.png)

Velocity banking routes your income through a line of credit, usually a HELOC, to lower the average daily balance and pay debt down faster than a standard mortgage. The only thing that reduces a balance is principal. The line changes how that principal moves and preserves access to the equity you build.

The argument over velocity banking has become loud enough to drown out the actual math. One camp says it is financial sleight of hand that cannot beat a low fixed mortgage. The other sells it like a debt-erasing miracle. Neither side is describing what disciplined practitioners actually do, which is why so many people walk away more confused than informed.

Velocity banking is not a trick that erases debt, and it is not a scam. It is a cash-management system whose value depends entirely on the spread between your line of credit and your mortgage, and on whether you stay disciplined enough to run it. Strip away the marketing and the dismissals, and you are left with a real conversation about interest, liquidity, and control of your capital.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we sit in an adjacent world: using a properly designed whole life policy as a capital base. The principles overlap. So when Michael Lush and Sam Kwak came on to set the record straight about what they teach, the discussion landed on the same question we ask about every dollar. Does the capital you deploy out-earn what it costs to borrow it?

This breakdown covers what velocity banking actually is, how the HELOC versus 30-year mortgage math really works, why first lien and second lien lines carry different risk, what promo rate stacking is, and where The And Asset framework diverges from generic velocity banking. We will also tell you who this is not for.

- Velocity banking only reduces debt by reducing principal. There is no hidden mechanism that skips that step.

- A HELOC charges interest on the daily balance, so routing income through it can cut interest cost versus an amortized mortgage.

- The strategy lives or dies on the rate spread. When the line costs more than the mortgage, the pure-payoff math weakens.

- First lien HELOCs are rarely frozen; second lien lines carried most of the 2008 freeze risk in falling markets.

- Promo rate stacking can keep a line cheap, but it depends on actively shopping rates and on promos continuing to exist.

- The And Asset adds one rule velocity banking does not enforce: only deploy borrowed capital that beats the loan cost.

The full conversation is worth watching for the back-and-forth on risk and the moment both guests agree with their own critic on the core math. Sam Kwak and Michael Lush walk through the strategy in their own words:

01 / The problemWhat is the velocity banking controversy actually about?

The controversy is about variables, not honesty. The loudest takedowns compare a 3% mortgage against a 21% line of credit, which no competent practitioner would ever use, and then declare the whole strategy dead. Michael Lush put it the way a marketer who runs split tests would: you cannot evaluate two products by changing five things at once.

Run the comparison cleanly and the picture changes. Compare a line of credit to a mortgage at the same rate, with the same cash flow, and the line of credit comes out slightly ahead or even, mostly because of how interest accrues and because you keep access to your equity. The disagreement was never really about the math. Both guests agreed with their critic on the one thing that matters: the only way to reduce debt is to reduce principal.

"You've got to remove the variables. Let's just compare product to product, run the math on the same numbers, then add one variable at a time.", Michael Lush

02 / The frameworkWhat does velocity banking actually teach?

Velocity banking, taught responsibly, is a cash-flow system that runs your income through a line of credit instead of a checking account so that idle dollars work against your debt or your equity instead of sitting still. Sam Kwak calls his version accelerated payoff and is careful not to call it banking, because his firm is not a bank. Michael Lush calls his approach the flow of money and frames it around optionality rather than debt freedom.

Both reject the idea that this is for everyone. They vet clients, turn most away, and pick up where a budgeting-first teacher like Dave Ramsey leaves off, with people who are already cash-flow positive. That honesty is the credible part. The strategy is a discipline, not a product.

