.png)

Is IUL a good investment? Strictly speaking, no, because indexed universal life is not an investment. It is life insurance with a cash-value component tied to a market index, subject to caps, floors, and rising internal costs. Judged as a pure investment it usually disappoints. Judged as a capital tool for a specific buyer, it can fit.

The question "is IUL a good investment" carries a hidden assumption that breaks the answer before you start. It treats an insurance contract as if it were a brokerage account, then grades it on the one thing it was never built to win: raw return. An indexed universal life policy will lose that contest to a low-cost index fund almost every time, because the fund has no cap, no cost of insurance, and full dividend participation. If return is the only metric, the conversation is over.

The honest answer is that IUL is not an investment at all, and judging it as one is exactly how buyers get burned on both ends. One agent oversells it as a tax-free market account. The next advisor dismisses it as a ripped-off mutual fund. Both are answering the wrong question, and the person caught in the middle pays for the confusion.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we design primarily with whole life. We are not here to sell you an IUL. We are here to tell you what an IUL actually is, where it can fit, where it fails, and why the high-rate illustration you were shown is the single most misleading document in this product category. If you want the mechanics first, our overview of how indexed universal life insurance works walks through the moving parts in order.

This piece reframes the question, then answers it. We cover what IUL is, the illustration trap, the four costs nobody itemizes, when it genuinely fits, and how the cash value relates to The And Asset, the disciplined framework we teach for using a policy as usable capital.

- IUL is life insurance with a cash-value component, not a registered investment, so judging it on raw return sets the wrong expectation.

- Index crediting is subject to a cap and a floor, and the insurer can lower caps and participation rates over time.

- The illustration trap is a high projected rate compounded for decades that the policy's non-guaranteed elements rarely sustain.

- A 0% floor protects against index loss, but cost of insurance and expenses still come out of cash value.

- IUL can fit a high-income earner who wants flexible premiums and accepts variability, not someone who needs certainty.

- The And Asset discipline applies to any cash-value policy: borrow only to deploy into a return that beats the loan cost.

01 / The wrong questionWhy "is IUL a good investment" breaks the answer

The phrase frames an insurance contract as an investment, and that framing guarantees a bad answer. An investment is something you buy expecting a return on capital, measured against other places that capital could go. An IUL is a life insurance policy with a savings feature attached. The death benefit is the product. The cash value is a byproduct of overfunding that product and letting it grow under a tax shelter.

When you grade a byproduct as if it were the headline, you get distortion in both directions. Sold as an investment, the cap and the costs get hidden. Dismissed as an investment, the death benefit, the tax treatment, and the access through loans get ignored. The accurate move is to stop asking whether it is a good investment and start asking whether it is a good insurance policy that also builds usable capital.

You do not own the index. You do not collect its dividends. You own a life insurance contract whose cash value moves with the index inside a cap and a floor. That is a different thing than investing, and the difference is the whole answer.

02 / What it actually isWhat does an IUL actually do with your money?

An IUL splits every premium into three jobs before any growth happens. Part pays the cost of insurance for the death benefit. Part pays policy expense and administrative charges. What remains goes into the cash value, where it is credited based on the movement of a market index such as the S&P 500, subject to a cap on the upside and a floor on the downside.

The floor is the feature agents lead with. In a year the index falls, the credited rate does not go below the floor, often 0%, so the index loss does not hit your cash value directly. The cap is the feature they mention last. In a year the index surges, your credited rate stops at the cap, so a 20% index year might credit you a single-digit number. You trade the tails. You give up the big up years to avoid the big down years, and the insurer keeps the spread.

The cash value is real, but it is not the index

Your cash value is a contractual account inside an insurance policy, not a position in the market. The crediting formula references the index. It does not invest in it. That distinction is why dividends from the underlying companies never reach you, and why the carrier can adjust the cap on next year's segments. The mechanism is closer to a structured note than a stock fund. A properly funded IUL still builds meaningful cash value over time, and that cash value is the part that can do a second job, which is where cash value functions as usable capital under The And Asset.

The index is a measuring stick, not a holding.

