.png)

Life insurance is generally not taxable: the death benefit is income-tax-free to beneficiaries under IRC Section 101(a), and cash value grows tax-deferred. Taxes apply only in specific cases, including a transfer-for-value sale, estate inclusion when the insured owns the policy, interest on a delayed payout, or a surrendered policy with a gain.

The tax treatment of life insurance is one of the few genuine advantages left in the tax code, and it is the part people understand the least. A reader hears "tax-free" from a marketer and "too good to be true" from a skeptic, and neither one tells them what is actually written in the statute. The truth sits in between, and it is more useful than either headline.

A life insurance death benefit is excluded from the beneficiary's income under IRC Section 101(a), cash value grows tax-deferred, and a properly structured policy loan is not a taxable event. Those three facts carry almost the entire topic. The exceptions are specific, and they matter, but they do not undo the general rule. They define its edges.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and tax questions come up on nearly every call. Most of the confusion is avoidable. This guide walks the whole picture in plain language: whether a payout is taxed, how cash value and policy loans are treated during your life, whether premiums are deductible, and the handful of situations that flip a tax-free benefit into a taxable one. We will cite the relevant tax code where it is settled and skip the speculation where it is not.

- A life insurance death benefit is generally income-tax-free to the beneficiary under IRC Section 101(a), whether paid to a person, trust, or business.

- Three exceptions make proceeds taxable: a transfer-for-value sale, estate inclusion when the insured owns the policy, and interest on a delayed payout.

- Cash value grows tax-deferred; you only owe income tax if you surrender or lapse the policy with a gain above your basis.

- A loan against a non-MEC policy is not taxable income, because you are borrowing against cash value, not withdrawing it.

- Personal premiums are not deductible; narrow business cases exist, such as employer-paid group term under IRC Section 79.

- A Modified Endowment Contract is taxed gain-first on loans and withdrawals, which is why And Asset policies are designed to stay non-MEC.

01 / The short answerIs life insurance taxable, yes or no?

Life insurance is not taxable in the way that matters most: the death benefit your beneficiaries receive is free from federal income tax. IRC Section 101(a) excludes "amounts received under a life insurance contract, if such amounts are paid by reason of the death of the insured" from gross income. That is the rule that covers the overwhelming majority of policies and payouts.

The reason this question generates so much confusion is that "life insurance" describes two different things at once. There is the death benefit, paid when the insured dies. And there is the living value of a permanent policy, the cash value that builds inside whole life or universal life. They are taxed under different rules. Most people asking whether life insurance is taxable are thinking about the payout. Some are thinking about the cash value. The answer is favorable for both, but the mechanics differ, so we will take them in turn.

Term life insurance has no cash value, so for a term policy the entire tax story is the death benefit, and the death benefit is income-tax-free. Permanent policies add the living tax treatment on top.

"Tax-free" is accurate, but it is not magic. It is a specific exclusion written into the code, with specific edges. Knowing the edges is what protects the benefit.

02 / The payoutAre life insurance proceeds taxable to the beneficiary?

In most cases, no. A death benefit paid because the insured died passes to the beneficiary free of federal income tax, and the beneficiary does not report it as income. A spouse, an adult child, a business partner, or a trust named as beneficiary all receive the proceeds under the same Section 101(a) exclusion. This holds for term and permanent policies alike. We cover the payout side in depth in Are Life Insurance Proceeds Taxable?, but the headline is simple: the lump sum is not taxed.

The one routine exception is interest. When a beneficiary chooses to receive the death benefit in installments instead of a lump sum, or when the insurer holds the money and pays it out over time, the insurer pays interest on the unpaid balance. The original death benefit stays tax-free. The interest is taxable income, and the insurer reports it on a Form 1099-INT. If you want the cleanest tax outcome, a lump sum keeps the entire amount on the tax-free side of the line.

The principal is tax-free. The interest on top of it is not.

03 / The exceptionsWhen does a life insurance death benefit become taxable?

A death benefit becomes taxable in three specific situations, and each one has a clear cause. These are the cases that send people searching, and the cases agents tend to skip. Here they are without the gloss.

1. The transfer-for-value rule

If a life insurance policy is sold or transferred for valuable consideration, the death benefit can lose its tax-free status. This is the transfer-for-value rule under IRC Section 101(a)(2). When it applies, the proceeds above what the new owner paid, plus the premiums they later paid, become taxable as ordinary income. It catches people in business buyouts, policy sales, and sloppy ownership transfers.

