.png)

Cash value life insurance for business owners is an overfunded whole life policy used as a business asset: a liquid reserve, opportunity capital to borrow against for deals, and a tax-advantaged place to store retained earnings. Cash value grows tax-deferred, and a properly structured policy loan is not taxable income.

Most profitable businesses carry more idle cash than their owners admit. Retained earnings pile up in an operating account or a low-yield sweep, doing almost nothing, because the alternative is locking the money somewhere it cannot be reached when a deal or a payroll crunch arrives. That tension defines the cash question for every business owner: too much sitting idle is a drag on return, and too little is a missed opportunity or a liquidity scare.

For a business with surplus cash and a long horizon, a properly structured cash value life insurance policy turns idle retained earnings into a reserve that keeps compounding and stays accessible. The cash value grows tax-deferred. You can borrow against it without unwinding the asset. And the policy puts a death benefit on the life of the owner or a key person at the same time, which matters for continuity and buy-sell planning.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and a meaningful share of them sit behind a business owner who got tired of watching capital do one job at a time. This piece covers what the strategy actually is, how the policy functions as a business asset step by step, the math that decides whether borrowing against it makes sense, the corporate-ownership rules under IRC Section 101(j), the tax treatment, and the honest tradeoffs. We will also name who this is wrong for.

- Business owners use a cash value policy three ways: a liquid reserve, opportunity capital to borrow against, and a tax-advantaged store for retained earnings.

- Cash value grows tax-deferred, and a properly structured policy loan against a non-MEC policy is not taxable income.

- The And Asset rule governs every loan: only borrow when the deployed return clears the carrier's loan cost.

- If the business owns a policy on an owner or key employee, IRC Section 101(j) notice-and-consent must be met before issue.

- Cash value does not exceed cumulative contributions before year 4, with break-even at year 5 or later for healthy insureds.

- This fits a business with surplus capital and a long horizon, not one short on operating cash or carrying high-interest debt.

01 / The problemWhat idle retained earnings actually cost a business

Idle retained earnings cost a business the return that capital could be earning somewhere else, every quarter it sits still. That is lost opportunity cost, and it is invisible because nothing shows up on the income statement. A six-figure cash buffer earning a low sweep rate feels safe, but it is quietly losing ground to inflation and to the deals the owner passes on because the money is "the reserve."

The instinct most owners reach for is a line of credit. A business line or a HELOC promises access without parking capital, but access is conditional. Lines get reduced, frozen, or repriced exactly when the economy turns, which is exactly when an owner needs them. Plenty of business owners learned that in 2020. The structural problem is not whether you have a reserve. It is whether the reserve does anything while it waits, and whether it disappears under stress.

A cash reserve that earns nothing is not conservative. It is an expensive insurance policy against opportunity, and the premium is everything that capital could have earned.

02 / The frameworkWhat does it mean to use cash value life insurance as a business asset?

Using cash value life insurance as a business asset means funding an overfunded whole life policy with surplus capital, then borrowing against its cash value to deploy into the business while the policy keeps compounding on its full value. That is the mechanism. The discipline layered on top of it is what we call The And Asset.

The borrow-and-deploy idea is not new. Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker, and his core insight holds for a business: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. If the framework is new to you, start with our pillar explainer, What Is Infinite Banking? The And Asset Guide, which lays out the borrow-and-deploy principle in full. The And Asset builds on Nash's foundation with one rule his broader teaching does not enforce.

