.png)

Life insurance proceeds paid to a beneficiary as a death benefit are generally not subject to federal income tax under IRC 101(a). The exceptions are interest added to a delayed payout, proceeds on a policy that was transferred for value, and estate tax when the insured owned the policy at death.

Most people ask whether life insurance proceeds are taxable at the worst possible moment, in the weeks after a death, when a check has already arrived and the fear is that a third of it belongs to the government. The short answer relieves that fear. The longer answer is where families and business owners lose money they did not need to lose.

A life insurance death benefit paid to a beneficiary is generally free of federal income tax, but it is not automatically free of estate tax, and those are two different questions. Confuse the two and you can structure a policy that pays out cleanly to a beneficiary while quietly adding hundreds of thousands of dollars to a taxable estate. The income-tax answer is simple. The full picture has edges.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the tax treatment of the death benefit is the foundation the entire strategy sits on. This article gives you the direct answer first, then walks through the three places proceeds actually do get taxed: interest on a delayed payout, the transfer-for-value rule, and estate inclusion. We will keep income tax and estate tax clearly separated, because that distinction is where most confusion lives.

This is general education, not tax or legal advice. Tax law changes, and the right answer for your situation depends on facts a qualified advisor needs to see. For the complete walkthrough of every tax angle, see our companion guide, Is Life Insurance Taxable? The Complete Guide.

- A death benefit paid to a beneficiary is generally excluded from gross income for federal income tax under IRC 101(a).

- Capital gains tax does not apply to a death benefit. It is not a sale and is not taxed as one.

- Interest the insurer adds to a delayed or installment payout is taxable, even though the death benefit is not.

- The transfer-for-value rule can make part of a death benefit taxable when a policy is sold or transferred for consideration.

- Estate tax is separate from income tax. If the insured owned the policy at death, the benefit can be included in the estate.

- An irrevocable life insurance trust or a third-party owner can keep the death benefit outside the taxable estate.

01 / The direct answerAre life insurance proceeds taxable at all?

A life insurance death benefit paid to a beneficiary is generally not subject to federal income tax. The Internal Revenue Code, at Section 101(a), excludes amounts received under a life insurance contract that are paid by reason of the insured's death from the beneficiary's gross income. A spouse, a child, or a business partner who receives a lump-sum death benefit generally reports none of it as income.

This is the rule that makes life insurance a planning tool rather than a gamble. The benefit arrives intact. It does not get diluted by a marginal income tax rate the way a withdrawal from a pre-tax retirement account does. For a family replacing lost income, that intact payout is the entire point.

The exclusion is broad, but it is not unconditional. Three situations move proceeds out of the safe column, and the rest of this guide is about those three. None of them are exotic. All of them are avoidable with the right structure.

The death benefit being income-tax-free is the part everyone gets right. The estate tax being a separate question is the part that costs families money, and almost no sales conversation mentions it.

02 / Income vs estate taxWhat is the difference between income tax and estate tax here?

