.png)

Buy-sell agreement life insurance funds the purchase of a deceased owner's share, paying surviving owners or the business an income-tax-free death benefit to complete the buyout at the agreed price. The attorney-drafted agreement and the CPA-set valuation control the terms. The insurance only supplies the cash.

Most partnership agreements are written for the day everyone is alive and getting along. The harder day, the one that actually tests the structure, is the morning after a co-owner dies. On that morning the surviving owners face a problem with no good improvised answer: they either buy the deceased owner's share from an estate that wants top dollar, or they accept a new business partner who never built anything and now owns a third of the company.

A buy-sell agreement decides that outcome in advance, and life insurance is what makes the decision affordable. The agreement is the legal machinery. It says who buys, who sells, at what price, and on what trigger. The life insurance is the funding mechanism that hands the buyer the exact dollars needed, at the exact moment they are needed, free of income tax under the Internal Revenue Code.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and a meaningful share of them sit underneath buy-sell agreements for closely held businesses. Before you go further, ground yourself in the broader picture with our guide to life insurance for business owners, because a buy-sell is one specific job inside a larger set of reasons a company carries coverage. This piece covers what a buy-sell funded with life insurance actually does, the two core structures (cross-purchase and entity-purchase), who owns the policies in each, the basis and valuation traps that quietly cost owners money, and where The And Asset framework changes the conversation for an owner who wants the policy to do more than sit there.

- A buy-sell agreement is a legal contract; life insurance funds it. The insurance does not replace the documents an attorney and CPA must draft.

- Cross-purchase means each owner insures the others. Entity-purchase means the business owns the policies and redeems the deceased owner's share.

- Cross-purchase generally gives surviving owners a step-up in cost basis. Entity-purchase usually does not, which can cost them at a future sale.

- Death benefits are generally income-tax-free under IRC Section 101, which is why insurance beats cash reserves or a bank loan for funding a buyout.

- The transfer-for-value rule can make a death benefit taxable if a policy is moved carelessly between owners or the entity.

- A permanent policy can fund the buyout and build a capital base the business can borrow against, which is where The And Asset applies.

01 / The problemWhat happens to a business when an owner dies without a funded plan

Without a funded buy-sell, the death of an owner forces a fire sale or a forced partnership, and both outcomes destroy value. The deceased owner's shares pass to their estate, which usually means a spouse or children who have a legal claim to a third or a half of the company and no role in running it. The surviving owners now negotiate a buyout with grieving heirs who, understandably, want the highest possible price. Nobody is thinking clearly. The business throws off less cash because a key person is gone. The worst possible moment to find a few hundred thousand dollars is the moment the plan demands it.

The alternatives to insurance all carry a cost. A cash reserve large enough to buy out a partner is capital sitting idle for years, dragging on returns. A bank loan adds interest and requires a lender to say yes during a crisis. An installment buyout stretches payments to the estate over years, which keeps the family financially entangled with the business long after anyone wanted that. Life insurance solves the funding problem in one stroke: a defined sum, delivered tax-free, on the day it is needed.

The buy-sell agreement is not the hard part. Lawyers draft those every day. The part that fails is funding. An unfunded agreement is a promise to find money you do not have, on the worst day to find it.

02 / The mechanicsHow does life insurance fund a buy-sell agreement?

Life insurance funds a buy-sell agreement by delivering a death benefit that matches the price of the deceased owner's share, so the buyer can complete the purchase immediately and in cash. The sequence is simple once the structure is set. An owner dies. The policy pays out. The buyer (either the surviving owners or the business) uses that death benefit to pay the agreed price to the estate. The estate hands over the shares. The surviving owners keep full control of a company they no longer share with an outside heir.

The reason this works so cleanly is the tax treatment. Under IRC Section 101(a), death benefits are generally received income-tax-free. The buyer gets full purchase-price dollars without first earning a larger pre-tax sum to net down to the number. A dollar of death benefit is a dollar of buying power. A dollar of business profit earmarked for a buyout is worth far less after tax.