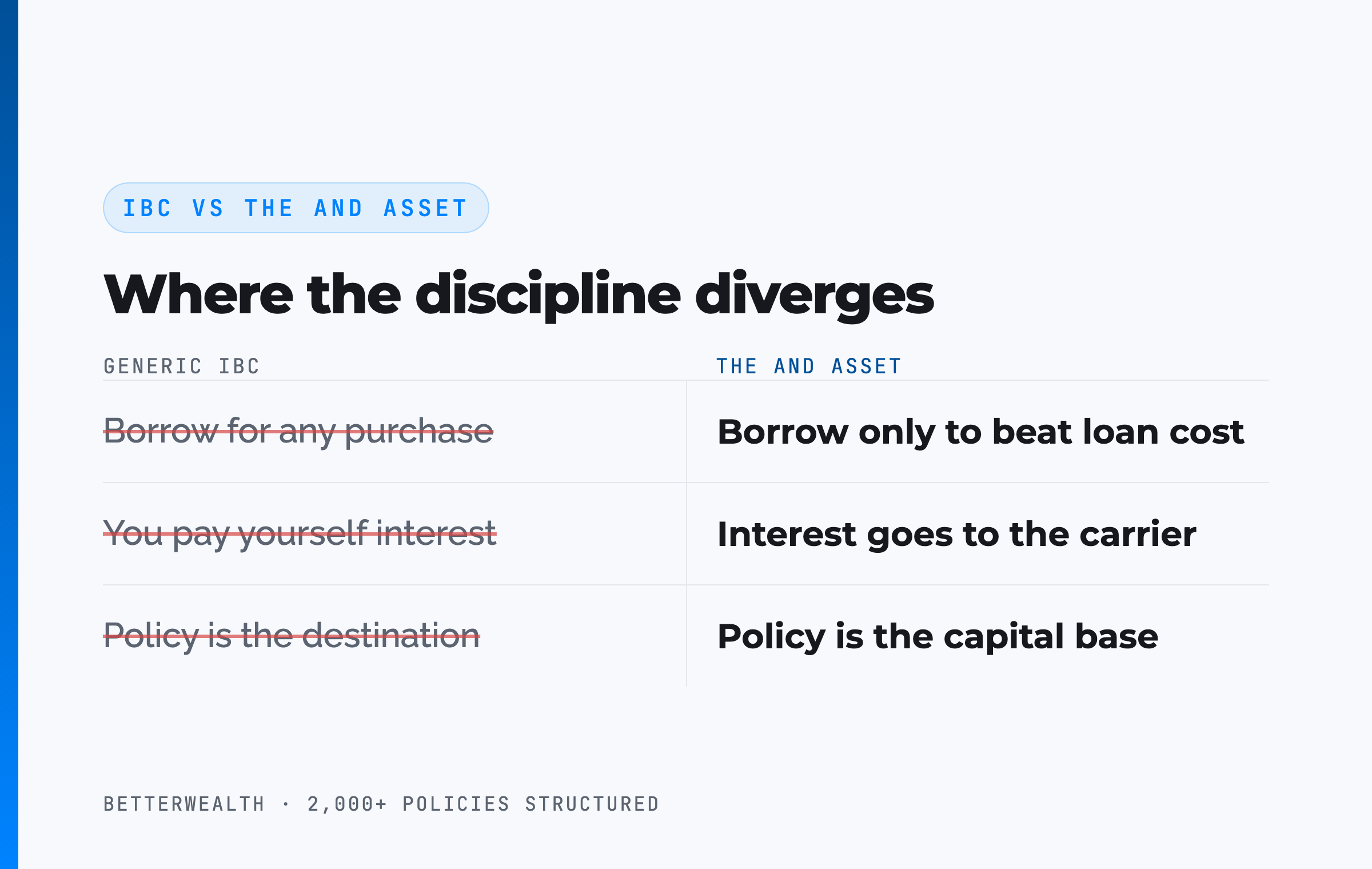

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns in the business while the policy compounds, net of mortality and expense charges, the entire time.

For a business owner, the distinction is sharper than it is for anyone else. You already think in terms of return on capital. The policy is the capital base. The value gets created in what you deploy that capital into.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. It is not a magic account. It is a disciplined way to make the same dollar earn inside the policy and inside your business at once.

03 / How it worksHow a business owner sets up a policy as an And Asset

A cash value policy functions as a business asset through five steps, and the order matters. The product is overfunded whole life, designed for maximum cash value rather than maximum death benefit. Here is the sequence we use when we structure one for a business owner.

- Decide who owns the policy. A policy can be owned personally by the owner or by the business entity. Personal ownership keeps it off the business balance sheet and is common when the owner funds it from compensation. Business ownership is used for key-person and buy-sell purposes, and it triggers the IRC Section 101(j) rules covered below. This is a decision to make with your tax advisor.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows without creating a Modified Endowment Contract. The PUA rider is the engine that builds early cash value. The base/PUA split is the single design decision that determines how much capital is accessible early.

- Fund with retained earnings. Route a portion of surplus cash or owner cash flow into the policy on a consistent schedule. The funding window is flexible, but the optimal horizon runs 10 to 25 years. Consistency matters more than size.

