.png)

Life insurance for business owners does three jobs: it protects the company against the death of a key person, funds an ownership buyout through a buy-sell agreement, and builds accessible cash value the business or owner can borrow against. Who owns, pays, and benefits decides the tax result.

Most business owners buy life insurance the way they buy a fire extinguisher, as a thing they hope never to use, bought once and forgotten. That framing misses what the tool actually does inside a company. A policy is not only a payout when someone dies. It can be a continuity plan, a succession mechanism, and a capital reserve, depending on how it is owned and structured.

The right question is not whether a business owner needs life insurance, but which of three jobs the policy is being hired to do. Each job has a different owner, a different beneficiary, and a different tax treatment. Confuse them, and you either overpay, underprotect, or trigger a tax bill that a few pages of paperwork would have avoided.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, many of them for business owners deploying capital. This guide covers the three core uses plainly, states the tax rules under IRC Sections 101 and 264 precisely, and shows where a permanent policy's cash value becomes capital the business can use. We are not your CPA or your attorney, and you will need both for the actual structures. What we can do is tell you how the pieces fit so the conversations with those advisors are sharper.

- Business life insurance does three jobs: key person protection, buy-sell funding, and accessible cash value for the business or owner.

- A death benefit is generally received income-tax-free under IRC Section 101(a), which is the core reason the structure works.

- Premiums are generally not deductible under IRC Section 264 when the business is directly or indirectly the beneficiary.

- Employer-owned policies must clear the IRC 101(j) notice-and-consent rules before issue, or the death benefit can become taxable.

- Who owns, who pays, and who benefits drives the tax result, so personal and business-owned policies are not interchangeable.

- A CPA and an attorney build the actual structures. This guide makes those conversations faster and more precise.

01 / The problemWhat a business actually loses, and what insurance covers

A business faces three distinct exposures when an owner or key contributor dies, and a single policy rarely covers all three. The first is operational: revenue, relationships, and institutional knowledge walk out the door with the person. The second is structural: a deceased owner's shares pass to heirs who may have no role in or knowledge of the company. The third is the slow leak almost nobody plans for: capital that sits idle in the business earning nothing while the owner waits for the right moment to deploy it.

Each exposure maps to a different use of life insurance. Key person coverage answers the first. A buy-sell agreement answers the second. A permanent policy's cash value addresses the third. Treating them as one purchase is how owners end up with the wrong amount of the wrong type owned by the wrong party.

The mistake is not buying too little life insurance. It is buying one policy to do three jobs, then discovering at the worst possible moment that it was structured for none of them.

02 / Key personHow does key person life insurance protect the business?

Key person life insurance protects the business by giving the company cash to survive the death of someone it cannot easily replace. The business owns the policy, pays the premium, and is the named beneficiary. When the insured dies, the death benefit goes to the company, not the family, and the company uses it to absorb lost revenue, recruit and train a replacement, and reassure lenders and partners that the business will continue.

The insured is usually a founder, a top producer, a lead engineer, or anyone whose absence would materially dent revenue. A bank that extended a loan on the strength of one person's relationships often requires this coverage. So does a partner who is counting on that person to keep the enterprise running.

The depth of this topic, including how to size the coverage to the revenue and recruiting cost actually at risk, is covered in our dedicated breakdown of how key person life insurance works. The short version: size it to what the business would spend to stay whole, not to a round number that sounds reassuring.