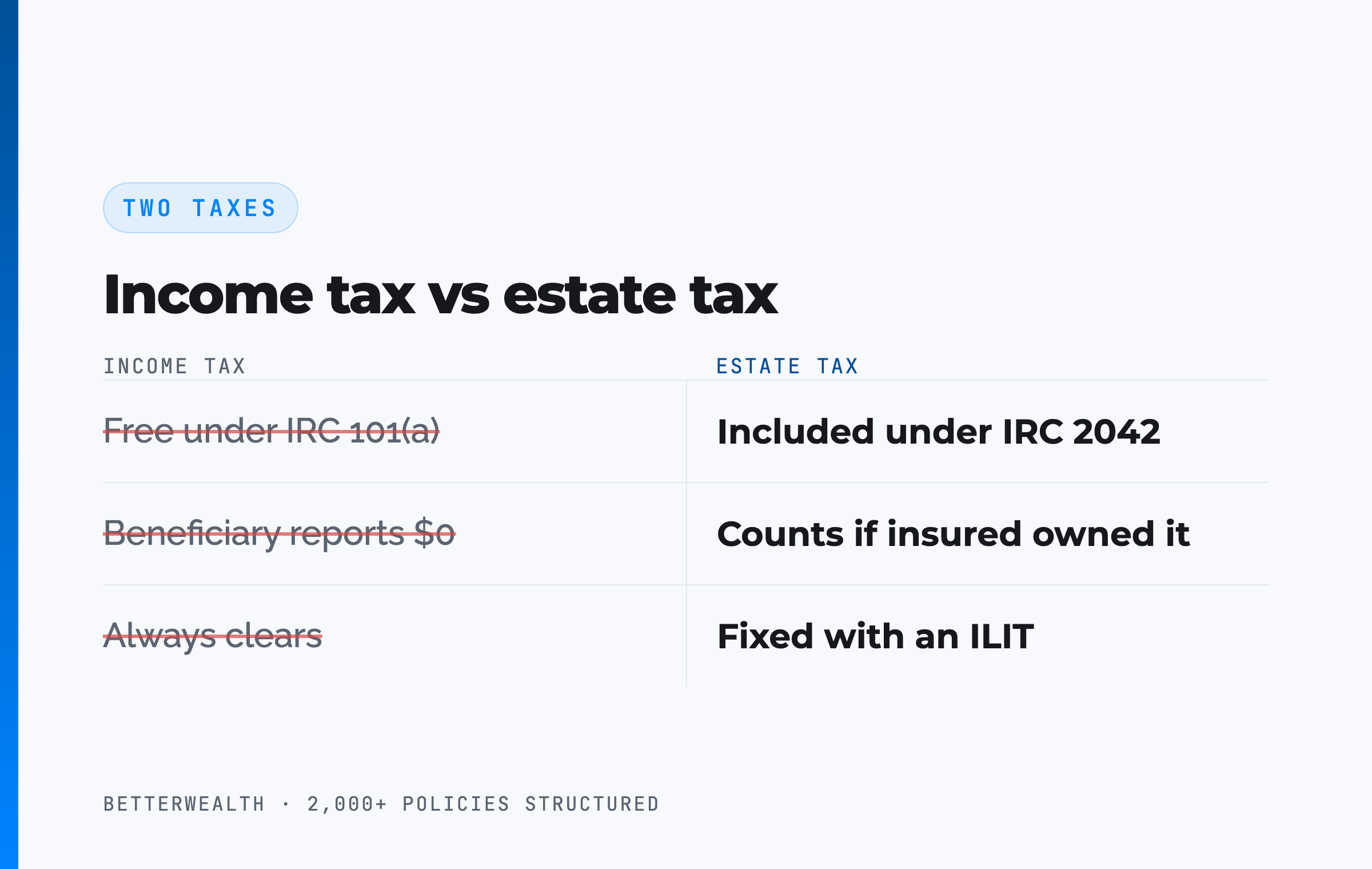

Income tax asks whether the beneficiary reports the proceeds as income, and estate tax asks whether the death benefit is counted in the deceased's taxable estate. They are two separate gates, decided by two separate parts of the tax code, and a death benefit can pass through one cleanly while getting caught in the other.

Picture a business owner who owns a large policy on his own life. When he dies, the death benefit goes to his beneficiaries income-tax-free under IRC 101(a). That part works exactly as advertised. But because he owned the policy, the full death benefit is also counted in his taxable estate under IRC 2042. If his estate is large enough to owe federal estate tax, the proceeds that arrived income-tax-free can still be reduced by estate tax.

This is the single most expensive misunderstanding in the field. People hear "life insurance is tax-free," assume that settles every tax question, and never look at ownership. Ownership is the variable that decides the estate-tax answer. We cover how to fix it in our guide on how to avoid tax on life insurance proceeds, but the first step is simply to stop treating the two taxes as one.

Income-tax-free does not mean estate-tax-free.

03 / Capital gainsDo capital gains taxes apply to a death benefit?

No. A death benefit paid to a beneficiary is not a capital gain and is never taxed as one. A capital gain comes from selling an appreciated asset for more than its cost basis. A death benefit is not a sale. It is a contractual payment triggered by the insured's death, and IRC 101(a) governs it, not the capital gains rules.

The confusion usually comes from a different transaction. A living policyholder who surrenders or sells a permanent policy for more than the total premiums paid into it can owe tax on the gain. That is a living-policyholder event, and it has nothing to do with the death benefit a beneficiary receives. When the question is specifically about proceeds paid at death, capital gains tax is off the table.

