.png)

Key person life insurance is a policy a business owns, pays for, and collects on as the beneficiary, covering an owner or employee the company cannot easily replace. If that person dies, the death benefit gives the business cash to absorb the disruption, recruit a successor, and reassure lenders and clients.

Most small and mid-sized companies are one funeral away from a cash crisis they never modeled. A single person often holds the relationships that drive revenue, the technical knowledge nobody documented, or the personal guarantee a lender relied on. When that person dies suddenly, the loss is not only human. It is financial, and it lands on the business in the same quarter the team is grieving.

Key person life insurance exists to convert that risk into a known, funded number instead of a hope that the business survives. The concept is simple. The business buys a life insurance policy on the person it cannot afford to lose, pays the premiums, and names itself as the beneficiary. If the insured dies, the company receives a death benefit it can use to keep the lights on while it rebuilds.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and key person coverage is one of the first questions we raise with an owner whose business depends heavily on one or two people. This guide covers what the coverage actually is, how to size it without guessing, who owns and benefits from the policy, and the tax treatment that trips up businesses who skipped a step before the policy was issued. We will also be honest about who does not need it.

- The business is the owner, premium payer, and beneficiary; the key person is the insured but holds no policy rights.

- Premiums are not tax deductible under IRC 264(a)(1), because the business is the beneficiary of the policy.

- The death benefit is income-tax-free only if the IRC 101(j) notice-and-consent rules were met before the policy was issued.

- Size coverage to the real financial loss, using a compensation multiple, profit contribution, or replacement-cost build-up.

- Term covers a defined risk window; permanent whole life builds cash value the business owns and can borrow against.

- Key person insurance protects the company; a buy-sell agreement transfers ownership. Many businesses need both.

01 / The problemWhat does a business actually lose when a key person dies?

A business loses revenue, knowledge, and credit standing all at once when a key person dies, and those losses arrive faster than a replacement can be hired. The salesperson who carried 40% of bookings takes their relationships with them. The founder who personally guaranteed the line of credit leaves the bank reassessing the loan. The lead engineer who never wrote anything down takes the product roadmap in their head.

None of this shows up on a balance sheet until it is too late. The company still owes payroll, rent, and debt service, but the engine that generated the cash to cover them has stalled. Key person insurance is the funded answer to a question every owner should ask once: if this person were gone next month, where would the money come from to survive the next year?

Most owners insure their building and their trucks without blinking, then leave the one person who drives the revenue completely uninsured. The asset most exposed to a single death is usually a person, not a thing.

02 / The frameworkWhat is key person life insurance, and how does it differ from personal coverage?

Key person life insurance is business-owned coverage on an individual whose death would cause the company a measurable financial loss. The difference from personal life insurance is ownership and purpose. A personal policy protects a family. A key person policy protects a business, and the business is the one that applies for it, pays for it, and receives the benefit.

The person insured, often called the key man or key employee, signs as the proposed insured and consents to the coverage, but owns none of it. They cannot name their spouse as beneficiary or borrow against it. The policy is a company asset, listed alongside the company's other assets, and the death benefit flows to the company to spend as it sees fit: bridging lost revenue, recruiting and training a successor, paying down debt the person guaranteed, or simply buying the team time to stabilize.