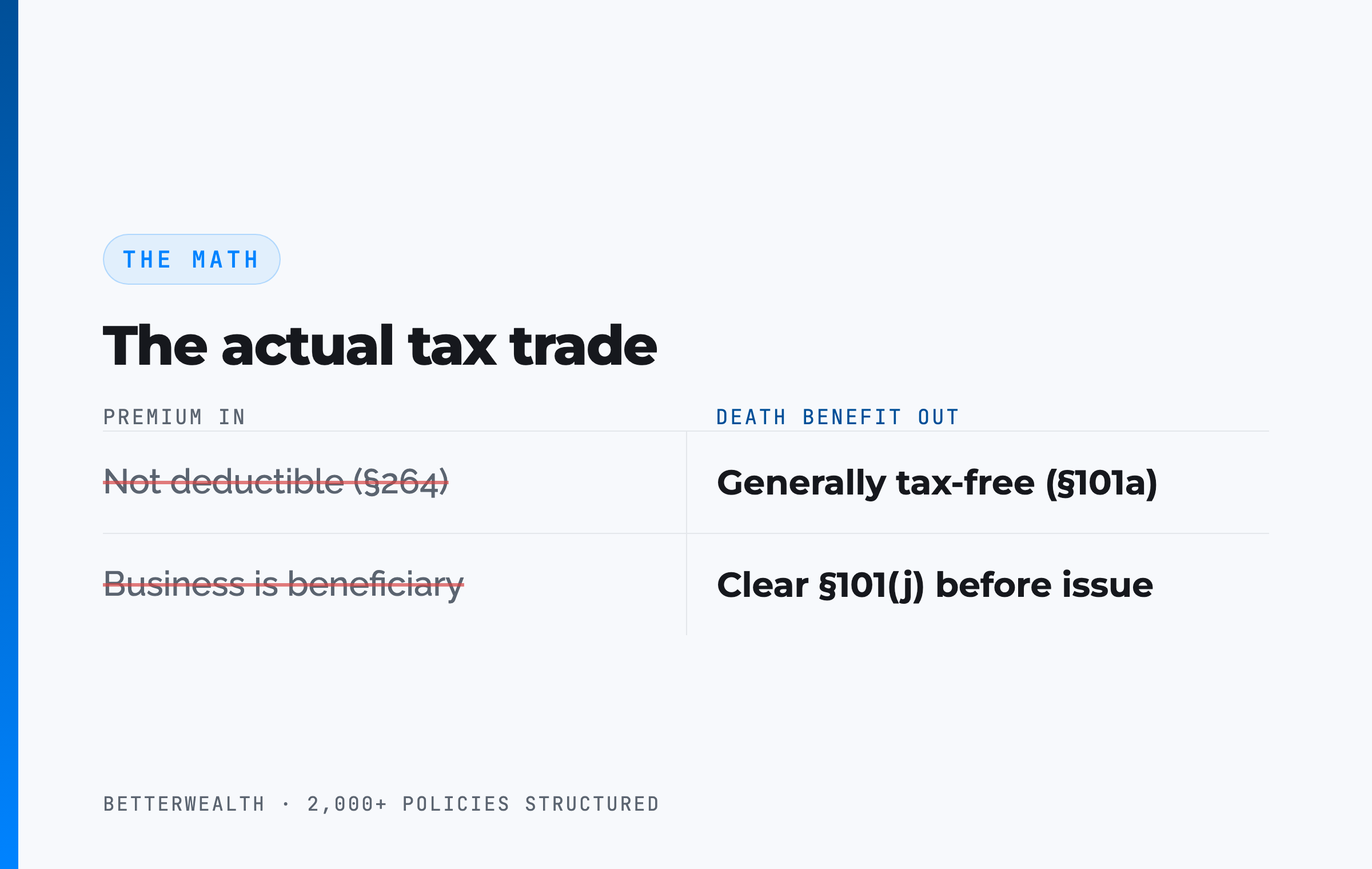

The business is the beneficiary. That changes the tax math.

Because the company is the beneficiary, the premium is generally not deductible under IRC Section 264. In exchange, the death benefit is generally received income-tax-free under IRC Section 101(a), provided the employer-owned rules are met. We cover those rules in section 05.

03 / Buy-sellHow does life insurance fund a buy-sell agreement?

Life insurance funds a buy-sell agreement by supplying the cash to buy a deceased owner's share at a price the agreement fixes in advance. A buy-sell agreement is the legal document that says what happens to ownership when an owner dies, retires, or exits. Without funding, that document is a promise with no money behind it. Life insurance is the money.

Picture two partners who each own half of a business worth several million dollars. One dies. The agreement says the survivor buys the deceased partner's half, and the family receives fair value in cash. The death benefit funds that purchase. The survivor keeps control of a business they understand. The family gets liquidity instead of an illiquid stake in a company they cannot run. Everyone gets what the agreement promised, because the cash showed up the day it was needed.

Cross-purchase versus entity purchase

The two common structures decide who owns the policies. In a cross-purchase, each owner buys a policy on the other owners, so the survivors personally hold the cash to fund the buyout. In an entity purchase (a stock redemption), the business owns the policies and buys back the deceased owner's shares. The choice affects basis, the number of policies required, and the tax outcome, which is exactly why an attorney drafts the agreement and a CPA models the consequences.

We go deep on both structures, including the trap of an unfunded or outdated agreement, in our guide to funding a buy-sell agreement with life insurance. The recurring failure we see is an agreement signed years ago, never funded, and never revalued, so the price in the document bears no relationship to what the business is worth today.

