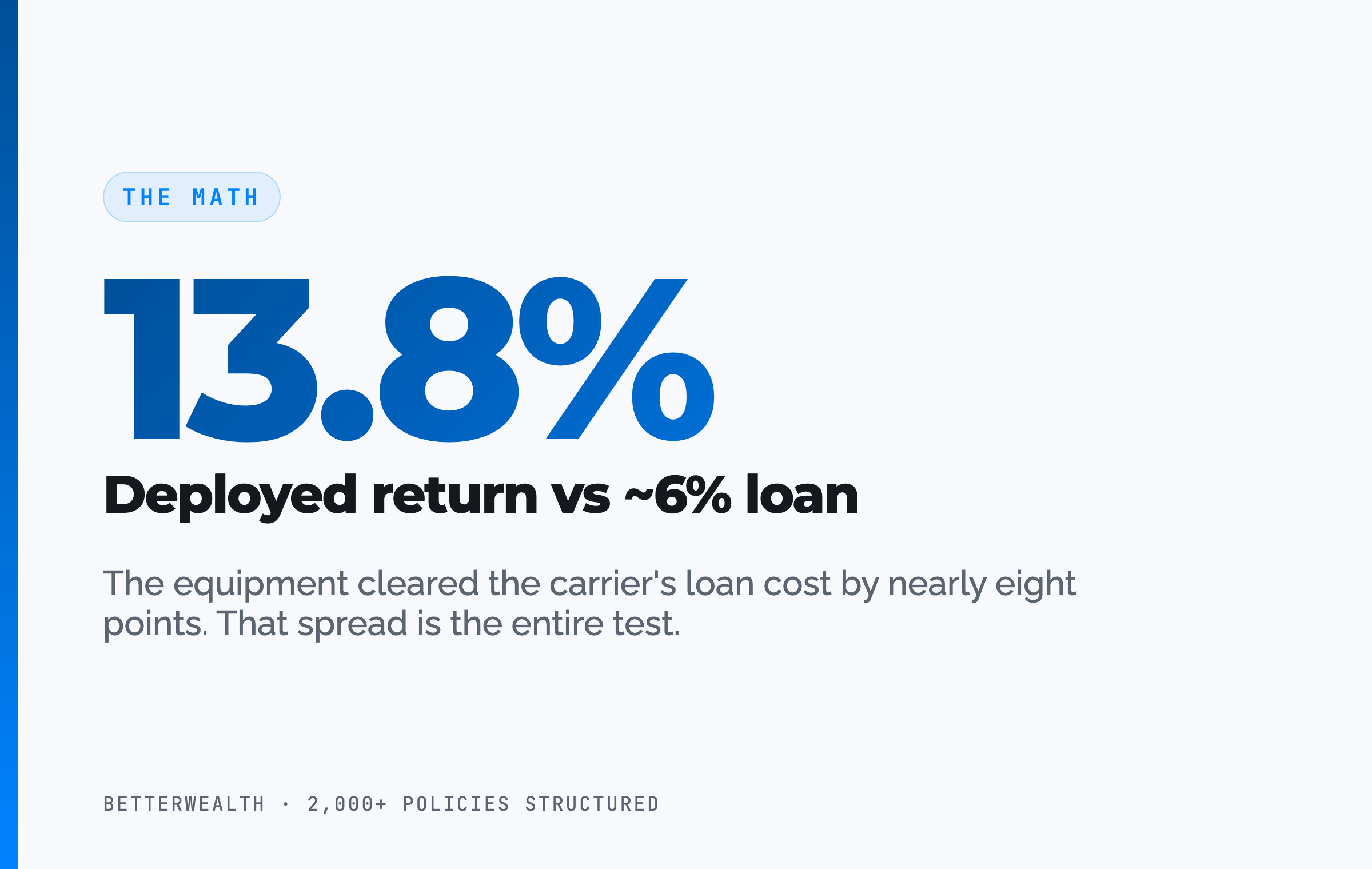

The return on whatever you deploy must exceed OneAmerica's loan cost, or you should not borrow. This is the entire test. OneAmerica uses a variable loan rate, so the number moves with the rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific rate as a variable to verify with OneAmerica, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, including the borrowed portion, and because OneAmerica is non-direct recognition, the dividend does not change while the loan is outstanding. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the policy has done two jobs with one dollar. If it is lower, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

06 / Non-direct recognitionWhy does non-direct recognition matter here?

Non-direct recognition matters because it makes the loan math simpler to track, which is a real convenience even though we do not treat the direct-versus-non-direct question as decisive. OneAmerica pays the same dividend whether or not you have a loan against the policy. There is no spread to adjust for and nothing to model differently when you borrow.

We take the stance that this feature is not as important as marketers make it. The carrier's overall value proposition, the policy design, and your funding discipline matter more. Many practitioners still choose OneAmerica partly because non-direct recognition is easier to explain to a client and easier to reason about year to year.

One quirk worth understanding: interest charged in advance

OneAmerica charges loan interest in advance, then credits it back as you repay. If you take a $10,000 loan, the carrier sets aside the $10,000 plus the year's interest up front. Pay the loan back halfway through the year and roughly half that interest is credited back to your available cash. You end up in the same place economically. It is just harder to read on the portal if you are not expecting it. Guardian handles loans the same way, so this is a known pattern, not a red flag.

