.png)

How to avoid tax on life insurance proceeds starts with a fact most people miss: the death benefit is already income-tax-free under IRC Section 101. The real exposure is federal estate tax on large estates, which you reduce by moving policy ownership outside your estate, usually through an irrevocable life insurance trust.

Most of the searches for how to avoid tax on life insurance proceeds are solving a problem that does not exist. A life insurance death benefit paid for the death of the insured is generally excluded from federal income tax. No deduction to chase, no strategy to deploy. The check arrives, and the income tax is already handled by the tax code.

The tax people actually need to plan around is estate tax, and it only touches large estates where the insured owned the policy. That is a narrower problem than the search volume suggests, and it has real, legitimate solutions. It is also a problem that gets oversold. Some agents pitch elaborate trust structures to people whose estates will never owe a dollar of estate tax.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we work alongside estate attorneys on the cases that need one. This guide separates the income-tax question (mostly already settled) from the estate-tax question (where the planning lives), then walks the structures that hold up: third-party ownership, an irrevocable life insurance trust, naming the right beneficiary, and taking the lump sum. If you want the broader tax picture first, our guide on whether life insurance is taxable grounds the basics before the estate-tax detail here.

- The death benefit is generally income-tax-free under IRC Section 101(a), so most proceeds need no tax planning at all.

- Estate tax applies only when you own the policy at death and your total estate exceeds the federal exemption.

- An irrevocable life insurance trust (ILIT) removes the policy from your taxable estate when drafted correctly.

- Transferring an existing policy to a trust starts a three-year clock under IRC Section 2035.

- Never name your estate as beneficiary; name a person or a trust to skip probate and creditor exposure.

- Take the lump sum, because interest on deferred installment payouts is taxable income to the beneficiary.

01 / The setupAre life insurance proceeds taxable at all?

Life insurance proceeds are generally not taxable as income. Under IRC Section 101(a), a death benefit paid because the insured died is excluded from the beneficiary's gross income. A spouse, a child, or a business partner who receives a $1,000,000 benefit reports zero of it as income in the ordinary case. This is the default, and it is why most people searching for a way to avoid the tax are chasing a tax that was never owed.

Three situations break that default, and they are the only ones worth your attention. Interest earned when proceeds sit with the insurer before payout is taxable. A policy that was sold or transferred for value can make part of the benefit taxable under the transfer-for-value rule. And estate tax can apply when the insured owned the policy and the total estate is large enough to be taxable. We cover the income-versus-estate distinction in depth in our companion piece on whether life insurance proceeds are taxable; the rest of this guide focuses on the estate-tax exposure, because that is where structure actually changes the outcome.

If someone is selling you a complex trust to "avoid the tax on your death benefit," ask which tax. For most families, the income tax was never there to avoid.

02 / The real exposureWhen are life insurance proceeds subject to estate tax?

Proceeds are pulled into your taxable estate when you, the insured, hold incidents of ownership in the policy at death and your total estate exceeds the federal exemption. That is the rule in IRC Section 2042, and the phrase that matters is incidents of ownership. If you can name the beneficiary, take a loan, surrender the policy, or change the terms, you own it for estate purposes. The death benefit then counts as part of your estate.

Here is the part the pitches skip: this only matters above the exemption. The federal estate tax exemption sits in the eight-figure range per individual for 2026, and a married couple can effectively shelter roughly double that with proper planning. Confirm the current figure with the IRS, because it is indexed for inflation and set by Congress. If your estate, death benefit included, lands under that threshold and your state has no estate or inheritance tax, you do not have a federal estate tax problem to solve.

State taxes are the trap people miss. Roughly 18 states plus Washington DC impose their own estate or inheritance tax, and several use thresholds well below the federal one. A family that is clear of federal estate tax can still owe at the state level. Your state of residence, not the headline federal number, often decides whether any of this applies to you.

Above the exemption, structure matters. Below it, it usually does not.

03 / The structuresHow do you keep proceeds out of the taxable estate?

You keep proceeds out of the taxable estate by making sure the insured does not own the policy. That is the whole principle. Every legitimate structure is a different way to separate the insured from ownership, and an estate attorney should draft whichever one fits your situation. Here is the sequence we use when we map a case.

