.png)

Section 7702 of the Internal Revenue Code defines the tests a life insurance policy must pass to earn its tax treatment: tax-deferred cash value growth, an income-tax-free death benefit, and policy loans treated as debt rather than taxable income. Meet the tests and the treatment holds; fail them and it collapses.

The phrase "tax-free income" sells policies and ruins credibility at the same time. An entrepreneur or a high-income physician hears it, runs the math in their head, and either dismisses the whole strategy as too good to be true or buys it for the wrong reason. Both outcomes trace back to the same problem. The tax treatment of permanent life insurance is real, it is durable, and it is governed by a specific section of the tax code that almost nobody who pitches it explains accurately.

A policy loan is tax-exempt cash flow, not tax-free income, and the difference is the entire strategy. One is a precise description of borrowing against an asset. The other is a marketing phrase that papers over the conditions that make the treatment work. When those conditions are understood, the tax advantage is defensible for decades. When they are ignored, the IRS has a clean path to reclassify everything.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and Section 7702 is the legal foundation under every one of them. This guide covers what Section 7702 actually governs, the two tests a policy must pass, why a loan is not income, the line you cannot cross without creating a Modified Endowment Contract, and how the tax treatment fits into the broader life insurance strategy we call The And Asset. We will also be precise about what the tax code does not promise.

- Section 7702 defines what qualifies as life insurance for federal tax purposes; meeting it unlocks the tax-deferred growth and loan treatment.

- A policy loan is tax-exempt cash flow, not tax-free income, because a loan is debt against your cash value, not a distribution.

- Cash value grows tax-deferred net of mortality and expense charges, with no annual tax while the policy stays in force.

- Overfunding past the 7-pay limit under Section 7702A creates a MEC, which taxes loans as ordinary income last-in-first-out.

- Section 7702 was added to the tax code in 1984; Congress updated its interest rate assumptions effective 2021.

- The treatment can collapse if the policy lapses with a loan outstanding, converting deferred gain into taxable income.

01 / The problemWhat Section 7702 actually governs (and what it doesn't)

Section 7702 governs one question: does a contract qualify as life insurance for federal income tax purposes? That is the whole job of the statute. It does not promise returns, it does not guarantee a rate, and it does not make anything magically free of tax. It draws the line between a contract the tax code treats as insurance and a contract it treats as an investment.

That distinction carries the entire tax advantage. A contract on the insurance side of the line gets tax-deferred internal growth, an income-tax-free death benefit under Section 101(a), and the ability to access cash through loans without triggering a taxable event. A contract that fails the tests loses those features and gets taxed like a brokerage account. So the tax strategy is not a trick. It is the consequence of designing a policy that stays on the right side of a definition Congress wrote in 1984.

The tax code does not give you a loophole. It gives you a definition. Everything people call "the tax-free strategy" is just the result of staying inside that definition on purpose.

02 / The two testsWhat are the two Section 7702 tests?

Section 7702 offers two tests, and a policy must satisfy one of them to be taxed as life insurance. They both do the same job from different angles: they keep the cash value from overwhelming the death benefit, which is what would turn the contract into a pure investment wrapper.

The Cash Value Accumulation Test (CVAT)

The Cash Value Accumulation Test limits the cash value relative to the death benefit at every point in time. Cash value can never exceed the net single premium needed to fund the policy's future benefits. For cash-value-focused designs, this is usually the test of choice because it permits more cash relative to premium. It is the test most often used under the hood of an And Asset policy.

The Guideline Premium Test (GPT)

The Guideline Premium Test limits the premium you can pay relative to the death benefit and layers in a cash value corridor that forces the death benefit to stay a set distance above the cash value. It caps contributions more tightly. Designs that prioritize a specific premium schedule sometimes use it. Neither test is better in the abstract. The right one depends on how the policy is built and what the owner is solving for.

Pass one test. The tax treatment follows.

03 / The loanWhy is a policy loan tax-exempt cash flow and not income?

