.png)

IUL vs whole life comes down to predictability versus index-linked upside. Whole life guarantees cash value growth, a level premium, and a level cost of insurance. Indexed universal life ties growth to an index with a cap and floor, uses flexible premiums and an increasing cost of insurance, and does not guarantee the crediting rate.

Most people compare these two products by staring at illustrations and picking the one with the bigger number in year 30. That is the wrong instinct, and it is exactly how a buyer ends up with a policy that does not behave the way the sales meeting promised. An illustration is a projection, not a contract. The difference between indexed universal life and whole life is not which one shows a larger figure on paper. It is which guarantees are real and which numbers can change after you sign.

The honest comparison is not "which one is better," it is "which set of tradeoffs matches what you are actually trying to do with the money." Whole life and indexed universal life solve different problems. One is built for predictability. The other is built for index-linked upside that you have to manage and fund. Confuse the two and you will be disappointed by whichever one you bought.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we get this question constantly from entrepreneurs and high-income earners who have been pitched both. We favor properly designed whole life for a cash-value capital strategy because predictability is the whole point of borrowing against an asset. That is a position, not a verdict on the product category. IUL is a legitimate tool, and there are situations where it fits better. This piece lays out the real differences: guarantees, cost structure, flexibility, and crediting, then tells you honestly which fits whom.

- Whole life guarantees cash value growth and a level cost of insurance; IUL guarantees only a floor on the index credit, not the crediting rate.

- IUL uses an increasing cost of insurance that rises with age, which can pressure cash value in later years if the policy is underfunded.

- IUL offers premium flexibility and index-linked upside, but caps that upside and shifts ongoing management onto the policyholder.

- For a cash-value banking strategy, predictability matters more than projected upside, which is why BetterWealth defaults to whole life.

- IUL can fit a buyer who wants index exposure, will fund the policy adequately, and will monitor it over time.

- The And Asset rule governs either product: only borrow when the deployed return clears the carrier's loan cost.

01 / The problemWhat this comparison actually has to solve

This comparison has to solve for the gap between what an illustration shows and what a contract guarantees, because that gap is where buyers get hurt. Both products are permanent life insurance with a cash value component, and both are sold with illustrations that project decades of growth. The projections look similar on the surface. The mechanics underneath them are not similar at all.

The deeper problem is that the two products are often sold by people with a reason to prefer one. Whole life agents lead with guarantees. IUL agents lead with the higher projected number and the market-linked story. Neither pitch tells you the part that matters most: which numbers are contractual and which can move against you after the ink dries. A real comparison strips the sales framing off both and looks at the structure.

The product with the bigger illustration is not the better product. It is usually the one with more assumptions baked in, which means more ways for reality to fall short of the page.

02 / GuaranteesHow do the guarantees actually differ?

Whole life guarantees the cash value and the cost structure; IUL guarantees only a floor on the index credit, which is a much narrower promise. This is the single biggest structural difference between the two, and most comparisons skim past it.

A whole life policy from a mutual carrier guarantees a minimum cash value at every point in the contract, a level premium that never rises, and a level cost of insurance. On top of those guarantees, the carrier pays non-guaranteed dividends, which a healthy mutual has often paid every year for a century or more. The policy compounds at the dividend rate net of mortality and expense charges, not at the gross dividend rate. The guaranteed floor is the contract. The dividend is the upside.

An IUL works in reverse. The guaranteed piece is a floor on the indexed credit, commonly 0 to 1%, which means the indexed account will not be credited a negative return when the market falls. That floor sounds like safety, and in a crash it helps. But the crediting rate above the floor is not guaranteed, the cap on the upside is set by the carrier and can be lowered, and the cost of insurance is deducted from cash value every year regardless of how the index performed. A 0% credit in a year when internal costs are rising means cash value goes down, not sideways.

Why the floor is not the same as a guarantee

A floor protects the index credit. It does not protect your cash value. In a flat or down market, the indexed account earns its floor while the increasing cost of insurance and policy charges keep coming out. The floor stops market losses from hitting the credit. It does not stop internal costs from eroding the balance. That distinction is the one IUL buyers most often miss.

A floor on the credit is not a floor on the account.

03 / Cost structureLevel cost versus increasing cost of insurance

Whole life uses a level cost of insurance and IUL uses an increasing one, and that single design choice drives most of the long-term divergence between the two. It is the least exciting part of the comparison and the most consequential.

