.png)

IUL pros include index-linked growth with a floor that blocks market losses, flexible premiums, tax-deferred cash value, and tax-favored loan access. The cons are caps and participation rates the carrier can lower, a cost of insurance that rises with age, illustration risk because the projected rate is not guaranteed, surrender charges, and lapse risk if the policy is underfunded.

An indexed universal life illustration is the most persuasive sales document in the insurance industry, and that is exactly the problem. It shows a smooth line climbing for forty years at a rate the agent picked, a death benefit that never wavers, and cash value that looks like a brokerage account with a safety net bolted on. Almost none of it is guaranteed, and the parts that are guaranteed live in a column the agent rarely turns to.

An IUL is not good or bad. It is a contract with real advantages and real costs, and whether it works depends entirely on how it is funded and which assumptions hold. The pros are genuine. The cons are genuine too, and most of them are mechanical features the illustration is allowed to project around. A reader being pitched deserves both halves of that ledger, side by side, with the math intact.

At BetterWealth, we have structured more than 2,000 policies across all 50 states. We design most client capital strategies on whole life, and we will explain why below, but we are not here to tell you an IUL is a scam. It is a tool. This breakdown covers the four pros that are real, the five cons illustrations tend to hide, the difference between the illustrated rate and the guaranteed one, and a step-by-step way to stress-test any IUL illustration before you sign it. We will also tell you who an IUL is wrong for.

- IUL upside is real: a 0% (or low) floor blocks index losses while credits track an index up to a cap.

- Caps and participation rates are not contractually fixed. The carrier can lower them on renewal.

- The illustrated rate is a projection, not a promise. Only the guaranteed column is contractual.

- Cost of insurance rises with age and is pulled from cash value, which can drain an underfunded policy.

- An underfunded IUL can lapse late in life, and a lapse with gains can trigger a tax bill.

- Stress-test every illustration: read the guaranteed column, re-run at a lower rate, model a cap cut.

01 / The problemWhy an IUL illustration is the wrong place to make this decision

The illustration is a marketing projection dressed as a financial statement, and treating it as a forecast is the single most common mistake buyers make. It is built on a credited rate the agent selects, caps the carrier can change, and a cost structure that climbs every year. Move any one of those inputs and the smooth forty-year line bends sharply.

If you want to understand the mechanics underneath that projection before you weigh the tradeoffs, start with our explainer on how indexed universal life insurance actually works. This piece assumes you know the basics and want the honest ledger. The point here is simple: an IUL can be a reasonable contract or a fragile one, and the difference is buried in details the sales conversation skips.

The illustration is not a forecast. It is a sales tool with a non-guaranteed column the size of a billboard and a guaranteed column nobody reads.

02 / The prosWhat does an IUL actually do well?

An IUL does four things well, and they are the reasons it sells. Each one is real. Each one also carries a string attached that the next section will pull on.

Index-linked upside with a floor

The headline feature is asymmetric crediting. Your cash value earns interest tied to the movement of an index like the S&P 500, up to a cap, and a floor (usually 0%) protects you in a down year. You are not invested in the market. You hold an insurance contract whose interest is calculated from an index formula. In a strong year the cap limits your gain. In a crash the floor blocks the loss. For someone who wants equity-flavored growth without sequence-of-returns risk, that structure has appeal.

Premium flexibility

An IUL sits on a universal life chassis, which means the premium is adjustable within limits. Pay more in a strong income year, pay less in a lean one, skip a payment if the cash value can cover the charges. Whole life does not bend this way. For an entrepreneur with uneven cash flow, that flexibility is a genuine advantage.

Tax-deferred growth and tax-favored access

Cash value grows tax-deferred inside the policy under the rules of IRC Section 7702. Properly structured and kept inside the limits that avoid a Modified Endowment Contract, you can access cash value through policy loans that are not treated as taxable income. The death benefit passes to heirs income-tax-free. These tax features are the same ones that make any permanent life policy useful as a capital tool. They are not unique to IUL, but they are real.

The pros are not the question. The durability is.

03 / The consWhat do most IUL illustrations hide?