A policy loan is tax-exempt cash flow because it is a loan, not a distribution, and borrowed money is not income under the tax code. When you borrow against your cash value, the insurer advances you funds and holds your policy as collateral. You have not sold anything, withdrawn anything, or realized a gain. There is no taxable event because no income exists to tax.

This is where the language matters more than anywhere else in the strategy. "Tax-free income" implies you received income and dodged the tax on it. You did neither. You took on a debt, secured by an asset that keeps compounding. Calling that income is both wrong and dangerous, because it sets up the reader to ignore the conditions that keep the loan free of tax.

The conditions that keep the loan untaxed

Two conditions hold the treatment together. The policy must stay in force, and it must not be a Modified Endowment Contract. Break either one and the math changes. If the policy lapses or is surrendered with a loan outstanding, the outstanding gain can be treated as taxable income in the year it lapses, which is the single most common way people lose this treatment. Borrow carelessly and you can manufacture a tax bill on money you already spent.

A loan is debt, not income. Treat it that way.

Marketers have ruined how this gets explained. There is no such thing as tax-free income from a policy loan. There is tax-deferred growth and tax-exempt loan access on a policy you keep in force. Precision is the strategy.

The Section 7702 strategy fits a specific person.

It fits you if

- You are a high-income earner who has maxed conventional tax-advantaged accounts

- You want tax-deferred growth with flexible, untaxed access to capital

- You can fund consistently for a decade or more

- You can name a use for borrowed capital that beats the loan cost

It does not fit you if

- You want a short-term tax dodge or a quick win

- You expect the dividend rate to be your return

- You cannot commit to keeping the policy in force long term

- You want a savings account, not a life insurance strategy

If you are in the first column, a 30-minute conversation will tell you whether a properly structured policy belongs in your plan. If you are in the second, we will tell you that too.

Book a Discovery Call04 / How it worksHow to keep a policy's Section 7702 treatment intact

Keeping the tax treatment intact comes down to five mechanical steps, and the order matters because each one protects the step before it. Here is the sequence we use when we structure a policy designed for cash value and capital access.

- Pass the 7702 tests. Design the policy to satisfy either the Cash Value Accumulation Test or the Guideline Premium Test. This is what makes the contract taxed as life insurance in the first place. Get this wrong and nothing else matters.

- Stay under the MEC limit. Fund the paid-up additions rider aggressively, but keep premiums inside the 7-pay limit under Section 7702A. The base/PUA split is the design lever that pushes cash value to the edge of the line without crossing it.

- Let cash value grow tax-deferred. Allow the cash value to compound net of mortality and expense charges. There is no annual tax on that internal growth while the policy is in force. Do not expect cash value to exceed your contributions early; for a healthy individual, break-even typically arrives at year five or later.

- Access cash through a policy loan. Borrow against the cash value rather than withdrawing it. A loan is debt, not a distribution, so it is not taxable income. The policy keeps compounding on its full value while the loan is outstanding.

- Keep the policy in force. Manage the loan so the policy does not lapse with a gain outstanding. A lapse can convert deferred gain into taxable income in a single year. This is the discipline that protects everything above it.

None of these steps is exotic. They are the unglamorous mechanics that turn a tax definition into a durable strategy, and they are exactly the part most sales presentations skip.

05 / The MEC lineWhat is a Modified Endowment Contract, and why does it matter?

A Modified Endowment Contract is a policy funded faster than the tax code allows for full insurance treatment, and crossing into MEC status quietly breaks the loan strategy. Section 7702A sets a 7-pay limit, a ceiling on how much premium can go in over the first seven years relative to the death benefit. Pay in faster than that and the contract becomes a MEC.

A MEC still keeps its income-tax-free death benefit. What it loses is the loan treatment. Loans and withdrawals from a MEC are taxed last-in-first-out as ordinary income, meaning gain comes out first and gets taxed first. Distributions before age 59 and a half carry an additional 10% penalty. For a strategy built on borrowing against the policy, that reclassification defeats the purpose.

