.png)

Life insurance premiums are generally not tax deductible: IRC Section 264 disallows the deduction because you are the policy's beneficiary, with narrow exceptions for group-term and charity-owned coverage. The real tax advantage of permanent life insurance is tax-deferred cash value growth and tax-favored access, not a premium write-off.

The question gets asked backward, and the way it gets asked usually leads to the wrong conclusion. People want to know whether they can write off life insurance premiums the way they write off a mortgage interest payment or a business expense. The answer for almost everyone is no. Then the conversation stops, and the reader walks away thinking life insurance carries no tax advantage at all.

The deduction question is the least interesting tax question you can ask about life insurance, and fixating on it hides the part of the tax code that actually matters. A premium deduction would save you a few cents on the dollar today. The tax treatment of how the money grows and how you access it is worth far more over a multi-decade horizon, and it is the reason this asset exists in the first place.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the deductibility question comes up on nearly every intake call. This guide gives the direct answer first, then the narrow situations where premiums actually are deductible, then why employer-paid key-person and split-dollar premiums are generally not. After that, we separate deductibility from the bigger point: the tax advantage of permanent life insurance lives in the cash value and the death benefit, not on the premium line of your return.

- Personal life insurance premiums are not tax deductible under IRC Section 264, because the payer is also a beneficiary.

- An employer can deduct group-term life insurance premiums on coverage up to $50,000 per employee as compensation.

- Premiums on a policy irrevocably owned by a qualified charity can be deductible as a charitable contribution.

- Key-person and most split-dollar premiums are not deductible because the business is the beneficiary.

- The real tax advantage is tax-deferred cash value growth, policy loans that are not taxable income, and an income-tax-free death benefit.

- Section 7702 is the code section that defines and protects that tax treatment.

01 / The problemWhy the deduction question leads people astray

The deduction question feels like the right question because most financial decisions get judged on their immediate tax impact. We are trained to ask what a thing does to this year's return. Life insurance does not reward that lens, and the people who evaluate it only through that lens conclude there is nothing here.

There is a logic to why the premium is not deductible, and it is worth understanding before the exceptions make sense. The government does not let you deduct a premium on the front end and then receive the death benefit income-tax-free on the back end. You get one tax benefit or the other, not both, on the same dollars. For permanent life insurance, the back-end treatment is the one worth having.

Asking whether life insurance is deductible is like asking whether a Roth contribution is deductible. It is not, and that is the point. The advantage is on the other end.

02 / The direct answerIs life insurance tax deductible for an individual?

No. Personal life insurance premiums are not tax deductible for an individual, full stop. IRC Section 264 disallows the deduction for premiums on any life insurance policy when the taxpayer is directly or indirectly a beneficiary of that policy. When you buy a policy on your own life and name your family as beneficiaries, you are indirectly a beneficiary, and the deduction is gone.

The IRS treats a personal life insurance premium as a personal expense. It sits in the same category as your groceries or your car payment, none of which reduce your taxable income. This holds whether the policy is term or permanent, and whether you pay $400 a year or $40,000 a year. The premium amount and the policy type do not change the answer.

This is the complete tax picture only for the premium. Whether the proceeds, withdrawals, or loans are taxable is a separate set of questions, and we cover the full picture in our guide on whether life insurance is taxable. The short version: the premium is not deductible, and the death benefit is generally not taxable. Those two facts are connected.

No deduction in. No tax out. That is the trade.

03 / The exceptionsWhen are life insurance premiums actually deductible?

Life insurance premiums are deductible in a few narrow situations, and each one shares a common thread: the person paying the premium is not the one collecting the benefit. Once that condition is met, the Section 264 disallowance no longer applies the same way. Three cases come up often enough to know.

Group-term life insurance provided by an employer

An employer can deduct premiums on group-term life insurance it provides to employees, because the business is paying for employee compensation, not buying coverage for its own benefit. The deduction runs through the ordinary compensation rules. The first $50,000 of coverage per employee is also tax-free to the employee under IRC Section 79. Coverage above $50,000 produces imputed income, a small amount the employee pays tax on, calculated from an IRS table. This is the single most common way a life insurance premium becomes deductible.

Policies owned by a qualified charity

If you irrevocably transfer ownership of a policy to a qualified charity, or the charity owns the policy from the start and you fund the premiums, those premium payments can be deductible as a charitable contribution. The deduction follows charitable rules, not insurance rules, because you have given the asset away. The charity, not you or your family, is the owner and beneficiary. Documentation and the irrevocable nature of the gift matter here, so this is a coordinate-with-your-CPA situation.

