.png)

Guardian ranks among the top carriers for infinite banking in 2026 on early cash value, offering direct-recognition whole life with a guaranteed fixed 5% loan rate for the first 10 years and full New York availability. The tradeoff is weaker long-term funding and growth, which makes it a short-pay and front-load carrier, not a decades-of-level-funding one.

Pros

- Industry-leading early cash value (85 to 93%+ on front-loads)

- Direct recognition with a guaranteed fixed 5% loan rate for 10 years

- A++ (Superior) financial strength, COMDEX 100

- Sells in all 50 states, including New York

- Disability income and long-term care riders on whole life

Cons

- Long-term funding and growth lag (projected IRR tops out near 3.5 to 4.1%)

- No PUA backfill or catch-up provision

- Q-Term rider gets more expensive each year it stays on

- High design complexity, rated 7/10 on the consumer complexity test

- PUA capacity drops to 1x base premium after year 10

The most popular question we get about infinite banking is which insurance company to choose, and the honest answer is that it depends on what you are trying to do with the policy. People compare dividend rates the way shoppers compare APYs, pick the highest number, and assume the carrier choice is the decision. It is not. The dividend rate is one input among several, and it tells you almost nothing about whether a policy will function the way you need it to.

The product, its design, and your understanding of how to use it matter far more than which top mutual is printed on the contract. Guardian is a strong carrier. It is also widely misread, sold by some agents as a no-compromise winner and dismissed by others for a long-term-funding weakness that is irrelevant to the right buyer.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and Guardian shows up often on the short list when a client needs early cash value or lives in New York. This review covers what the company actually is, how its Whole Life 95 product behaves under both a cashflow and a front-load design, the math that decides whether borrowing against it makes sense, and the honest tradeoffs nobody puts in a sales deck. We will also tell you who Guardian is not for.