An unfunded buy-sell is a handshake with a dead partner's family. The document names a price. The insurance is what makes that price real.

04 / Cash valueHow a permanent policy becomes a business capital reserve

A permanent policy becomes a capital reserve because, beyond the death benefit, it accumulates a cash value the owner can borrow against while it keeps compounding. Term insurance covers the first two jobs cleanly and cheaply: it is pure protection, it expires, and it builds no cash value. Permanent insurance adds a living asset. A properly designed whole life policy grows a borrowable cash value net of mortality and expense charges, which means the business or the owner has a pool of capital that does not sit in a checking account earning nothing.

This is where life insurance stops being only a death-triggered payout and starts being a balance-sheet asset. A business owner with cash value can borrow against the policy to fund inventory, cover payroll through a slow season, or seize an acquisition, while the policy continues to compound on its full value. The mechanics, ownership questions, and tax treatment of using a policy this way are the subject of our guide on how business owners use cash value life insurance.

Two precision points keep this honest. Cash value does not exceed cumulative premiums in the early years. For a healthy individual with a well-designed policy, break-even typically lands at year five or later, and any illustration showing year-one or year-two break-even is fiction. And the policy compounds at the dividend rate net of mortality and expense charges, not at the gross dividend rate an agent might quote.

Business life insurance fits a specific owner doing specific things.

It fits you if

- Your business would lose real revenue if a key person died

- You have partners and need a funded succession plan

- You want a capital reserve you control, not idle cash

- You can name a use for borrowed capital that beats the loan cost

It does not fit you if

- You only need term protection and nothing more

- You want a tax deduction on the premium (you generally will not get one)

- You are looking for a savings account dressed up as insurance

- You cannot identify a productive use for the cash value

If you are in the first column, a 30-minute conversation will tell you how to size and own each piece. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The tax rulesIs life insurance tax-deductible for a business?

Generally, no. Premiums on a business life insurance policy are not deductible under IRC Section 264 when the business is directly or indirectly a beneficiary of the policy. This catches most owners by surprise, because so many business expenses are deductible. Life insurance is built differently, and the reason is the offsetting benefit on the other side.

That offsetting benefit is the death benefit itself. Under IRC Section 101(a), life insurance proceeds paid by reason of the insured's death are generally received free of federal income tax. The tax code's logic is a tradeoff: you do not deduct the premium going in, and the proceeds come out income-tax-free. For a buy-sell or key person policy, that tax-free death benefit is the entire point, so the lost deduction is a fair price.

The IRC 101(j) trap on employer-owned policies

Employer-owned policies carry a rule that quietly converts a tax-free benefit into a taxable one if you skip a step. Under IRC Section 101(j), when a business owns a policy on an employee, the income-tax-free treatment applies only if the business gave written notice, obtained the employee's written consent, and met a stated exception, all before the policy was issued. Miss the notice-and-consent, and the death benefit above the premiums the business paid can become taxable income to the company. This is paperwork, completed once, before issue. It is also one of the most common and most expensive oversights we see.

Notice and consent. Before the policy is issued. Every time.

A separate hazard is the transfer-for-value rule, which can taint the tax-free death benefit when a policy is sold or transferred for consideration outside specific safe harbors. This is one more reason the structure belongs in the hands of a CPA and an attorney, not a spreadsheet and good intentions.

Anyone selling you business life insurance as a tax deduction is selling you the wrong story. The premium is generally not deductible. The death benefit is generally tax-free. That is the actual trade.

06 / OwnershipPersonal or business-owned: who owns, pays, and benefits?

The right owner depends entirely on the job the policy is doing, and getting it wrong is what creates avoidable tax problems. Three questions decide every business life insurance structure: who owns the policy, who pays the premium, and who receives the death benefit. The answers are not cosmetic. They determine deductibility, basis, and whether the proceeds land where they are supposed to.

For income replacement, the policy is usually owned personally by the owner or an irrevocable trust, paid with personal dollars, and payable to the family. For key person coverage, the business owns it, pays it, and collects it. For a buy-sell, ownership follows the structure: the individual owners in a cross-purchase, or the company in an entity purchase. Each arrangement produces a different tax outcome, which is why a CPA and an attorney should confirm the structure before the application is signed.

| The job | Typical owner | Who pays | Beneficiary |

|---|---|---|---|

| Income replacement | Owner personally or a trust | Personal funds | The owner's family |

| Key person | The business | The business | The business |

| Buy-sell (cross-purchase) | The other owners | The other owners | The surviving owners |

| Buy-sell (entity purchase) | The business | The business | The business |

Read the table as a starting map, not a prescription. The right structure for your entity type, your state, and your goals is a conversation with your advisors. What the map shows is that there is no single correct owner, only a correct owner for each job.