Older alimony arrangements

Under divorce or separation agreements executed on or before December 31, 2018, premiums paid on a policy for the benefit of an ex-spouse could be deductible as alimony, when the agreement required it and the ex-spouse owned the policy. The Tax Cuts and Jobs Act changed alimony treatment for agreements executed after that date, so alimony, including premiums paid as alimony, is no longer deductible for newer agreements. This exception is shrinking as older decrees age out, but it still applies to pre-2019 arrangements.

Every exception works for the same reason: the premium payer gave up the benefit. The moment you are the one who collects, the deduction disappears.

04 / Business policiesCan a business deduct key-person or split-dollar premiums?

Generally no. A business cannot deduct premiums on key-person or split-dollar life insurance, because the business is directly or indirectly the beneficiary, which is exactly the situation IRC Section 264 disallows. This trips up a lot of owners who assume any premium their company pays is a deductible business expense. It is not, when the company stands to collect.

Key-person insurance is a policy a business buys on the life of a founder or critical employee, with the business as owner and beneficiary, to absorb the financial hit if that person dies. The premiums are not deductible. The offsetting benefit is that the death proceeds are generally received income-tax-free, so the structure trades a deduction you cannot take for a benefit you do not pay tax on. C corporations should also be aware of how this interacts with the corporate alternative minimum tax, which is a CPA conversation.

Split-dollar arrangements, where an employer and an employee share the cost and benefits of a policy, follow their own regime under the split-dollar regulations. The employer's premium payments are generally not deductible. Depending on whether the arrangement is structured as an economic-benefit or a loan regime, the employee may recognize income or imputed interest. The mechanics are detailed, and this is not a do-it-yourself area.

If the business collects, the business does not deduct.

05 / The frameworkWhat the deduction question misses entirely

The tax advantage of permanent life insurance is on the back end, in how the cash value grows and how you access it, and the premium deduction question never touches it. This is where the strategy we practice, The And Asset, actually lives. The premium being non-deductible is a footnote. The cash value treatment is the headline.

Three features do the work. Cash value grows tax-deferred inside the policy, so the annual growth does not show up on your 1040. You can access that cash value through policy loans, and a loan is not taxable income because it is debt, not a distribution, as long as the policy stays in force and is not a Modified Endowment Contract. The death benefit passes to your beneficiaries generally income-tax-free under IRC Section 101(a). The code section that defines and protects all of this is Section 7702. We break down exactly how that works in our guide to the Section 7702 tax strategy.