- Confirm the income-tax-free status. Verify the benefit qualifies under IRC Section 101(a), which it almost always does for a policy paid on the insured's death. This is your baseline. You are protecting an already income-tax-free benefit from a separate estate tax.

- Measure your estate exposure. Add the death benefit to everything else you own. Compare the total to the federal exemption and to your state's threshold. If you are under both, stop. No structure is needed, and paying for one is waste.

- Move ownership outside your estate. Have a party other than the insured own the policy. The two common routes are an irrevocable life insurance trust or direct third-party ownership by another adult. Both remove the insured's incidents of ownership.

- Respect the three-year rule. If you transfer an existing policy into a trust, IRC Section 2035 reaches back three years. Die inside that window and the proceeds rejoin your estate. Having the trust apply for a brand-new policy from day one sidesteps the lookback.

- Name the right beneficiary. Name a person or the trust, never your estate. Naming the estate drags proceeds through probate and can expose them to creditors and estate-level tax.

- Take the lump sum. Choose a single payout over interest-bearing installments, so the beneficiary never reports the insurer's interest as taxable income.

None of this is a loophole. It is the ordinary machinery of estate planning, the same machinery used for real estate and business interests. The reason it works is that the tax code taxes what you own at death, and a properly owned policy is not yours to be taxed.

The irrevocable life insurance trust (ILIT)

An ILIT is the workhorse structure. The trust owns the policy and is named as its beneficiary, so the death benefit never enters the insured's estate. You fund premiums by gifting money to the trust, often using Crummey notices so the gifts qualify for the annual gift-tax exclusion, and the trustee pays the carrier. At death, the trust receives the proceeds and distributes them to your heirs under the terms you set, free of estate tax.

The tradeoff is real and worth stating plainly. Irrevocable means irrevocable. You give up control. You cannot borrow against the policy yourself, change the beneficiaries on a whim, or unwind the trust because your circumstances shifted. That loss of control is the price of moving the asset out of your estate, and it is why an ILIT belongs to people with a genuine estate tax problem, not everyone with a policy. Have a qualified estate attorney draft it. This is not a document to assemble from a template.

Third-party ownership without a trust

A simpler route is to let another adult own the policy outright. An adult child can own a policy on a parent, or one spouse can own a policy on the other, so the insured holds no incidents of ownership. It avoids the cost and rigidity of a trust. The downside is control again, plus the three-party risk covered below. For straightforward family situations it can work. For anything with blended families, creditors, or sizable sums, the trust's guardrails usually win.

Estate-tax structures fit a specific person, not everyone with a policy.

You likely need a structure if

- Your total estate exceeds the federal exemption

- You live in a state with its own estate or inheritance tax

- You own a large policy on your own life

- You want proceeds to bypass probate cleanly

You probably do not if

- Your estate sits comfortably under the exemption

- Your state levies no estate or inheritance tax

- You value control and flexibility over the tax savings

- The death benefit is modest relative to your estate

If you are in the first column, the right move is a conversation that includes an estate attorney. If you are in the second, we will tell you to keep it simple and save the legal fees.

Book a Discovery Call04 / The payout choiceWhy does taking the lump sum lower your tax?

Taking the lump sum lowers tax because it removes the one piece of a payout that is taxable: interest. The death benefit itself is income-tax-free whether you take it all at once or in pieces. The difference appears when you leave the money with the insurer and choose an installment or interest-income option. The insurer pays interest on the held balance, and that interest is taxable income to the beneficiary, reported each year it is paid.

A beneficiary who takes $750,000 as a lump sum reports no income from it. The same beneficiary who leaves it with the carrier and draws it down over a decade reports the interest portion of each payment as taxable income. The principal stays tax-free; the growth on it does not. If the goal is the cleanest tax outcome, take the lump sum and invest or deploy the proceeds on your own terms.

"Tax-free payout" is true of the death benefit, not of the interest an insurer pays to hold it for you. The installment option quietly converts a tax-free benefit into a partly taxable one.

05 / The mistakesWhere do people accidentally create a tax?

Most life insurance tax problems are self-inflicted, created by ownership and beneficiary choices nobody flagged at application. The benefit was going to be tax-free. A setup error turned it taxable. Three mistakes account for nearly all of them.