- Let the early years capitalize. Do not expect to break even on day one. You will not. For a healthy insured, cash value stays below cumulative contributions through the first several years and typically crosses total contributions at year 5 or later. Any illustration showing year-two break-even is fiction.

- Borrow and deploy. After about 30 days from initial funding, you can take a policy loan collateralized by your cash value. Put the borrowed capital into an activity that beats the carrier's loan cost, then repay from the cash flow that activity produces. The policy compounds on its full value the entire time.

The mechanics of step two are where most of the value is won or lost, and most agents gloss over it. If you want the full breakdown of the base/PUA split and why design beats carrier choice, our overview for owners, Life Insurance for Business Owners: The Complete Guide, covers the structuring decisions in depth.

The reserve and the opportunity capital are the same dollars

This is the part that trips people up. The cash value is not split into a "reserve bucket" and an "investment bucket." It is one pool. When you borrow against it, the loan is collateralized by the cash value rather than withdrawn from it, so the full balance keeps compounding while you have capital working in the business. The reserve and the opportunity capital are the same dollars doing two jobs. That is the structural feature, and it is why a credit line is not a substitute.

One pool. Two jobs.

This fits a specific kind of business doing specific things.

It fits you if

- Your business throws off surplus cash that sits idle

- You have a long capital horizon (10+ years)

- You can name uses for capital that beat the loan cost

- You want a reserve that compounds and cannot be frozen

It does not fit you if

- Your business is short on operating cash

- You are carrying high-interest debt right now

- You want a savings account, not a capital strategy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether this belongs in your capital structure and how to design it. If you are in the second, we will tell you that too.

Book a Discovery Call04 / The mathDoes the deployed return clear the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow. This is the entire test, and for a business owner it is usually easier to pass than for anyone else, because you already have uses for capital with known returns. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6 percent range, but treat the specific number as a variable to verify with your carrier, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, including the borrowed portion, adjusted by the carrier's recognition structure. Your deployed capital earns its own return inside the business. If that return clears the loan cost, you are ahead on the spread, and the dollar has done two jobs. If it does not, you have borrowed money to lose money slowly. The honest constraint is the whole strategy: if you cannot find a use that beats the loan rate, do not borrow. Leave the capital compounding inside the policy.

If the deal does not clear the loan rate, do not borrow.

05 / Ownership rulesWhat is COLI, and what does IRC 101(j) require?

COLI is corporate-owned life insurance, a policy a business owns on the life of an owner or a key employee, and IRC Section 101(j) sets the rules that keep its death benefit tax-free. Section 101(j) was enacted as part of the Pension Protection Act of 2006. Its default rule is blunt: the death benefit on an employer-owned policy is treated as taxable income to the business to the extent it exceeds the premiums paid, unless the business met specific requirements before the policy was issued and an exception applies.

The gateway is notice and consent, and it has to happen before the policy is in force. The employee must be notified in writing that the business intends to insure their life, told the maximum face amount the business could buy, and informed that the business will be a beneficiary. The employee must consent in writing. Miss that step before issue and you generally cannot fix it later. The business also files IRS Form 8925 each year to report its employer-owned contracts.

When this matters and when it does not

If the owner holds the policy personally and funds it from compensation, Section 101(j) is not the governing rule, because the business does not own the contract. The 101(j) machinery applies specifically to employer-owned policies: key-person coverage, buy-sell funding owned at the entity level, and similar arrangements. The point is not to scare you off business ownership. It is to make sure that if you go that route, the notice-and-consent paperwork is handled before issue, not discovered after a death claim. We coordinate this with your CPA and attorney rather than around them.

Notice and consent happen before issue, or not at all.

The fastest way to turn a tax-free death benefit into a taxable one is to skip a one-page consent form before the policy is issued. Get the ownership question right first.

06 / The tax treatmentWhy the tax mechanics make this work for retained earnings

The tax treatment is what makes a cash value policy a credible home for retained earnings rather than just another place to park cash. Two features do the work. First, the cash value grows tax-deferred inside the policy under the current tax treatment of permanent life insurance, so the surplus compounds without an annual tax drag the way a taxable account would carry. Second, a loan taken against a properly structured, non-MEC policy is not taxable income while the policy stays in force, because it is a loan collateralized by cash value, not a withdrawal of gain.