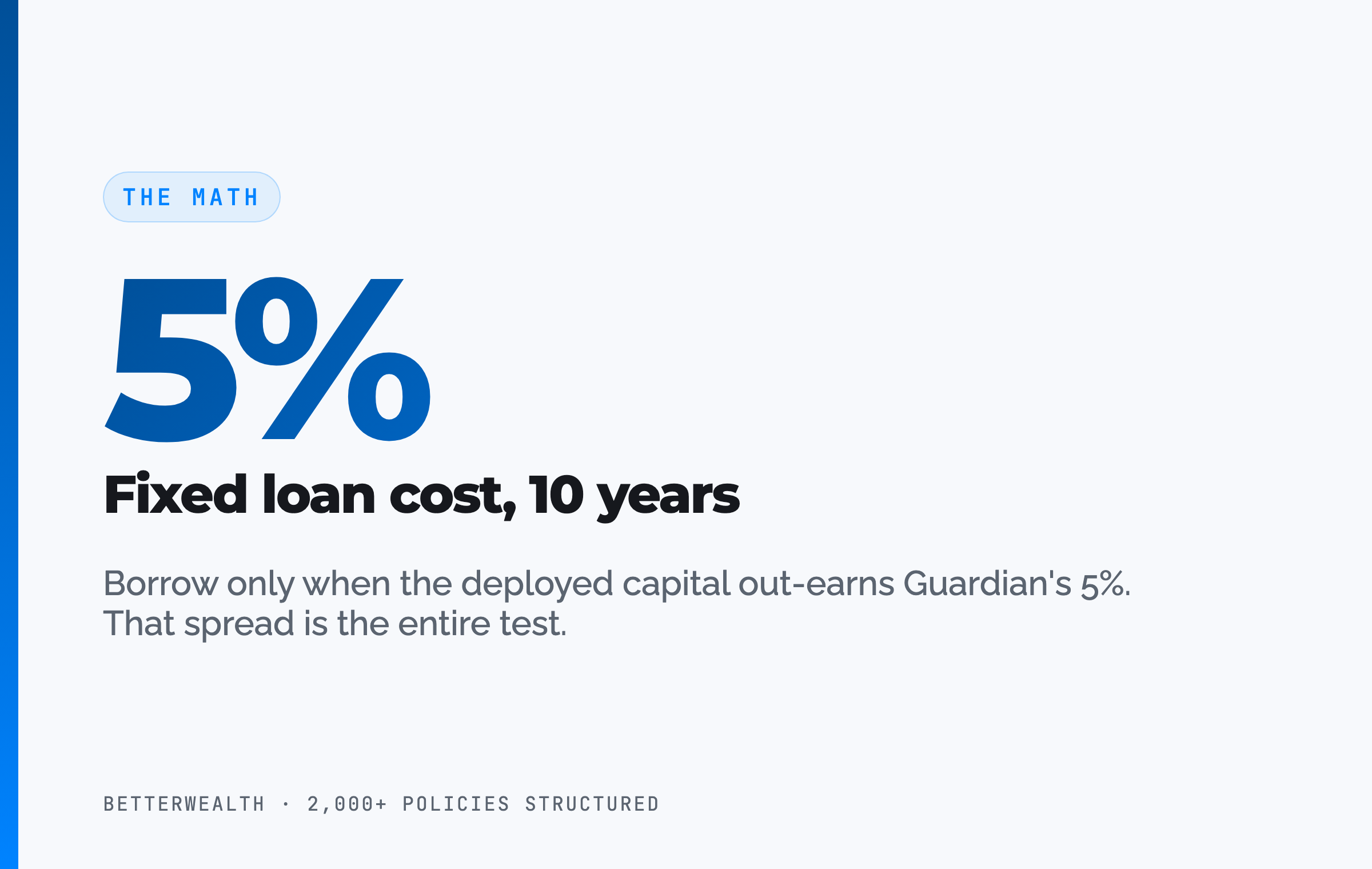

- Guardian is a direct-recognition carrier that guarantees a fixed 5% loan rate for the first 10 policy years, regardless of the rate environment.

- Its strength is early cash value, reaching 85 to 93%-plus of premium in year one on a front-load design.

- Its weakness is long-term funding: the Q-Term rider gets costlier yearly and PUA capacity drops to 1x base after year 10.

- The And Asset rule still governs: only borrow when the deployed return clears Guardian's 5% loan cost.

- Guardian sells in all 50 states including New York, where many competing carriers cannot operate.

- Guardian offers a waiver of premium rider that covers scheduled paid-up additions, not just the base premium, if you become disabled.

If you want to see the actual policy illustrations behind these numbers, Alden walks through both the cashflow and front-load designs on screen, including the year-by-year cash value and the term-insurance mechanics that drive Guardian's results:

01 / The problemWhat carrier choice actually solves (and what it doesn't)

Carrier choice solves for a handful of structural questions, not for the headline dividend rate. The real questions are whether the company will still be paying dividends in forty years, whether its loan mechanics and recognition type fit how you plan to use capital, and whether its product can be designed to push cash value where you need it without triggering a Modified Endowment Contract.

Guardian answers the stability question convincingly. A company founded in 1860, mutual since 1925, paying dividends for 157 years, rated COMDEX 100 and AM Best A++ (Superior), is not a stability risk. The harder questions are about design and funding horizon, which is where this review spends most of its time.

"The product, its design, and your understanding are what matter most. The carrier choice among top mutuals is secondary." That is how Alden Armstrong puts it, and it is the right way to read this whole review.

02 / The frameworkWhat does it mean to run infinite banking with Guardian?