One distinction worth fixing in your mind: the insurance does not set the price, the trigger, or the terms. The legally binding agreement does, and it has to be drafted by an attorney. The valuation has to be set with a CPA or qualified appraiser. The policy is the checkbook, not the contract.

The agreement decides. The policy pays.

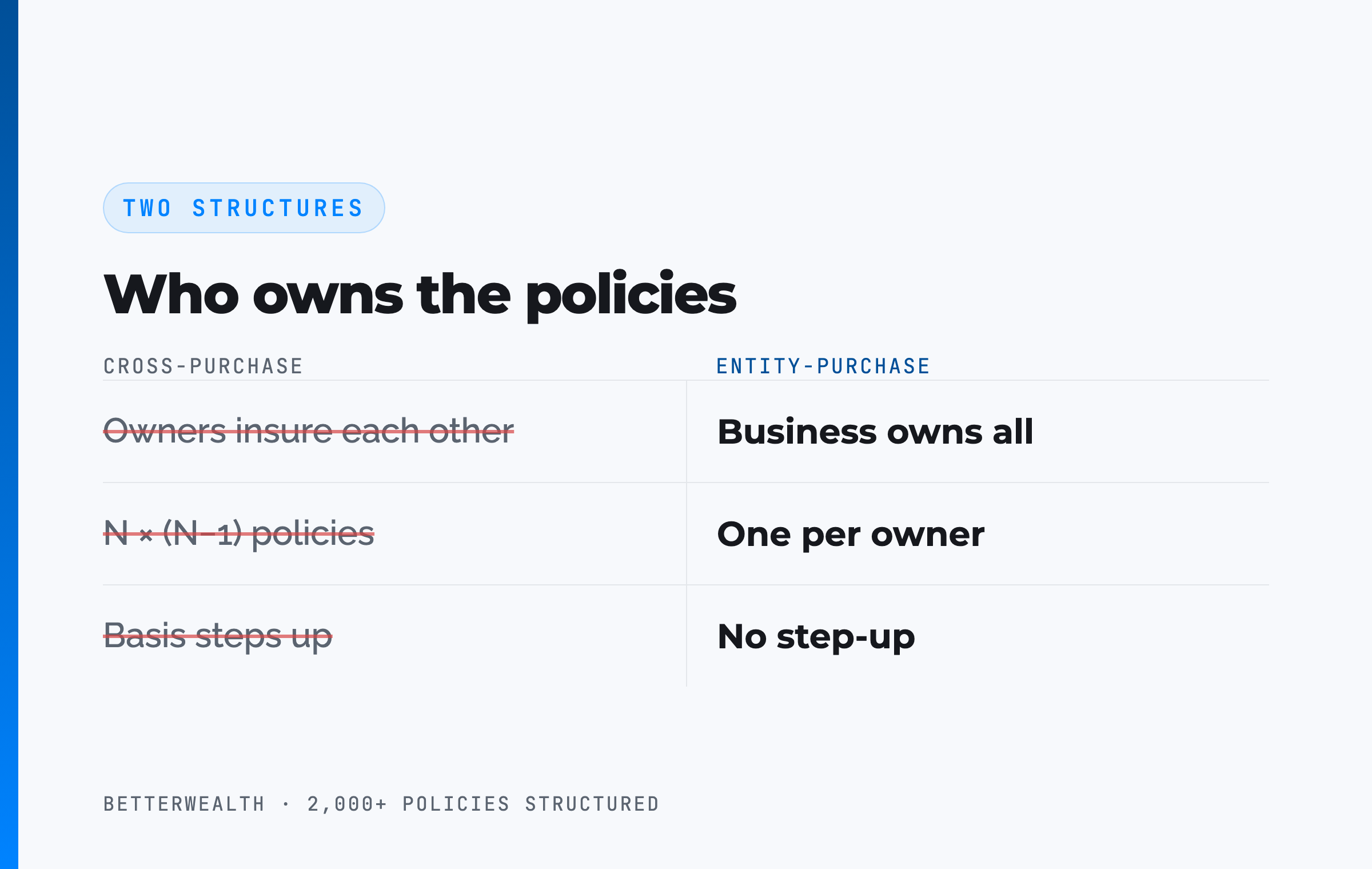

03 / The structuresCross-purchase vs entity-purchase: who owns the policies?