There are safe-harbor exceptions that preserve the exclusion: transfers to the insured, to a partner of the insured, to a partnership the insured is a member of, or to a corporation in which the insured is a shareholder or officer. The rule is technical, and the cost of getting it wrong is a taxable death benefit, so an ownership change on an existing policy is a moment to involve a tax advisor.

2. Estate inclusion when the insured owns the policy

The death benefit is income-tax-free even when it is pulled into the taxable estate, but estate tax is a separate tax from income tax. Under IRC Section 2042, if the insured held "incidents of ownership" in the policy at death, the right to change the beneficiary, to borrow against it, to surrender it, the death benefit is included in the gross estate. The federal estate-tax exemption is high enough that most estates owe nothing. Larger estates, and estates in states that levy their own estate or inheritance tax, are where this bites.

The fix is ownership. When a policy is owned by an irrevocable life insurance trust rather than by the insured, the proceeds sit outside the estate. We walk through ownership structure and the estate question in How to Avoid Tax on Life Insurance Proceeds.

3. Interest on a delayed or installment payout

The third case is the interest point from the section above. Whenever the insurer pays interest on a benefit it held or paid in installments, that interest is taxable even though the underlying death benefit is not. It is the most common of the three, and the smallest in dollar terms.

Nobody plans to trigger the transfer-for-value rule. They trigger it by moving a policy in a business deal without checking the safe harbors. The tax bill is the death benefit itself.

04 / The living valueIs the cash value of life insurance taxable?

Cash value grows tax-deferred, which means the annual growth inside a permanent policy is not taxed as it accumulates. A whole life policy builds cash value year after year through guaranteed growth and dividends, and none of that internal growth shows up on your tax return while it stays inside the policy. This deferral is the feature that makes permanent life insurance useful as a capital base rather than just a death benefit.

A point on the growth itself, because marketers get it wrong constantly. The cash value does not compound at the headline dividend rate. It compounds at the dividend net of the policy's mortality and expense charges, which is the figure that actually accumulates inside the contract. Any pitch that quotes the gross dividend rate as your growth rate is overstating the number.

A tax event happens only when you take the gain out and end the policy's protection. If you surrender or let the policy lapse and the cash value you receive exceeds your cost basis, the premiums you paid in, the gain above basis is taxed as ordinary income. Hold the policy, and that gain stays deferred. The mechanics of how Section 7702 governs this living tax treatment are the subject of The Tax-Free Strategy: How Section 7702 Protects Wealth.

05 / Policy loansAre life insurance policy loans taxable?

A loan against a properly structured, non-MEC policy is not taxable income. This is the part of the tax treatment that does the heavy lifting in a capital strategy. When you take a policy loan, you are not withdrawing your cash value. You are borrowing against it, using the cash value as collateral, and a loan is not a taxable distribution. The policy keeps compounding on its full value while the loan is outstanding.

Two things can turn a loan into a taxable event. The first is a Modified Endowment Contract, which we cover next. The second is letting the policy lapse or surrendering it while a loan is outstanding. If that happens and there is a gain, the outstanding loan is treated as a distribution, and the gain becomes taxable income, sometimes a painful surprise because the cash to pay the tax already went out the door as the loan. Keeping the policy in force is what keeps the loan access tax-free.

Why the loan treatment matters for a capital strategy

This is the tax mechanic that makes The And Asset function. You access capital through a non-taxable loan while the underlying policy continues to compound, which is how the same dollar can do two jobs. The tax treatment is necessary, but it is not the strategy by itself. The discipline is the strategy.

A loan is not income. A surrendered policy with a gain is.

The tax treatment is a tool, not a reason on its own.

The cash-value angle fits you if

- You are an entrepreneur or high-income earner already deploying capital

- You want tax-deferred growth plus non-taxable access to capital

- You can name a use for borrowed dollars that beats the loan cost

- You have a 10-year-plus horizon

It does not fit you if

- You only need a death benefit (term life is cheaper and tax-free too)

- You are chasing a tax dodge with no capital plan behind it

- You want a savings account, not a capital base

- You would fund it past the MEC limit for the tax break alone

If you are in the first column, a 30-minute conversation will tell you whether a properly designed policy fits. If you are in the second, we will tell you that too.

Book a Discovery Call06 / The MEC lineWhat is a Modified Endowment Contract, and why does it change the tax?

A Modified Endowment Contract is a life insurance policy funded faster than the IRS allows, and it changes how money comes out during your life. Congress created the MEC rules under IRC Section 7702A to stop people from stuffing a policy with cash purely for the tax-free loan access. If your funding crosses the 7-pay limit, a test that caps how much premium can go in over the first seven years relative to the death benefit, the policy is permanently classified as a MEC.