The counterintuitive part is that the MEC limit is what forces good design. To put the maximum capital to work without tripping the line, you carry more death benefit than a pure cash play would suggest. That extra death benefit adds internal cost, which is the price of staying inside the definition. A well-built policy rides close to the MEC line on purpose and never crosses it.

The MEC limit is not a flaw in the strategy. It is the guardrail that keeps the strategy legal. Designing right up to it, and not past it, is most of the skill.

06 / The frameworkHow does Section 7702 fit into The And Asset?

Section 7702 is the legal foundation; The And Asset is the strategy built on top of it. The tax treatment makes the policy an efficient place to hold and access capital. The framework decides what you do with that capital. This is the broader strategy we cover in our pillar guide, What Is Infinite Banking? The And Asset Guide, and Section 7702 is the engine room underneath it.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule that Nash's broader teaching does not enforce.

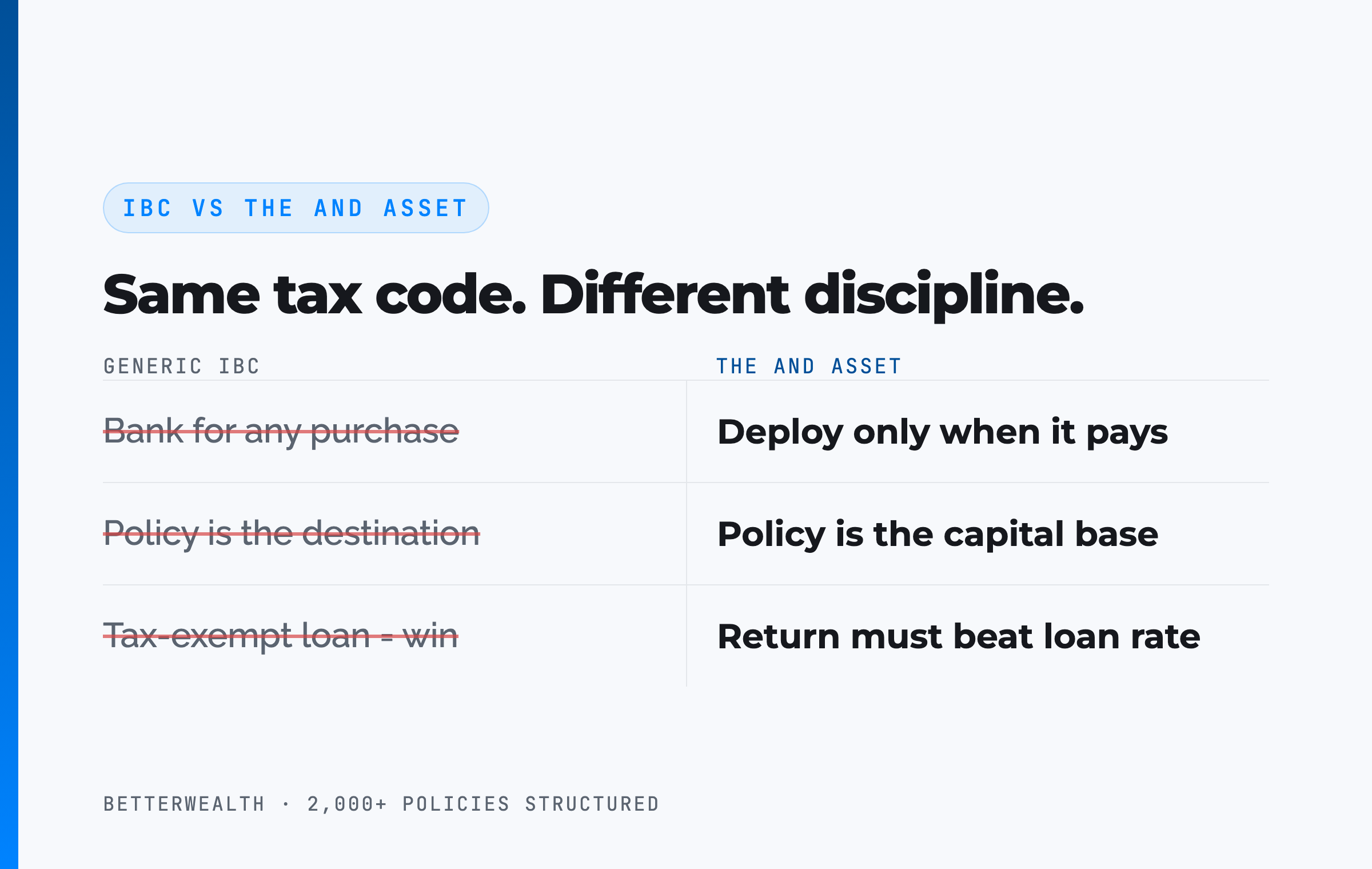

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The tax treatment under Section 7702 does not change that test. A tax-exempt loan that funds a losing deal is still a losing deal. The tax advantage is the wrapper. The discipline is the strategy.

The tax treatment is the floor, not the reason.

07 / The mathDoes the return still have to clear the loan cost?