In a whole life policy, the cost of insurance is leveled and locked into a fixed premium. You pay the same amount every year, and the internal charge for the death benefit does not climb as you age. The carrier prices for your whole life up front. That is why the premium is higher early: you are pre-funding the cost that a term-style product would charge you later.

In an IUL, the cost of insurance is the actual annual cost of the death benefit at your current age, and that cost rises every year. Early on, when you are young, it is cheap, which is part of why IUL illustrations look attractive and why the premium can start lower. Later, as the per-thousand cost of insurance climbs into your 60s, 70s, and beyond, those charges can become a real drag on cash value. If the policy is funded well and the cash value is large, it absorbs the rising cost. If the policy is underfunded or crediting underperforms, the increasing cost of insurance can outrun the growth and force higher premiums or, in a worst case, a lapse.

An IUL is cheap when you are young and the cost of insurance is low. The bill for the death benefit does not disappear. It is deferred, and it grows. Whether that matters depends entirely on how the policy is funded.

04 / FlexibilityWhere IUL has a real advantage

IUL's genuine advantage is flexibility: you can vary the premium within limits, and you get index-linked growth without being directly invested in the market. For the right buyer, that flexibility is worth something real.

With an IUL, you can fund more in a strong cash-flow year and less in a tight one, as long as you keep enough in the policy to cover the increasing cost of insurance and avoid a lapse. The cash value tracks an index, often the S&P 500 price index, subject to the cap and participation rate, so you get some of the upside of a rising market with a floor against a falling one. You are not buying the index. You are buying a crediting formula tied to it.

Whole life is the opposite on flexibility. The premium is fixed. You commit to it, and that commitment is the discipline that produces the guarantees. A well-built whole life policy does add funding flexibility through a paid-up additions rider, which lets you overfund within IRS limits to accelerate cash value. But the base premium is not optional. If rigid commitment is a problem for your cash flow, that is a genuine point in IUL's favor, and an honest comparison says so.

For the full mechanics of how indexed crediting, caps, and the increasing cost of insurance interact, we wrote a dedicated explainer on how indexed universal life insurance actually works. Read that alongside this comparison if IUL is on your short list.

Flexibility is a feature. It is also a responsibility.

05 / PredictabilityWhy does predictability win for a banking strategy?

Predictability wins for a cash-value banking strategy because the entire strategy depends on borrowing against a known value and repaying on a known schedule. Variability in the cash value is not a feature here. It is a risk to the plan.

Think about what a banking strategy actually requires. You build cash value, you borrow against it for a productive use, and you repay from the cash flow that use generates. Every step assumes you know roughly what the cash value will be and what it costs to borrow against it. Whole life delivers that. The guaranteed cash value gives you a known collateral base. The level cost of insurance means the policy's internal cost does not surprise you in year 25. The dividend adds to the base without ever subtracting from the guarantee.

An IUL introduces variables exactly where a banking strategy wants certainty. The crediting rate moves. The cap can be lowered. The cost of insurance rises. A few low-credit years against rising internal costs can leave the cash value below where the illustration projected, right when you were counting on it as collateral. None of that makes IUL a bad product. It makes IUL a poor match for a strategy whose whole premise is reliable access to a predictable asset.

We go deeper on the case for the whole life side, including the honest objections, in our honest answer on whether whole life insurance is worth it. If you are weighing the whole life half of this decision, start there.

IUL is not built to be a predictable collateral base, and that is fine. It was built for index-linked accumulation. Asking it to anchor a borrowing strategy is asking it to do a job it was not designed for.

06 / The frameworkWhat The And Asset says about both products

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base, and it applies one rule to any product you borrow against. Whatever you deploy the borrowed capital into must produce a return greater than the carrier's loan cost. If it does not, you do not borrow.

The And Asset is built on Nelson Nash's foundation. Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker, and his core insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with a discipline Nash's broader teaching does not enforce.