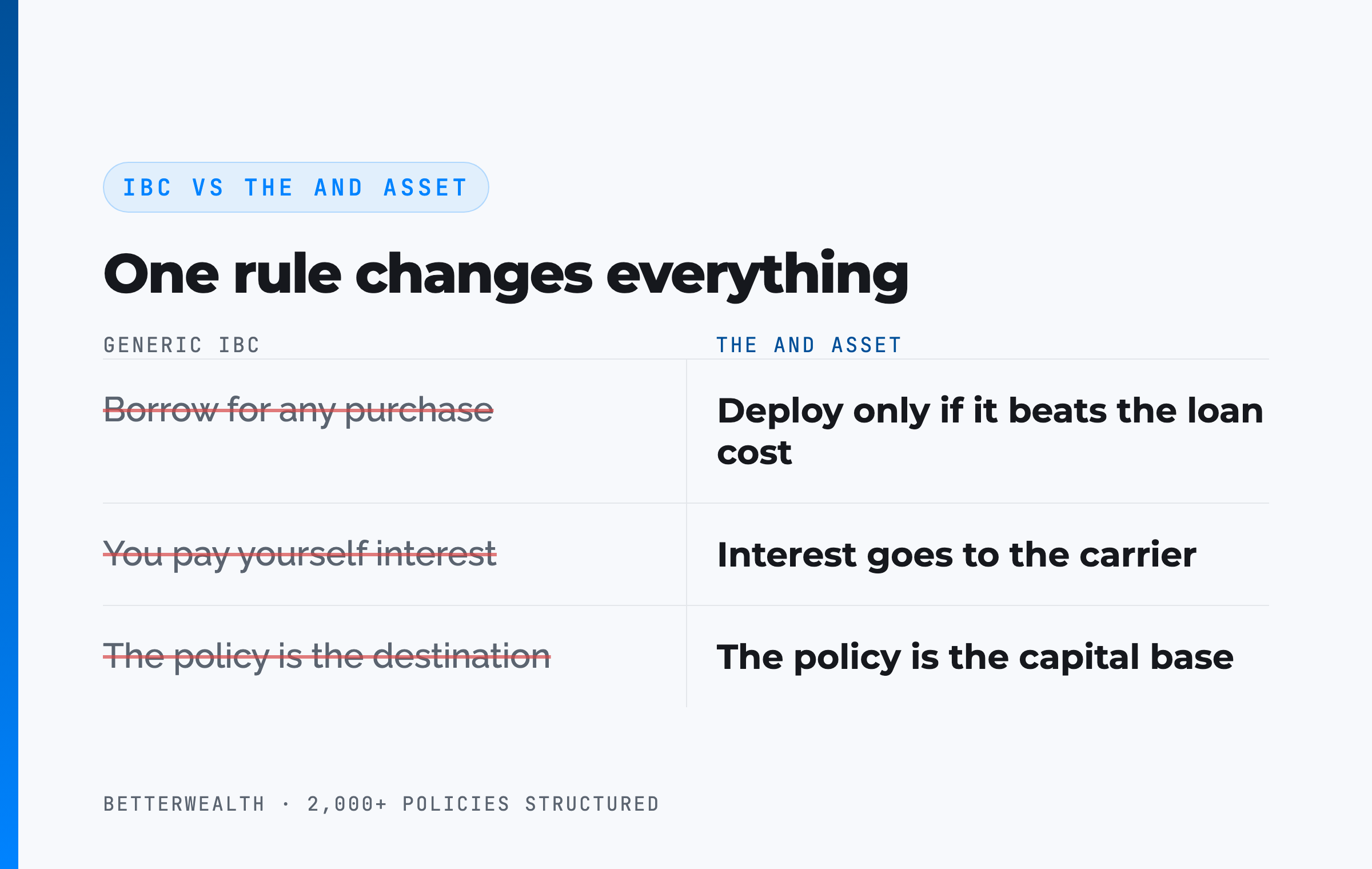

Where velocity banking ends and The And Asset begins

Velocity banking and infinite banking share a root: control of the banking function and the cost of lost opportunity. Nelson Nash pioneered using whole life insurance as a personal banking system, and his insight still holds. You either pay interest to outside lenders or you lose money to capital sitting idle. We respect that foundation. The And Asset builds on it with one rule neither generic velocity banking nor generic IBC enforces.