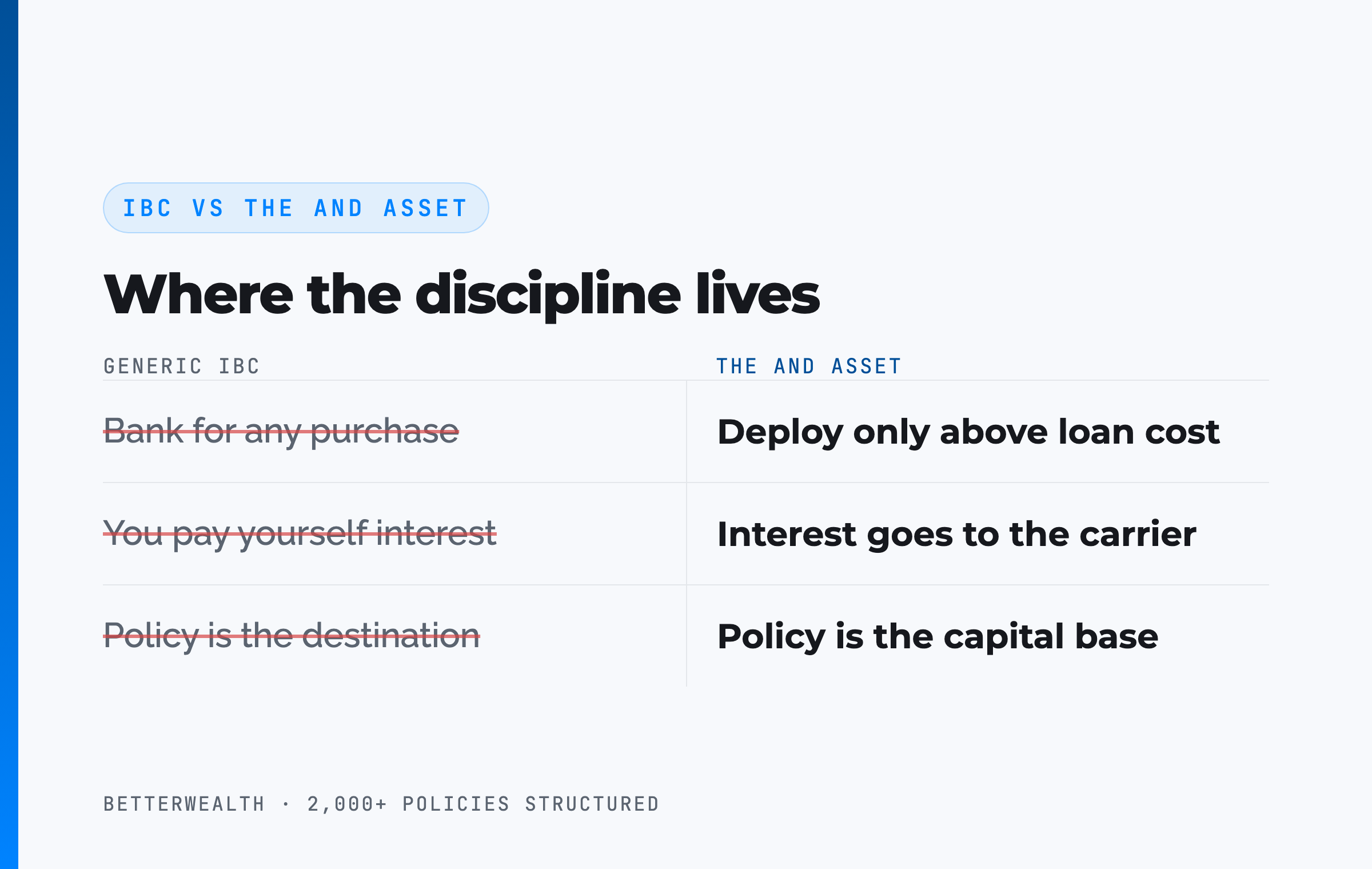

Where IBC ends and The And Asset begins

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker, and his insight about lost opportunity cost is the foundation we build on. IBC says you can use a whole life policy as a personal bank for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money.

The tax treatment matters here because the marketing crowd uses it dishonestly. Many IBC marketers tell people they are paying themselves interest. You are not. The interest on a policy loan goes to the insurance company. Your return is what you earn by deploying the borrowed capital elsewhere, while the policy keeps compounding net of mortality and expense charges. The tax-favored access is real. The "pay yourself interest" framing is not.

Marketers have ruined how this gets explained. The tax win is not a premium write-off and it is not paying yourself interest. It is tax-deferred growth and access you do not get taxed on.

06 / How it worksHow to capture the tax advantage that does exist

Capturing the real tax advantage of permanent life insurance comes down to five steps, and the deduction is not one of them. The point is to stop optimizing for a write-off you cannot get and start optimizing for the treatment you can.

- Stop chasing the premium deduction. Accept that the premium is a non-deductible personal expense under Section 264. Build the plan around the back-end treatment instead. Trying to make the premium deductible distorts the design.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows. The base/PUA split is the single design decision that determines how much cash value works for you early. Push toward the limit without tipping into a Modified Endowment Contract, because a MEC loses the favorable loan treatment.

- Let the cash value grow tax-deferred. The growth compounds inside the policy net of mortality and expense charges, with no annual tax bill on it. Do not expect to break even immediately. For a healthy individual, a well-designed policy reaches break-even at year 5 or later, and any illustration showing year-one break-even is fiction.

- Access capital through policy loans. Borrow against the cash value rather than withdrawing it. A policy loan is not taxable income because it is debt collateralized by your policy, not a distribution. This is the tax-favored access that makes the asset useful while you are alive.

- Deploy where the return beats the loan cost. Put the borrowed capital into an activity that produces a return greater than the carrier's loan rate. The policy compounds on its full value the entire time the loan is outstanding.

The first step is the one most people skip. They keep hunting for a way to deduct the premium and miss the treatment that is sitting right there.

The tax treatment only matters if the strategy fits you.