The two structures differ in one fundamental way: who owns the life insurance and who completes the buyout. That single choice drives the number of policies, the cost basis outcome, and the administrative complexity. Get this decision right with your attorney and CPA before any policy is issued, because unwinding it later can trigger taxes.

Cross-purchase: owners insure each other

In a cross-purchase agreement, each owner personally buys and owns a policy on every other owner. If owner A dies, owners B and C each collect a death benefit and use it to buy A's share directly from A's estate. The shares move from the estate to the surviving owners as individuals.

The advantage that matters most over time is cost basis. Because the surviving owners personally paid for the additional shares, their cost basis in the company steps up by the amount they paid. When they eventually sell the business, that higher basis means a smaller taxable gain. The disadvantage is policy count. With three owners you already need six policies, because each owner insures two others. Add a fourth owner and you are at twelve. Premiums also differ by age and health, so a younger owner can end up paying more to insure an older partner than the reverse, which feels lopsided.

Entity-purchase: the business owns the policies

In an entity-purchase agreement, sometimes called a stock redemption, the business itself owns a policy on each owner and is the beneficiary. When an owner dies, the company collects the death benefit and redeems (buys back) the deceased owner's share. The surviving owners end up owning a larger percentage of the company without personally writing a check.

The advantages are simplicity and equity. One policy per owner instead of a web of them. Premiums are paid by the business, spreading the cost evenly rather than penalizing younger owners. The cost is the basis outcome. In a C corporation redemption, the surviving owners generally do not get a step-up in their personal cost basis, because the entity bought the shares, not them. That can mean a larger taxable gain when the business is sold years later. Pass-through entities such as S corporations and partnerships have their own basis nuances that a CPA needs to map for your specific situation.

Owners pick entity-purchase because it has fewer policies, then sell the company a decade later and discover the basis they gave up cost them more in capital gains tax than every premium they ever saved.

04 / Head to headCross-purchase, entity-purchase, and going unfunded

Compared side by side, the structures trade administrative simplicity against tax efficiency, and going unfunded trades a premium you can budget for a crisis you cannot. The table sets the two funded structures against the unfunded default on the dimensions that actually decide the outcome.

| Dimension | Cross-Purchase | Entity-Purchase | Unfunded |

|---|---|---|---|

| Who owns the policies | Each owner owns a policy on every other owner | The business owns one policy per owner | No policies; buyout comes from cash, a loan, or installments |

| Number of policies | N × (N−1): grows fast as owners are added | One per owner: simplest to administer | None |

| Cost basis to survivors | Step-up: survivors' basis rises by what they paid | Generally no step-up in a C-corp redemption | No transaction structure; basis treatment uncertain |

| Best fit | 2 to 3 owners who want the basis advantage | More owners, or owners who want even cost and simple admin | Nobody plans for this; it is the default when no one acts |

Who owns the policies. This is the line that defines everything else. Cross-purchase keeps ownership and the buyout in the hands of the individuals. Entity-purchase centralizes both in the company. The right answer depends on owner count, the entity type, and what the basis outcome is worth to you at a future sale.

Number of policies. Two owners are easy either way. At three owners, cross-purchase already means six policies, and the math gets unwieldy from there. Owners with four or more partners often move to entity-purchase or a hybrid for administrative sanity, then solve the basis problem another way with their CPA.

The unfunded column. This is not really a strategy. It is what happens when owners keep meaning to set this up and never do. The buyout still has to happen. It just happens with borrowed money, depleted reserves, or a multi-year payout that keeps a grieving family financially tied to the business.