07 / The And AssetWhat turns business cash value into deployable capital?

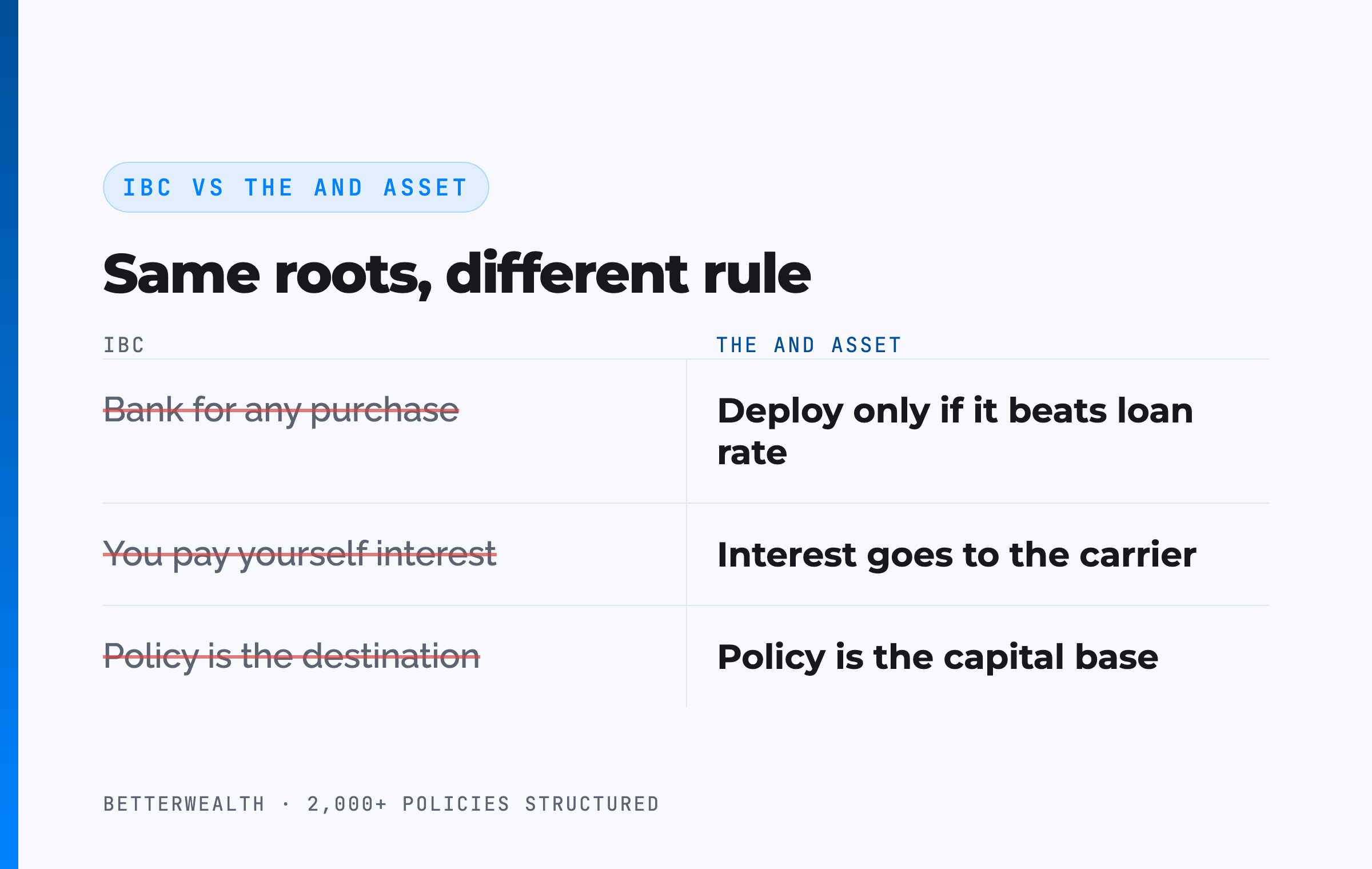

What turns cash value into deployable capital is a discipline we call The And Asset, and it is where most generic infinite banking advice goes wrong. Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. For a business owner, that threshold is natural, because owners already think in IRR and opportunity cost. If a piece of equipment, an inventory buy, or an acquisition will out-earn the loan rate, borrowing makes sense. If it will not, leave the cash value compounding and do not borrow.