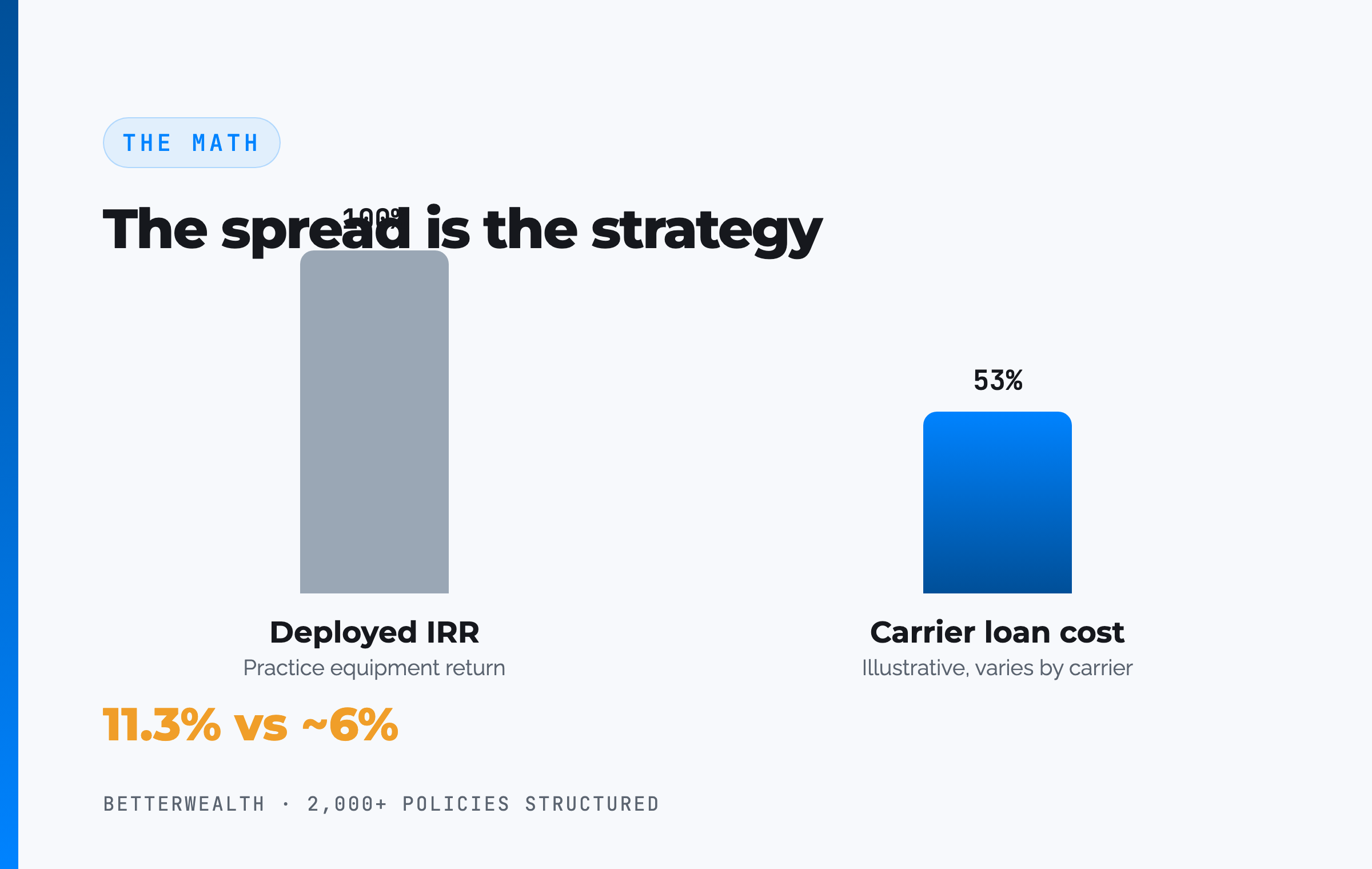

The return on whatever you deploy must exceed the carrier's loan cost, and the tax treatment does not lower that bar. People assume the tax advantage means the loan is close to free. It is not. You borrow at the carrier's loan rate, which varies by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat that as a variable to verify, not a constant.

Here is the full picture. The policy keeps compounding on its full cash value, net of internal costs, while the loan is outstanding. Your deployed capital earns its own return. The loan interest goes to the carrier, not back to you. If the deployed return clears the loan cost, you are ahead on the spread, and the same dollar has done two jobs. The Section 7702 treatment means you did not pay tax to access that dollar. It does not mean the dollar was free to borrow.

No tax on access. Real cost on the loan. Both are true.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to keep policies inside the Section 7702 and MEC lines while maximizing cash value. Free, email-gated, no spam.

Open the Vault08 / The historyWhy the legislative history matters (and what to ignore)

Section 7702 was added to the Internal Revenue Code in 1984, and that single fact corrects a lot of bad content. The favorable tax treatment of permanent life insurance is older than Section 7702 itself. What 1984 added was the definitional framework: the tests that decide whether a modern contract still earns that treatment. Congress wrote those rules to stop policies from being used as pure tax-sheltered investment accounts.

Be skeptical of any source that assigns Section 7702 a century-long history or claims another account type was modeled on it. Those origin stories circulate widely and are usually wrong. The defensible version is narrow: the tax treatment of life insurance predates the modern tests, the tests themselves date from 1984, and Congress updated the section's prescribed interest rate assumptions effective 2021. On a topic the IRS enforces, unsourced history is a credibility risk, not a flourish.