05 / How to set it upHow do you fund a buy-sell agreement with life insurance, step by step?

You fund a buy-sell with life insurance through five steps, and the order protects you from the tax traps. Skipping the legal and valuation work and going straight to buying policies is the most common, and most expensive, mistake.

- Set the business value. Have a CPA or qualified appraiser establish a value, or a written formula the owners agree to and revisit on a set schedule. A stale value is the reason a buyout funds 60% of what the share is actually worth. The valuation method belongs in the agreement.

- Have an attorney draft the agreement. The buy-sell is a legally binding contract. An attorney defines the triggering events (death first, often disability and departure too), the price or formula, and which funding structure applies. The insurance funds this document. It does not replace it.

- Choose the structure. Decide between cross-purchase and entity-purchase with your attorney and CPA, weighing owner count, entity type, and the basis outcome. This decision determines who applies for and owns the policies.

- Place the policies correctly. Apply for coverage with the correct owner and beneficiary for the chosen structure. Ownership errors, or later transfers of existing policies into the structure, can trip the transfer-for-value rule and make the death benefit taxable. Confirm placement with a tax advisor before the policies are issued.

- Fund, maintain, and coordinate. Keep premiums current, revisit the valuation as the business grows, and make sure the death benefit keeps pace with the rising value of each owner's share. A policy sized to a $2M business does not fund a buyout when the company is later worth $5M.

That last point is the one owners forget. The business grows. The buy-sell price grows with it. The death benefit has to grow too, or you have a partially funded agreement and a gap that surviving owners cover out of pocket.

Value first. Documents second. Policies last.

A funded buy-sell fits a specific kind of business.

It fits you if

- You co-own a business with one or more partners

- You want to keep control if a co-owner dies

- You would rather budget a premium than improvise a buyout

- The business has real, growing value to protect

It may not fit you if

- You are the sole owner with no co-owners to buy out

- You have no documented value or valuation method yet

- You want insurance to replace the legal documents

- The business is pre-revenue with nothing to transfer

If you are in the first column, a 30-minute conversation will map which structure and how much coverage your situation calls for. If you are in the second, we will tell you that honestly too.

Book a Discovery Call06 / The tax trapsThe transfer-for-value rule and the valuation problem

Two tax issues quietly undo buy-sell plans that looked fine on paper, and both are avoidable with the right advisor in the room. The first is the transfer-for-value rule. The second is a sloppy or stale valuation.

The transfer-for-value rule

The transfer-for-value rule lives in IRC Section 101(a)(2), and it can turn a tax-free death benefit into taxable income. The general rule is that if a life insurance policy is transferred for valuable consideration, the death benefit above the buyer's cost can become taxable. This becomes a live risk when a business switches from entity-purchase to cross-purchase and moves existing policies among owners, or when owners trade policies to simplify a structure. There are safe-harbor exceptions, including transfers to the insured and certain transfers among partners, but they are specific. Do not move a policy inside a buy-sell structure without a tax advisor confirming the transfer qualifies for an exception.

The valuation problem

A buy-sell is only as good as the number written into it. If the agreement names a value the owners set five years ago and never updated, the buyout funds an outdated figure and the estate gets shortchanged or the survivors overpay. Worse, for family businesses, IRC Section 2703 says a buy-sell price among family members has to reflect arm's-length terms to control the estate tax value. A price the IRS views as artificial can be ignored for estate tax, which defeats part of the planning. The fix is a documented valuation method, set with a CPA, and revisited on a schedule the agreement specifies.

The death benefit is tax-free until someone moves a policy the wrong way and makes it taxable. The transfer-for-value rule has wrecked more buy-sell plans than any market downturn ever has.

07 / The frameworkWhere The And Asset changes the buy-sell conversation

The And Asset changes the conversation by asking the policy to do two jobs instead of one. A buy-sell can be funded with term insurance, which is pure death-benefit coverage for a defined period at the lowest premium. For many owners, that is the right call, and we say so. If the only goal is covering the buyout risk for a set number of years, term does it cheaply.