It fits you if

- You are an entrepreneur or high-income earner with a long capital horizon

- You have maxed your other tax-advantaged accounts

- You can name a use for capital that beats the loan cost

- You want tax-favored access to capital, not just a death benefit

It does not fit you if

- You are buying it expecting a premium deduction

- You want a savings account, not a capital strategy

- You are in the early stages of building wealth

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether a properly designed policy belongs in your plan. If you are in the second, we will tell you that too.

Book a Discovery Call07 / The mathDoes the return clear the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow. This is the entire test, and it is what separates a disciplined strategy from an expensive habit. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6 percent range, but treat the specific number as a variable to verify with the carrier, not a constant.

Here is the structure. You borrow at the carrier's loan rate. The policy keeps compounding on its full cash value, including the borrowed portion, net of internal costs. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the same dollar has done two jobs. If it is lower, you have borrowed money to lose money slowly, and no tax treatment fixes that. The tax-favored access is only an advantage when the underlying math works.

If the deal does not clear the loan rate, do not borrow.

08 / Where people get this wrongThe two tax myths that cost people money

Two tax myths dominate this topic, and both come from marketing rather than the code. Naming them is how you avoid buying the wrong thing for the wrong reason.

The first myth is that you can write off the premium. You cannot, for personal coverage, and an agent who implies otherwise is either careless or selling. If your reason for owning a policy is a deduction, the reason is wrong, and the policy will disappoint you. The second myth is the phrase "tax-free." Permanent life insurance offers tax-deferred growth and tax-favored loan access, both real, but the word "tax-free" gets thrown around without the conditions attached. The treatment depends on the policy staying in force, staying inside the Section 7702 definition, and not becoming a Modified Endowment Contract. Surrender the policy with a gain, or let it lapse with a loan outstanding, and a tax bill can appear.

Precision is the credibility test here. The honest version is more useful than the oversold version, because it tells you what to actually do: keep the policy in force, design it to avoid MEC status, and access cash through loans rather than taxable withdrawals.

"Tax-free" with no conditions attached is a marketing word. Tax-deferred growth and non-taxable loan access, with the policy kept in force and outside MEC limits, is the accurate version.

09 / The fitWho should care about this, and who should not?

The tax treatment of permanent life insurance matters most to entrepreneurs, business owners, and high-income earners who have already filled their other tax-advantaged accounts and want tax-favored access to capital they can deploy. For that person, the inability to deduct the premium is irrelevant, and the back-end treatment is a genuine edge in a broader capital strategy.

It matters far less, and may not be worth the cost, for someone in the early stages of building wealth, someone looking for a simple savings vehicle, or someone whose only interest is the deduction they are not going to get. If you cannot identify an activity that beats the loan cost, no tax feature makes this the right tool. The discipline is the strategy, and the tax treatment is a benefit layered on top of a sound decision, never a reason to make an unsound one.

10 / Head to headLife insurance against other tax-advantaged vehicles

Compared to the other tax-advantaged tools high earners use, permanent life insurance trades the front-end deduction for tax-deferred growth, tax-favored access, and an income-tax-free death benefit. The table sets it against a 401(k), a Roth IRA, and a taxable brokerage account on the dimensions that decide where a dollar goes.

| Dimension | Permanent Life Insurance | Traditional 401(k) | Roth IRA | Taxable Brokerage |

|---|---|---|---|---|

| Premium / contribution deductible? | No (IRC 264) | Yes, within limits | No | No |

| Growth taxed annually? | No, tax-deferred inside the policy | No, tax-deferred | No, tax-free if rules met | Yes, on gains and dividends |

| Access before 59½ | Policy loans anytime, not taxable income | Penalty plus tax | Contributions out anytime; gains restricted | Fully liquid |

| Treatment at death | Income-tax-free death benefit (IRC 101a) | Taxable to heirs as income | Generally tax-free to heirs | Stepped-up basis |

The deduction tradeoff. A traditional 401(k) gives you the front-end deduction life insurance does not, then taxes every dollar on the way out as ordinary income. Life insurance reverses that: no deduction now, favorable treatment later. Which you prefer depends on your view of future tax rates and your need for access before retirement age.

Access is the real differentiator. A 401(k) restricts access before 59½ under rules set by Congress. Policy loans carry no age gate and are not taxable income, which is why the strategy appeals to people who deploy capital and need it available, not locked away.