The reason this matters for planning is that a properly structured permanent policy builds cash value the owner can access during life, and the death benefit still passes income-tax-free to beneficiaries later. Knowing which event triggers which tax keeps you from making a living decision based on a death-benefit rule, or the reverse.

04 / The interest exceptionIs the interest on a delayed payout taxable?

Yes. When the insurer holds the proceeds and adds interest, or pays the death benefit in installments rather than a lump sum, the interest portion is taxable income to the beneficiary. The underlying death benefit stays income-tax-free. Only the interest the insurer pays on top of it is taxed.

This shows up in two common ways. First, a beneficiary chooses a settlement option that pays the death benefit over time, and each payment is part return of the income-tax-free principal and part taxable interest. Second, there is a gap between the date of death and the date the claim is paid, and the insurer credits interest for that period. The insurer reports the taxable interest on a Form 1099-INT, and the beneficiary includes it as income.

How the interest gets separated from the benefit

The death benefit and the interest are tracked separately, which is what keeps the exclusion intact. If a beneficiary receives a $500,000 death benefit plus $9,400 of interest that accrued before payment, the $500,000 is excluded under IRC 101(a) and the $9,400 is taxable. The numbers used here are illustrative. The principle is fixed: principal is excluded, interest is income.

The benefit is free. The interest is not.

05 / The transfer-for-value ruleWhen does selling a policy create a tax bill?

The transfer-for-value rule can make part of a death benefit taxable when a policy is transferred to someone else for valuable consideration. Under IRC 101(a)(2), if a policy is sold or transferred for value, the income-tax exclusion can be lost, and the new owner may owe income tax on the death benefit to the extent it exceeds what they paid plus subsequent premiums.

This is the rule that surprises business partners. Two owners set up a cross-purchase buy-sell arrangement and transfer policies between themselves, or a policy changes hands as part of a deal, and a transfer for value has occurred without anyone naming it. The death benefit that would have been fully excluded is now partly taxable.

The exceptions that preserve the exclusion

The code carves out several transfers that do not trip the rule. A transfer to the insured, to a partner of the insured, to a partnership in which the insured is a partner, or to a corporation in which the insured is a shareholder or officer generally keeps the exclusion intact. A transfer where the new owner takes the old owner's cost basis, such as certain gifts, is also protected.

The practical lesson is to never move a policy for consideration without checking whether an exception applies first. The fix is almost always to route the transfer through one of the recognized exceptions. The cost of getting it wrong is a death benefit that loses its income-tax-free status, which is the one feature that made the policy worth owning.

Business partners transfer policies to each other for a buy-sell and assume the death benefit is still tax-free. Without an exception, the transfer-for-value rule says otherwise.

06 / Estate inclusionWhen are proceeds pulled into the taxable estate?

Life insurance proceeds are pulled into the taxable estate when the insured owned the policy or held incidents of ownership at death. Under IRC 2042, the full death benefit is included in the gross estate if the insured had the power to change the beneficiary, borrow against the policy, surrender it, or otherwise control it. Ownership, not who receives the money, is what triggers inclusion.

For most families this never matters, because the federal estate tax only applies above an exemption amount that sits in the millions per individual and is indexed over time. The estate-tax exemption is set by statute and has changed repeatedly, so the specific figure should be confirmed for the current year rather than assumed. The families who need to watch this are the ones whose estates, including the death benefit, approach or exceed that threshold.

How an ILIT keeps proceeds out of the estate

An irrevocable life insurance trust owns the policy instead of the insured. Because the trust holds the policy and the insured retains no incidents of ownership, the death benefit is generally excluded from the taxable estate under IRC 2042. The structure has to be set up correctly, the trust has to own the policy, and a three-year lookback under IRC 2035 applies when an existing policy is transferred into the trust before death. Buy the policy inside the trust from the start and the lookback is not a concern.

This is where ownership design does the work that beneficiary choices cannot. We walk through the full set of options, including ILITs and third-party ownership, in how to avoid tax on life insurance proceeds. The point to carry out of this section is that estate inclusion is a structural problem with a structural solution.

The tax answer depends on how the policy is owned.

