.png)

Indexed universal life insurance (IUL) is permanent life insurance whose cash value is credited based on a market index like the S&P 500, with a cap that limits gains and a floor, usually 0%, that limits index losses. You are not invested directly in the market, and the cost of insurance rises with age.

Most people meet indexed universal life through a one-page illustration with a single number on it, a projected rate of return that makes the columns climb in a smooth diagonal for forty years. That illustration is the product of assumptions, not a contract. The number sells the policy, and almost nothing about how the policy actually behaves shows up in the part of the page the buyer is looking at.

An IUL is a flexible-premium life insurance policy with a cash value that earns interest tied to an index, and the words "tied to" are doing more work than most agents admit. Your money is not in the market. The carrier credits you a rate based on how an index moves, then limits that rate on the top with a cap and protects it on the bottom with a floor. Both the cap and the cost of insurance can change after you sign.

At BetterWealth, we have structured more than 2,000 life insurance policies across all 50 states, and we get the IUL question constantly. Our designs are built on whole life, for reasons this article will make clear, but that does not make IUL a scam or a bad product. It makes it a different product with a different risk profile. The job here is to show you exactly how it works so you can judge it on the mechanics instead of the illustration.

This guide covers what an IUL is, how the index crediting actually credits, the four moving parts that decide whether the policy performs, the math that should govern any decision to borrow against it, and an honest comparison with whole life.

- An IUL credits cash value based on an index like the S&P 500, but your money is never invested directly in that index.

- A cap limits your upside and a floor, usually 0%, limits your downside, so flat or down index years credit little or nothing.

- The carrier can lower the cap and the participation rate after you buy, which is the risk illustrations rarely emphasize.

- The cost of insurance rises every year with age, and an underfunded IUL can drain itself and lapse.

- Illustrated rates are projections, not guarantees, so the gap between illustrated and actual results is the central IUL risk.

- IUL trades whole life's guarantees for index-linked upside and flexible premiums, which suits some buyers and not others.

01 / The problemWhy the illustration is the wrong place to start

The illustration is the wrong place to start because it shows one possible future as if it were the only one. An IUL illustration runs on an assumed crediting rate, an assumed cost-of-insurance schedule, and an assumed cap that holds for decades. Change any of those three, and the smooth diagonal bends. Real index returns are not smooth. Caps move. Costs rise.

This matters more for an IUL than for almost any other policy because the buyer is usually told to compare illustrated numbers across carriers, picking the one with the highest projected rate. That is the equivalent of choosing a flight by the cheapest fare on the screen before you read the fare rules. The headline number is real. What it costs you is in the fine print.

The illustrated rate is a sales tool, not a promise. A carrier can show you a beautiful projection and still lower your cap the year after you sign.

02 / The definitionWhat is indexed universal life insurance, really?

Indexed universal life insurance is permanent life insurance built on a universal life chassis, with a cash value that earns interest linked to the performance of a market index. It has three parts: a death benefit, a flexible premium, and a cash value that grows through index crediting rather than a fixed declared rate or a stock subaccount.

The universal life chassis is what gives an IUL its flexibility and its fragility. You can dial the premium up or down within IRS limits, and you can adjust the death benefit. The same flexibility means the policy does not enforce the funding discipline a whole life premium does. An IUL will let you underfund it, and an underfunded IUL is a policy quietly working against itself.

The "indexed" part is the crediting method. Instead of a guaranteed rate, the carrier ties your interest to an index like the S&P 500. You get a version of the index's movement, filtered through a cap, a floor, and a participation rate. We will take those apart in the next section, because they are the whole game.

How IUL differs from other universal life

IUL sits between two cousins on the universal life family tree. Fixed universal life credits a declared interest rate set by the carrier, with no index involved. Variable universal life invests your cash value directly in market subaccounts, so you take the real gains and the real losses. IUL splits the difference: index-linked crediting with a floor, but no direct market participation. You give up the full upside in exchange for the downside floor.

No direct market exposure. No guaranteed growth either.

03 / The mechanicsHow does an IUL credit interest?

An IUL credits interest by measuring how the chosen index moves over a segment, then applying a cap, a participation rate, and a floor to that movement. The carrier does not put your money in the index. It holds your cash value in its general account and buys options that pay off based on index performance, which is how it can offer a floor at all. Here is the sequence.

- Your premium is split. Each payment first covers the cost of insurance and policy expense charges. What remains becomes cash value available to be credited.