But term expires, and it builds nothing along the way. An owner with a long horizon, who plans to hold the business for decades and wants capital working the whole time, is leaving something on the table. This is where a properly structured whole life policy enters, and where The And Asset framework applies. The same policy that funds the buyout also accumulates cash value the business or the owner can borrow against, net of mortality and expense charges, while the death benefit stays in force permanently.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

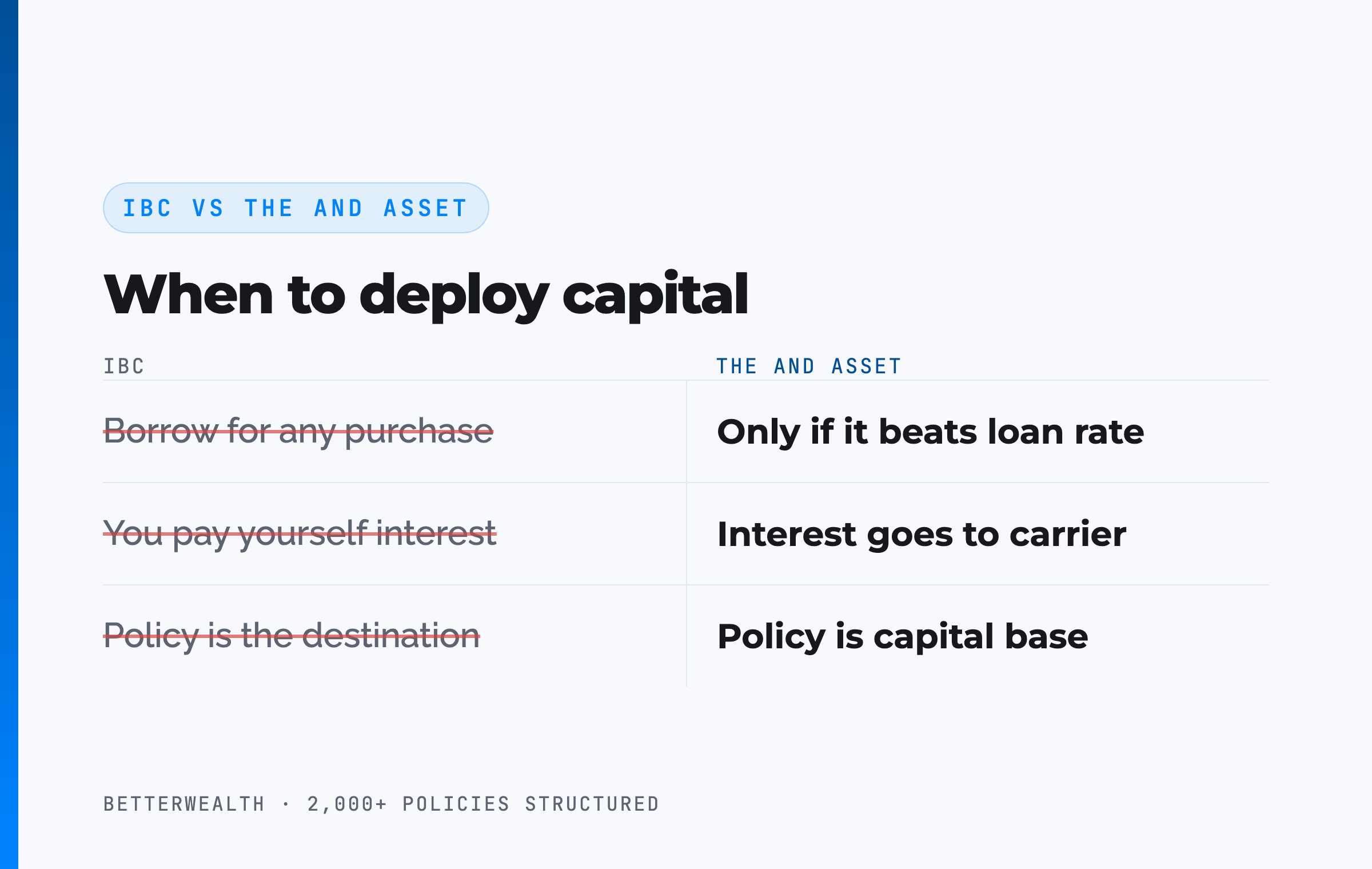

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding. In a buy-sell context, that means the cash value inside a funding policy is not a piggy bank for the company's payroll gaps. It is a capital base the business borrows against only when the deal beats the loan rate.

If the deal does not clear the loan rate, do not borrow.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use when we structure buy-sell funding, compare cross-purchase against entity-purchase, and size a policy to a growing business. Free, email-gated, no spam.

Open the Vault08 / The distinctionBuy-sell insurance vs key person insurance: which problem are you solving?

Buy-sell insurance and key person insurance both use life insurance on a business owner, but they solve opposite problems, and conflating them leaves a gap. A buy-sell transfers ownership: it funds the purchase of a deceased owner's share so control stays with the survivors. Key person insurance protects the business itself against the economic loss of a vital person, replacing lost revenue and giving the company time to recover or recruit.

The simplest way to keep them straight is to ask what the death benefit is for. If it pays the estate to buy out a share, that is a buy-sell. If it pays the business to absorb the hit of losing a rainmaker, that is key person. Many companies carry both, on the same person, because losing an owner-operator triggers both problems at once. We break the protection side down in our guide to key person life insurance and how it works, and the two strategies are designed to sit side by side, not compete.

A buy-sell keeps the wrong person from owning your company. Key person keeps the company alive long enough to replace the right person. They are not interchangeable, and a business that needs one usually needs both.

09 / The mathDoes a permanent policy beat term for funding a buyout?

A permanent policy beats term only when the owner has a use for the cash value that clears the carrier's loan cost, and not otherwise. This is the same discipline that governs every And Asset decision. Term funds the death-benefit obligation at the lowest premium and is the correct tool when covering the buyout risk for a defined window is the entire goal.