This applies to you if

- You own a large policy on your own life

- Your estate may approach the federal exemption

- You are transferring a policy in a business deal

- You want the benefit to pass clean to heirs

It matters less if

- Your estate is well below the exemption

- A spouse is the direct beneficiary of a modest policy

- You hold a single small term policy

- You are not moving the policy for consideration

If you are in the first column, a short conversation about ownership and structure can prevent a tax bill that beneficiary choices alone will not fix. If you are in the second, we will tell you that too.

Book a Discovery Call07 / How to read itHow to tell whether your proceeds are taxable

Determining whether a specific payout is taxable follows a short, ordered sequence, and the order matters because each question rules out a different tax. Here is the sequence we use when a client asks about a policy.

- Confirm it is a death benefit. A payment made by reason of the insured's death is the amount IRC 101(a) excludes from income. A living surrender or sale is a different transaction with different rules.

- Separate any interest. If the insurer added interest or is paying in installments, split the interest from the principal. The principal is income-tax-free. The interest is taxable.

- Trace how the policy was acquired. If the policy was transferred for valuable consideration, check whether a transfer-for-value exception applies. If none does, part of the benefit may be taxable income.

- Identify the owner at death. If the insured owned the policy or held incidents of ownership, the death benefit can be included in the taxable estate under IRC 2042, regardless of who received it.

- Confirm the structure. An ILIT or a third-party owner changes the estate answer. Verify ownership and beneficiary designations with a qualified advisor before relying on any of this.

Run those five questions and you will know which of the three exceptions, if any, applies to your situation. Most policies clear all five and the proceeds are fully income-tax-free. The ones that do not are usually fixable, and the fix is almost always about ownership rather than the beneficiary line.

08 / The strategy layerWhy tax treatment makes the policy a capital base

The income-tax-free death benefit is not just a feature for heirs. It is one reason a properly structured whole life policy works as a capital base during your life, which is the foundation of what we call The And Asset. The tax treatment of the death benefit and the access to cash value combine to make the policy a place capital can sit and still do work.