Where The And Asset fits a permanent key person policy

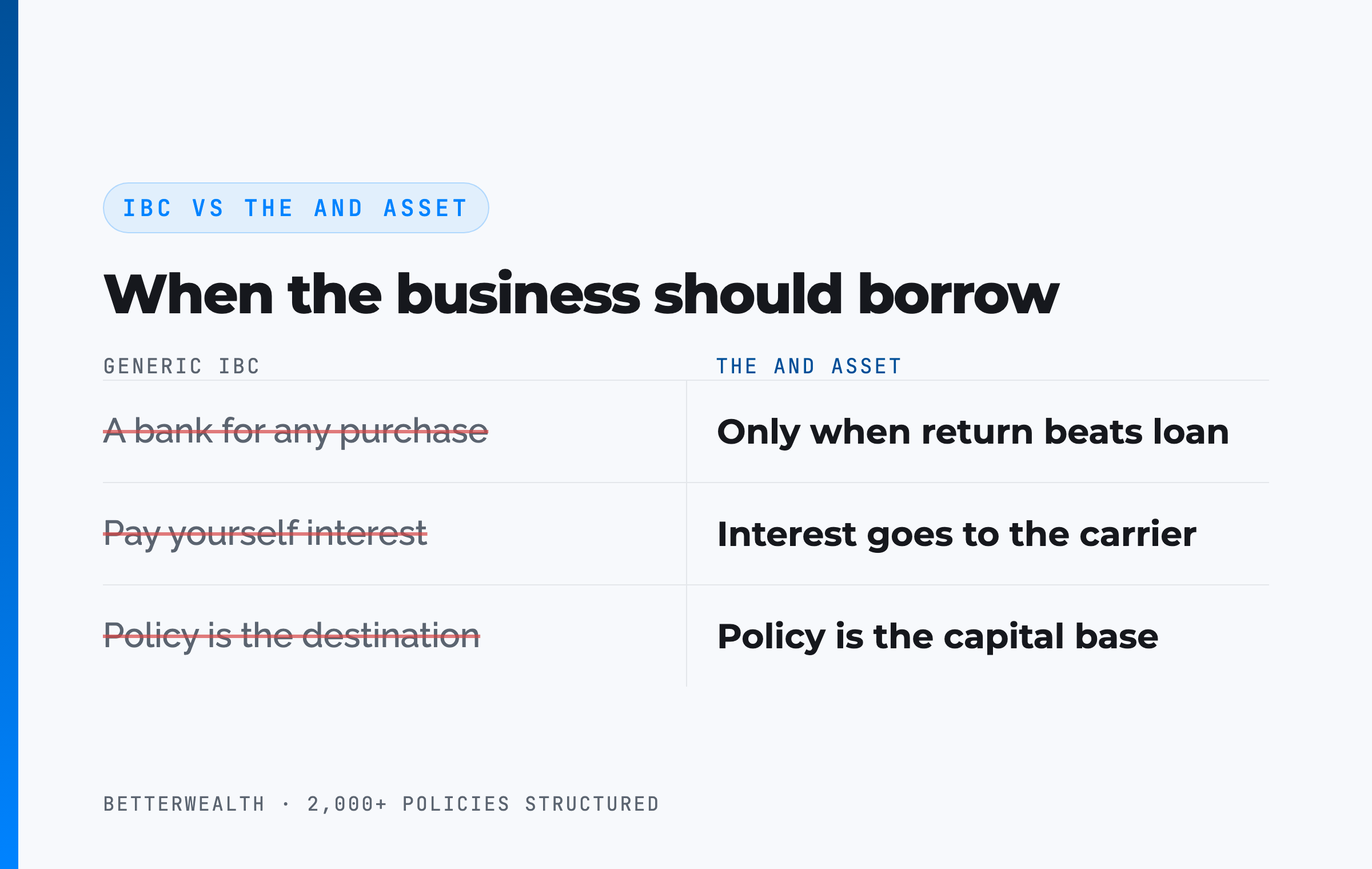

When a key person policy is written as permanent whole life rather than term, the business owns more than a death benefit. It owns a growing pool of cash value, and that is where The And Asset framework applies. Nelson Nash pioneered the idea of using whole life insurance as a private banking system in Becoming Your Own Banker. We credit that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

IBC says you can use a whole life policy as a banking system for any purchase. The And Asset says the business only borrows against the policy when the deployed capital produces a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The interest on a policy loan goes to the insurance company, not back to you, so your return has to come from what the borrowed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges. A key person policy can do two jobs at once: protect the company against a death, and serve as a capital base the company deploys with discipline.

The death benefit protects you. The cash value works for you.

03 / OwnershipWho owns, pays for, and benefits from the policy?

The business owns the policy, pays the premiums, and is named as the beneficiary, while the key person is only the insured. This three-part alignment is the defining feature of key person coverage, and getting it right is what keeps the structure clean for both legal and tax purposes.

- Applicant and owner: the business entity (LLC, S corp, C corp, or partnership). It controls the policy and reports it as a company asset.

- Premium payer: the business, using after-tax dollars, because the premiums are not deductible.

- Insured: the key person, who must consent in writing before the policy is issued.

- Beneficiary: the business, which receives the death benefit directly.

The insured's consent is not a formality. It is a legal requirement, and for employer-owned policies it is also a tax requirement under the rules covered below. An insurable interest must exist at the time the policy is issued, which a business clearly has in an owner or a high-impact employee. If that person later leaves the company, the business can usually keep the policy in force, but it should revisit whether the coverage still serves a purpose.

Key person coverage fits a specific kind of business.