Naming your estate as beneficiary

This is the most common and the most avoidable. When you name your estate, the proceeds flow into the probate process instead of straight to a person. They can be reached by your creditors, they get tangled in probate delays, and they are counted in the estate for tax purposes. Name a specific person or a trust. The fix costs nothing and takes one beneficiary-form change.

The three-party problem

When the policy owner, the insured, and the beneficiary are three different people, the IRS can treat the death benefit as a taxable gift from the owner to the beneficiary. A wife owns a policy on her husband and names their adult son as beneficiary, and the payout can be characterized as a gift from her. This is the Goodman triangle, and it surprises families every year. Keep the owner and the beneficiary the same party, or route everything through a trust, and the problem disappears.

Transferring a policy for value

Selling or transferring a policy for consideration can trigger the transfer-for-value rule, making part of the death benefit taxable as income. This shows up in business buy-sell arrangements and policy sales more than in family planning. There are exceptions, but they are specific. Before any policy changes hands for money, get the structure reviewed so a tax-free benefit does not become a taxable one.

The tax is rarely the policy's fault. It is the paperwork's.

06 / The frameworkWhere The And Asset fits, and where it doesn't

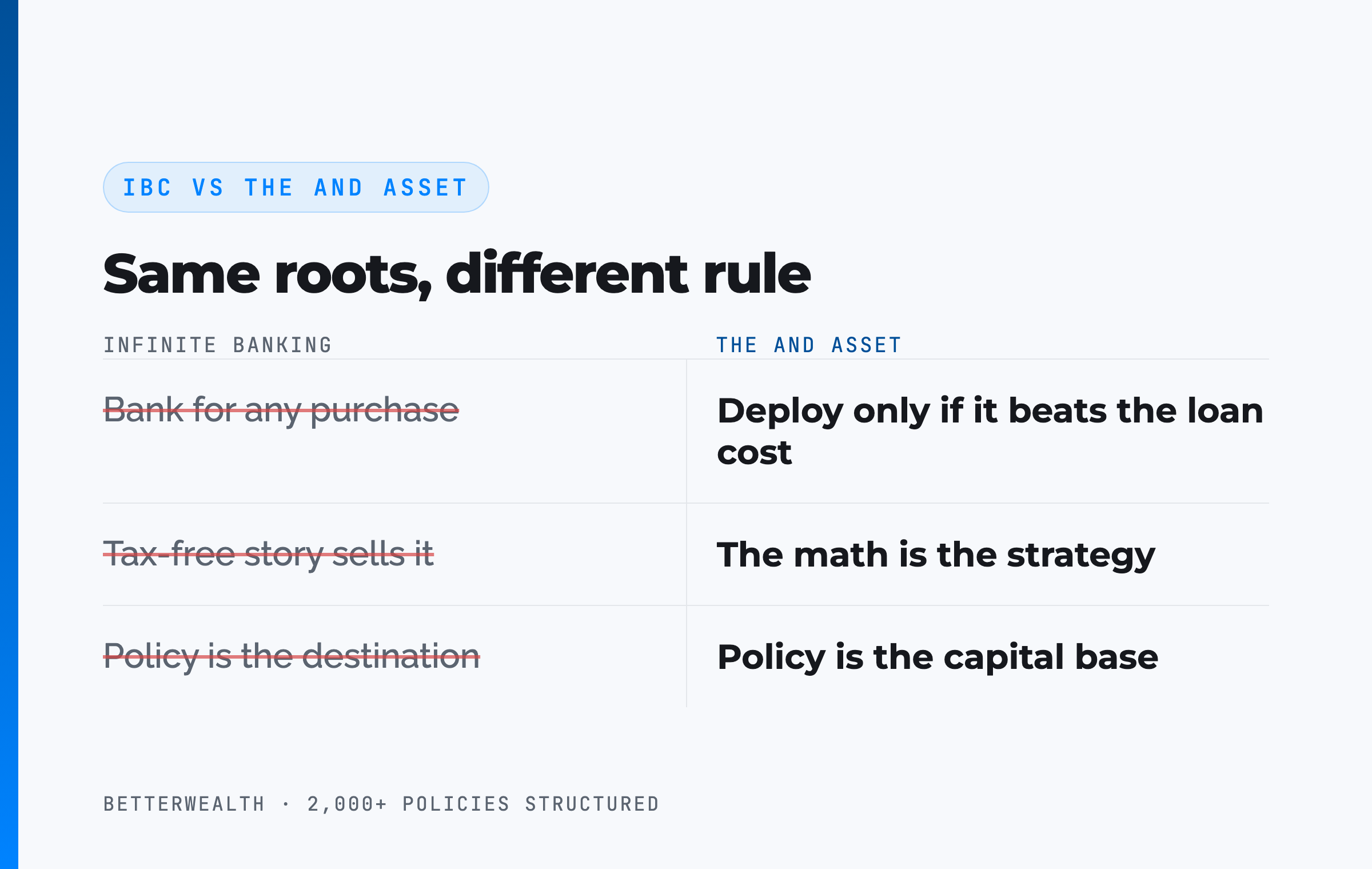

Everything above concerns the death benefit, the money your heirs receive after you are gone. The And Asset is about the opposite end of the policy: the capital you put to work while you are alive. The two are separate questions, and conflating them is how marketing muddies the water.

Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker. We respect that foundation. The And Asset builds on it with one rule that the broader infinite banking message does not enforce. IBC says you can use a whole life policy as a personal bank for any purchase, and it leans hard on the tax-free story to sell it. The And Asset says you only deploy capital from the policy when the borrowed dollars produce a return greater than the carrier's loan cost. The tax treatment is a feature, not the strategy. The strategy is the math.

This distinction matters on a tax page because the tax advantages of life insurance get oversold as the whole pitch. The income-tax-free death benefit is real. The living tax treatment of policy loans is real. Neither one makes a policy worth owning by itself. A policy earns its place when the capital inside it is deployed into activity that clears the loan rate, while the policy keeps compounding at the dividend rate net of mortality and expense charges. If you cannot name a use for that capital that beats the loan cost, the tax benefits alone are not a reason to buy.

Marketers have ruined how this gets explained. The tax-free death benefit is a genuine feature. It is not, on its own, a financial plan, and it is not why The And Asset works.