03 / The illustration trapWhy the projection you were shown rarely holds

The illustration trap is the practice of showing a high projected credited rate compounded across thirty or forty years, producing a cash-value column that looks like it beat the market. It is the most persuasive and least reliable document in this category. The number is a projection built on non-guaranteed assumptions, and the two assumptions doing the heavy lifting, the credited rate and the cap, are the two the insurer can change.

Run the same policy at a lower credited rate and the picture inverts. Costs that were quietly covered by the high projection now eat into cash value, the policy needs more premium to stay in force, and the tax-free income the agent promised shrinks or disappears. Regulators saw enough of this to introduce the NAIC's Actuarial Guideline 49, which constrains the maximum rate an IUL can be illustrated at and limits the benefit of bonus multipliers. It narrowed the worst abuses. It did not close the gap between a projection and a guarantee.

Marketers have ruined how this product gets explained. An illustration is a sales tool, not a promise. Read the guaranteed columns, and if the policy only works at the projected rate, it does not work.

The defense is simple and almost nobody does it. Ask for the policy run at a credited rate two or three points below the projection. Ask what happens to the premium if the cap drops. A policy that survives that stress test is a policy you can plan around. A policy that collapses under it was sold to you on a number that was never yours to keep.

04 / How to evaluate itHow to judge an IUL before you judge its return

Evaluating an IUL honestly means separating its two jobs and stress-testing the funding before any return number enters the conversation. The product is a permanent life insurance contract with a flexible-premium chassis, which means you carry more responsibility for keeping it healthy than you would with a level-premium whole life policy. Here is the sequence we use.

- Separate the two jobs. Ask what the policy delivers as life insurance, then separately what the cash value can do as capital. A single blended return number hides both answers and is the source of most disappointment.

- Read the guarantees, not the illustration. Look at the guaranteed columns. The credited rate is capped, the cap is not guaranteed, and the cost of insurance rises as you age. The guaranteed page tells you the floor of the experience.

- Stress-test the funding. Run the policy at a credited rate well below the projection and confirm it stays in force without a surprise premium call in later years. Fragility shows up here, not on the sales page.

- Let cash value capitalize. Expect the early years to trail cumulative premiums. A healthy policy reaches break-even at year five or later, then cash value can begin to exceed total contributions. Any illustration showing year-one or year-two break-even is fiction.

- Borrow only when the math clears the loan cost. Take a policy loan against cash value only to deploy into an activity that returns more than the carrier's loan cost. Repay from the cash flow that activity produces. If nothing clears the loan cost, do not borrow.

Notice that none of these steps is about the index. The index is the part of the policy you cannot control. The funding, the design, and the discipline are the parts you can, and they decide the outcome far more than whether the S&P had a good decade.

An IUL fits a specific person, not everyone who gets pitched one.

It can fit you if

- You want permanent coverage with flexible premiums

- You accept index-linked variability and capped upside

- You will fund it consistently and monitor it

- You can name a use for capital that beats the loan cost

It does not fit you if

- You want a guaranteed outcome

- You were sold it as a market replacement

- You cannot fund it through a flat year

- You have no use for borrowed capital that clears the loan cost

If you are in the first column, a 30-minute conversation will tell you whether an IUL, a whole life policy, or no policy at all fits your plan. If you are in the second, we will tell you that just as directly.

Book a Discovery Call05 / The four costsCan an IUL lose money? The costs nobody itemizes

An IUL can erode even in a year the index rises, because four costs sit between the index and your cash value, and an illustration rarely lists them in plain English. Understanding them is what separates a buyer from a mark.

First, the cost of insurance. This is the charge for the death benefit, and it climbs every year as you age. A policy that felt cheap at 40 can feel expensive at 70 if it is underfunded. Second, policy expense and administrative charges, which come out regardless of index performance. Third, the cap and participation rate, which are not direct fees but function like one: every point the index earns above your cap is value the insurer keeps. Fourth, the floor's hidden catch. A 0% credited year still incurs the cost of insurance and expenses, so flat crediting can mean a net decline in cash value.

Stack those together and the failure mode becomes clear. If costs outrun crediting in an underfunded policy, the cash value drains to cover the charges, and the policy can lapse. A lapse with an outstanding loan is the worst case, because the forgiven loan can become taxable income in the year everything collapses. None of this is exotic. It is the ordinary physics of a flexible-premium contract that was funded on optimism.