Non-direct versus direct recognition is not the deciding factor people think it is. With OneAmerica, non-direct simply means a loan never changes your dividend, which keeps the math clean.

07 / Where it winsPUA flexibility, fast access, and a long-term care edge

OneAmerica's strongest features are flexibility, speed, and a hybrid long-term care line that no other dividend-paying mutual matches. These are the things that shape your experience for thirty years, long after the dividend comparison is forgotten.

Paid-up additions flexibility

OneAmerica has one of the most flexible PUA riders in the field. You can fund up to 3x the base premium at any point during the policy year, in any number of payments, all the way up to the MEC limit. A thousand dollars at a time across ten months works fine. The minimum to keep the rider active is just $120 a year, which is generous. If your cash flow swings, because you are in sales or run a seasonal business, this rider lets the policy ride out the swings. The one limit is the catch-up provision: a missed year can be backfilled only to the average of the prior three years, so funding to the maximum keeps your catch-up room hot.

Loan access that actually moves

OneAmerica offers some of the fastest loan access we have seen, with policy loans available about two weeks after initial funding. Small loans go through the online portal. Larger loans run through your agent or the carrier with signature verification for anti-money-laundering compliance. For a strategy built on actually using capital, speed is leverage.

The hybrid long-term care giant

OneAmerica leads the mutual market in hybrid long-term care. Its Asset Care and Annuity Care products are among the strongest in the industry, and it is one of the few dividend-paying mutuals with a serious hybrid LTC line. For a client who wants whole life and long-term care planning under one roof, that is a genuine edge. The LTC business also gives the company a revenue stream unrelated to life insurance, which supports its stability.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare carriers like OneAmerica, Penn Mutual, and Guardian. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the honest tradeoffs

OneAmerica's benefits come with tradeoffs that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, growth. OneAmerica illustrates in the bottom quarter against other top mutuals, with long-term IRR near 2.9 to 3.5%. Compared to the wider marketplace the product trails on cash value access, growth, and accumulation, so if maximum cash value or accumulation is your priority, this is a genuine reason to look elsewhere. Second, the PUA cap: the maximum design lands near a 25/75 base-to-PUA ratio, so you cannot push as much extra cash into the policy as a 10/90 design at another carrier allows. Third, conservative underwriting: we have seen OneAmerica come back with a standard rating where another carrier offered preferred plus, so a complex medical history may belong with a competing application. Fourth, growing pains: rapid practitioner adoption over the last few years has strained customer service and underwriting turnaround, and the illustration software is dated, functional but old school. And like most smaller carriers, OneAmerica does not operate in New York.

Against those tradeoffs sits the reason practitioners keep coming back. The PUA rider bends to almost any funding pattern, loan money shows up in about two weeks, and the hybrid long-term care line has no real peer among dividend-paying mutuals. The numbers are the price of admission for that experience.

A workhorse, not a racehorse. That is the trade.

The product falls on its face a lot of times when you compare it head to head on growth. That is exactly why we love the carrier in some situations and use it selectively in others.

The shape of a cashflow policy over its first decade

Consider a 40-year-old funding a OneAmerica Whole Life 95 policy at $50,000 a year on a cashflow design, the same profile Alden walks through in the video. The specific dollar figures depend on age, health class, and design, so treat these as the shape of a typical policy rather than a quote.

Through the first few years, cash value trails cumulative contributions, exactly as a real policy should. Around year four, each premium dollar starts adding more than a dollar of cash value. Around year eight, total cash value crosses total contributions. No earlier. Any illustration showing a year-two break-even is marketing fiction.

Once that cash value has built, the policy becomes a base to borrow against. The And Asset rule decides whether to act: only when a deployment, say revenue-producing equipment for the business, projects a return above OneAmerica's loan cost does borrowing make sense. Because OneAmerica is non-direct recognition, the dividend keeps paying as if no loan existed, and the policy compounds on its full value the entire time. The owner repays from the cash flow the deployment throws off.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and policy reviews are common with this carrier. On a discovery call, a practitioner looks at your specific situation and tells you whether a OneAmerica policy, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call09 / The fitWho is OneAmerica right for, and who isn't it?

OneAmerica is right for the entrepreneur or high-income earner who would trade a point of illustrated growth for a rider that flexes with their income and loan money they can reach in about two weeks, and who may want long-term care planning under the same roof. It fits the value creator with variable income who needs catch-up room, and the client who wants a smaller, well-designed policy where the front-load under $100,000 is competitive on early cash value.

It is the wrong carrier for someone chasing the highest cash value or long-term IRR, for a New York resident, or for anyone looking for a savings vehicle rather than a capital base. If you cannot name an activity that beats the loan cost, no carrier is right for you, and OneAmerica will not change that.