A composite: the business owner whose policy almost cost his heirs $2.1M

Consider a 58-year-old business owner with a total estate of $24,300,000, including a $5,250,000 whole life policy he owned personally and named his children to receive. This is a representative composite, not a single named client, and the figures are illustrative.

Because he held incidents of ownership, the entire $5,250,000 counted in his estate under IRC Section 2042. With his estate already above the federal exemption, that benefit was exposed at the 40% top rate, an estimated $2,100,000 of avoidable estate tax sitting on top of the rest of his estate's bill.

Working with his estate attorney, he had a newly formed irrevocable life insurance trust apply for and own a replacement policy, funded by annual gifts under Crummey notices. Because the trust owned the policy from inception, there was no three-year lookback to wait out. The death benefit now passes to his children outside his estate. His heirs keep the proceeds his old structure would have taxed. The legal and design work cost a fraction of the $2,100,000 it protected.

The policy was never the problem. The ownership was.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the design frameworks, structuring checklists, and questions we walk through before we ever recommend a carrier or a trust. Free, email-gated, no spam.

Open the Vault07 / Head to headOwnership structures compared

The right ownership structure trades control for estate-tax protection, and the correct choice depends on the size of your estate and how much flexibility you are willing to give up. The table sets the four common arrangements against the dimensions that decide the outcome.

| Dimension | You own the policy | ILIT owns it | Another adult owns it | Business owns it |

|---|---|---|---|---|

| In your taxable estate? | Yes, if you have incidents of ownership | No, when drafted correctly | No, the insured holds no ownership | Depends on ownership and beneficiary setup |

| Control over the policy | Full control | None; the trustee controls it | Owner controls it, not the insured | The business controls it |

| Three-year rule risk | N/A | Applies to transferred policies; avoid with a new policy | Applies to a transferred policy | Applies to a transferred policy |

| Best fit | Estates under the exemption | Large estates needing protection plus control of terms | Simple family situations | Buy-sell and key-person planning |

You own it. The default, and the right answer for the majority of families whose estates sit under the exemption. Full control, full flexibility, and no estate tax because there is no taxable estate to begin with. Do not over-engineer a problem you do not have.

The ILIT owns it. The structure for a genuine estate tax problem. It removes the policy from your estate and lets you dictate how proceeds are distributed, at the cost of control. A new policy issued to the trust avoids the three-year lookback entirely.