The cons of an IUL are mostly structural, which is why illustrations can project right past them. Here are the five that decide whether a policy thrives or quietly fails, and none of them shows up on the glossy first page.

Caps and participation rates the carrier can lower

The cap is the ceiling on your index credit, and the participation rate is the percentage of the index gain you receive. Neither is locked for the life of the contract on most IUL designs. The carrier can lower them at renewal, subject only to a contractual minimum that often sits far below the rate you were illustrated. A policy sold on a 9% cap can be servicing a 6% cap a decade later, and the illustration that sold you assumed the higher number the whole way.

A cost of insurance that climbs with age

The internal cost of insurance in an IUL is not level. It rises as you age, and on a universal life chassis those charges are deducted from your cash value every year. While the policy is young and crediting is strong, the rising cost is invisible. Later in life, if credits underperform the illustration or you stop funding, the climbing cost can eat into cash value faster than interest replaces it. This is the mechanism behind most IUL horror stories.

Illustration risk: the rate is not guaranteed

The credited rate on the illustration is an assumption, not a contract. Actuarial Guideline 49 exists precisely because carriers were illustrating rates high enough to mislead, and it caps how optimistic the projection can be. Even within those limits, the illustrated rate is a number the agent chose. The only figures the carrier is bound to are in the guaranteed column, which shows maximum charges and minimum interest. Read that column and you are reading the actual promise.

Surrender charges

Cancel an IUL in the early years, or pull cash value above a set amount, and the carrier deducts a surrender charge. The schedule often runs 10 to 15 years and declines over time. During that window, the cash value you can actually access is lower than the account value on your statement. Buy an IUL, change your mind in year four, and you learn what the surrender schedule costs.

Lapse risk if the policy is underfunded

This is the one that turns a tax-advantaged plan into a tax bill. Because the chassis carries rising costs, an underfunded IUL can run out of cash value to cover its own charges and lapse, sometimes decades after issue. If the policy lapses with an outstanding loan or accumulated gains, the IRS can treat the forgiven loan and gains as taxable income. The policy you bought for tax efficiency hands you a bill in your seventies.

A 0% floor does not mean you cannot lose money. The index credit holds at zero in a flat year. The policy charges come out anyway.

04 / How to stress-testHow do you pressure-test an IUL illustration before you sign?

You stress-test an IUL by attacking the assumptions the illustration depends on, one at a time, and watching whether the policy still works. A design that only survives at the maximum illustrated rate is a design built on hope. Run these five steps with the agent in the room.

- Read the guaranteed column first. Ignore the non-guaranteed projection for a moment. Find the column built on maximum charges and minimum credited interest. If the policy collapses there, you are buying a best-case scenario the carrier never promised.

- Re-run at a lower crediting rate. Ask for the same design illustrated at two to four points below the headline rate. If a 7% illustration only stays in force at 7%, it is fragile. A sound design degrades gracefully, it does not fall off a cliff.

- Model a cap reduction. Ask what happens if the cap drops to the contractual minimum. The carrier controls that lever, so you should see the downside before you trust the upside.

- Trace the cost of insurance at older ages. Look at the per-year charges at ages 70, 80, and 90. Confirm the cash value can absorb them under a conservative crediting rate, not just the illustrated one.

- Confirm funding versus the minimum to stay in force. Compare the premium you actually plan to pay against the minimum needed to keep the policy alive. The gap between those two numbers is your margin of safety. A thin margin is how lapses happen.

If the agent resists running any of these, that resistance is your answer. A policy that holds up under pressure is one an honest agent will happily stress-test in front of you.

If it only works at the top rate, it does not work.

An IUL fits a specific person with specific expectations.

It can fit you if

- You want index-linked upside with a downside floor

- Your income is uneven and you value premium flexibility

- You will fund it well above the minimum, for decades

- You understand the rate is a projection, not a promise

It does not fit you if

- You want contractual guarantees you can count on

- You will fund only the minimum premium

- You are building a borrowing strategy on predictable mechanics

- You were sold on the illustrated rate alone

If you are in the first column, the design and funding discipline are everything. If you are in the second, a guaranteed structure is probably the better fit, and we will tell you so plainly.