- Cash value is allocated to an index account. You choose one or more index strategies, most commonly tied to the S&P 500, sometimes with a point-to-point or monthly crediting method.

- The segment runs. Over a set period, usually a year, the carrier tracks the index from start to end. Dividends on the index are not included, which already separates your credit from the index's total return.

- The cap and participation rate limit the upside. If the index rises 14% and your cap is 9%, you are credited 9%. If your participation rate is below 100%, you receive only that share of the gain before the cap applies.

- The floor protects the downside. If the index falls, your index credit is the floor, usually 0%. You do not lose value to the index, but the cost of insurance and policy charges still come out, so your cash value can still go down in a flat year.

That last point is the one that surprises people. A 0% floor protects you from index losses. It does not protect you from the policy's own internal costs. In a year the index is flat and you are credited zero, the cost of insurance is still deducted, and your net cash value can fall.

The four levers the carrier controls

Four numbers decide what your IUL actually earns, and the carrier sets all four. The cap is the ceiling on your credit. The participation rate is the share of the gain you receive. The floor is your downside protection. The cost of insurance is what gets subtracted regardless. When an IUL underperforms its illustration, it is almost always because the carrier lowered the cap, raised the cost of insurance, or both, in a way the original illustration assumed would never happen.

You control the premium. The carrier controls the math.

04 / The risksThe four risks agents skip

Four risks decide whether an IUL performs as sold, and most sales conversations skip all four. We list them plainly because naming the tradeoffs is the honest way to explain any financial product. For the full inventory, our breakdown of IUL pros and cons covers what agents don't explain in more depth.

1. Cap and participation rate risk

The carrier can lower your cap and participation rate after you own the policy. The cap that made the illustration look strong is a current declared rate, not a guaranteed one. When carriers face pressure on their option budgets, caps come down across in-force books, and the policyholder absorbs it. Your upside shrinks and there is nothing in the contract that stops it.

2. Rising cost of insurance

The cost of insurance climbs every year as you age, because the insurer's risk of paying the death benefit climbs. In the early years this is manageable. In later years, on an underfunded policy, the annual charge can become large enough to consume the index credits and then start eating the cash value itself. This is the engine behind most IUL failures.

3. Illustration risk

Illustration risk is the distance between the projected rate and the realized rate. A policy illustrated at a high crediting rate that actually earns less over thirty years will hold far less cash value than the buyer was shown, and may require higher premiums later just to stay alive. The 2021 AG49-A regulation tightened illustration assumptions for exactly this reason, after a stretch of projections that did not hold up.

4. Lapse risk

An IUL can lapse and take your money and your coverage with it. If premiums and crediting do not keep pace with the rising cost of insurance, the policy borrows from its own cash value to stay in force, and that spiral can end in a lapse. A lapse with a large outstanding loan can also create a taxable gain, turning a coverage problem into a tax bill. Funding discipline is the only thing that prevents it.

An IUL is not "set it and forget it." It is a policy you have to keep funded and watch, because the costs inside it only go one direction.

IUL fits a specific person, and it is not most people.

It may fit you if

- You want flexible premiums and accept variable crediting

- You will fund it well above the minimum and monitor it

- You understand caps and the cost of insurance can move

- You want index-linked upside with a downside floor

It does not fit you if

- You want a guaranteed cash value you can count on

- You will fund only the minimum premium

- You were sold it as a market-beating investment

- You will not watch the policy after year one

If you are weighing an IUL against a whole life design, a 30-minute conversation will show you the difference on your own numbers. If you are in the right column, we will tell you that too.

Book a Discovery Call05 / The frameworkWhere IUL meets The And Asset

The And Asset is BetterWealth's framework for using a permanent policy as a capital base you borrow against, and it applies to an IUL only when the policy is funded and behaving like a capital base rather than a bet on caps. Nelson Nash pioneered the idea of using permanent life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule the broader teaching does not enforce.

IBC says you can use a permanent policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many marketers say you are paying yourself interest. You are not. The interest goes to the insurer. Your return is what your deployed capital earns elsewhere.