It is a complement, not a replacement. None of this argues for skipping the 401(k) match or the Roth. Permanent life insurance is the tool some high earners add after the conventional accounts are full, for the access and the treatment the others do not offer.

A composite: the owner who stopped chasing the deduction

Consider a 43-year-old S-corporation owner, preferred non-tobacco, who came in convinced his company should buy his life insurance so the premium would be deductible. It would not have been, because the structure he wanted made the business an indirect beneficiary. This is a representative composite, not a single named client.

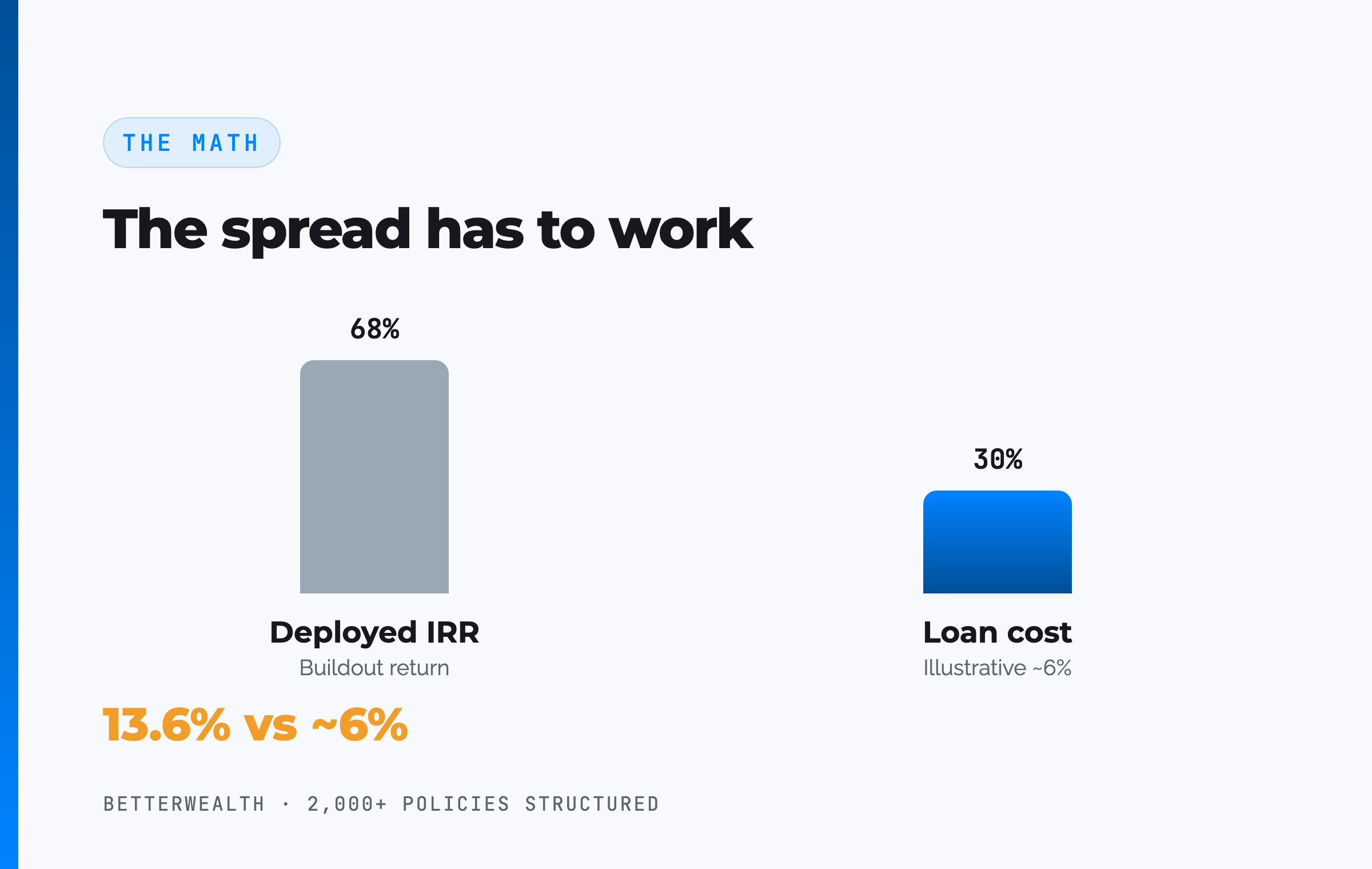

We redirected the plan. He owns the policy personally, takes no premium deduction, and accepts that the premium is a personal expense. Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year six, with roughly $312,000 of accessible cash value, he borrows $164,500 against the policy to fund a buildout of additional revenue space for his business. The buildout returns an estimated 13.6% IRR. The loan cost is illustrative at around 6 percent, so the spread works in his favor by more than seven points. The policy loan is not taxable income, the policy keeps compounding on its full value, and repayment runs on a 44-month schedule funded by the new revenue. The deduction he wanted would have saved him a fraction of what the back-end treatment delivered.