Book a Discovery Call05 / The frameworkWhere The And Asset lands on IUL

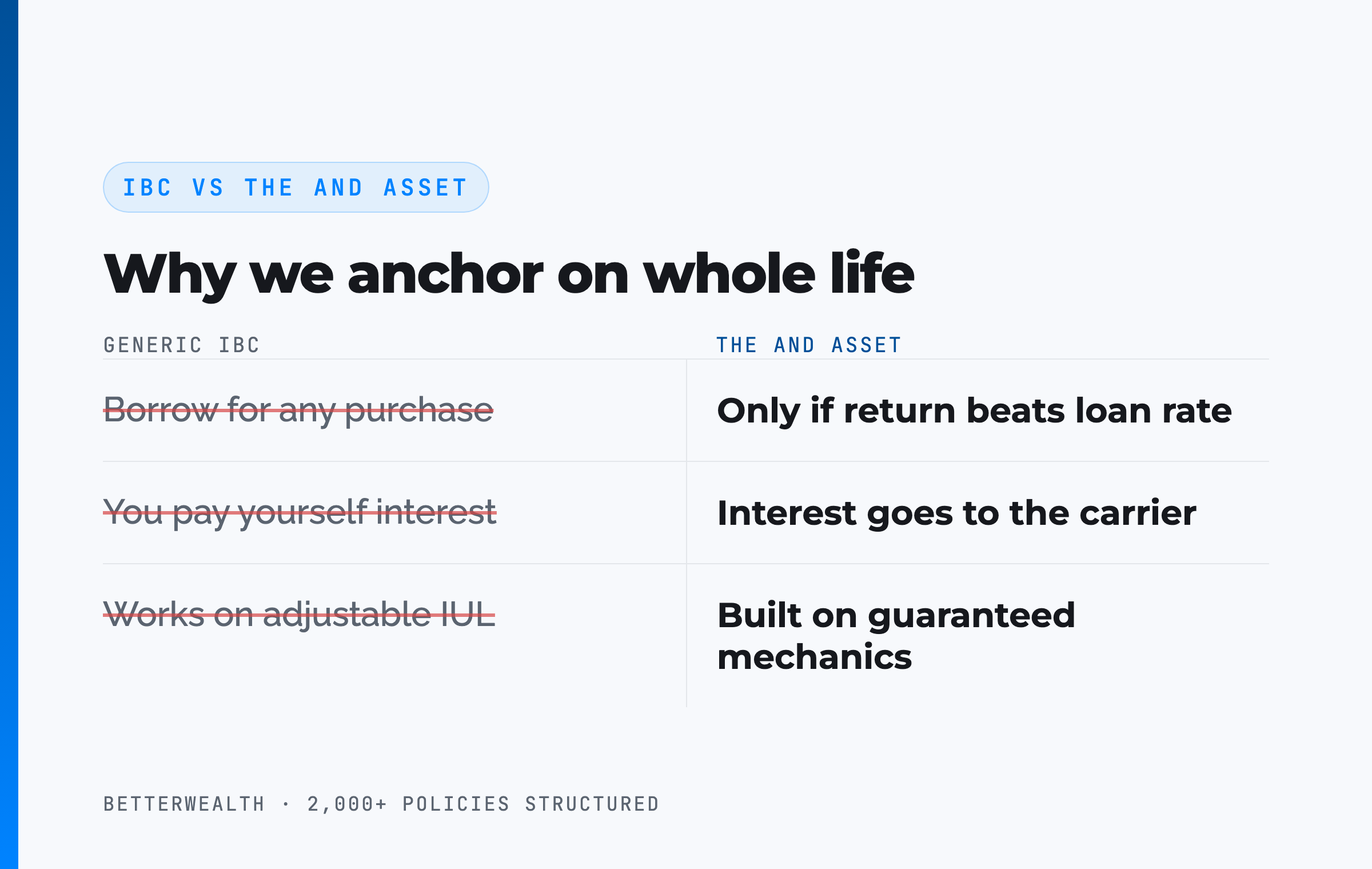

The And Asset is built on whole life, not IUL, and the reason is the same reason this whole article exists: a capital strategy depends on mechanics you can predict. The And Asset is BetterWealth's framework for using a properly structured cash value policy as a capital base you borrow against, while the policy keeps compounding. Nelson Nash pioneered the idea of using life insurance as a personal banking system in Becoming Your Own Banker. We respect that foundation. The And Asset builds on it with one rule his broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a cash value policy as a personal bank for any purchase. The And Asset says you only deploy capital when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. That discipline is the entire strategy. And it depends on knowing, in advance, what your policy will grow at and what your loan will cost.