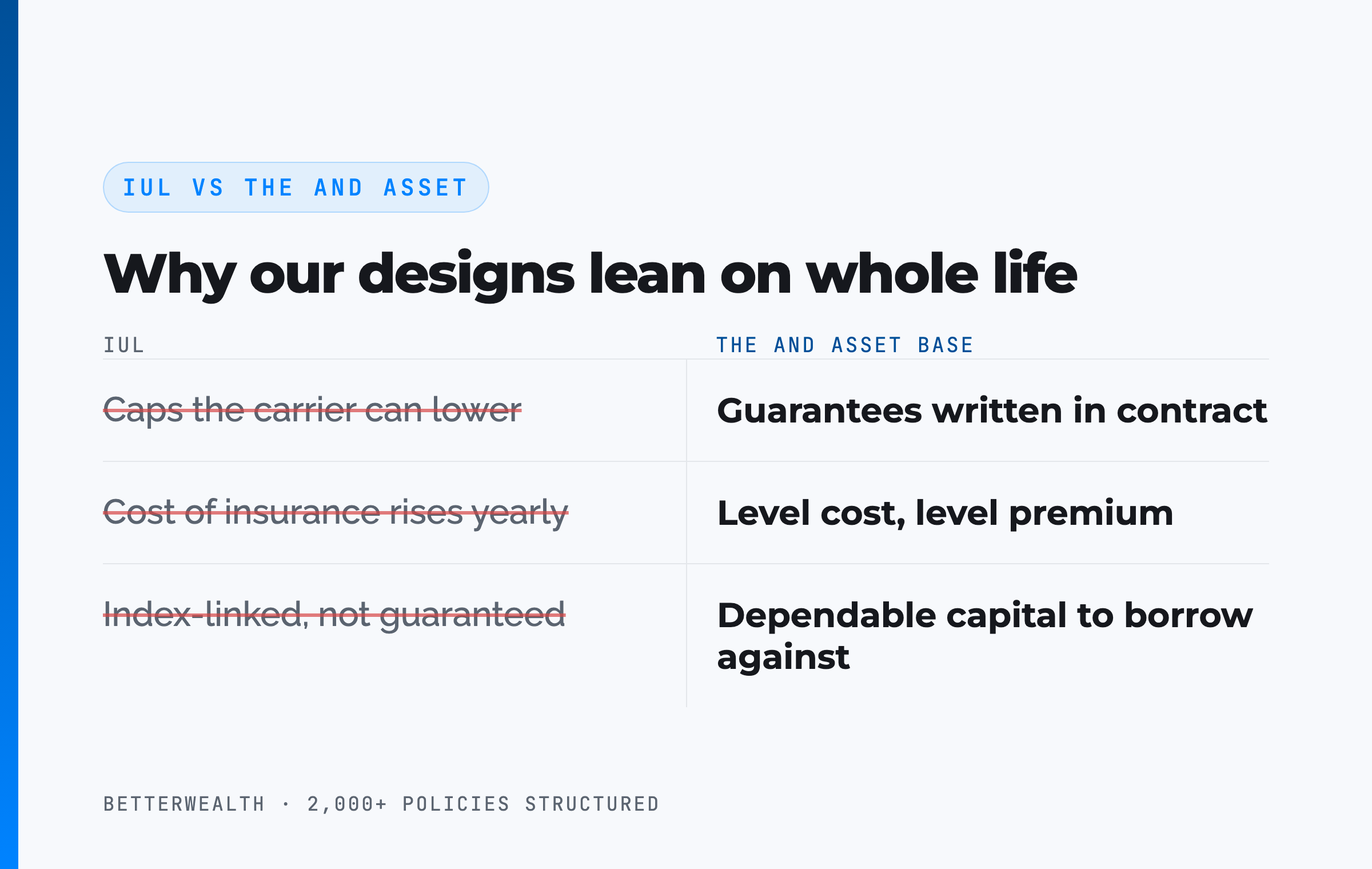

This is also why our own designs lean on whole life rather than IUL. The And Asset depends on a stable, predictable capital base. Whole life's guaranteed cash value and guaranteed minimum give you a floor under the capital you intend to borrow against. An IUL's cash value depends on caps and crediting the carrier can change, which adds a variable to the one number the strategy needs to be dependable. IUL can be structured for cash value, and some people do exactly that, but you are building the foundation on a surface that moves.

The math has to work. Every time.

Marketers have ruined how this strategy gets explained. The policy is the capital base, not the destination. The value is what you deploy the capital into, not the illustration.

06 / The mathDoes the return clear the loan cost?

Any decision to borrow against an IUL comes down to one test: does the deployed return exceed the carrier's loan cost? Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with the carrier, not a constant.