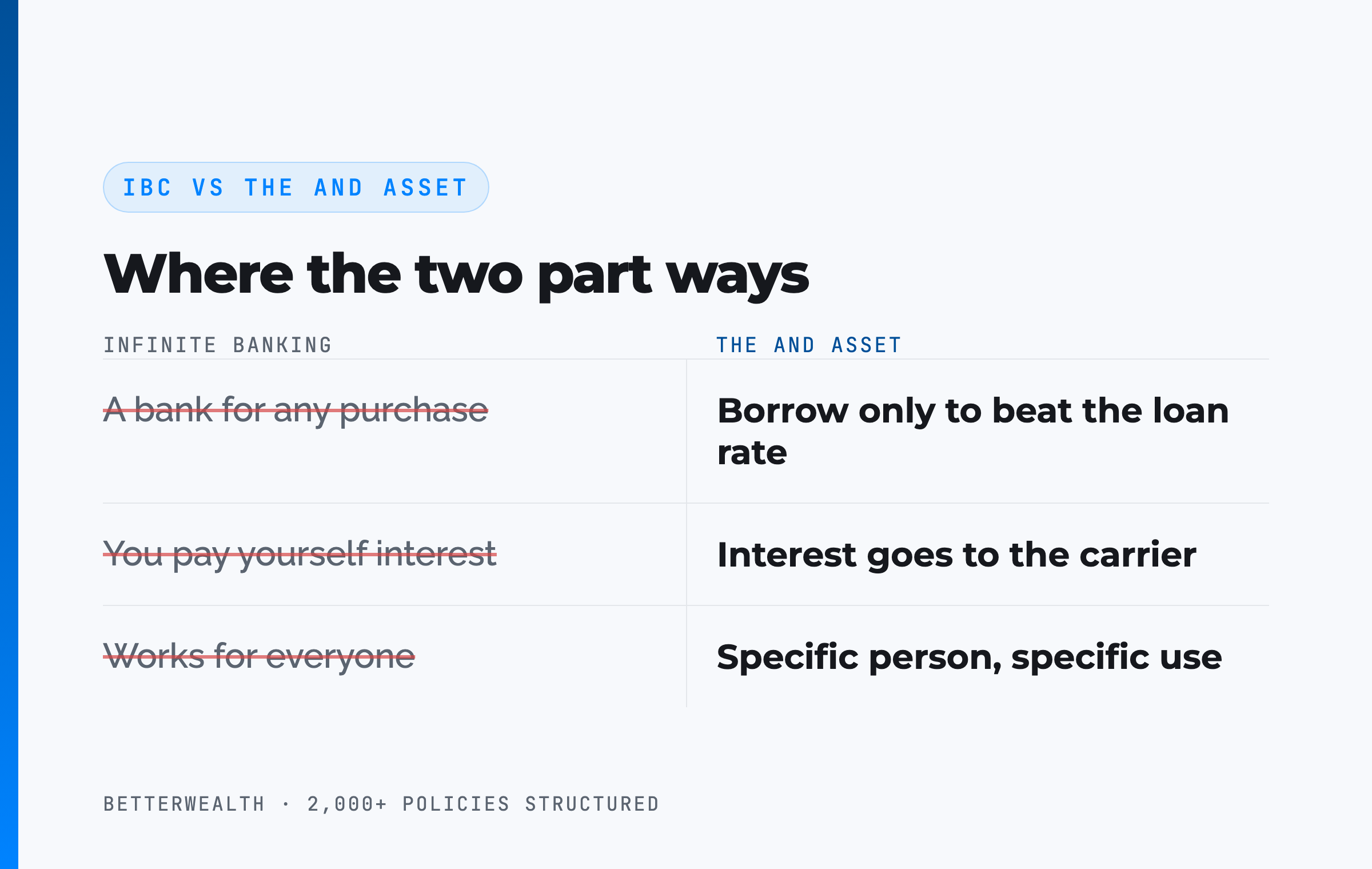

Running infinite banking with Guardian means using a properly structured Guardian whole life policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top of it is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to Guardian. Your return is what your deployed capital earns elsewhere while the policy compounds uninterrupted.

The distinction carries weight here because Guardian's fixed 5% loan rate gives the disciplined version of this strategy a known threshold to clear. When you can name your cost of borrowing in advance, the math gets simpler.

If the spread is not there, the strategy is not there.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. You are paying the insurance company, and your return comes from what you deploy into.