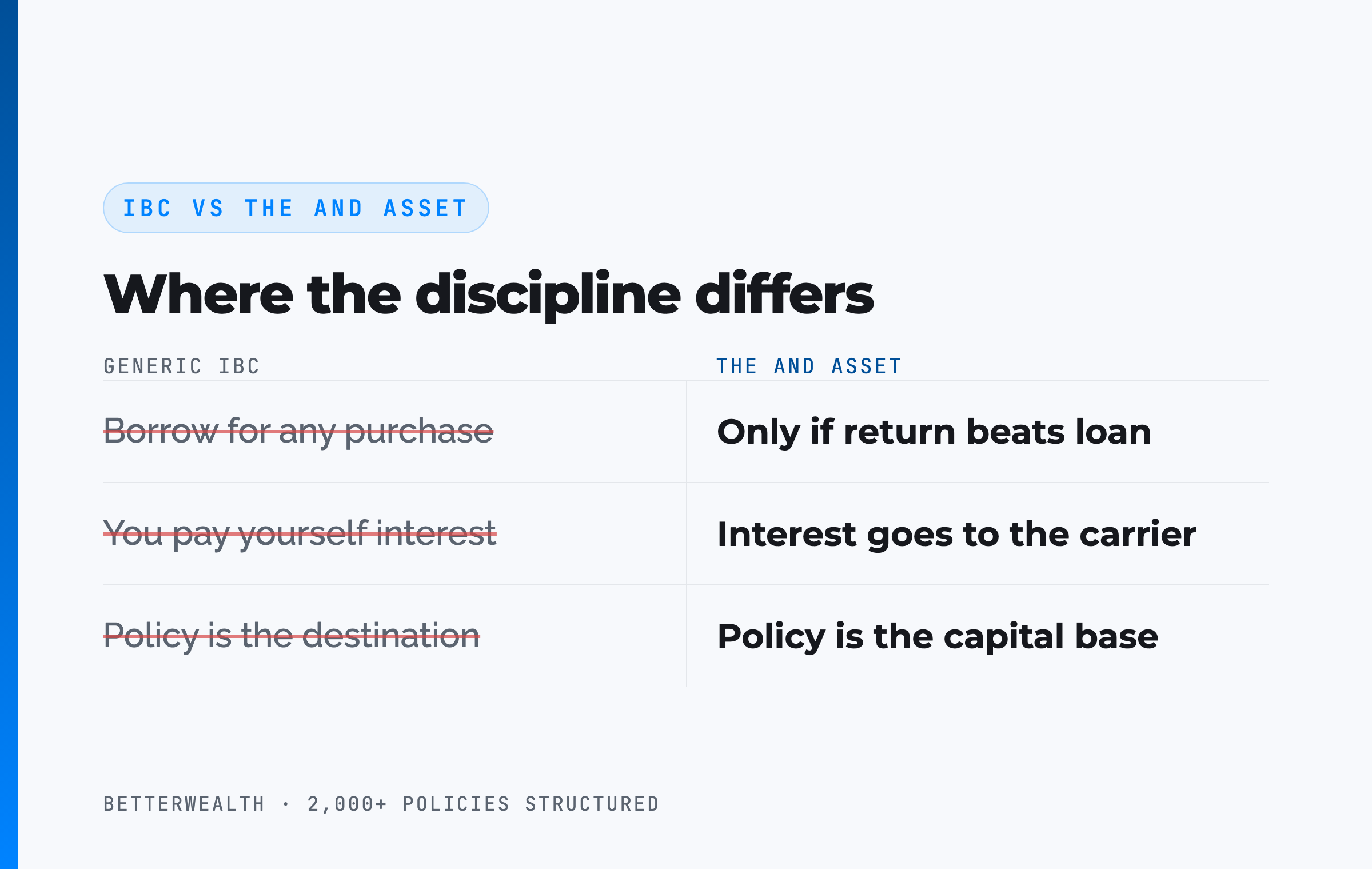

Where IBC ends and The And Asset begins

IBC says you can use a cash value policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges. The discipline of repayment is the whole strategy.

This framework is why product choice matters so much for our clients. The And Asset rewards a predictable collateral base, which is why we default to whole life. The rule itself does not change with the product. Whether you hold whole life or IUL, if you cannot name a use for the capital that beats the loan cost, do not borrow.

The math has to work. Every time.

The product depends on the job you need it to do.

Whole life fits you if

- You want a predictable cash value to borrow against

- You value guarantees over projected upside

- You can commit to a fixed premium

- You are running a cash-value capital strategy

IUL may fit you if

- You want index-linked upside with a floor

- You need premium flexibility year to year

- You will fund and monitor the policy actively

- You accept non-guaranteed crediting

If you are not sure which column you are in, a 30-minute conversation will tell you which product fits your plan, or whether neither does. We will tell you that too.

Book a Discovery Call07 / The mathDoes the return clear the carrier's loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow against either product. This is the test that decides whether a cash value policy is doing two jobs or just one expensive one.