The case for permanent is the dual function. The policy funds the buyout and builds a capital base. But the second job only creates value if the business actually deploys the cash value into something that out-earns the loan cost. Borrow at the carrier's loan rate, deploy into an expansion or an acquisition returning more than that rate, and the spread works in the owner's favor while the policy keeps compounding on its full value. Borrow to cover a slow month with no return on the other side, and you have added cost for nothing. The math is the filter. If a business cannot identify a use for borrowed capital that beats the loan rate, the cash value should stay put, and term may be the better-fit funding tool.

A composite: three partners who funded the buyout and built a capital base

Consider three equal partners in a specialty contracting firm, ages 44, 47, and 51, with the business valued at $3,720,000, so each share is worth roughly $1,240,000. They use a cross-purchase agreement, drafted by their attorney, with the value set by their CPA and revisited every two years. Each partner funds permanent whole life policies on the other two. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative premiums, exactly as a healthy policy should. By year four, each premium dollar starts adding more than a dollar of cash value. At year six, combined cash value crosses total premiums paid. No earlier. Any illustration showing a year-two break-even is marketing fiction.

In year nine, the oldest partner borrows $214,000 against his accumulated cash value to fund a shop expansion the firm had been deferring. The expansion returns an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread runs almost eight points in the firm's favor. The policy keeps compounding on its full value the entire time, and the buy-sell death benefit stays fully in force. Repayment runs on a 47-month schedule funded by the expansion's own margin. The same dollars that protect the ownership transfer also financed real growth.

One dollar. Two jobs. That is the And.

The honest 30 minutes about funding your buyout.

We have structured more than 2,000 policies across all 50 states, many of them underneath buy-sell agreements. On a discovery call, a practitioner looks at your ownership structure and tells you which funding approach fits, how much coverage your buyout actually needs, and whether term or permanent is the right tool. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQBuy-sell agreement life insurance questions

How does life insurance fund a buy-sell agreement?