A 0% year is not a free year.

This is not for everyone, and an IUL is not for everyone. If you cannot fund it through a flat stretch and you will not read the guaranteed page, the most likely outcome is a policy that underperforms what you were promised and costs more than you expected.

06 / The frameworkWhere The And Asset fits, and where it does not

The And Asset is BetterWealth's framework for using a properly structured permanent policy as a capital base you borrow against, and it applies to an IUL only when the policy is funded to behave like a capital base rather than a bet on caps. The discipline is what matters, not the product label.

Nelson Nash pioneered the idea of using permanent life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule the broader teaching does not enforce.

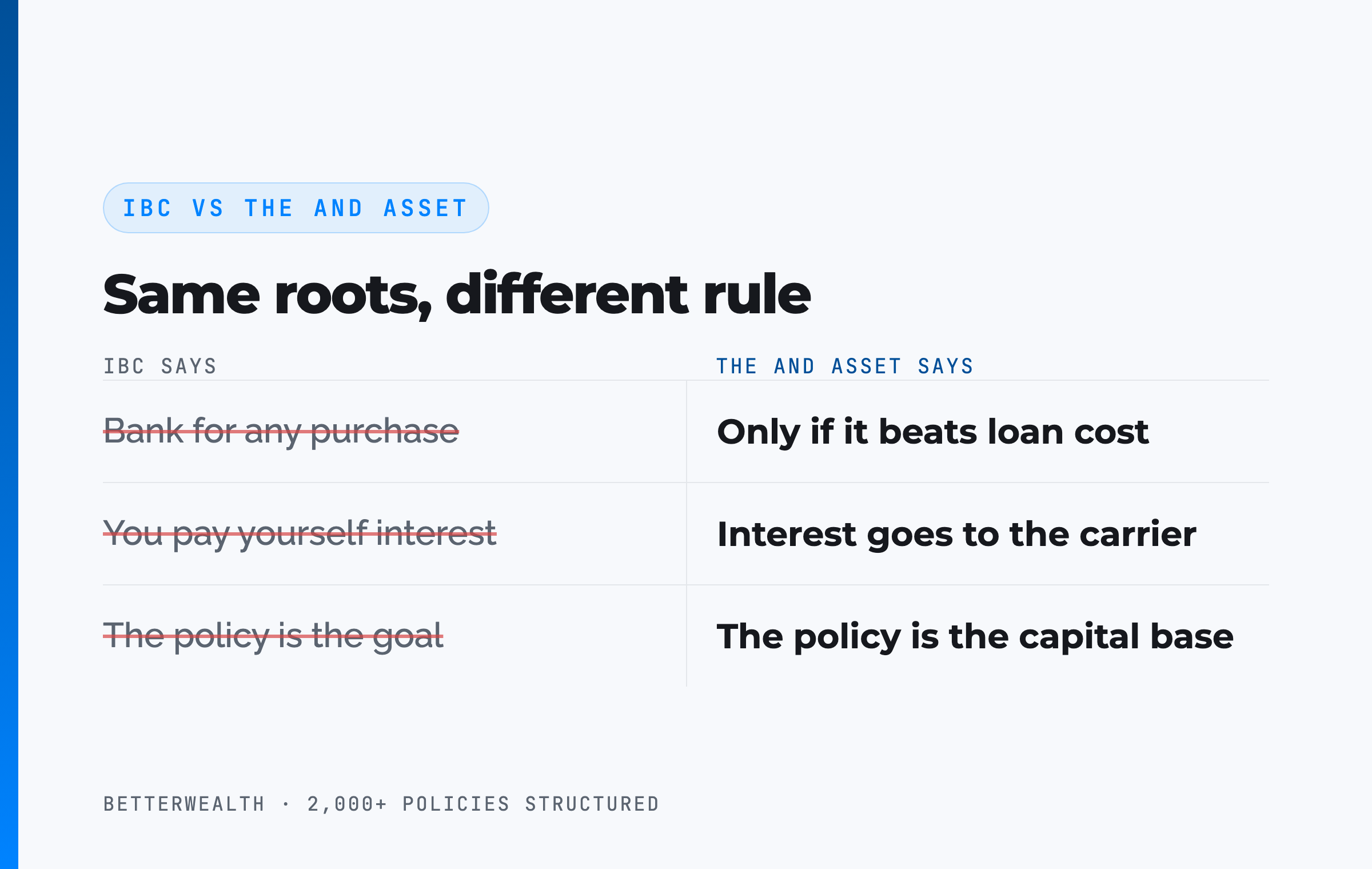

Where IBC ends and The And Asset begins

IBC says you can use a permanent policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of its internal charges.