The consequences are specific. Loans and withdrawals from a MEC are taxed gain-first, meaning the growth comes out first and is taxed as ordinary income, and a 10% penalty can apply if you are under age 59 and a half. The death benefit of a MEC is still income-tax-free. The change is entirely on the living, distribution side.

This is why policy design matters for tax outcomes, not just for growth. A policy built for The And Asset is deliberately structured with enough death benefit and a controlled funding schedule to stay under the MEC limit, so loans remain non-taxable. Overfund it past the line for the tax break, and you lose the very treatment you were funding it for.

The MEC limit is the one number where "more premium" can make the tax treatment worse. Crossing it converts your tax-free loan access into a taxable distribution problem.

07 / PremiumsAre life insurance premiums tax deductible?

Personal life insurance premiums are not tax deductible. The IRS treats them as a personal expense, the same category as your mortgage payment or your groceries, so you pay them with after-tax dollars. This catches people off guard because so much of life insurance's tax advantage sits on the back end, but the premium itself buys you no deduction. We go deeper on the deductibility question in Is Life Insurance Tax Deductible?

The business side has a few narrow openings, and they are narrow on purpose. Employer-paid group term life insurance up to $50,000 of coverage is a deductible business expense and tax-free to the employee under IRC Section 79; coverage above $50,000 creates imputed income to the employee. A business generally cannot deduct premiums on a policy where the business itself is the beneficiary, under the disallowance rules of IRC Section 264. Certain alimony-related and charitable arrangements have their own treatment. None of these turn personal coverage into a deduction.

You fund the premium with after-tax dollars. The advantage comes later.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to keep policies non-MEC, tax-efficient, and built for capital access. Free, email-gated, no spam.