Life insurance funds a buy-sell agreement by paying a death benefit when an owner dies, giving the surviving owners or the business the cash to buy the deceased owner's share at the price set in the agreement. Death benefits are generally received income-tax-free under IRC Section 101, so the buyout happens with tax-free dollars instead of a bank loan or a cash reserve.

What is the difference between a cross-purchase and an entity-purchase buy-sell?

In a cross-purchase agreement, each owner buys a life insurance policy on every other owner and uses the death benefit to buy the deceased owner's share directly. In an entity-purchase (stock redemption) agreement, the business itself owns the policies and redeems the deceased owner's share. Cross-purchase generally gives surviving owners a step-up in cost basis; entity-purchase usually does not.

Who owns the life insurance policies in a buy-sell agreement?

In a cross-purchase agreement, the individual owners own policies on one another. In an entity-purchase agreement, the business owns the policies on each owner and is the beneficiary. Placing ownership incorrectly can trigger the transfer-for-value rule, so the structure should be set with an attorney and a CPA before policies are issued.

Does the death benefit from a buy-sell policy get taxed?

Life insurance death benefits are generally received income-tax-free under IRC Section 101(a). The main exception is the transfer-for-value rule under Section 101(a)(2): if a policy is transferred for valuable consideration without meeting an exception, part of the death benefit can become taxable. This is a common risk when switching buy-sell structures, so coordinate any transfer with a tax advisor.

How many life insurance policies does a buy-sell agreement need?

An entity-purchase agreement needs one policy per owner because the business owns all of them. A cross-purchase agreement needs each owner to insure every other owner, which is N times (N minus 1) policies. Two owners need two policies, three owners need six, and four owners need twelve, which is why cross-purchase gets unwieldy as the owner count grows.

Should a buy-sell agreement use term or permanent life insurance?

Term insurance funds the death-benefit obligation cheaply for a defined period and fits owners who only need to cover the buyout risk. Permanent whole life costs more but builds cash value the business or owners can access, and it does not expire before a long-horizon owner exits. Many owners blend the two: term for the bulk of the obligation and permanent for the portion they want to double as a capital base.

Who sets the value used in a buy-sell agreement?

The owners set the value with a CPA or qualified appraiser, usually as a fixed price or an agreed formula written into the agreement and revisited on a schedule. The value matters for both the buyout and estate tax purposes. Under IRC Section 2703, a buy-sell price among family members must reflect arm's-length terms to control the estate tax value, so the valuation method should be documented and defensible.

Can a buy-sell agreement work without life insurance?

Yes, but the alternatives are weaker. Without insurance, surviving owners fund a buyout from cash reserves, a bank loan, or installment payments to the deceased owner's estate. Each ties up capital, adds interest cost, or stretches the payout over years. Life insurance delivers the full purchase price in tax-free dollars at the exact moment it is needed.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. In a buy-sell context, a permanent policy can fund the buyout and build a capital base at the same time.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is a buy-sell agreement the same as key person insurance?

No. A buy-sell agreement transfers ownership when an owner dies or leaves, funding the purchase of their share. Key person insurance protects the business against the economic loss of a vital employee or owner, replacing lost revenue and buying time to recover. They solve different problems, and many businesses carry both.

- IRC Section 101 (Cornell Law), the tax treatment of life insurance death benefits, including the transfer-for-value rule at 101(a)(2).

- IRC Section 2703 (Cornell Law), the rules governing whether a buy-sell price controls the estate tax value of a business interest.

- IRS Publication 525, taxable and nontaxable income, including the general income-tax-free treatment of life insurance proceeds.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- LIMRA, life insurance industry data and research.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, including the coverage that funds buy-sell agreements for closely held businesses. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you co-own a business and want an honest read on how to fund your buyout, book a discovery call. We will tell you if term, permanent, or no policy at all is the right answer.