It fits you if

- One or two people drive most of your revenue or financing

- Their sudden loss would threaten the company's survival

- You have lenders, investors, or clients who depend on that person

- You want the death benefit to fund a real recovery plan

It is less urgent if

- No single person is hard to replace

- Revenue is spread across a deep team

- The business could run for a year without any one person

- You are confusing it with a buy-sell or estate plan

If you are in the first column, a 30-minute conversation will tell you how much coverage you actually need and how to structure it. If you are in the second, we will tell you that too.

Book a Discovery Call04 / How it worksHow do you size a key person policy without guessing?

You size a key person policy to the financial loss the person's death would cause, not to a round number that feels safe. The goal is a defensible figure the carrier will underwrite and the business can justify. Here is the sequence we use, and the order matters.

- Identify the key person. Name the individual whose death would directly threaten revenue, financing, or operations. If losing them would barely register, they are not a key person for insurance purposes.

- Quantify the financial loss. Estimate lost profit during the transition period, the cost to recruit and ramp a replacement, and any loans or contracts that hinge on that person remaining. Be concrete. A number you can show a lender beats a number you pulled from the air.

- Choose a sizing method. The three common approaches are a multiple of the person's compensation (often in the range of five to ten times), a contribution-to-profits estimate (the share of profit attributable to that person over the years it would take to recover), and a replacement-cost build-up (recruiting, training, lost productivity, and bridge financing added together). Run more than one and reconcile them.

- Set ownership, payer, and beneficiary. The business is the applicant, owner, premium payer, and beneficiary. The key person is the insured and must give written consent before the policy is issued.

- Meet the notice-and-consent rules. Before issue, give the employee written notice that you intend to insure them and the maximum coverage amount, obtain their written consent, and confirm an exception under the employer-owned rules applies. File Form 8925 with the company return each year.

- Work with a professional. Have a qualified insurance professional and a tax advisor confirm the sizing, the ownership structure, and the consent paperwork before the policy is issued. The rules are unforgiving once the contract exists.

Underwriting will test your number against the person's income and the company's financials, so a sized-to-loss figure underwrites more smoothly than an inflated one. Reconciling two or three methods into a single amount is the practical work that separates a real policy from a guess.

Coverage is not a vanity number. It is the cash the business will actually need to survive a specific person's absence. Size it to the loss, document the math, and the carrier and your CFO will both thank you.

05 / The taxesHow is key person life insurance taxed?

Key person insurance has two tax facts that matter, and most of the confusion comes from people assuming it works the way personal coverage does. It does not. The premiums are not deductible, and the death benefit is income-tax-free only if the business cleared specific hurdles before the policy was issued.

Premiums are not deductible

Under IRC 264(a)(1), a business cannot deduct premiums on a life insurance policy when it is directly or indirectly a beneficiary of that policy. Because the company is the beneficiary of a key person policy, the premiums come out of after-tax dollars. Owners sometimes hope to write the premiums off as a business expense. They cannot, and an agent who implies otherwise is setting up a problem with the IRS. The tradeoff is on the other side: the death benefit can come in income-tax-free, which is where the value sits.

The death benefit and the IRC 101(j) trap

Life insurance death benefits are generally excluded from income under IRC 101(a). For employer-owned life insurance, IRC 101(j) adds a condition that is easy to miss and impossible to fix later. For policies issued after the rules took effect (employer-owned contracts issued after August 17, 2006, under the Pension Protection Act of 2006), the death benefit above the premiums the business paid is income-tax-free only if two things are true. First, before the policy was issued, the business gave the employee written notice of the coverage and the maximum amount, the employee gave written consent, and an exception applies (for example, the insured was an employee within 12 months of death, or was a director or highly compensated employee). Second, the business meets the annual reporting requirement on Form 8925.

Miss the notice-and-consent step before issue, and the death benefit that exceeds total premiums paid can become taxable income to the business. There is no retroactive cure. This is the single most common and most expensive mistake we see with business-owned coverage, and it is entirely avoidable with paperwork done in the right order. Tax rules change and apply differently by entity and situation, so confirm the specifics with a qualified tax advisor before you rely on any of this.

A key person death benefit is not automatically tax-free. It is tax-free if you did the consent paperwork before the policy was issued. The order is the whole game.

06 / Term or permanentShould key person insurance be term or whole life?

Term and permanent both work for key person coverage, and the right answer depends on how long the risk lasts and whether the business wants an asset or only protection. Term insurance covers a defined window, say 10 or 20 years, at the lowest premium, and builds no cash value. When the term ends, the coverage ends. For a risk that is genuinely temporary, like a founder's role through the payoff of a specific loan, term is efficient and honest.