The structure of the decision is the same as it is for any And Asset policy. You borrow at the loan rate. Your cash value continues to be credited, subject to the policy's loan and crediting mechanics. Your deployed capital earns its own return. If that return clears the loan cost, the spread works in your favor and the dollar has done two jobs. If it does not, you have borrowed money to lose money slowly. The added wrinkle with an IUL is that the crediting side of that equation is less certain than it is with whole life, so the deployed return has to clear the loan cost by a wider margin to justify the variability.

If the deal does not clear the loan rate, do not borrow.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we compare permanent policies, including how we pressure-test an IUL illustration against the guarantees. Free, email-gated, no spam.

Open the Vault07 / The upsideWhat an IUL genuinely does well

An IUL has real advantages, and ignoring them would be as dishonest as overselling them. The downside floor is the headline: in a year the index drops, your index credit is zero rather than a loss, which appeals to people who want growth potential without watching cash value fall in a crash. That floor is a structural feature, not a marketing claim.

The flexible premium is the second genuine advantage. A business owner with an uneven income can fund heavily in a strong year and lighter in a lean one, within limits, in a way a fixed whole life premium does not allow. The third is tax treatment: the cash value grows tax-advantaged under IRC 7702, and policy loans are not taxable income while the policy stays in force and is not a Modified Endowment Contract. The fourth is index-linked upside above what a fixed-rate policy credits, when caps hold and the index cooperates.

None of these advantages are free. The floor costs you the cap. The flexible premium costs you the discipline that keeps the policy alive. The upside costs you certainty. That is the trade an IUL asks you to make, and for the right person it is a fair one.

IUL is not a bad product. It is a product that gets sold to the wrong people with the wrong expectations, which is a sales problem, not a contract problem.

08 / Head to headIUL vs whole life: where each one wins

IUL trades whole life's guarantees for index-linked upside and premium flexibility, and the right choice depends on what you value more: certainty or potential. Neither is universally better. We design primarily with whole life because the strategy we teach depends on a dependable capital base, but a person who wants flexible funding and accepts variability can have a legitimate reason to choose IUL. For a deeper side-by-side, see our honest comparison of IUL and whole life insurance.

| Dimension | Indexed Universal Life | Whole Life |

|---|---|---|

| Cash value growth | Index-linked, capped on the upside, floored on the downside, not guaranteed | Guaranteed minimum plus non-guaranteed dividends, compounding net of mortality and expense charges |

| Premium | Flexible within IRS limits; can be underfunded | Fixed and level; the structure enforces funding |

| Cost of insurance | Rises each year with age, deducted from cash value | Level, built into the level premium for life |

| Carrier discretion | Carrier can lower caps and participation rates after issue | Guarantees are contractual and cannot be lowered |

| Best fit | Flexible funder who accepts variability for upside potential | Capital-base builder who wants certainty to borrow against |

Growth. Whole life gives you a guaranteed cash value floor and a dividend on top, where the guaranteed portion cannot move. IUL gives you index-linked upside with a 0% floor on the index credit, but no guarantee on the growth itself, because caps and costs can shift. One is a known minimum. The other is a range.

Discipline. A whole life premium is the same every year, which forces the funding the strategy needs. An IUL lets you pay less, which feels like freedom and behaves like risk, because the rising cost of insurance does not pause when your premium does.

Certainty. The whole life guarantees are written into the contract. The IUL caps are declared by the carrier and can be lowered. If you are building a capital base you intend to borrow against for decades, that difference is the whole decision.