Open the Vault08 / The frameworkWhere The And Asset fits the tax picture

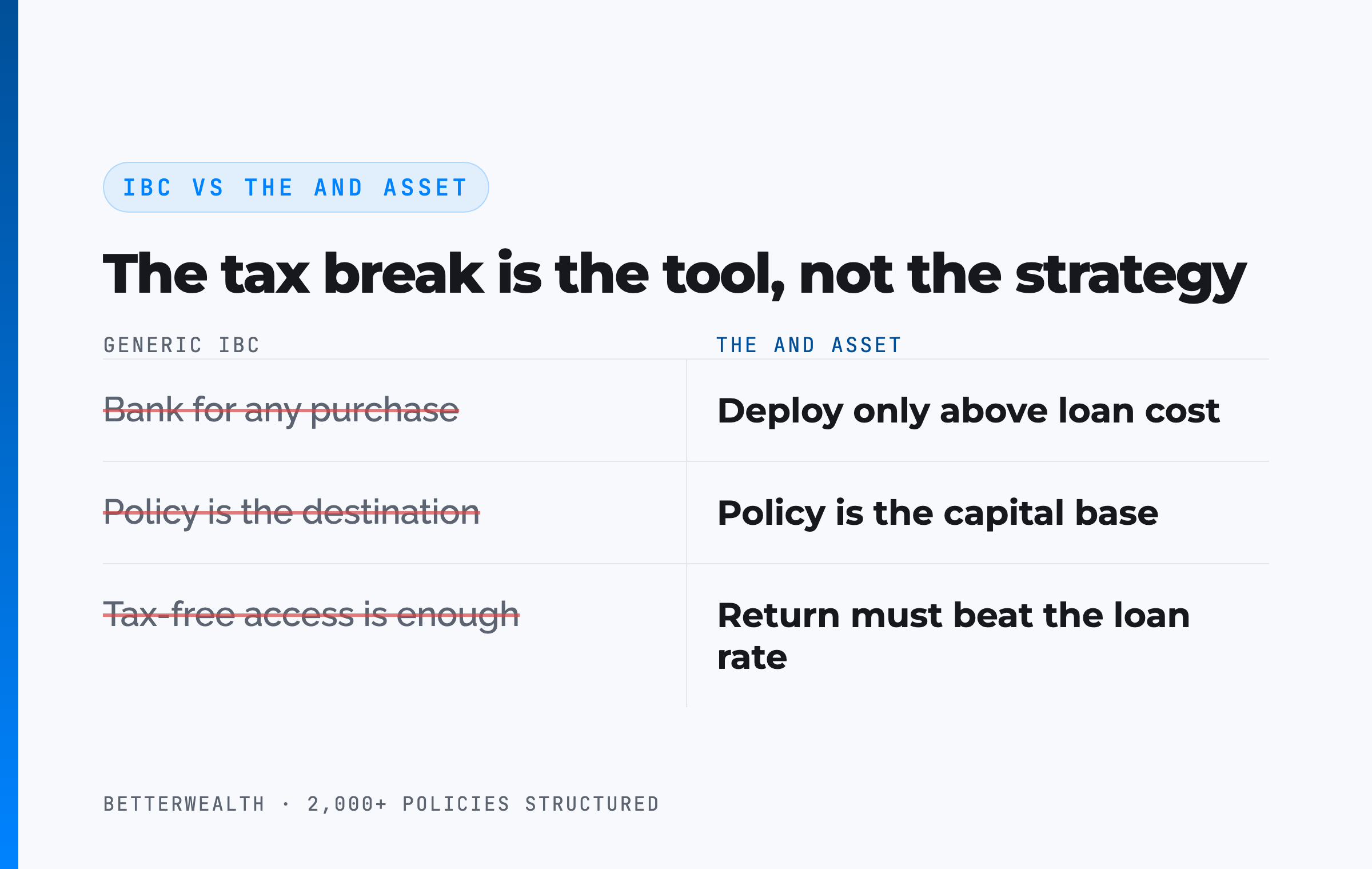

The favorable tax treatment is the reason a permanent policy can serve as a capital base, but the tax treatment is not the strategy. The And Asset is BetterWealth's framework for using a properly structured whole life policy as that capital base. You borrow against it through non-taxable loans, the policy keeps compounding on its full value, and you deploy the capital into something that earns more than the loan costs.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. We respect that foundation. The And Asset builds on it with one rule his broader teaching does not enforce. IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The tax-free loan access is what makes the mechanism efficient. The discipline of clearing the loan rate is what makes it work.

So the tax answer and the strategy answer are different questions. Life insurance is tax-advantaged for everyone who owns it. The And Asset is for a specific person: the entrepreneur, business owner, or high-income earner who already deploys capital and can clear the loan cost. If you cannot identify a use for borrowed dollars that beats that cost, the tax treatment alone is not a reason to fund a policy.

09 / Head to headHow life insurance tax treatment compares

Against the accounts entrepreneurs actually use, life insurance trades the highest possible early liquidity for tax-deferred growth, non-taxable access, and an income-tax-free transfer at death. The table sets a permanent policy against a Roth IRA, a traditional 401(k), and a taxable brokerage account on the four tax dimensions that decide where capital should sit.

| Tax dimension | Permanent Life Insurance | Roth IRA | Traditional 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Contributions | After-tax; not deductible | After-tax; not deductible | Pre-tax; deductible now | After-tax; not deductible |

| Growth | Tax-deferred inside the policy, net of internal costs | Tax-free | Tax-deferred | Taxed annually on dividends and realized gains |

| Access before 59½ | Non-taxable loans against cash value, no age limit | Contributions out anytime; gains restricted | Penalty plus tax before 59½ | Fully liquid; gains taxed when sold |

| Transfer at death | Income-tax-free death benefit under IRC 101(a) | Tax-free to heirs within distribution rules | Taxable as ordinary income to heirs | Stepped-up basis; estate-tax rules apply |

Contributions. Life insurance premiums and Roth contributions are both after-tax, so neither gives you a deduction today. A traditional 401(k) is the only one of the four that lowers this year's taxable income, which is its main appeal and its main constraint. We compare the policy directly against the 401(k) in our infinite-banking-versus-401(k) breakdown.

Growth and access. The policy's edge is the combination: tax-deferred growth plus non-taxable loan access at any age, with no early-withdrawal penalty. A 401(k) defers tax but locks the money up until 59 and a half. A brokerage account is fully liquid but pays tax on gains every year you realize them.

Transfer. The income-tax-free death benefit is the cleanest transfer of the four. A traditional 401(k) passes to heirs as taxable ordinary income, which is the opposite outcome at the worst possible time.

A composite: the contractor who borrowed without a tax bill

Consider a 44-year-old general contractor, preferred non-tobacco, funding an overfunded whole life policy at $38,000 per year on a cashflow design built to stay under the MEC limit. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. Around year three, each premium dollar starts adding more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing a year-two break-even is marketing fiction.

In year seven, with roughly $284,000 of accessible cash value, the contractor borrows $146,500 against the policy to buy a used excavator that expands his bid capacity. The loan is not taxable income, because the policy is non-MEC and stays in force. The equipment returns an estimated 17.3% IRR through new jobs it makes possible, against an illustrative loan cost of around 6%, so the spread works in his favor by more than eleven points. The policy keeps compounding on its full value the entire time. Repayment runs on a 39-month schedule funded by the equipment's own revenue.