This is where IUL and whole life part ways for our purposes. Some marketers sell IUL as a higher-octane banking policy by pointing at its illustrated rates. The problem is that the loan math behind the strategy needs predictable inputs, and an IUL's adjustable caps, variable crediting, and rising cost of insurance introduce variables that a contractually guaranteed whole life design does not. We are not saying an IUL cannot grow cash value. We are saying we will not anchor a multi-decade borrowing strategy to a number the carrier can change. If you are weighing the two structures directly, our honest comparison of IUL versus whole life insurance walks through the tradeoffs line by line.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest on a policy loan. You are paying the carrier, and your return comes from what you deploy the capital into.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and stress-test checklists we use when we compare policy structures like IUL and whole life. Free, email-gated, no spam.

Open the Vault06 / The mathDoes the deployed return clear the loan cost?

Whatever you borrow against a cash value policy for, the return on the deployed capital must exceed the carrier's loan cost, or you should not borrow. This is the test that governs The And Asset regardless of policy type. Loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with the carrier, not a constant.

The structure of the decision is the same on any permanent policy. You borrow at the carrier's loan rate. The policy keeps compounding on its value. Your deployed capital earns its own return. If that return clears the loan cost, the same dollar has done two jobs and you are ahead on the spread. If it does not, you have borrowed money to lose money slowly. With an IUL, the added wrinkle is that the policy's own growth, the cost side of your spread, is less predictable than it would be under a guaranteed design. That uncertainty is a cost in itself.

If the deal does not clear the loan rate, do not borrow.

07 / Head to headIUL against whole life and a brokerage account

Compared with the alternatives an entrepreneur actually weighs, an IUL trades guarantees for upside potential and trades simplicity for flexibility. The table sets it against a guaranteed whole life design and a taxable brokerage account on the dimensions that decide whether a policy can anchor a capital strategy.

| Dimension | Indexed Universal Life | Whole Life (And Asset) | Taxable Brokerage |

|---|---|---|---|

| Growth | Index-linked, capped, with a floor; rate not guaranteed | Guaranteed cash value plus a dividend, net of internal costs | Full market growth and loss, no floor |

| Guarantees | Minimal; caps, participation, and costs can change | Contractual; guaranteed values and loan provisions | None; you bear all market risk |

| Cost structure | Cost of insurance rises with age, pulled from cash value | Level premium; internal costs built into the design | Fund and advisory fees, taxed on gains yearly |

| Loan mechanics | Available, but growth backing the loan is variable | Predictable; loan cannot be called, terms you set | Margin loans can be called; no policy loan feature |

Growth and guarantees. An IUL offers more upside than whole life in a strong index run, capped, with a floor. Whole life offers less ceiling and a contractual floor you can build a plan around. The brokerage offers the most upside and the least protection. None is best in the abstract.

Cost structure. The rising cost of insurance is the IUL's defining long-term risk. Whole life folds its costs into a level premium, which is why its cash value timeline is predictable: it does not exceed cumulative contributions before year four, with break-even at year five or later for a healthy individual.

Loan mechanics. For a borrowing strategy, predictability is the whole game. Whole life's guaranteed values and non-callable loans give the math a fixed footing. An IUL can be borrowed against too, but the growth backing the loan moves with caps and crediting, which is why we anchor The And Asset on whole life.

A composite: the founder who stress-tested the illustration first

Consider a 43-year-old founder, preferred non-tobacco, who came to us holding an IUL illustration from another agent showing cash value growing at a credited 6.9% for life. This is a representative composite, not a single named client.

The original illustration showed the policy thriving for forty years. When we re-ran the identical design at 4.4%, two and a half points below the headline rate, and held the premium at the minimum the buyer had been told was "flexible," the cash value started losing ground to the rising cost of insurance around year fourteen and trended toward a lapse in the policyholder's late seventies. The floor never failed. The charges did the damage.