Here is the honest part about IUL specifically. We design primarily with whole life because The And Asset depends on a dependable capital base, and whole life gives you contractually guaranteed cash value and a level premium. An IUL introduces variables a guaranteed policy does not: caps that can drop, costs that rise, and a credited rate that swings with the index. An IUL can still serve as an And Asset for someone who wants flexible funding and accepts that variability, but the discipline has to be tighter, not looser, because the capital base itself is less predictable. If certainty is what you are after, the comparison runs through our breakdown of IUL versus whole life insurance.

The math has to work. Every time.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring questions we use when we pressure-test an IUL or a whole life illustration before anyone signs. Free, email-gated, no spam.

Open the Vault07 / The fitWho is an IUL actually right for?

An IUL is right for a high-income earner who wants permanent coverage, values premium flexibility, and is comfortable taking on index-linked variability along with the responsibility of monitoring the policy. The flexible-premium chassis is an advantage for someone whose income is lumpy, a business owner or commissioned earner who wants to fund heavily in strong years and lighter in lean ones, as long as the policy stays adequately funded.

It is the wrong product for someone who wants a guaranteed result, who was told it would replace their market portfolio, or who will not stay engaged with funding for decades. Those buyers are usually better served by whole life, where the cash value and premium are contractual, or by simply separating their insurance and their investing entirely. The worst outcome is the buyer in the middle who wanted certainty, was sold variability, and only learns the difference when the cap drops.

If you cannot identify a productive use for borrowed capital that beats the loan cost, the cash-value-as-capital argument does not apply to you, and no policy design changes that. The strategy is the discipline, not the contract.

08 / Head to headIUL against the alternatives

Compared to the vehicles it gets measured against, an IUL trades raw return for a death benefit, tax treatment, and access, while carrying more variability than whole life. The table sets it against a low-cost index fund, whole life insurance, and a Roth IRA on the dimensions that actually decide fit.

| Dimension | Indexed Universal Life | Index Fund | Whole Life | Roth IRA |

|---|---|---|---|---|

| Growth | Index-linked, capped upside, 0% floor, net of rising internal costs | Full index return, no cap, taxed on gains | Guaranteed cash value plus non-guaranteed dividends, net of charges | Full market return, tax-free if rules met |

| Guarantees | Floor on crediting, but caps and costs are not guaranteed | None; full market risk | Guaranteed cash value and level premium | None on growth; tax treatment is the guarantee |

| Access | Policy loans and withdrawals, not taxable income while in force | Fully liquid, settles in days | Policy loans, not taxable income while in force | Contributions anytime; gains restricted before 59½ |

| Death benefit | Yes, income-tax-free to beneficiaries | No | Yes, income-tax-free to beneficiaries | No |

Growth. For pure accumulation, the index fund wins because it keeps the full return and the dividends. An IUL is not trying to win that race. It is packaging a capped, floored crediting formula inside a tax-advantaged insurance contract, which is a different proposition than market participation.

Guarantees. This is where IUL and whole life part ways. Whole life gives you a guaranteed cash value and a premium that never changes. An IUL gives you a floor on a single year's crediting, while the cap and the cost of insurance stay variable. One trades upside for certainty. The other trades certainty for capped participation and flexibility.

Access and death benefit. Against a Roth, the IUL's edge is the death benefit and loan access without the 59½ restriction, traded for capped growth and real internal costs. The Roth's edge is uncapped, genuinely tax-free growth with no cost of insurance. They solve different problems and should not be forced into the same column.