This is the contrast that matters: many marketers say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns in the business while the policy keeps compounding uninterrupted. If you are new to the framework, our pillar explainer covers what infinite banking is and how The And Asset guide reframes it for people who actually deploy capital.

If the deal does not beat the loan rate, do not borrow.

Loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6 percent range, but treat the specific number as a variable to verify, not a constant. The discipline is permanent. The rate is not.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use when we structure key person, buy-sell, and cash-value policies for business owners. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsThe honest case for and against business life insurance

Business life insurance carries real tradeoffs that disqualify it for some owners, and pretending otherwise is how agents lose trust. The benefits are concrete: a tax-free death benefit under Section 101(a), continuity when a key person dies, a funded succession plan, and a permanent policy's borrowable cash value as a capital reserve. Those are worth real money to the right owner.

The costs are just as concrete. Premiums are generally not deductible. Permanent coverage costs more than term, and the cash value takes years to build, with break-even typically at year five or later. The structures require a CPA and an attorney, which means real fees and real coordination. And the IRC 101(j) rules and transfer-for-value traps punish sloppy paperwork. If your only need is pure protection for a defined period, term insurance does that job for a fraction of the cost, and you should not pay for features you will never use.

Right tool, right job, or it is just expensive.

Permanent insurance is not better than term. It does a different job. The skill is matching the tool to the job, not buying the most expensive version and hoping it covers everything.

09 / How it worksHow a business owner puts a policy to work, step by step

Putting business life insurance to work follows five steps, and the order keeps you out of trouble. This is the sequence we walk owners through before any application is signed.

- Name the job. Decide which exposure you are covering: key person protection, ownership succession, income replacement, or cash value as capital. Most owners need more than one, sized separately.

- Set ownership, payer, and beneficiary. Match each job to the right owner, payer, and beneficiary using the map in section 06. This single decision drives the tax result.

- Clear the employer-owned rules. If the business owns a policy on an employee, complete the IRC 101(j) written notice and consent before the policy is issued. Do this first, not later.

- Confirm the tax treatment with advisors. Have your CPA confirm deductibility and basis, and your attorney draft or update the buy-sell agreement and any valuation clause. Premiums are generally not deductible under IRC 264 when the business benefits.

- Deploy cash value with discipline. If the policy is permanent and builds cash value, borrow against it only for an activity that returns more than the carrier's loan cost. Otherwise, leave it compounding.

None of these steps is exotic. They fail only when an owner skips one, usually the paperwork in step three or the advisor coordination in step four, and discovers the gap at the worst possible time.

10 / Head to headTerm, permanent, and the alternatives owners actually use

Compared to the other ways a business holds protection and capital, a permanent policy trades higher early cost for a tax-free death benefit and a borrowable cash value. The table sets term insurance, permanent insurance, and a plain cash reserve against the four dimensions that matter to a business owner.

| Dimension | Term life | Permanent (cash value) | Business cash reserve |

|---|---|---|---|

| Death benefit | Yes, for a fixed term, then expires | Yes, for life, generally tax-free under §101(a) | None; it is cash, not coverage |

| Builds usable capital | No cash value | Borrowable cash value, compounding net of costs | Fully liquid, but earns little and is taxed on yield |

| Cost | Lowest premium for the coverage | Higher premium; break-even at year 5+ | No premium; full opportunity cost of idle cash |

| Best job | Pure key person and buy-sell protection on a budget | Long-horizon protection plus a capital base | Short-term operating liquidity |

Term life. For pure protection over a defined window, term is the right answer and the cheapest one. It funds a key person need or a buy-sell on a budget. It builds no cash value, so it is not a capital asset, and it expires.

Permanent insurance. A permanent policy costs more and takes years to build cash value, but it pairs a lifelong, generally tax-free death benefit with a borrowable capital base. That is the structure behind The And Asset, and it fits owners with a long horizon who will actually deploy the capital.

Cash reserve. Cash in the business is liquid and simple, but it earns almost nothing and carries the full opportunity cost of sitting idle. The case for cash value is that the same dollar can stay protected, keep compounding, and still back a loan when an opportunity appears.