Permanent whole life costs more per dollar of death benefit, but the business owns a cash value that grows over time, compounding net of mortality and expense charges. That cash value is a company asset the business can borrow against, which is where the policy stops being a pure expense and starts being part of the capital structure. A key person policy built this way carries protection and an And Asset in one contract.

The cash value is real but it is not instant. A well-designed policy does not see cash value exceed cumulative premiums until around year four at the earliest, with break-even for a healthy insured typically landing at year five or later. Any illustration that shows cash beating contributions in year one or two is fiction. If the business needs the protection to function as a long-term, borrowable asset, permanent makes sense. If it needs cheap coverage for a known, finite risk, term does the job.

Term rents the protection. Permanent owns the asset.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we set up business-owned policies, size coverage, and decide between term and permanent. Free, email-gated, no spam.

Open the Vault07 / Where it fitsHow key person coverage fits a broader business protection plan

Key person insurance is one piece of a business protection plan, and it is frequently confused with two other tools that solve different problems. Sorting them out prevents both over-insuring and dangerous gaps.

The first distinction is succession. Key person insurance protects the business from the loss of a critical person. When the topic shifts to who takes over an owner's stake, you are in different territory: funding a buy-sell agreement with life insurance is how co-owners guarantee the money exists to buy out a deceased owner's shares from their estate. A buy-sell policy and a key person policy can both insure the same founder, but they have different owners, different beneficiaries, and different purposes. One keeps the company solvent. The other keeps ownership orderly.

The second distinction is scope. Key person coverage sits inside the larger question of how an owner protects the enterprise, their family, and their own balance sheet at the same time. For the full picture of how these policies work together, see our guide to life insurance for business owners, which maps key person, buy-sell, and personal coverage into a single plan. The point is to install each tool for the job it actually does, rather than buying one product and hoping it covers everything.

08 / The tradeoffsThe real benefits and honest limits of key person insurance

Key person insurance delivers a funded recovery plan, but it comes with limits worth naming before you buy. Pretending it has no downsides is how agents lose trust.

The benefits are concrete. The death benefit arrives income-tax-free when the rules are met, gives the business immediate liquidity at the worst possible moment, and signals stability to lenders and clients who might otherwise panic. A permanent policy adds a cash value asset the business controls. The protection is also flexible: the company decides how to spend the proceeds, with no strings attached.

The limits are equally real. Premiums are not deductible, so the coverage is a true after-tax cost. Permanent policies carry meaningful premiums and lower early cash value, so they reward patience, not a need for quick liquidity. The 101(j) paperwork must be perfect before issue, or the tax treatment is at risk. And no policy replaces the person. It buys time and money to rebuild, which is valuable, but it does not restore the relationships or knowledge that walked out the door. Sized and structured well, those tradeoffs are acceptable. Ignored, they turn a protection plan into a liability.

It funds the recovery. It does not erase the loss.

09 / Head to headKey person insurance against the alternatives

Compared to the other ways a business can prepare for losing a critical person, key person insurance trades a non-deductible premium for guaranteed, income-tax-free liquidity exactly when it is needed. The table sets it against self-funding a reserve, a buy-sell agreement, and going uninsured, on the dimensions that matter when the worst happens.

| Dimension | Key Person Insurance | Self-Funded Reserve | Buy-Sell Agreement | No Coverage |

|---|---|---|---|---|

| What it solves | Replaces lost profit and funds recovery after a key death | Same goal, but only if the reserve is already large enough | Funds transfer of a deceased owner's shares, not operating loss | Nothing; the loss hits cash flow directly |

| Funding at death | Full death benefit, available immediately | Limited to whatever has been saved so far | Death benefit earmarked for the buyout, not operations | None |

| Tax treatment | Premiums non-deductible; benefit income-tax-free if 101(j) met | Reserve built with after-tax dollars, earnings taxed yearly | Premiums non-deductible; benefit funds share purchase | No premium, but full financial exposure |

| Asset value before death | Permanent design builds borrowable cash value the business owns | Liquid, but drags as idle cash and is exposed to the business | Cash value possible, but committed to the buyout purpose | None |

What it solves. Key person insurance and a self-funded reserve aim at the same target, but the reserve only works if it is already big enough on the day it is needed. Insurance delivers the full amount from day one of the policy, which is the entire point of insuring a risk you cannot self-fund yet.