10 / Head to headOneAmerica against the alternatives

Compared to other carriers entrepreneurs actually consider, OneAmerica trades growth for flexibility, access speed, and a long-term care option. The table sets it against Penn Mutual and Guardian, the two carriers practitioners weigh it against most often, on the dimensions that matter for capital strategy.

| Dimension | OneAmerica WL 95 | Penn Mutual | Guardian |

|---|---|---|---|

| Long-term growth (illustrated IRR) | Lower: ~2.9 to 3.5% | Highest among top mutuals: ~4.2 to 5.3% | Mid: ~3.5 to 4.5% |

| Early cash value (year 1, cashflow) | 60 to 75% (near 90% on a sub-$100K front-load) | 77 to 87% | 80 to 87% |

| Loan recognition | Non-direct (dividend unaffected by loans) | Direct, guaranteed 0.65% spread yrs 1-10, 0% yr 11+ | Direct, fixed 5% for first 10 years |

| PUA flexibility | Most flexible: anytime payments, $120/yr minimum | Very flexible, full catch-up | Limited without the Q-Term rider |

| Standout edge | Hybrid long-term care (Asset Care), fast loan access | Long-term performance, ACE underwriting | Early cash value, brand strength |

Growth. Penn Mutual's projected long-term IRR runs roughly a point and a half higher than OneAmerica's at the top of the range. If accumulation is the goal, that gap compounds over decades and is hard to ignore.

Flexibility and access. OneAmerica wins here. The PUA rider funds anytime up to 3x base for a $120 annual minimum, and loan money is available in about two weeks. For a value creator with lumpy cash flow, that flexibility can outweigh a point of illustrated IRR.

The long-term care factor. Neither Penn Mutual nor Guardian offers a hybrid long-term care line like OneAmerica's Asset Care. A client who wants whole life and LTC planning at one carrier has a reason to choose OneAmerica that the growth numbers do not capture.

FAQOneAmerica infinite banking questions

Is OneAmerica good for infinite banking?

OneAmerica is an IBC-friendly carrier with a solid whole life product, the most flexible paid-up additions rider in the field, fast loan access, and non-direct recognition. Its weakness is below-average illustrated growth, so it fits a value creator who prizes flexibility, service, and a hybrid long-term care option over maximum cash value and IRR.

Is OneAmerica direct or non-direct recognition?

OneAmerica is a non-direct recognition carrier. Its dividend stays the same whether or not you have a policy loan outstanding, using a variable loan rate. That makes loan tracking simpler than under a direct-recognition carrier.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is OneAmerica available in New York?

No. OneAmerica does not sell its whole life products in New York. It operates in 49 states plus Washington DC. New York residents need a different carrier for an And Asset policy.

What is OneAmerica's dividend rate for 2026?

OneAmerica does not publish its dividend interest rate. Society of Actuaries data and recent rate increases place it near 6.1% for 2026, with roughly $36.4 million declared to policyholders. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges, and dividends are not guaranteed.

What is OneAmerica's best product for infinite banking?

OneAmerica's Whole Life 95, designed for maximum cash value, is the product used for And Asset and infinite banking style designs. It pairs a heavy paid-up additions rider with a one-year renewable term rider that keeps the early death benefit level while permanent coverage grows underneath it.

Why does OneAmerica have lower growth?

OneAmerica illustrates conservatively and prices for stability over headline numbers, so its long-term internal rate of return runs near 2.9 to 3.5% on current projections, in the bottom quarter among top mutuals. The cashflow design tops around 3.0 to 3.5% and the front-load around 2.9 to 3.4%. Dividends are not guaranteed, so only the projected numbers can be shown.

How fast can you access cash from a OneAmerica policy?

OneAmerica offers some of the fastest loan access in the industry, with policy loans available about two weeks after initial funding. Small loans can be initiated through the online portal, and larger loans go through your agent or the carrier with signature verification. Interest is charged in advance and credited back on repayment.

How flexible are OneAmerica's paid-up additions?

OneAmerica has one of the most flexible PUA riders in the field. You can fund up to 3x the base premium at any time during the policy year, in any number of payments, and keep the rider active with a $120 annual minimum. The catch-up provision is limited to the average of the prior three years, and the maximum PUA caps the design near a 25/75 base-to-PUA ratio.

What is OneAmerica's long-term care advantage?

OneAmerica leads the mutual market in hybrid long-term care through its Asset Care and Annuity Care products. Among mutual carriers that pay dividends on whole life, it is one of the few with a strong hybrid LTC line, which lets some clients pair an And Asset policy with long-term care planning at the same carrier.

OneAmerica vs Penn Mutual or Guardian for infinite banking?

OneAmerica wins on PUA flexibility, loan-access speed, and hybrid long-term care, and it is non-direct recognition. Penn Mutual leads on long-term IRR and is direct recognition with a guaranteed loan-to-dividend spread. Guardian leads on early cash value. The right carrier depends on policy design and your time horizon, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, OneAmerica's A+ (Superior) financial strength rating and industry lapse benchmarks.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- OneAmerica, declared dividend, Whole Life 95, and Asset Care product information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Specializes in policy structure and carrier comparisons across the IBC series, and walks through the OneAmerica Whole Life 95 illustrations in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a OneAmerica policy fits your plan, book a discovery call. We will tell you if it does not.