03 / Financial strengthWhy does Guardian's stability matter for this strategy?

Guardian's stability matters because The And Asset depends on the carrier still performing as illustrated years from now, and stability is the only thing that guarantees the contract you sign today behaves the way it should later. A company that pays generously this year but chases low-quality business will not perform the same way in year 25.

Two metrics tell the real story. The first is the dividend: roughly $1.7 billion declared for 2026 at a projected 6.25% rate. The dividend rate is gross. Your cash value does not grow at 6.25%. It grows at the dividend net of mortality and expense charges, which is the figure that actually compounds inside the policy. Any agent quoting the gross rate as your growth rate is either careless or selling.

The second metric is the lapse ratio, and almost nobody talks about it. Guardian's lapse ratio sits at 3.3% from 2020 to 2025, against a 5.1% industry average. A low lapse ratio means policyholders are keeping their policies, which means the policies are doing what the illustrations promised. It is a satisfaction signal hiding inside an actuarial table. When agents oversell a policy and the client leaves anyway, that shows up as a bad lapse rate. Guardian's is well below average. One honest caveat: Guardian markets heavily to affluent, high-income buyers, who lapse less often than the general population regardless of product, so part of that low number reflects the clientele, not just the contract.

04 / How it worksHow a Guardian policy actually functions as an And Asset

A Guardian policy functions as an And Asset through five mechanical steps, and the order matters. The product is Whole Life 95, designed for maximum early cash value rather than maximum death benefit. Here is the sequence we use when we structure one.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider. With Guardian, the engine is the Q-Term rider, which lets you fund up to 10x base premium in PUA while it is on the policy. The base/PUA split is the single design decision that determines early cash value.

- Fund on a short horizon. Choose a cashflow design (level premium) or a front-load design (more in year one, then level). Guardian performs best with 7 to 15 years of funding, because the Q-Term rider gets more expensive every year it stays on the contract.

- Let the early years capitalize. First-year cash value lands around 80 to 88% of premium on a cashflow design and 85 to 93%-plus on a front-load. Note that Guardian's illustrations run one year conservative: they do not show the end-of-year-one dividend, which rolls into the next year.

- Borrow against the policy. About 30 days after initial funding, you can take a policy loan collateralized by your cash value, at Guardian's guaranteed fixed 5% rate for the first 10 years. The death benefit and cash value still belong to you. You are borrowing against them, not withdrawing.

- Deploy and repay. Put the borrowed capital into an activity that beats the 5% loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

On a well-designed Guardian cashflow policy, the capitalization point, where a dollar of premium adds more than a dollar of cash value, arrives as early as year two. Break-even, where total cash value catches total contributions, typically lands around year five on a cashflow design and year four on a front-load. Do not expect day-one break-even. You will not get it, and any illustration that promises it is not telling the truth.

Cashflow design versus front-load design

The two designs solve for different funding personalities. A cashflow design keeps the premium level, year after year, and lands first-year cash value in the 80 to 88% range, with break-even around year five and steady compounding after that. A front-load design front-ends a larger premium, then drops to a level amount, reaches 85 to 93% cash value in year one, and pulls break-even forward to about year four. Exact year-by-year values depend on age, health rating, and the base/PUA split, so run a current illustration before you anchor on any single number.

Front-loading buys more term insurance to justify the early premium, and that Q-Term gets expensive fast, so Guardian front-loads work best on a 10-year-or-shorter pay. You trade long-term funding capacity for more capital working sooner. Neither design is "better." They fit different people.

Early cash value is where Guardian wins.

Guardian fits a specific person doing specific things.

It fits you if

- You want maximum cash value in years one to five

- You plan to short-pay or front-load (10 to 15 years)

- You value a known, fixed cost of borrowing

- You live in New York and need an A++ carrier

It does not fit you if

- You plan to fund level premiums for decades

- You are chasing the highest long-term IRR

- You need a PUA backfill or catch-up provision

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether Guardian or another carrier fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the return clear Guardian's loan cost?