Policy loan rates vary by carrier and by the rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat any specific number as a variable to verify with the carrier, not a constant. Here is the structure of the decision. You borrow at the carrier's loan rate. The policy keeps compounding on its full cash value while the loan is outstanding. Your deployed capital earns its own return. If that return clears the loan cost, you are ahead on the spread, and the same dollar has done two jobs. If it does not, you have borrowed money to lose money slowly.

The product affects the reliability of this math, not the rule. Whole life gives you a guaranteed collateral base, so you know what you are borrowing against. With an IUL, the collateral base can move with crediting and rising costs, which makes the spread harder to count on. The discipline is identical. The certainty underneath it is not.

If the deal does not clear the loan rate, do not borrow.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare products like whole life and IUL for real clients. Free, email-gated, no spam.

Open the Vault08 / Where people get this wrongThe marketing traps on both sides

Buyers get burned on both sides of this comparison, and the traps are mirror images of each other. Knowing them is the fastest way to read any illustration honestly.

The IUL trap is the maximum-illustrated rate. An IUL sold at its highest allowable illustrated crediting rate looks spectacular, because the upside is projected and the increasing cost of insurance looks small at the front. The fix is simple: ask for the policy run at the guaranteed rate and at a conservative rate, then look at how it holds up in the later years when the cost of insurance has climbed. If it only works at the maximum rate, it does not work.

The whole life trap is the opposite. Some agents quote the gross dividend rate as if it were your growth rate. It is not. Your cash value grows at the dividend net of mortality and expense charges, which is a lower number. Anyone quoting the gross rate as your return is either careless or selling. And no honest whole life illustration shows cash value exceeding cumulative contributions in the first few years. Break-even lands at year 5 or later for a healthy individual. Any illustration showing year-one or year-two break-even is fiction.

Marketers have ruined how both of these products get explained. The honest version is less exciting and far more useful: read the guaranteed column, not the projected one.

09 / Head to headIUL vs whole life, side by side

Compared directly, whole life trades flexibility and projected upside for guarantees and predictability, while IUL trades guarantees for index-linked growth and funding flexibility. The table sets them against each other on the four dimensions that decide the choice.

| Dimension | Whole Life | Indexed Universal Life (IUL) |

|---|---|---|

| Guarantees | Guaranteed cash value and level premium, plus non-guaranteed dividends on top | Floor on the index credit (often 0 to 1%); crediting rate and cap not guaranteed |

| Cost of insurance | Level for life, built into a fixed premium | Increases every year with age; cheap early, climbs later |

| Premium flexibility | Fixed base premium; overfund via paid-up additions rider within limits | Flexible within limits; vary funding year to year |

| Growth driver | Dividends net of mortality and expense charges; predictable | Index-linked credit, capped on the upside, floored on the downside; variable |

| Best fit | Predictable capital base for a banking strategy | Index-linked accumulation with active funding and monitoring |

| Tax treatment | Loans not taxable income under IRC 7702 | Loans not taxable income under IRC 7702 |

Guarantees. Whole life puts the guarantee in the contract and the upside in the dividend. IUL puts the guarantee in a floor on the credit and leaves the growth rate and cap to the carrier and the market. If you want to know what the policy will be worth, whole life answers more of that question in writing.

Cost and flexibility. IUL wins on flexibility and starting cost. Whole life wins on cost certainty over a lifetime. The increasing cost of insurance is IUL's hidden variable, and the fixed premium is whole life's hidden discipline. Which one is an advantage depends on your cash flow and your time horizon.

Fit for a capital strategy. For The And Asset, predictability is the deciding factor, and whole life provides it. IUL can build cash value and can be borrowed against, but the variability that makes it attractive for accumulation works against a strategy built on reliable collateral. Match the product to the job.

A composite: the buyer who almost chose on the illustration

Consider a 43-year-old business owner, preferred non-tobacco, deciding between a whole life policy funded at $48,000 per year and an IUL pitched at a similar outlay. This is a representative composite, not a single named client.

The IUL illustration, run at its maximum allowable rate, showed a larger year-30 number than the whole life policy. Run at the guaranteed rate, the same IUL showed the increasing cost of insurance eating into cash value in the later years and required higher premiums to stay in force. The whole life policy showed the same modest guaranteed column whether the market cooperated or not.

This owner needed the policy as a capital base, not an accumulation bet. Through the first three years, the whole life cash value trailed cumulative contributions, exactly as a real policy should. By year three, each premium dollar added more than a dollar of cash value. At year five, total cash value crossed total contributions. No earlier.