Both features come with conditions, and the conditions are the whole point. The policy has to stay under the Modified Endowment Contract limit to preserve the loan treatment, which is why design discipline matters from day one. And if a policy lapses or is surrendered with a loan outstanding, gain that was deferred can become taxable, sometimes at the worst possible time. These are not reasons to avoid the strategy. They are reasons to structure it correctly and manage it over time, which is what a practitioner is for.

Stated plainly: this is not a way to make taxable income disappear. It is a way to let surplus capital compound on a tax-deferred basis and stay accessible through loans that are not, by themselves, a taxable event. Anyone promising "tax-free returns" without explaining the MEC limit and the lapse risk is selling, not explaining.

07 / Where people get this wrongThe mistakes that turn a good tool into a bad one

The most common mistakes are not about the concept. They are about execution, and each one is avoidable. The first is buying a policy designed for death benefit instead of cash value, which buries the early capital under commission-heavy base premium. Without a heavy paid-up additions rider, this is an expensive death benefit, not a capital base.

The second mistake is borrowing for consumption instead of deployment. A business owner who pulls policy loans to cover lifestyle or to plug a recurring cash shortfall is not running The And Asset. They are running an expensive overdraft. The third is treating the policy as a short-term play. Cash value rewards a long horizon, and an owner who needs the money back in two years should not start. The fourth is getting the ownership and 101(j) details wrong, which we covered above.

The policy does not create the return. Your business does. The policy lets the capital you deploy keep compounding while it is at work, which is a structural edge, not a yield.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we build a cash value policy as a business asset, including the base/PUA split and the loan-cost math. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the four honest tradeoffs

The benefits of a cash value policy come with four tradeoffs that disqualify it for some businesses, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, the long horizon. Cash value does not exceed cumulative contributions before year 4, and break-even lands at year 5 or later for a healthy insured. If you need the capital to outpace contributions quickly, this is the wrong tool. Second, the capital commitment. Funding a policy from retained earnings means that cash is committed to a multi-year plan, and a business with volatile cash flow may not want that. Third, the discipline requirement. The strategy only works if every loan clears the loan cost, and an undisciplined borrower will erode the advantage. Fourth, the management burden. Staying under the MEC limit and keeping the policy in force requires ongoing attention, not a set-and-forget mentality.

Against those tradeoffs sits the structural benefit that defines the strategy: capital that compounds tax-deferred, stays accessible through loans that are not taxable income, cannot be frozen by a lender, and lets the same dollar work inside the policy and inside the business at once. For the right owner, that combination is hard to replicate anywhere else.

Slow to build. Hard to beat once it is built.

09 / The fitWho is this right for, and who isn't it?

This is right for the established business owner with surplus retained earnings, a long capital horizon, and a steady stream of uses for capital that beat the carrier's loan cost. It fits the owner who is tired of idle cash, who values a reserve that compounds and cannot be called, and who already thinks in terms of return on capital. For that owner, a cash value policy is one of the few places where the reserve and the opportunity fund are the same money.

It is wrong for the early-stage business still hunting for product-market fit, the owner short on operating cash, and anyone carrying high-interest debt that a cash infusion should retire first. It is also wrong for the owner who wants a savings vehicle with no strategy behind it. If you cannot name an activity that beats the loan cost, no policy design changes that answer.

10 / Head to headThe policy against the alternatives business owners use

Compared to the capital tools business owners actually reach for, a cash value policy trades day-one liquidity for control, tax treatment, and uninterrupted compounding. The table sets it against a business line of credit, a SEP or solo 401(k), and cash sitting in the bank, on the four dimensions that matter for a business reserve.

| Dimension | Cash Value Policy (And Asset) | Business Line of Credit | SEP / Solo 401(k) | Cash in the Bank |

|---|---|---|---|---|

| Growth | Compounds tax-deferred on full cash value, even while borrowed against | None (it is a credit line, not an asset) | Market growth, tax-deferred | Minimal; loses ground to inflation |

| Access under stress | Loans after ~30 days; cannot be called or frozen by the carrier | Can be reduced, frozen, or repriced when you need it most | Restricted before 59½ (penalty plus tax) | Immediate, but spending it ends the reserve |

| Tax treatment | Tax-deferred growth; properly structured loans are not taxable income | Interest may be deductible as a business expense | Deferred now, taxed as ordinary income later | Interest taxed annually as ordinary income |

| Control | Loan cannot be called; you set repayment terms | Lender controls terms and can revoke access | Access rules set by Congress, not you | Full control, but no leverage feature |

Growth. A cash value policy keeps compounding tax-deferred on its full value while you borrow, which a credit line cannot do because a line is not an asset. That uninterrupted compounding is the structural feature that makes the same dollar do two jobs.