The return on whatever you deploy must exceed Guardian's loan cost, or you should not borrow. This is the entire test. Guardian's advantage here is that its loan cost is fixed and known: a guaranteed 5% for the first 10 policy years, regardless of where prime rates sit. Most carriers tie the loan rate to the rate environment, so you are estimating a moving cost. With Guardian, the threshold is a hard number.

Here is the structure of the decision. You borrow at 5%. Your policy keeps compounding on its full cash value, including the borrowed portion, adjusted by Guardian's direct recognition. Your deployed capital earns its own return. If that return is higher than 5%, you are ahead on the spread, and the policy has done two jobs with one dollar. If it is lower, you have borrowed money to lose money slowly.

If the deal does not clear 5%, do not borrow.

06 / Direct recognitionWhy does Guardian's direct recognition actually help?

Direct recognition helps here because Guardian uses it to guarantee a fixed 5% loan rate, which removes the single biggest unknown in the borrowing decision. Guardian is a direct recognition carrier. When you borrow, the dividend on the borrowed portion can be adjusted up or down depending on the rate environment, the same mechanism we covered in our Penn Mutual review. The difference is the loan rate itself: fixed at 5% for 10 years.

The common fear about direct recognition is that borrowing drags your dividend down. Sometimes it does, and sometimes the carrier adjusts it up. Guardian's design trades a little dividend variability for a guaranteed cost of borrowing, which is exactly what a disciplined capital plan wants.

Why a fixed loan rate matters for active deployers

Picture a real estate investor who borrows against the policy to fund a deal. With a variable-rate carrier, the cost of that loan moves with the market, so the spread between your deployed return and your borrowing cost shifts under you. With Guardian, the cost is locked at 5% for a decade. You can underwrite a deal knowing the loan side of the math will not change. From year 11 on, most Guardian whole life products let you keep a fixed rate, switch to variable, or maintain direct recognition. Knowing your cost of borrowing in advance is a real edge when you are underwriting a syndication or a rental acquisition.

Direct recognition is not the dirty word people think it is. With Guardian it locks your cost of borrowing at 5% for 10 years, which makes a deployment decision cleaner, not harder.

07 / Where it winsEarly cash value, fixed loan rate, and living-benefit riders

Guardian's strongest features are early cash value, a known cost of borrowing, and a set of living-benefit riders rare in the whole life market. These are the features that shape your experience long after the dividend comparison is forgotten.

Early cash value and short-pay strength

Guardian leads the charge on first-year cash value. On a front-load it can reach 92% in year one, with the capitalization point hitting as early as year two, meaning the second year you put in a dollar and have more than a dollar of cash value available that same year. Cases we take to Guardian almost always center on early cash value from a front-load, paired with short funding. This is where they excel.

The fixed 5% loan rate

Knowing your exact cost of borrowing every time you borrow is the feature long-term loan users care about most. For real estate investors, syndication partners, and business owners running money through the policy, a guaranteed 5% for 10 years removes a variable from every deal. One nuance: Guardian charges the full year of loan interest up front, so the portal shows the whole year's interest as due. Repay early within the policy year and they credit it back. You do not lose it, but it reads less cleanly than daily accrual.

Disability income and long-term care riders

Guardian writes a large share of its business in disability income for white-collar professionals, and it lets you add disability income and long-term care acceleration riders to its whole life products. A single contract can carry cash value, a death benefit, and living-benefit riders for disability income and long-term care. Guardian also offers a waiver of premium rider that covers scheduled paid-up additions, not just the base premium, if you become disabled, which keeps a high-cash-value design funding itself through a disability. That rider costs extra and can be expensive, but the fact that it covers PUAs at all is uncommon in the market.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare carriers like Guardian, Penn Mutual, and MassMutual. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the honest tradeoffs

Guardian's benefits come with tradeoffs that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, long-term funding and growth lag. The Q-Term rider that makes early cash value so strong gets more expensive every year, and PUA funding capacity drops to 1x base premium after year 10. Fund level premiums for 20-plus years and Guardian becomes inefficient, with projected long-term IRR topping out around 3.5 to 4.1%. Penn Mutual, built for long horizons, projects roughly 4.2 to 5.3% over the same window, so on a multi-decade level-funded plan you are leaving close to a full percentage point of IRR on the table. Compounded over 30 years, that gap is real money.