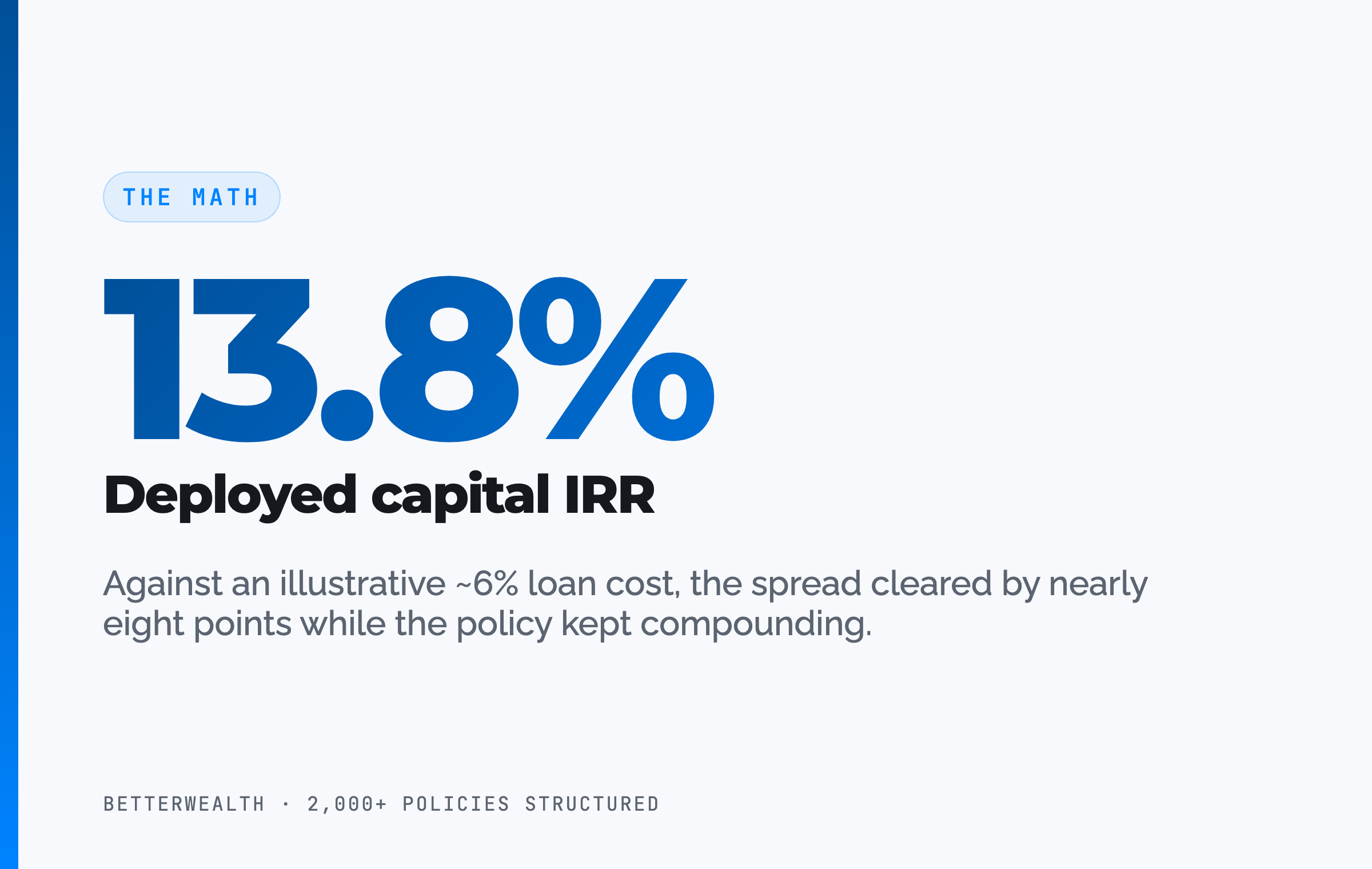

In year seven, with roughly $352,000 of accessible cash value, the owner borrowed $164,500 against the policy to fund an inventory expansion. The expansion returned an estimated 13.8% IRR. The loan cost was illustrative at around 6%, so the spread worked in the owner's favor by nearly eight points. The policy kept compounding on its full value the entire time. Repayment ran on a 38-month schedule funded by the expansion's own cash flow. The predictable collateral base is what made the decision to borrow a calculation instead of a gamble.

One dollar. Two jobs. That is the And.