Access under stress. A line of credit is faster on paper, but it can vanish exactly when you need it, as many owners learned in 2020. A policy loan cannot be called by the carrier. The 30-day initial wait and the slower early build are the cost of access that does not disappear in a downturn.

Tax and control. Tax-deferred growth plus loans that are not taxable income give the policy a treatment a taxable account cannot match, and a retirement plan restricts access until 59½ under rules set by Congress. The And Asset trades the highest possible early liquidity for control and tax treatment you keep.

A composite: the owner who deployed retained earnings at year seven

Consider a 43-year-old owner of a profitable services business, preferred non-tobacco, funding an overfunded whole life policy at $60,000 per year from retained earnings on a cashflow design. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

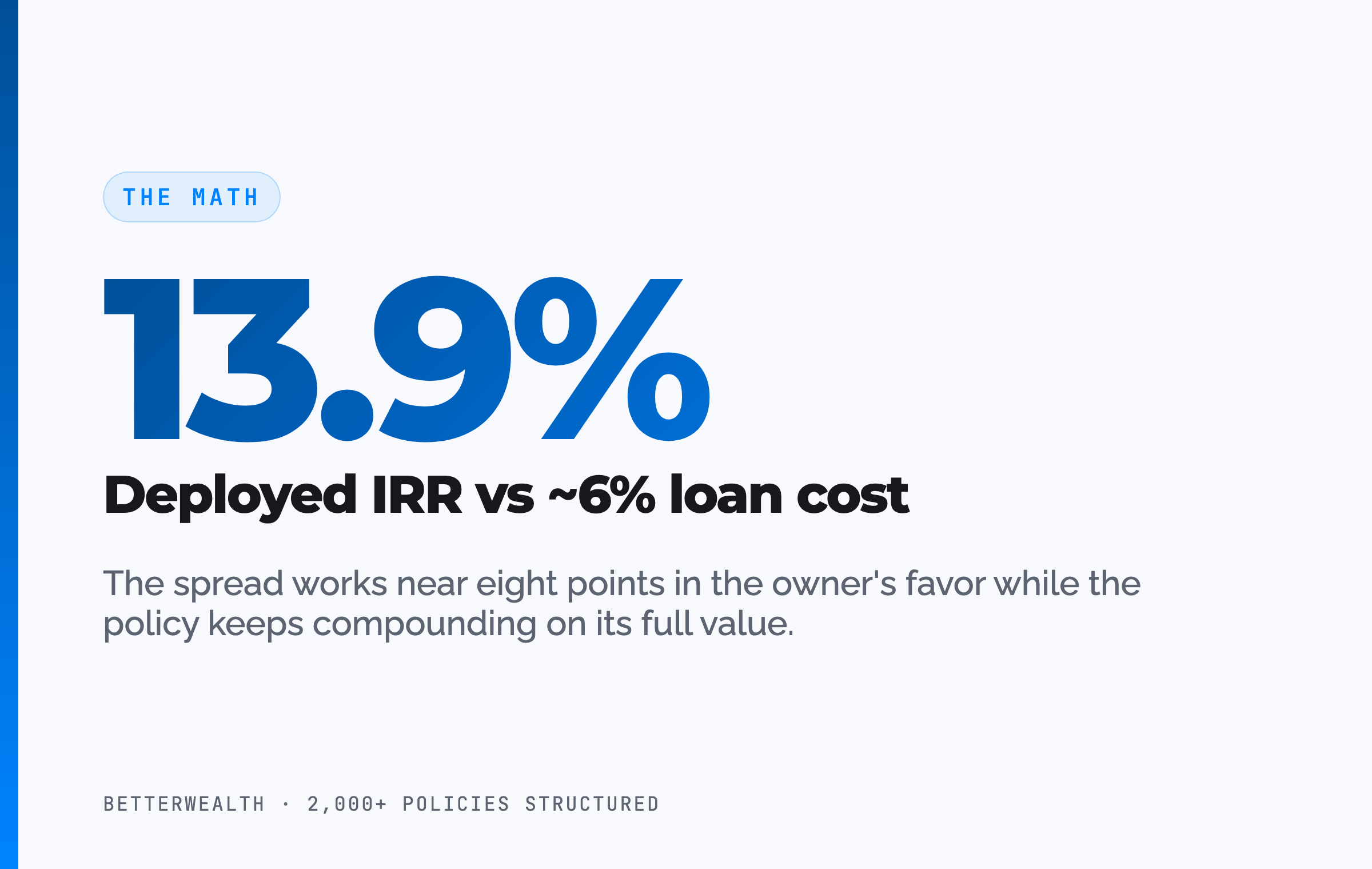

In year seven, with roughly $437,000 of accessible cash value, the owner borrows $213,500 against the policy to fund a second-location buildout the business had been delaying. The expansion returns an estimated 13.9% IRR through added margin. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by nearly eight points. The policy keeps compounding tax-deferred on its full value the entire time. Repayment runs on a 44-month schedule funded by the new location's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits your business.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your business, your cash position, and your time horizon, then tells you whether a cash value policy, a different structure, or nothing at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQCash value life insurance for business owners

How do business owners use cash value life insurance?

Business owners use a properly structured, overfunded whole life policy as a business asset in three ways: a liquid reserve they can access, opportunity capital they borrow against for deals, and a tax-advantaged place to store retained earnings. The cash value grows tax-deferred, and a properly structured policy loan is not taxable income while the policy stays in force.

Is cash value life insurance a good place to store retained earnings?

It can be, for a business with surplus cash earning little where it sits. Cash value grows tax-deferred and stays accessible through policy loans, so retained earnings keep compounding while remaining available for opportunities. The constraint is the long horizon: cash value does not exceed cumulative contributions before year 4, with break-even at year 5 or later for a healthy insured.

What is COLI, and what is the IRC 101(j) notice-and-consent rule?

COLI is corporate-owned life insurance, a policy a business owns on the life of an owner or key employee. Under IRC Section 101(j), enacted as part of the Pension Protection Act of 2006, the death benefit on an employer-owned policy is generally taxable income unless the employer met written notice-and-consent requirements before the policy was issued and an exception applies. Employers also file IRS Form 8925 each year.