One dollar. Two jobs. No tax bill on the access.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and tax-treatment breakdowns we use when we structure a policy for tax-favored access instead of a deduction that does not exist. Free, email-gated, no spam.

Open the VaultFAQLife insurance tax deduction questions

Is life insurance tax deductible?

In most cases, no. Personal life insurance premiums are not tax deductible under IRC Section 264, because the taxpayer paying the premium is also a beneficiary of the policy. The IRS treats premiums as a personal expense, the same way it treats most things you buy for yourself.

Are life insurance premiums ever tax deductible?

Yes, in narrow situations. An employer can generally deduct premiums for group-term life insurance up to $50,000 of coverage per employee as a compensation expense. Premiums on a policy irrevocably owned by a qualified charity can be deductible as a charitable contribution. Some divorce decrees executed on or before December 31, 2018 treated premiums paid for an ex-spouse as deductible alimony.

Can a business deduct life insurance premiums?

Usually not. Under IRC Section 264, a business cannot deduct premiums on a policy where it is directly or indirectly a beneficiary. That disallows the deduction for most key-person and split-dollar arrangements. The main exception is group-term coverage provided to employees, which is deductible as compensation.

Is key person life insurance tax deductible?

No. Premiums on key person life insurance are not tax deductible, because the business owns the policy and is the beneficiary. IRC Section 264 disallows the deduction whenever the premium payer is directly or indirectly a beneficiary. The tradeoff is that the death benefit is generally received income-tax-free.

Why is life insurance not tax deductible?

Life insurance premiums are not deductible because the tax code treats them as a personal expense and because the eventual death benefit is received income-tax-free under IRC Section 101(a). Congress does not allow a deduction on the front end and a tax-free benefit on the back end for the same dollars.

Is group-term life insurance tax deductible?

Yes, for the employer. A business can deduct the cost of group-term life insurance it provides to employees as a compensation expense. Coverage up to $50,000 per employee is also tax-free to the employee under IRC Section 79. The value of coverage above $50,000 is added to the employee's taxable income as imputed income.

Are whole life insurance premiums tax deductible?

No. Whole life insurance premiums are not tax deductible for an individual. The tax advantage of whole life is not a premium write-off. It is the tax-deferred growth of cash value and the ability to access that cash value through policy loans that are not treated as taxable income.

What is the real tax advantage of permanent life insurance?

The real tax advantage is on the back end, not the premium. Cash value grows tax-deferred inside the policy net of internal charges, you can access it through policy loans that are not taxable income, and the death benefit passes income-tax-free under IRC Section 101(a). Section 7702 is the code section that defines these rules.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Can I deduct life insurance as a business expense if I am self-employed?

Generally no. A self-employed person cannot deduct premiums on a personal life insurance policy, because they are the beneficiary under IRC Section 264. Life insurance is also specifically excluded from the self-employed health insurance deduction. Premiums for group-term coverage provided to employees remain deductible to the business.

- IRC Section 264 (Cornell Law), the provision disallowing deductions for life insurance premiums when the payer is a beneficiary.

- IRC Section 79 (Cornell Law), the group-term life insurance rules, including the $50,000 tax-free threshold.

- IRC Section 101 (Cornell Law), the income-tax-free treatment of life insurance death benefits.

- IRC Section 7702 (Cornell Law), the definition of life insurance for tax purposes, behind tax-deferred cash value and loan treatment.

- IRS Publication 525, taxable and nontaxable income, including group-term life imputed income.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

This article is educational and not tax, legal, or investment advice. The Internal Revenue Code is detailed and fact-specific, and rules change. Confirm any deduction, exclusion, or strategy with a qualified CPA or tax attorney before acting on it.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether the tax treatment of a properly designed policy fits your plan, book a discovery call. We will tell you if it does not.