10 / The fitWho should choose which, honestly

Choose whole life when you need a predictable capital base and you value guarantees over projected upside, and choose IUL when you want index-linked growth and will actively fund and monitor the policy. That is the honest split, and it holds for most people.

Whole life is the right tool for the entrepreneur or high-income earner building a cash-value capital strategy, who will commit to a fixed premium, who plans to borrow against a known value, and who wants the policy to behave the same way in year 25 as the contract promised in year one. It is the default for The And Asset because the strategy depends on the predictability whole life provides.

IUL is the right tool for a buyer who wants index exposure with downside protection, who values the ability to flex premiums, who will keep the policy funded enough to absorb the rising cost of insurance, and who will read the illustration again every few years instead of filing it away. It also shows up in some estate and large-death-benefit planning where the flexible structure fits. The buyer has to accept the variables. An IUL is something you manage. It is not set and forget, and any pitch that frames it that way is selling, not advising.

FAQIUL vs whole life questions

What is the difference between IUL and whole life insurance?

Whole life insurance guarantees cash value growth, a level premium, and a level cost of insurance, with non-guaranteed dividends on top. Indexed universal life ties cash value growth to an index with a cap and a floor, uses a flexible premium and an increasing cost of insurance, and does not guarantee the crediting rate. Whole life is predictable; IUL trades predictability for index-linked upside.

Is IUL or whole life better for infinite banking?

For a cash-value banking strategy, properly designed whole life is the more predictable base because its guaranteed cash value and level cost of insurance make the loan-and-repay math reliable. IUL can be used, but its non-guaranteed crediting and increasing cost of insurance add variables that work against a strategy built on borrowing against a known value.

Does IUL have guaranteed cash value?

IUL guarantees a floor on the index credit, commonly 0 to 1%, so the indexed account does not lose value to market declines. It does not guarantee the crediting rate above that floor, and the increasing cost of insurance is deducted from cash value every year, so total cash value can decline if the policy is underfunded or crediting is low.

What is the cost of insurance difference between IUL and whole life?

Whole life uses a level cost of insurance built into a fixed premium, so the internal charge does not rise as you age. IUL uses an increasing cost of insurance that rises every year with your age, which is inexpensive early and can become a meaningful drag on cash value in later years if the policy is not funded to absorb it.

Can you lose money in an IUL?

The indexed account of an IUL will not be credited below its floor in a down market, but cash value can still decline because the increasing cost of insurance and policy charges are deducted regardless of crediting. In a string of low-credit years against rising internal costs, an underfunded IUL can lose cash value and, in a worst case, lapse.

Why does BetterWealth favor whole life for a capital strategy?

BetterWealth favors properly designed whole life for a cash-value capital strategy because predictability is the point. The And Asset depends on borrowing against a known cash value and repaying on a known schedule. Whole life's guaranteed cash value, level cost of insurance, and contractual floor make that math reliable. IUL can fit, but it adds variables a borrowing strategy does not need.

When does IUL make sense over whole life?

IUL can fit a buyer who wants index-linked upside, values premium flexibility, will keep the policy adequately funded, and will monitor the illustration over time. It is also used for some estate and high-death-benefit cases. The buyer has to accept non-guaranteed crediting and an increasing cost of insurance, and treat the policy as something to manage, not set and forget.

Is whole life or IUL more expensive?

Whole life carries a higher fixed premium for the same death benefit because more of the cost is guaranteed and level. IUL usually starts cheaper because its cost of insurance is low early and the premium is flexible. Over a full lifetime the comparison narrows, because IUL's increasing cost of insurance climbs while whole life's stays level.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Can I convert or roll an IUL into a whole life policy?

You cannot convert an existing IUL into a whole life policy, but you can apply for a new whole life policy and, in some cases, move cash value through a 1035 exchange. A 1035 exchange can carry tax basis without triggering a taxable event, but surrender charges, new underwriting, and a fresh cash value timeline apply, so it only makes sense after a careful review.

The honest 30 minutes about which product fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen this decision go both ways. On a discovery call, a practitioner looks at your specific situation and tells you whether whole life, IUL, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call- Nelson Nash, Becoming Your Own Banker. The origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law). The tax code provision behind the tax treatment of cash value and policy loans for both whole life and IUL.

- NAIC. Model regulations and consumer guidance on life insurance illustrations, including indexed universal life.

- LIMRA. Life insurance industry data on product sales, persistency, and lapse benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether whole life, IUL, or neither fits your plan, book a discovery call. We will tell you if it does not.