A composite: the illustration that did not hold

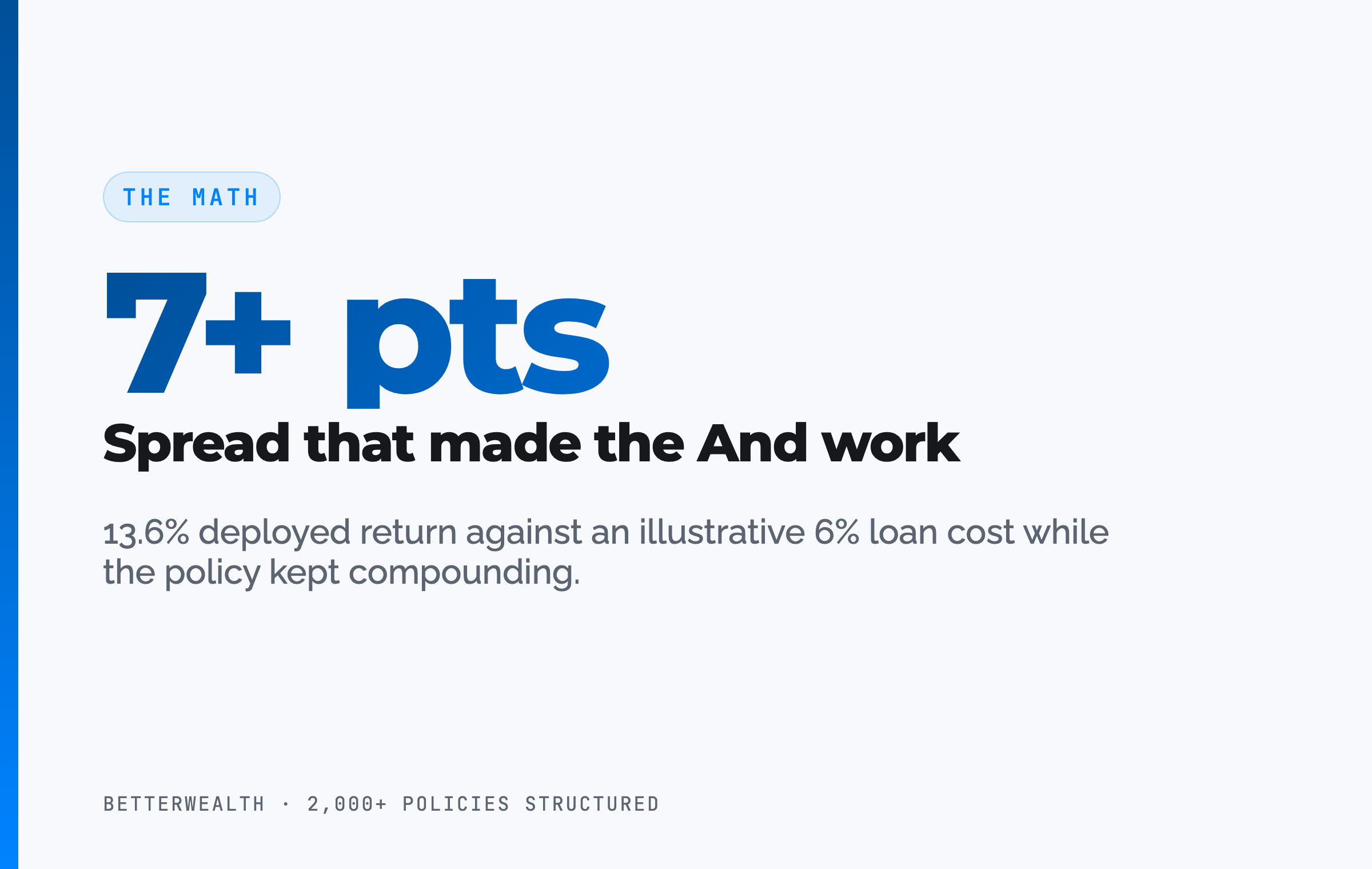

Consider a 44-year-old business owner, preferred non-tobacco, who was shown an IUL illustration projecting a 6.8% credited rate and funding it at $37,500 per year. This is a representative composite, not a single named client, and it shows what the reframe looks like in dollars.

Through the first three years, cash value trailed cumulative contributions, exactly as a real policy should. The illustration had shown break-even closer to year four on its projected rate. Re-run at the credited rate the policy actually earned, with the cap trimmed once along the way, break-even landed in year six instead. Nothing failed. The policy simply behaved like the non-guaranteed contract it always was, not like the projection.