No tax on the loan. Two returns on the dollar. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a properly designed policy, a different approach, or nothing at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQLife insurance and tax, answered

Is life insurance taxable?

Life insurance is generally not taxable. The death benefit is excluded from the beneficiary's gross income under IRC Section 101(a), and cash value grows tax-deferred. Taxes apply only in specific cases, including a transfer-for-value sale, estate inclusion when the insured owns the policy, interest on a delayed payout, or a surrendered policy with a gain.

Are life insurance proceeds taxable to the beneficiary?

In most cases, no. A death benefit paid by reason of the insured's death is income-tax-free to the beneficiary under IRC Section 101(a), whether the beneficiary is a person, a trust, or a business. The principal is not reported as income. Only interest the insurer adds on a delayed or installment payout is taxable.

When is a life insurance death benefit taxable?

A death benefit becomes taxable in three situations. First, a transfer-for-value: the policy was sold or transferred for consideration without a safe-harbor exception, making part of the proceeds ordinary income. Second, estate inclusion: the insured owned the policy, so the benefit is part of the taxable estate for estate-tax purposes. Third, interest on a delayed or installment payout is taxable income.

Is the cash value of life insurance taxable?

Cash value grows tax-deferred inside the policy, so the annual growth is not taxed as it accrues. A tax event happens only if you surrender or lapse the policy with a gain, where the gain above your cost basis is taxed as ordinary income, or if the policy is a Modified Endowment Contract and you take a distribution.

Are life insurance policy loans taxable?

A loan against a properly structured, non-MEC policy is not taxable income. You are borrowing against your cash value, not withdrawing it, so there is no taxable distribution. A loan can become taxable if the policy is a Modified Endowment Contract, or if the policy lapses or is surrendered while a loan is outstanding and there is a gain.

Are life insurance premiums tax deductible?

Personal life insurance premiums are not tax deductible. The IRS treats them as a personal expense. A few narrow business cases exist, such as employer-paid group term coverage up to $50,000 under IRC Section 79, but a business generally cannot deduct premiums on a policy where it is the beneficiary. Premiums paid for personal coverage are paid with after-tax dollars.

What is the transfer-for-value rule?

The transfer-for-value rule says that if a life insurance policy is transferred for valuable consideration, the death benefit can lose its income-tax-free status, and the portion above what the new owner paid plus later premiums becomes taxable income. Safe-harbor exceptions exist, including transfers to the insured, a partner of the insured, a partnership the insured is in, or a corporation the insured is a shareholder or officer of.

Is life insurance subject to estate tax?

A death benefit is income-tax-free but can still be included in the taxable estate if the insured held incidents of ownership in the policy at death under IRC Section 2042. The federal estate-tax exemption is high enough that most estates owe nothing, but larger estates, or those in states with their own estate tax, can owe tax. Holding the policy in an irrevocable life insurance trust keeps it out of the estate.

Is a Modified Endowment Contract taxed differently?

Yes. A Modified Endowment Contract, or MEC, is a policy funded faster than the IRS 7-pay limit allows. Distributions and loans from a MEC are taxed on a gain-first basis as ordinary income, and a 10% penalty can apply before age 59 and a half. The death benefit of a MEC is still income-tax-free. A policy designed for The And Asset is deliberately structured to stay under the MEC limit.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. The tax-deferred growth and non-taxable loan access are what make the structure work.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Do beneficiaries have to report life insurance on their taxes?

A beneficiary generally does not report a lump-sum death benefit on a tax return because it is excluded from gross income under IRC Section 101(a). If the payout was delayed or paid in installments and the insurer added interest, the insurer reports that interest on a Form 1099-INT, and only that interest is taxable. The principal stays tax-free.

- IRC Section 101 (Cornell Law), the exclusion of life insurance death benefits from gross income, and the transfer-for-value rule.

- IRC Section 7702 (Cornell Law), the tax code definition of life insurance governing cash value treatment, added in 1984.

- IRC Section 7702A (Cornell Law), the Modified Endowment Contract rules and the 7-pay test.

- IRC Section 2042 (Cornell Law), inclusion of life insurance proceeds in the gross estate via incidents of ownership.

- IRS, Life Insurance Proceeds, the agency's plain-language guidance on taxation of proceeds.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

This article is educational and is not tax or legal advice. Tax treatment depends on your specific facts and on current federal and state law, which can change. Confirm any decision with a qualified tax advisor or attorney before acting.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a properly designed policy fits your tax and capital plan, book a discovery call. We will tell you if it does not.