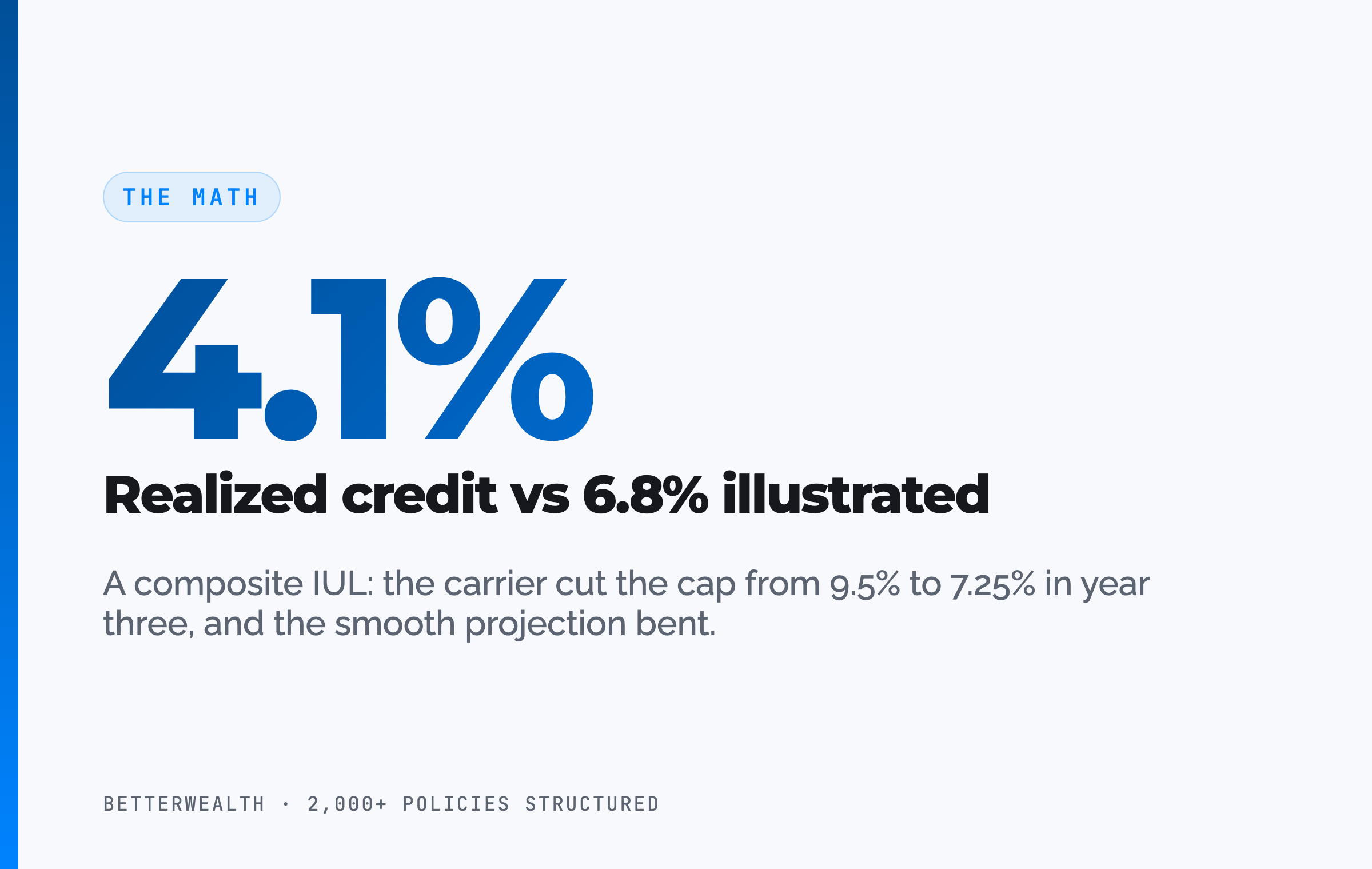

A composite: the illustration that did not hold

Consider a 44-year-old marketing-agency owner, preferred non-tobacco, who was shown an IUL illustrated at a 6.8% crediting rate with a 9.5% cap, funding $31,000 per year. This is a representative composite, not a single named client, and the numbers are illustrative.

Through the early years, cash value trailed cumulative contributions, exactly as a real policy does once the cost of insurance and policy charges are paid first. Break-even, where total cash value catches total contributions, did not arrive until past year 5. Any IUL illustration showing year-two break-even is fiction.

The deeper lesson was the cap. In year three the carrier lowered the cap from 9.5% to 7.25% across the in-force book, and two flat index years credited near the 0% floor while the rising cost of insurance kept coming out. By year eight, the realized average credit sat near 4.1%, not the 6.8% on the original page, and the projected cash value column was roughly a third lower than the buyer had been shown. The policy was not failing. It was simply doing what the contract allowed, while the illustration had assumed the best case would hold for thirty years.

The contract did what it said. The illustration did not.

The honest 30 minutes about whether IUL fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner pressure-tests the illustration you are holding, shows you the guarantees underneath it, and tells you whether an IUL, a whole life design, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call09 / The verdictIs an IUL a good investment, and who is it for?