A composite: the partners who funded their buy-sell and built a reserve

Consider two co-owners of a logistics business, both 44, preferred non-tobacco, each owning half of a company valued at roughly $4.2 million. This is a representative composite, not a single named client.

They started with a cross-purchase buy-sell, each owning a $2,100,000 policy on the other, with the agreement revalued annually so the price tracks the business. That alone solved the structural exposure: if either dies, the survivor buys the shares and the family receives fair cash value.

They chose a permanent design over term for one partner who wanted a capital base. Through the first three years, that policy's cash value trailed cumulative premiums, exactly as a real policy should. By year six, on the overfunded design, cash value crossed total contributions. No earlier. In year eight, with roughly $318,000 of accessible cash value, that partner borrowed $164,500 against the policy to buy revenue-producing equipment for the fleet. The equipment returned an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread worked in the owner's favor by nearly eight points, and the policy kept compounding on its full value the entire time. Repayment ran on a 41-month schedule funded by the equipment's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about how to structure it.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your business, your partners, and your goals, and tells you how to size and own each piece, working alongside your CPA and attorney. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQLife insurance for business owners, answered

Why do business owners need life insurance?

Business owners use life insurance for three jobs: protecting the business against the death of a critical person through key person coverage, funding ownership succession through a buy-sell agreement, and building accessible cash value the business or owner can borrow against. A personal policy can also replace income for the owner's family. Most owners need at least two of these, sized separately.

Is life insurance tax-deductible for a business?

Generally no. Under IRC Section 264, premiums are not deductible when the business is directly or indirectly a beneficiary of the policy. The offsetting benefit is that the death benefit is generally received income-tax-free under IRC Section 101(a). Have a CPA confirm your specific structure.

What is key person life insurance?

Key person life insurance is a policy the business owns and pays for on an owner or employee whose death would materially hurt the company. The business is the beneficiary and uses the death benefit to absorb lost revenue, recruit a replacement, and reassure lenders and partners. Coverage is sized to the revenue and recruiting cost tied to that person.

How does life insurance fund a buy-sell agreement?

Life insurance funds a buy-sell agreement by providing the cash to buy out a deceased owner's share at a price the agreement sets in advance. When an owner dies, the death benefit funds the purchase, so surviving owners keep control and the family receives fair value without forcing a sale. The agreement should be revalued regularly so the price stays current.

What are the IRC 101(j) employer-owned life insurance rules?

IRC Section 101(j) requires that before a business issues a policy on an employee, it gives written notice, obtains written consent, and meets a stated exception. If those notice-and-consent steps are skipped, the death benefit above the premiums paid can become taxable income to the business. Complete the paperwork before the policy is issued.

Should a business owner own life insurance personally or through the business?

It depends on the job. Income replacement for the owner's family is usually a personally owned policy. Key person and buy-sell coverage is usually owned and paid by the business or the other owners. Who owns, pays, and benefits drives the tax result, so confirm each structure with a CPA and an attorney before applying.

What is cash value life insurance for a business?

Cash value life insurance is a permanent policy that accumulates a borrowable cash value alongside the death benefit. A business owner can use that cash value as a capital reserve, borrowing against it for opportunities while the policy continues to compound net of mortality and expense charges. Term insurance, by contrast, builds no cash value.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

How much life insurance does a business owner need?

The amount depends on the job. Key person coverage is sized to the revenue and recruiting cost tied to that person. Buy-sell coverage is sized to each owner's share at the agreed valuation. Personal income replacement is sized to the family's needs. Each job is calculated separately, then combined into a total.

Does the death benefit from a business life insurance policy get taxed?

A death benefit is generally received income-tax-free under IRC Section 101(a). The main exceptions are employer-owned policies that fail the IRC 101(j) notice-and-consent rules and certain transfer-for-value situations. Confirm your structure with a CPA so the proceeds stay tax-free.

- IRC Section 101 (Cornell Law), the income-tax-free treatment of death benefits, including the 101(j) employer-owned rules.

- IRC Section 264 (Cornell Law), the general bar on deducting premiums when the business is a beneficiary.

- IRS Form 8925, the employer-owned life insurance reporting form tied to the 101(j) rules.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- LIMRA, life insurance industry data, including business-owned and small-business coverage trends.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, many for business owners protecting and deploying capital. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on how to structure coverage for your business, book a discovery call. We will tell you if it does not fit.