IBC says use the policy as a personal bank for any purchase. The And Asset says you only deploy capital, whether from a HELOC or a policy loan, into an activity that returns more than the loan costs. Anything less is an expensive way to spend money. Many marketers say you pay yourself interest. You do not. The interest goes to the lender or the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges.

The math has to work. Every time.

The line of credit is not the strategy. Deploying borrowed dollars into a return that beats the loan rate is the strategy. Without that discipline, you have an expensive checking account.

03 / The mathDoes paying a mortgage with a HELOC actually save money?

It can, and the reason is mechanical, not magical. A mortgage charges interest on a fixed amortized balance that only updates once a month. A HELOC charges interest on the average daily balance. When you park your full income against the line the day it arrives, you shrink the balance interest is calculated on for as long as that money sits there.

Sam Kwak named the core mechanism directly: reduction of the daily balance. Lower the daily balance and you lower the interest accrued, even before you touch the principal in a meaningful way. Add Michael Lush's promo rate stacking, where the line carries a low introductory rate, and the cost of the borrowed dollars can fall well below a 30-year mortgage. Stack a card you pay in full each month for daily expenses, and you delay drawing the line at all.

None of this defies arithmetic. A line of credit at 2% beats a mortgage at 5% in every scenario, because 2 is less than 5. The honest caveat is the rate. When the HELOC sits above the mortgage, the pure payoff advantage narrows or disappears, and the case shifts from cost savings to optionality.

"Your 3% is not 3%." That on-camera line is a warning about total interest paid over a full term, which can reach 60% to 90% of the amount borrowed. It is the total interest percentage, not the interest rate. Read it that way.

A line of credit strategy fits a specific person.

It fits you if

- You are cash-flow positive and disciplined

- You want access to your equity, not locked-away principal

- You can name a use for capital that beats the loan cost

- You will actually run the system, not just admire it

It does not fit you if

- You spend more than you earn

- You hold a sub-3% mortgage with thin cash flow

- You want a shortcut instead of a system

- You have no productive use for borrowed dollars

If you are in the first column and want to know whether a whole life policy adds anything to what you are already doing, a 30-minute conversation will tell you. If you are in the second, we will tell you that too.

Book a Discovery Call04 / The riskFirst lien vs second lien HELOC: which one gets frozen?