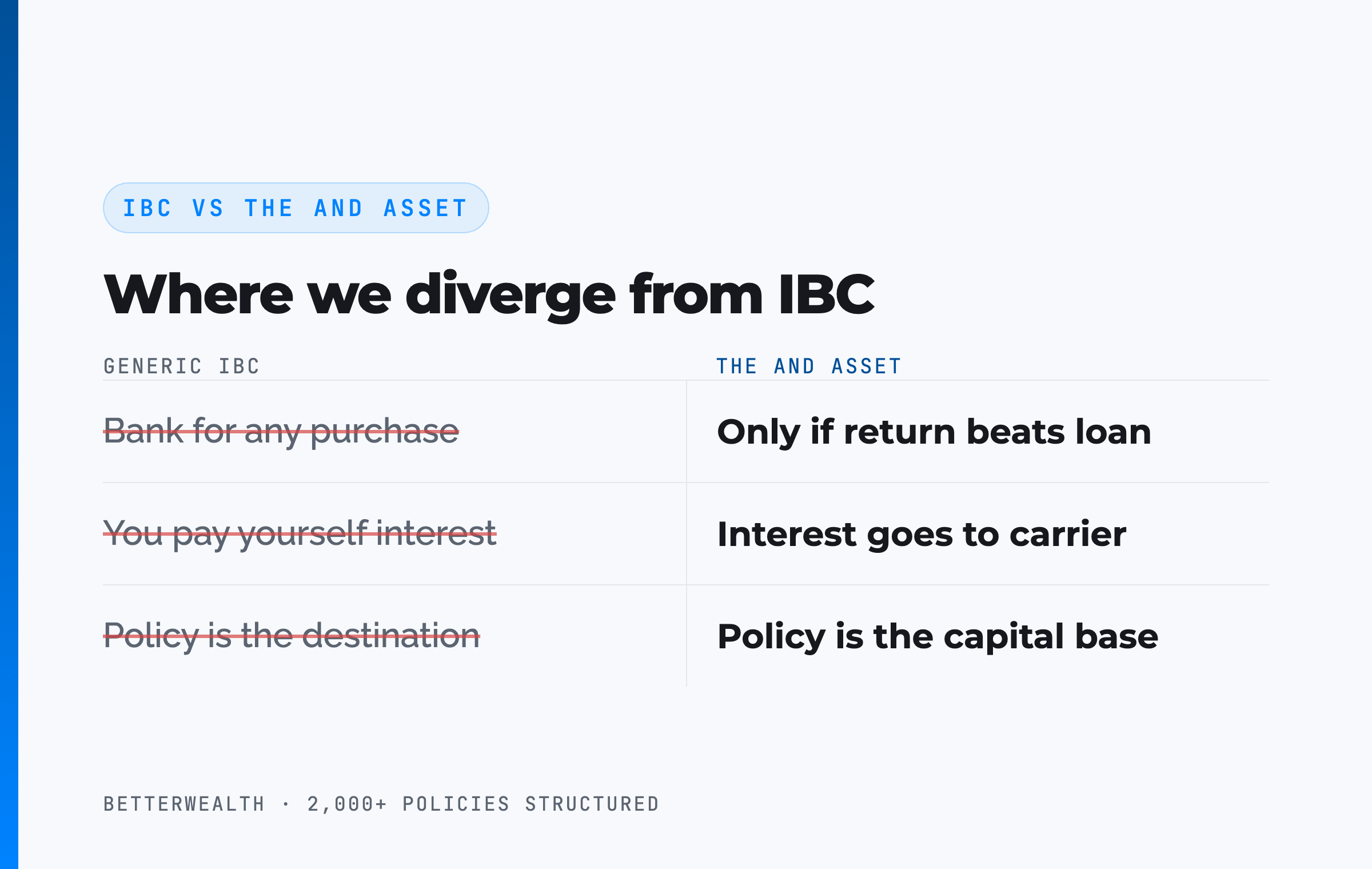

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We credit that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges. The income-tax-free death benefit is the backstop that makes that capital base reliable, not the strategy itself.

Marketers sell the tax-free death benefit as the whole story. It is the foundation, not the strategy. The strategy is what you do with the capital while you are alive.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the design frameworks, ownership-structure checklists, and tax-treatment breakdowns we use when we build policies that pass clean to the next generation. Free, email-gated, no spam.

Open the Vault09 / Head to headLife insurance proceeds against other inherited assets

Compared to the other assets a family inherits, a life insurance death benefit is one of the few that arrives without an income tax attached. The table sets it against an inherited pre-tax retirement account, an inherited taxable brokerage account, and an inherited annuity, on the tax dimensions that decide how much actually reaches the heir.

| Dimension | Life Insurance Death Benefit | Inherited Pre-Tax IRA / 401(k) | Inherited Taxable Brokerage | Inherited Annuity |

|---|---|---|---|---|

| Income tax to heir | Generally none under IRC 101(a) | Distributions taxed as ordinary income | Gains after death taxed; step-up applies to date-of-death value | Gain portion taxed as ordinary income |

| Capital gains | Not applicable to the death benefit | Not applicable; taxed as ordinary income | Step-up in basis often resets the gain | Not applicable; gain is ordinary income |

| Estate tax exposure | Included if insured owned the policy; avoidable via ILIT | Included in the taxable estate | Included in the taxable estate | Included in the taxable estate |

| Speed to heir | Paid on a death claim, often within weeks | Subject to distribution rules and timelines | Available after probate or transfer | Subject to payout election rules |

Income tax. The death benefit is the only asset in the table that generally reaches the heir free of income tax. An inherited pre-tax retirement account, by contrast, is taxed as ordinary income as it is withdrawn, which can push the heir into a higher bracket in the years they take distributions.

Estate tax. Every asset here can be included in the taxable estate, and the death benefit is no exception when the insured owned the policy. The difference is that life insurance has a clean structural fix, the ILIT, that the other assets do not have in the same form.

The takeaway. Life insurance is income-tax-advantaged on the way to the heir and estate-tax-manageable with the right ownership. That combination is why it anchors so many estate plans, and why the ownership question deserves more attention than the beneficiary line usually gets.

A composite: the income-tax-free benefit that almost got an estate-tax bill

Consider a 58-year-old business owner who held a $2,150,000 whole life policy on his own life, with his two children named as beneficiaries. This is a representative composite, not a single named client.

The income-tax side was never in doubt. His children would receive the full death benefit without reporting a dollar of it as income. The problem sat one gate over. Because he owned the policy outright, the entire $2,150,000 counted toward his gross estate under IRC 2042, and his other assets already put his estate near the federal exemption. The income-tax-free benefit was about to be reduced by estate tax.