Are policy loans from a business life insurance policy taxable income?

A loan taken against a properly structured, non-MEC whole life policy is not taxable income while the policy stays in force, because it is a loan collateralized by cash value, not a withdrawal of gain. If the policy lapses or is surrendered with a loan outstanding, previously deferred gain can become taxable. Structure and ongoing management matter.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Should the policy be owned by me or by my business?

It depends on the goal and the entity structure. Personal ownership keeps the policy off the business balance sheet and is common when the owner funds it from compensation. Business ownership is used for key-person coverage and buy-sell funding, but it triggers the IRC Section 101(j) notice-and-consent rules and Form 8925 reporting. This is a decision to make with a tax advisor.

How fast can a business owner access the cash value?

Most carriers allow policy loans within about 30 days of initial funding, with smaller loans available by phone and larger loans through a loan form. The loan cannot be called by the carrier the way a bank can freeze a line of credit, which is part of why business owners value the cash value as a reserve.

Does the cash value keep growing while I borrow against it?

Yes. A policy loan is collateralized by the cash value rather than withdrawn from it, so the full cash value continues to compound, adjusted by the carrier's recognition structure. That uninterrupted compounding is what lets the same dollar do two jobs, the core of The And Asset.

Who should not use cash value life insurance for their business?

A business that is early-stage, short on operating cash, or carrying high-interest debt should not tie capital up in a long-horizon policy. The strategy fits an owner with surplus retained earnings, a long time horizon, and clear uses for capital that beat the loan cost. If you cannot name a use that clears the loan rate, do not borrow.

What does it cost to get started, and how is the policy designed for cash value?

A cash-value-focused policy minimizes base premium and maximizes the paid-up additions rider, pushing early cash value as high as the IRS allows without creating a Modified Endowment Contract. Funding is flexible, with an optimal horizon of 10 to 25 years. The base/PUA split is the single design decision that most determines early accessible cash, which is why design matters more than carrier choice.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 101 (Cornell Law), including 101(j), the employer-owned life insurance rules and the notice-and-consent requirement.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- IRS Form 8925, the report of employer-owned life insurance contracts.

- LIMRA, life insurance industry data and persistency benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you run a business and want an honest read on whether a cash value policy fits your capital structure, book a discovery call. We will tell you if it does not.