Second, there is no PUA backfill: miss a year of paid-up additions and you cannot make it up later. Third, this is a complex product. Guardian rates a 7 out of 10 on the consumer complexity test, and IBC-style or front-load approvals can take finesse because the company is large, traditional, and careful about non-standard funding. Fourth, the commission structure is back-loaded, which matters to advisors more than clients but is worth knowing. And one more thing buyers should hear plainly: Guardian does not market or endorse infinite banking as a strategy. It is a white-collar carrier selling to high-income professionals whose products happen to be well suited to high early cash value. You are using the product against the grain of how the company positions it, which is fine, but it means design and approval lean on your team, not Guardian's marketing.

Against those tradeoffs sits the strength that defines the company: early cash value and a fixed cost of borrowing that few carriers match. If your plan is short-pay or front-load, the long-term gap may never touch you. If it is decades of level funding, that gap is the reason to look elsewhere.

This is not for everyone, and Guardian is not for everyone. If you plan to fund level premiums for decades, the Q-Term cost and PUA limits work against you, and another carrier probably fits better.

09 / The fitWho is Guardian right for, and who isn't it?

Guardian is right for the entrepreneur or real estate investor who wants maximum early cash value, a known cost of borrowing, and a short-pay or front-load funding plan. It fits the value creator who will move a lot of capital through the policy in the first 10 years and who can name productive uses for borrowed dollars that beat 5%. It is also one of our premier choices for New York residents, who cannot use several competing carriers.

It is the wrong carrier for someone who plans to fund level premiums for decades, who is chasing the highest possible long-term IRR, or who needs the flexibility of a PUA catch-up provision. If you cannot identify an activity that beats the 5% loan cost, no carrier is right for you, and Guardian will not change that.

10 / Head to headGuardian against the other top mutuals

Compared against the other carriers entrepreneurs actually weigh, Guardian trades long-term growth for early cash value and a fixed cost of borrowing. The table sets it against Penn Mutual, MassMutual, and New York Life on the dimensions that matter for an And Asset design.

| Dimension | Guardian | Penn Mutual | MassMutual | New York Life |

|---|---|---|---|---|

| Loan recognition | Direct; fixed 5% for 10 years | Direct; 0.65% spread yrs 1-10, 0% yrs 11+ | Non-direct (variable) | Non-direct (variable) |

| Year-1 cash value (cashflow) | 80 to 88% | 77 to 87% | 75 to 85% | 80 to 87% |

| Long-term IRR (projected) | 3.5 to 4.1% | 4.2 to 5.3% | 3.8 to 4.9% | 3.6 to 4.7% |

| PUA flexibility | Moderate; no backfill | Most flexible; full catch-up | Least flexible (ALIR/PALIR) | Limited; no backfill |

| New York | Available | Not available | Available | Available |

Recognition and loan cost. Guardian and Penn Mutual are both direct recognition, but Guardian fixes the loan rate at 5% for 10 years while Penn Mutual guarantees a spread. MassMutual and New York Life are non-direct, so their loan rate floats with the rate environment.

Early cash value vs long-term growth. Guardian's 80 to 88% year-one cashflow access is at the top of this group, but its projected 3.5 to 4.1% long-term IRR is the lowest of the four. Penn Mutual reverses that profile: lower early access, stronger long-term growth. MassMutual and New York Life sit in between, both non-direct recognition.

New York and flexibility. Guardian is one of the carriers that can write in New York, which Penn Mutual cannot. On PUA flexibility, Penn Mutual leads with full catch-up provisions, while Guardian offers no backfill at all. For the full field, see our guide to the best life insurance companies for infinite banking.