Here is the part that mattered more than the rate. In year eight, with roughly $214,000 of accessible cash value, the owner borrowed $96,000 against the policy to acquire revenue-producing equipment for the business. That deployment returned an estimated 13.6% IRR against an illustrative loan cost near 6%, a spread of more than seven points in the owner's favor. Repayment ran on a 44-month schedule funded by the equipment's own cash flow, and the policy kept compounding on its full value the entire time. The IUL was a mediocre investment and a workable capital base. Those are two different verdicts, and only the second one was ever the point.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether an IUL fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner reads your actual illustration, stress-tests the funding, and tells you whether an IUL, a whole life policy, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQIs IUL a good investment? Common questions

Is IUL a good investment?

IUL is not an investment, so judging it as one sets the wrong expectation. Indexed universal life is life insurance with a cash-value component tied to a market index, subject to caps, floors, and rising internal costs. As a pure investment it usually underperforms a low-cost index fund. As a capital tool with tax features and a death benefit, it can fit a specific buyer with a long horizon.

Why is IUL not technically an investment?

An IUL is a life insurance contract, not a registered security. You do not own the index, you do not receive its dividends, and your gains are capped while your costs rise with age. The cash value is credited based on index movement subject to a cap and a floor, which is a different mechanism than owning shares.

What is the illustration trap with IUL?

The illustration trap is when an agent shows a high projected credited rate compounded for decades, making the policy look like a market-beating account. Caps and participation rates are not guaranteed and the insurer can lower them, so the projected rate often does not hold. Regulators introduced Actuarial Guideline 49 to rein in the most aggressive illustrations, but the gap between projection and reality remains the main reason buyers feel misled.

What is the difference between IUL and whole life insurance?

Whole life has guaranteed cash value, a level guaranteed premium, and dividends from a mutual carrier. IUL has flexible premiums, index-linked crediting subject to caps and floors, and internal costs that rise with age and are not guaranteed. Whole life trades upside for certainty. IUL trades certainty for capped index participation and flexibility.

Can an IUL lose money?

The cash value will not be credited less than the policy floor in a negative index year, which is often 0%. But the internal cost of insurance and expense charges still come out of the account, so a 0% credited year can still reduce net cash value. If costs outrun crediting and the policy is underfunded, it can lapse, and a lapse with an outstanding loan can trigger a tax bill.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured permanent life insurance policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a permanent policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is an IUL a good vehicle for The And Asset?

An IUL can serve as a capital base for The And Asset only when it is funded to behave like one and the buyer accepts its variability. We design primarily with whole life because the strategy depends on a dependable cash value, and IUL's caps, floors, and rising costs introduce variables a guaranteed policy does not. The discipline is the same: borrow only to deploy into a return that beats the loan cost.

Who should consider an IUL?

An IUL can fit a high-income earner who wants permanent coverage, flexible premiums, and is comfortable with index-linked variability and the responsibility of monitoring funding. It does not fit someone who wants a guaranteed outcome, who was sold it as a market replacement, or who cannot fund it consistently. If you need certainty, whole life is usually the better permanent structure.

How are IUL cash value and loans taxed?

Cash value grows tax-deferred under IRC Section 7702, and a properly structured policy loan is not treated as taxable income while the policy stays in force and is not a Modified Endowment Contract. If the policy lapses or is surrendered with gains, or if it becomes a MEC, tax consequences can apply. Treat the tax treatment as conditional on keeping the policy in force, not as automatic.

Is IUL better than investing in an index fund?

For pure accumulation, a low-cost index fund usually wins because it has no cap, no cost of insurance, and full dividend participation. IUL is not competing on raw return. It competes on the package of a death benefit, tax-deferred growth, creditor protection that varies by state, and access through policy loans. Compare it on that package, not on return alone.

- Nelson Nash, Becoming Your Own Banker. The origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law). The tax code provision behind the tax treatment of life insurance cash value and loans.

- NAIC. Actuarial Guideline 49 and consumer guidance on indexed universal life illustrations.

- LIMRA. Life insurance industry data, including indexed universal life sales trends.

- FINRA. Investor guidance on the fine print of indexed universal life insurance.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether an IUL fits your plan, book a discovery call. We will tell you if it does not.