If a presentation tells you Section 7702 is "over a hundred years old" or that another retirement account "was built on it," close the tab. The tests came in 1984. The accuracy is the authority.

09 / Head to headSection 7702 treatment versus other tax wrappers

Compared to the tax wrappers high-income earners already use, a Section 7702 policy trades day-one liquidity for flexible, untaxed access and control. The table sets it against a Roth IRA, a traditional 401(k), and a taxable brokerage account on the four dimensions that decide where capital should live.

| Dimension | Section 7702 Policy | Roth IRA | Traditional 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Growth taxation | Tax-deferred, net of internal costs, while in force | Tax-free growth after funding with after-tax dollars | Tax-deferred now, taxed later | Taxed annually on gains and dividends |

| Access to capital | Loans anytime; not taxable while in force and non-MEC | Contributions anytime; earnings restricted before 59½ | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

| Contribution limits | No statutory cap; bounded by the MEC line and death benefit | Low annual cap with income phase-outs | Annual cap set by the IRS | No limit |

| Death benefit | Generally income-tax-free under §101(a) | Passes to heirs, subject to account rules | Taxable as ordinary income to heirs | Stepped-up basis at death |

Growth and access. A 7702 policy grows tax-deferred and lets you access capital through loans without a taxable event, which a 401(k) cannot do before 59 and a half without penalty. That access is the feature high-income earners are usually missing once their qualified accounts are maxed.

Limits. A Roth IRA is excellent but capped and phased out at higher incomes. A Section 7702 policy has no statutory contribution cap; its ceiling is the MEC line relative to the death benefit, which is why design matters so much.