A composite: the real estate investor who deployed at year six

Consider a 43-year-old real estate investor, preferred non-tobacco, funding a Guardian Whole Life 95 policy on a front-load design: $94,000 in year one, then $47,000 per year through year 10. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By the second year, each premium dollar already adds more than a dollar of cash value, the capitalization point Guardian reaches early. At year four, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year six, with roughly $334,000 of accessible cash value, the investor borrows $148,000 against the policy at Guardian's guaranteed 5% to fund the down payment and rehab on a rental property. The property returns an estimated 13.2% IRR through cash flow and forced appreciation. The loan cost is fixed at 5%, so the spread works in the investor's favor by more than eight points. The policy keeps compounding on its full value the entire time. Repayment runs on a 44-month schedule funded by the rental's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a Guardian policy, another carrier, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQGuardian infinite banking questions

Is Guardian good for infinite banking?

Guardian is one of the strongest carriers for early cash value and short-pay designs in 2026, with direct recognition, a guaranteed fixed 5% loan rate for the first 10 years, and A++ financial strength. Its weakness is long-term funding and growth, so it fits a front-load or short-pay strategy rather than decades of level funding.

Is Guardian direct or non-direct recognition?

Guardian is a direct recognition carrier. It guarantees a fixed 5% loan rate for the first 10 policy years regardless of the rate environment. From year 11 onward, most whole life products let you choose a fixed or variable loan rate.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is Guardian available in New York?

Yes. Guardian sells its whole life products in all 50 states including New York, which makes it one of our premier carriers for New York residents when the design fits. Many competing carriers, including Penn Mutual, cannot operate in New York.

What is Guardian's dividend rate for 2026?

Guardian's projected dividend interest rate for 2026 is 6.25%, with roughly $1.7 billion declared to policyholders. The dividend rate is gross. Actual cash value growth is the dividend net of mortality and expense charges. Dividends are declared annually by the board and are not guaranteed.

What is Guardian's best product for infinite banking?

Guardian's Whole Life 95, designed for maximum early cash value, is the product used for And Asset and infinite banking style designs. It is built with a Q-Term rider that allows up to 10x base premium in paid-up additions to accelerate early cash value while staying under the MEC limit.

Does Guardian have a paid-up additions backfill option?

No. Guardian does not offer a backfill or catch-up provision on its PUA rider, so a year of missed paid-up additions cannot be made up later. While the Q-Term rider is on the policy you can fund up to 10x base premium; without it you are limited to 3x base in years 1 to 10 and 1x base from year 11 on.

How fast can you access cash from a Guardian policy?

Guardian allows policy loans about 30 days after initial funding. Smaller loans can be requested through the online portal, and larger loans go through your agent or the carrier with a signature. Guardian charges the full year of loan interest up front and credits it back if you repay early within the same policy year.

Why does Guardian's long-term performance lag?

Guardian builds its high-cash-value policies with a one-year renewable Q-Term rider that gets more expensive every year it stays on the policy, and PUA funding capacity drops to 1x base premium after year 10. That combination makes decades of level funding inefficient, so Guardian's projected long-term IRR tops out around 3.5 to 4.1%, behind carriers like Penn Mutual that are built for long-horizon funding.

Guardian vs Penn Mutual or MassMutual for infinite banking?

Guardian is direct recognition with a fixed 5% loan rate and industry-leading early cash value, best for short-pay and front-load designs. Penn Mutual is direct recognition with the strongest long-term growth. MassMutual and New York Life are non-direct recognition. The right carrier depends on your funding horizon and design, not the dividend rate alone.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, Guardian's A++ (Superior) financial strength rating.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- Guardian Life, declared dividend and product information.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Leads policy structure and carrier comparisons across the IBC series, and walks through the Guardian cashflow and front-load illustrations in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a Guardian policy fits your plan, book a discovery call. We will tell you if it does not.