Another adult or a business owns it. Third-party ownership is simpler than a trust and works for clean family situations, but it carries the three-party gift risk. Business ownership belongs to buy-sell and key-person arrangements, where the transfer-for-value rule needs a careful review before any policy moves.

The honest 30 minutes about whether you even have a tax to plan for.

We have structured more than 2,000 policies across all 50 states, and we work with estate attorneys on the cases that need one. On a discovery call, a practitioner looks at your estate, your state, and your policy, and tells you whether you need a structure or whether you are already fine. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the strategy.

Book a Discovery CallFAQLife insurance proceeds and tax questions

Are life insurance proceeds taxable?

Life insurance proceeds paid because of the insured's death are generally not subject to federal income tax under IRC Section 101(a). The main exceptions are interest paid on deferred installments, policies transferred for value, and estate tax when the insured owned the policy and the total estate exceeds the federal exemption.

How do I avoid tax on life insurance proceeds?

For most people there is no income tax to avoid, because the death benefit is already income-tax-free. To avoid estate tax on a large policy, move ownership outside your estate (usually through an irrevocable life insurance trust), name a person or trust rather than your estate as beneficiary, and take the death benefit as a lump sum to avoid taxable interest.

When are life insurance proceeds subject to estate tax?

Proceeds are included in your taxable estate when you, the insured, hold incidents of ownership in the policy at death under IRC Section 2042, and your total estate exceeds the federal estate tax exemption. Only estates above that exemption owe federal estate tax, which tops out at a 40% rate. Several states also levy their own estate or inheritance tax at lower thresholds.

What is an irrevocable life insurance trust (ILIT)?

An ILIT is an irrevocable trust that owns a life insurance policy so the death benefit sits outside the insured's taxable estate. The trust is the owner and beneficiary, the insured gifts premium money to the trust, and at death the proceeds pass to heirs free of estate tax. Drafting one requires a qualified estate attorney, and it is irrevocable, so you give up control of the policy.

What is the three-year rule for life insurance?

Under IRC Section 2035, if you transfer an existing policy you own into an ILIT and die within three years of the transfer, the proceeds are pulled back into your taxable estate. Having the trust apply for and own a new policy from the start avoids the three-year lookback entirely.

Should I name my estate as the beneficiary of my life insurance?

No. Naming your estate as beneficiary routes the proceeds through probate, can expose them to your creditors, and can pull them into estate tax calculations. Name a specific person or a trust instead so the proceeds pass directly and stay outside the probate estate.

Is the lump sum or installment payout better for taxes?

The lump sum is generally cleaner for taxes. The death benefit itself is income-tax-free either way, but when proceeds are left with the insurer and paid in installments, the interest portion the insurer pays is taxable income to the beneficiary. Taking the lump sum avoids that taxable interest.

Can having three different people on one policy cause a tax?

Yes. When the policy owner, the insured, and the beneficiary are three different people, the IRS can treat the death benefit as a taxable gift from the owner to the beneficiary. This is often called the Goodman triangle. Keep the owner and beneficiary the same party, or use a trust, to avoid it.

Do I need a trust if my estate is under the exemption?

Usually not. If your total estate, including the death benefit, sits under the federal exemption and your state has no estate or inheritance tax, the proceeds pass income-tax-free and estate-tax-free without any special structure. Paying for a trust you do not need is a common and avoidable cost.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base during your lifetime. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. It shares roots with IBC but operates on different principles. It concerns the living use of the policy, not the death-benefit estate planning covered in this guide.

- IRC Section 101 (Cornell Law), the exclusion of life insurance death benefits from gross income.

- IRC Section 2042 (Cornell Law), proceeds included in the gross estate through incidents of ownership.

- IRC Section 2035 (Cornell Law), the three-year rule on transferred policies.

- IRS, Estate Tax, current federal exemption amounts and filing requirements.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

This article is educational and does not constitute tax or legal advice. Federal and state estate tax rules, exemption amounts, and thresholds change with legislation and inflation indexing. Confirm current figures with the IRS and work with a qualified estate attorney and tax professional before establishing any trust or changing policy ownership.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, and we coordinate with estate attorneys on the cases that need one. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether you even have a tax to plan for, book a discovery call. We will tell you if you are already fine.