Buy-sell is not a substitute. A buy-sell agreement solves ownership succession, not operating loss. Its death benefit is committed to buying out an owner's shares. A company can need both a key person policy and a buy-sell on the same founder, because they pay for different problems.

The asset angle. A permanent key person policy builds cash value the business owns and can borrow against under The And Asset discipline, only when the deployed return clears the loan cost. A reserve sits idle, and going uninsured leaves the full loss on the table.

A composite: the manufacturer who insured its co-founder

Consider a 12-person specialty manufacturer whose co-founder and head of engineering, age 44 and a preferred non-tobacco risk, drives product development and personally guaranteed the company's equipment line of credit. This is a representative composite for illustration, not a single named client, and the figures are illustrative rather than a quote.

The business sized coverage at $2,700,000 by reconciling three methods: roughly six times the co-founder's compensation, an estimate of profit attributable to her over a three-year recovery window, and a replacement-cost build-up that included the lender's exposure on the guaranteed line. The company applied as owner and beneficiary, the co-founder consented in writing before issue, and the business filed Form 8925 each year, keeping the death benefit income-tax-free under IRC 101(j).

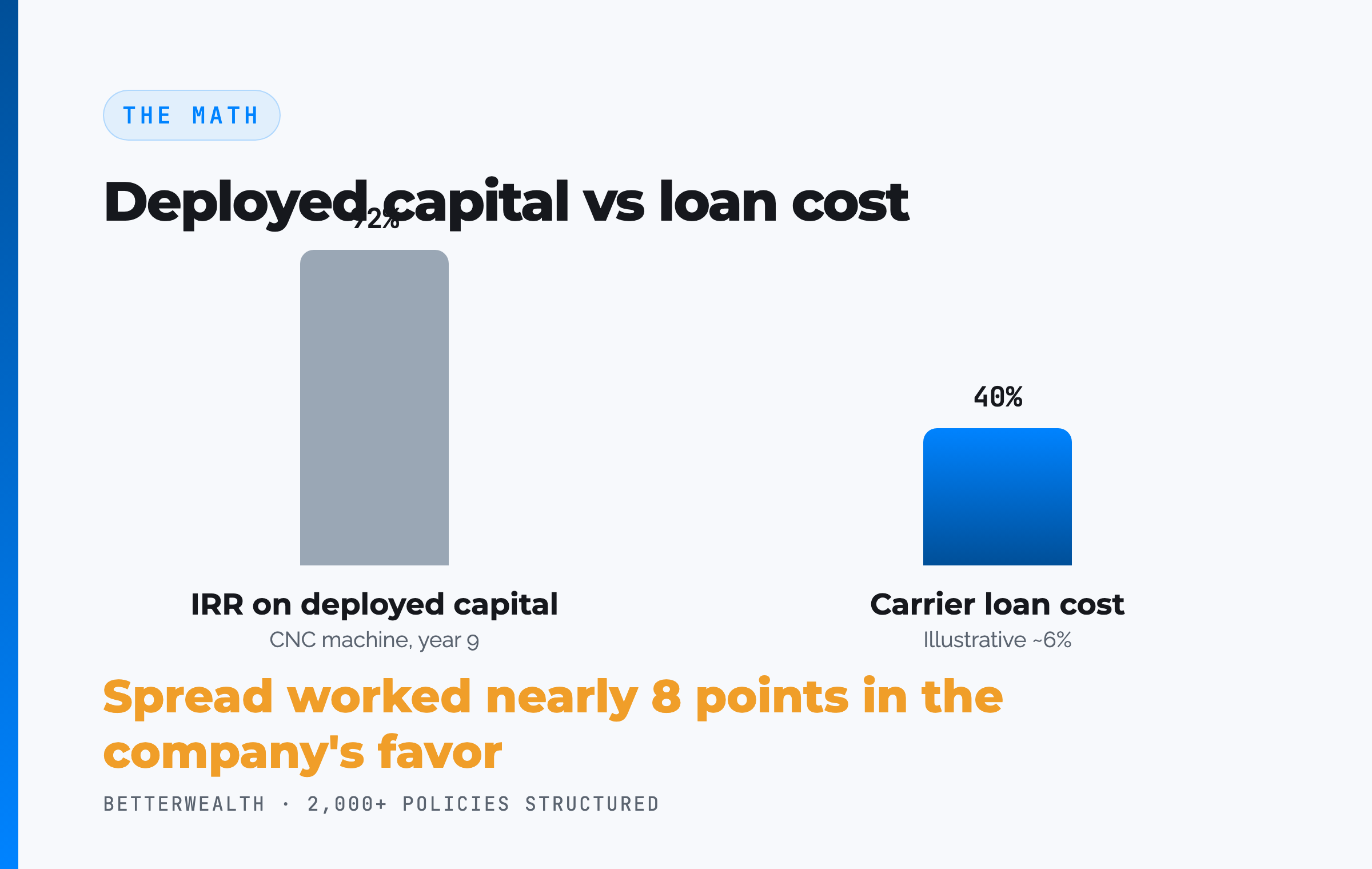

They structured it as overfunded whole life at $47,000 per year so the policy would protect the company and build an asset. Year-one cash value landed near $33,800, below the $47,000 contributed, exactly as a real policy behaves. Through the early years cash value trailed cumulative premiums. Break-even arrived at year six. No earlier.

In year nine, with accessible cash value built up, the business borrowed $128,500 against the policy to buy a revenue-producing CNC machine. The machine returned an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread worked in the company's favor by nearly eight points, and the policy kept compounding on its full value the entire time. Repayment ran on a 44-month schedule funded by the machine's own output. The death benefit stayed in place the whole time, ready if the co-founder were lost.

One contract. Protection and capital. That is the And.

The honest 30 minutes about whether your business needs this.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at how dependent your business is on one or two people, helps you size coverage to the real loss, and makes sure the ownership and consent paperwork is done in the right order. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the strategy.

Book a Discovery CallFAQKey person life insurance questions

What is key person life insurance?

Key person life insurance is a policy a business owns, pays for, and collects on as the beneficiary, covering an owner or employee the company cannot easily replace. If that person dies, the death benefit gives the business cash to absorb the disruption, recruit a successor, and reassure lenders and clients.

Who owns and pays for a key person policy?

The business is the applicant, owner, premium payer, and beneficiary. The employee or owner is the insured, but holds no ownership in the policy. The insured must give written consent before the policy is issued under IRC 101(j).