An IUL is life insurance with a cash value feature, not an investment in the way a brokerage account is, and judging it as an investment is where most buyers go wrong. It is not registered as a security. You do not own the index, you do not collect its dividends, and your upside is capped while your costs rise with age. We answer the investment question directly in our honest take on whether IUL is a good investment, and the short version is that anyone selling it as a market-beating vehicle is overselling it.

So who is it for? The flexible-income earner who will fund the policy well above the minimum, monitor it, and value the downside floor and premium flexibility enough to accept that caps and costs can move. It is the wrong product for someone who wants a guarantee they can borrow against without watching the policy, who will pay only the minimum premium, or who was told it would beat the market. If you cannot name a use for the cash value beyond "it grows," the case for an IUL over a simpler, guaranteed design gets thin.

FAQIndexed universal life insurance questions

How does indexed universal life insurance work?

Indexed universal life insurance is permanent life insurance whose cash value is credited based on the movement of a market index like the S&P 500, with a cap that limits gains and a floor, usually 0%, that limits index losses. You are not invested directly in the market. Premiums are flexible, and the cost of insurance is deducted each year and rises with age.

Is your money invested in the stock market in an IUL?

No. Your cash value is not invested directly in the stock market. The carrier credits interest based on the performance of an index, within a cap and a floor, but you do not own the index, collect its dividends, or take its full gains or losses. The carrier uses options to fund the index credit while holding your cash value in its general account.

What is a cap and a floor in an IUL?

A cap is the maximum interest the carrier will credit in a segment, even if the index rises more. A floor is the minimum, usually 0%, so a negative index year credits zero rather than a loss. Both the cap and the participation rate can be changed by the carrier after you buy the policy, which is a risk most illustrations do not emphasize.

What is a participation rate in an IUL?

A participation rate is the percentage of the index's gain the carrier credits before any cap applies. A 100% participation rate with a 9% cap credits the full index gain up to 9%. A participation rate below 100% credits only part of the gain. Like the cap, the participation rate is set by the carrier and can change after you own the policy.

What is illustration risk in an IUL?

Illustration risk is the gap between the illustrated rate an agent shows you and the actual rate the policy earns over time. Illustrated rates are projections, not guarantees. If the index underperforms, the carrier lowers the cap, or the cost of insurance rises faster than assumed, real cash value can fall well short of the illustration. The 2021 AG49-A rule tightened these assumptions for that reason.

Can an IUL policy lapse?

Yes. An IUL can lapse if it is underfunded. The cost of insurance rises with age, and if premiums and crediting do not keep pace, the policy can drain its own cash value to cover charges and eventually collapse. A lapse with an outstanding loan can also trigger a taxable event. Funding discipline is what keeps the policy alive.

Are IUL policy loans tax-free?

Policy loans against an IUL are not treated as taxable income under IRC 7702 while the policy stays in force and is not a Modified Endowment Contract. The tax treatment depends on the policy never lapsing with a large loan balance. If the policy lapses or is surrendered with gains and an outstanding loan, the gain can become taxable.

IUL vs whole life: which is better for cash value?

Whole life offers a guaranteed cash value, a guaranteed minimum, and a level cost of insurance built into a level premium. IUL offers index-linked upside with a downside floor, flexible premiums, and no guaranteed growth, since caps and the cost of insurance can move. Whole life trades upside for certainty. IUL trades certainty for upside potential. Which fits depends on your horizon and your tolerance for variability.

Is IUL a good investment?

IUL is life insurance with a cash value feature, not an investment in the way a brokerage account is. It is not registered as a security, you do not own the index, and your upside is capped while charges rise with age. It can hold tax-advantaged cash value, but anyone selling it as a market-beating investment is overselling it.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured permanent life insurance policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. Our designs are built on whole life's guarantees rather than projected index credits.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a permanent policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

- IRC Section 7702 (Cornell Law): the tax code provision defining life insurance and the tax treatment of cash value and policy loans.

- NAIC: Actuarial Guideline 49-A (AG49-A) and the standards governing IUL illustrations.

- FINRA: investor guidance on indexed universal life insurance and what to question before buying.

- Nelson Nash, Becoming Your Own Banker: the origin of the infinite banking concept.

- LIMRA: life insurance industry data, including indexed life sales and persistency benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold off an illustration. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you are holding an IUL illustration and want an honest read on what is guaranteed and what is not, book a discovery call. We will tell you if it does not fit.