The fix was not to throw the IUL out. It was to fund it well above the minimum and accept the surrender schedule honestly: year-one accessible cash value of $33,800 against $47,000 contributed, with break-even on accessible value landing at year five, not the year-two crossover the first agent implied. Funded with discipline and stress-tested at a conservative rate, the policy held. The lesson was the process, not the product.

The floor held. The funding is what saved it.

The honest 30 minutes about whether an IUL fits you.

We have structured more than 2,000 policies across all 50 states. We have seen IULs work when funded with discipline, and we have seen them fail when sold on the illustration alone. On a discovery call, a practitioner looks at your situation and tells you whether an IUL, a whole life design, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQIUL pros and cons questions

What are the main pros and cons of an IUL?

The pros of an IUL are index-linked growth with a floor that protects against market losses, flexible premiums, tax-deferred cash value, and tax-favored access through loans. The cons are caps and participation rates the carrier can lower, a cost of insurance that rises with age, illustration risk because the illustrated rate is not guaranteed, surrender charges, and lapse risk if the policy is underfunded.

Is the IUL illustrated rate guaranteed?

No. The illustrated rate in an IUL is a projection, not a guarantee. Index credits depend on caps and participation rates the carrier can change, and Actuarial Guideline 49 limits how high carriers may illustrate. Only the guaranteed column, which shows minimum interest and maximum costs, reflects what the carrier is contractually obligated to deliver.

Can an IUL lose money?

An IUL's index credit usually cannot fall below a 0% floor, so a down market year credits zero rather than a loss. Cash value can still decline, because policy charges and the cost of insurance are deducted every year, including flat years. Over several low-credit years, those charges can erode cash value even though the index floor held.

Why does the cost of insurance matter in an IUL?

The cost of insurance in an IUL is not level. It rises as you age, and on a universal life chassis those rising charges are pulled from your cash value. If crediting underperforms the illustration or you stop funding, climbing costs can drain the cash value and put the policy at risk of lapsing later in life.

How do you stress-test an IUL illustration?

Read the guaranteed column first, then ask the agent to re-illustrate at a credited rate two to four points below the headline number, model what happens if the cap is lowered, trace the cost of insurance at older ages, and confirm the planned premium against the minimum needed to keep the policy in force. A design that only works at the maximum illustrated rate is fragile.

What are surrender charges on an IUL?

Surrender charges are fees the carrier deducts if you cancel an IUL or withdraw above a set amount during the early years, often a schedule that runs 10 to 15 years and declines over time. They exist to recover the carrier's upfront costs. During the surrender period, the cash value you can actually access is lower than the account value shown on the statement.

Can an IUL lapse?

Yes. Because an IUL sits on a universal life chassis with rising costs, an underfunded policy can run out of cash value to cover its charges and lapse, often decades after issue. A lapse with an outstanding loan or gains can also create a taxable event, turning a tax-advantaged plan into a tax bill at the worst possible time.

Is an IUL better than whole life insurance?

Neither is universally better. An IUL offers more upside potential and premium flexibility, with non-guaranteed caps and a rising cost structure. Whole life offers contractual guarantees, a dividend net of internal costs, and predictable loan mechanics, with less upside. The right choice depends on what the policy needs to do and how much you value guarantees over potential.

Is an IUL good for infinite banking?

Some marketers sell IUL as a higher-return version of infinite banking, pointing to its illustrated rates. The math behind a borrowing strategy depends on predictable loan and growth mechanics, and an IUL's adjustable caps, variable crediting, and rising costs introduce variables that a guaranteed whole life design does not. For The And Asset, we build the capital base on whole life for that reason.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured cash value life insurance policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. We build it on whole life because the strategy depends on contractual guarantees.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a cash value policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- NAIC, Actuarial Guideline 49 and consumer guidance on indexed universal life illustrations.

- LIMRA, life insurance industry data, including indexed universal life sales and persistency.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you are holding an IUL illustration and want an honest read on whether it holds up, book a discovery call. We will tell you if it does not.