Are key person life insurance premiums tax deductible?

No. Premiums on key person life insurance are not deductible. IRC 264(a)(1) denies a deduction for premiums on any life insurance policy where the business is directly or indirectly a beneficiary. The business pays premiums with after-tax dollars.

Is the key person death benefit taxable?

The death benefit is generally income-tax-free under IRC 101(a), but for employer-owned policies it is income-tax-free only if the IRC 101(j) notice-and-consent requirements were met before the policy was issued and an exception applies. Miss those steps and the benefit above premiums paid can become taxable. Verify with a tax advisor.

What are the IRC 101(j) notice and consent requirements?

Before an employer-owned policy is issued, the business must notify the employee in writing that it intends to insure them and the maximum amount, obtain the employee's written consent, and confirm an exception applies. The business also files Form 8925 with its return each year. These steps cannot be fixed after issue.

How much key person coverage does a business need?

Coverage is sized to the financial loss the person's death would cause, not a round number. Common methods are a multiple of compensation, a contribution-to-profits estimate, or a replacement-cost build-up covering lost profit, recruiting, and any loans tied to that person. Reconcile the methods into one figure with a professional.

Should key person insurance be term or permanent?

Term covers a defined risk window at the lowest premium and builds no cash value. Permanent whole life costs more but the business owns a growing cash value asset it can borrow against, so the policy doubles as a capital base. The right choice depends on how long the risk lasts and whether the business wants an asset or only protection.

Is key person insurance the same as a buy-sell agreement?

No. Key person insurance protects the business from the financial loss of losing a critical person. A buy-sell agreement funds the transfer of ownership when an owner dies or exits. A company often needs both, and they are structured differently with different owners and beneficiaries.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Do you need the employee's permission to take out key person insurance?

Yes. The insured must give written consent before the policy is issued. For employer-owned policies, IRC 101(j) requires written notice and written consent before issue, and consent does not transfer if the person later leaves. Insuring someone without consent can forfeit the income-tax-free treatment of the death benefit.

- IRC Section 264 (Cornell Law), the provision that denies a deduction for premiums where the business is a beneficiary.

- IRC Section 101 (Cornell Law), the exclusion of death benefits from income, including the 101(j) employer-owned rules.

- IRS Form 8925, the annual report of employer-owned life insurance contracts.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- LIMRA, life insurance industry data and business-coverage research.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, including business-owned coverage for owners and key employees. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether your business needs key person coverage and how to size it, book a discovery call. We will tell you if it does not.