The fix was structural, not cosmetic. He established an irrevocable life insurance trust to own a newly issued policy, so he held no incidents of ownership at death. Because the trust owned the policy from issue, the three-year lookback under IRC 2035 was not a factor. The death benefit now passes both gates: income-tax-free to the trust's beneficiaries and outside his taxable estate.

Same benefit. Two taxes. One structural fix.

The honest 30 minutes about how your policy is taxed.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at how your policy is owned and tells you whether the proceeds pass clean or need a structural fix. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the tax and structure questions.

Book a Discovery CallFAQLife insurance proceeds and taxes

Are life insurance proceeds taxable?

A life insurance death benefit paid to a beneficiary is generally not subject to federal income tax under IRC 101(a). The main exceptions are interest the insurer adds to a delayed or installment payout, proceeds on a policy acquired through a transfer for value, and estate tax when the insured owned the policy at death.

Are life insurance death benefits subject to income tax?

No. The death benefit itself is excluded from the beneficiary's gross income under IRC 101(a). A beneficiary who receives a lump-sum death benefit generally reports none of it as taxable income. Interest paid on top of the death benefit is the exception and is taxable.

Is the interest on life insurance proceeds taxable?

Yes. If the insurer holds the proceeds and pays interest, or pays the death benefit in installments that include interest, the interest portion is taxable income to the beneficiary. The underlying death benefit stays income-tax-free; only the interest is taxed.

What is the transfer-for-value rule?

The transfer-for-value rule, under IRC 101(a)(2), says that if a life insurance policy is transferred to another party for valuable consideration, the income-tax exclusion can be lost. Part of the death benefit then becomes taxable, unless the transfer falls within a recognized exception such as a transfer to the insured or to a partner of the insured.

Are life insurance proceeds subject to estate tax?

They can be. Income tax and estate tax are separate questions. If the insured owned the policy or held incidents of ownership at death, the death benefit is included in the taxable estate under IRC 2042. A death benefit that is income-tax-free can still face estate tax if the insured owned the policy.

Do capital gains taxes apply to a life insurance death benefit?

No. A death benefit paid to a beneficiary is not a capital gain and is not taxed as one. Capital gains can apply when a living policyholder sells or surrenders a policy for more than the cost basis, but that is a different transaction from a death benefit paid at death.

What is the difference between income tax and estate tax on life insurance?

Income tax asks whether the beneficiary reports the proceeds as income. Under IRC 101(a), a death benefit is income-tax-free. Estate tax asks whether the death benefit is counted in the deceased's taxable estate. If the insured owned the policy, the death benefit can be income-tax-free and still included in the estate.

How does an ILIT keep life insurance out of my estate?

An irrevocable life insurance trust owns the policy instead of the insured, so the insured holds no incidents of ownership at death. Because the insured does not own the policy, the death benefit is generally excluded from the taxable estate under IRC 2042. The trust must be set up and funded correctly, and a three-year lookback under IRC 2035 applies to existing policies transferred into it.

Are life insurance proceeds taxable if paid in installments?

The death benefit portion stays income-tax-free, but the interest built into installment payments is taxable. When a beneficiary chooses installments instead of a lump sum, each payment is part return of the income-tax-free death benefit and part taxable interest.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. The income-tax-free death benefit is part of why the policy works as a capital base.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

- IRC Section 101 (Cornell Law), the exclusion of life insurance death benefits from gross income, and the transfer-for-value rule at 101(a)(2).

- IRC Section 2042 (Cornell Law), inclusion of life insurance proceeds in the gross estate based on incidents of ownership.

- IRC Section 2035 (Cornell Law), the three-year lookback for certain transfers made before death.

- IRS, Life Insurance Proceeds, the agency's guidance on when proceeds and interest are taxable.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on how your policy is taxed and whether it is structured to pass clean, book a discovery call. We will tell you if it is not.

1. "Is Life Insurance Taxable? The Complete Guide" (/blogs/is-life-insurance-taxable) → wired from the intro and the Keep Reading block (full tax picture).

2. "How to Avoid Tax on Life Insurance Proceeds" (/blogs/how-to-avoid-tax-on-life-insurance-proceeds) → wired from H2 02 (income vs estate) and H2 06 (estate inclusion).

3. Pillar "What Is Infinite Banking?" → wired in the Keep Reading block.