The honest tradeoff. The brokerage account wins on raw liquidity and simplicity. The policy wins on tax treatment and control, and it asks for a long horizon and disciplined funding in return. This is a capital wrapper, not a market substitute.

A composite: the physician who accessed capital without a tax event

Consider a 44-year-old physician, preferred non-tobacco, who has maxed her 401(k) and backdoor Roth and is looking for what comes next. She funds a whole life policy at $63,500 per year on a cashflow design, structured to satisfy the Cash Value Accumulation Test and stay inside the 7-pay limit. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year eight, with roughly $498,000 of accessible cash value, she borrows $215,000 against the policy to acquire revenue-producing equipment for her practice. Because the loan is debt and not a distribution, the $215,000 is not taxable income. The policy keeps compounding on its full value the entire time. The equipment returns an estimated 11.3% IRR against an illustrative loan cost near 6%, so the spread works in her favor by more than five points. Repayment runs on a 47-month schedule funded by the equipment's own cash flow, and the policy never lapses, so the Section 7702 treatment stays intact.

No tax on access. A real return on deployment. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a properly designed, Section 7702 compliant policy belongs in your plan, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQSection 7702 tax questions

What is Section 7702 in life insurance?

Section 7702 of the Internal Revenue Code defines the tests a contract must pass to be taxed as life insurance. When a policy qualifies, its cash value grows tax-deferred, the death benefit is generally income-tax-free under Section 101(a), and policy loans are treated as debt rather than taxable distributions.

Is a policy loan tax-free income?

No. A policy loan is tax-exempt cash flow, not tax-free income. It is a loan against your cash value, so it is not income at all. It is only free of tax as long as the policy stays in force and is not a Modified Endowment Contract. If the policy lapses with a loan outstanding, the gain can become taxable.

When was Section 7702 added to the tax code?

Section 7702 was added to the Internal Revenue Code in 1984. The favorable tax treatment of permanent life insurance predates that, but the specific definitional tests in Section 7702 date from 1984, and Congress updated the section's interest rate assumptions effective 2021.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does cash value grow tax-free or tax-deferred?

Cash value grows tax-deferred. There is no annual tax on the internal growth while the policy stays in force, and the growth compounds net of mortality and expense charges. The growth can be accessed tax-efficiently through loans, but tax-deferred is the precise word for the accumulation phase, not tax-free.

What is a Modified Endowment Contract (MEC)?

A Modified Endowment Contract is a policy that was funded faster than the 7-pay limit set in Section 7702A. A MEC keeps its income-tax-free death benefit, but loans and withdrawals are taxed last-in-first-out as ordinary income, with a 10% penalty before age 59 and a half. Proper design avoids the MEC line on purpose.

Is the death benefit from life insurance taxable?

For a policy that qualifies under Section 7702, the death benefit is generally received income-tax-free by the beneficiary under Section 101(a). Estate tax can still apply depending on ownership and the size of the estate, which is a separate question from income tax.

What are the two Section 7702 tests?

Section 7702 offers two tests, and a policy must satisfy one of them. The Cash Value Accumulation Test limits cash value relative to the death benefit. The Guideline Premium Test limits premium relative to the death benefit and adds a cash value corridor. Cash-value-focused designs typically use the Cash Value Accumulation Test.

Why do marketers call this tax-free income?

Because it sounds better than the accurate version. The honest description is tax-deferred growth plus tax-exempt loan access on a policy kept in force. Calling a loan tax-free income skips the conditions that make it work and is the kind of overselling that damages credibility on a topic the IRS takes seriously.

- IRC Section 7702 (Cornell Law), the statutory tests defining a contract as life insurance for tax purposes.

- IRC Section 7702A (Cornell Law), the Modified Endowment Contract rules and the 7-pay test.

- IRC Section 101 (Cornell Law), the income-tax exclusion for life insurance death benefits.

- Internal Revenue Service, primary guidance on the tax treatment of life insurance contracts.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a Section 7702 strategy fits your plan, book a discovery call. We will tell you if it does not.