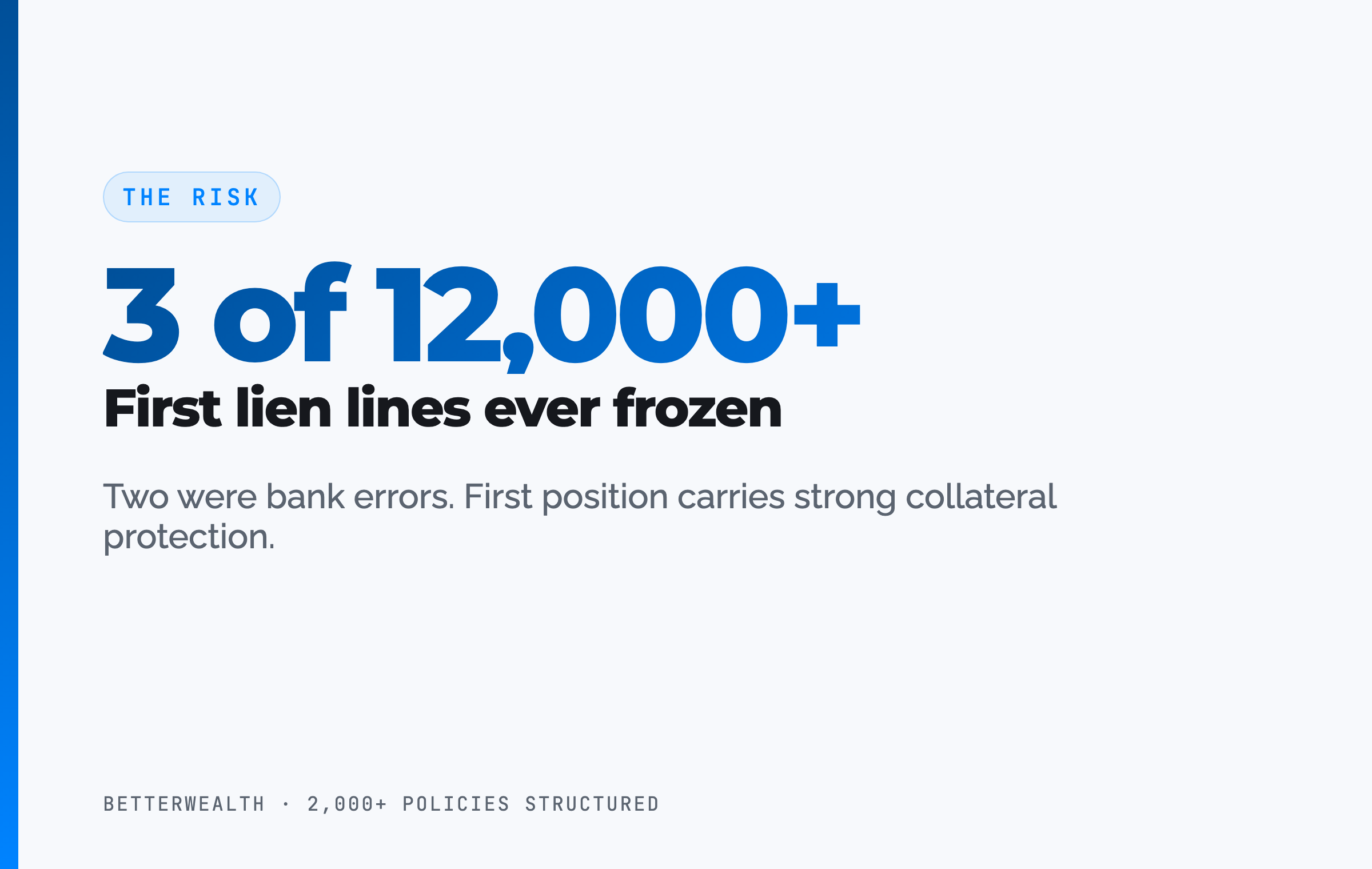

First lien HELOCs are rarely frozen, and second lien lines carry most of the freeze risk people are afraid of. The difference is collateral. A first lien sits in the same position a mortgage holds, with first claim on the home, so the bank has little reason to cut it. A second lien sits behind the mortgage with no guaranteed recovery if the home is foreclosed, which is exactly why those lines got reduced during the 2008 downturn, concentrated in markets that saw steep price drops.

The fear most people carry comes from a story about a second lien line in a crashing market, applied to every HELOC. Lush reports three frozen lines across more than 12,000 first lien clients, two of them bank errors. A first lien freeze generally requires a severe drop in the property's value, the kind of decline that would be a market-wide event, not a quiet bank decision.

The risk nobody reads in their mortgage

A mortgage carries an acceleration clause that lets the lender call the loan due under conditions spelled out in your closing documents. It happens. Lush described a borrower whose loan was called through no fault of his own, because the bank could not place the paper it wanted to sell. The point is not that mortgages are dangerous. It is that "the bank can call it" is true of both products, and the first lien line often gives you more options to fight or move, where a called mortgage leaves foreclosure as the path.

Both products carry risk. Optionality is the difference.

A 50% home-value collapse is what it would take to threaten a first lien line. That is an implosion, not a Tuesday. Pricing a strategy around that scenario means pricing a mortgage around it too.

05 / Promo rate stackingWhat is promo rate stacking, and is it real?

Promo rate stacking is the practice of rolling from one introductory HELOC rate into the next as each promotional period ends, keeping the borrowed cost low. Banks flood the market with low promo rates because a HELOC is a trip wire to win a relationship, and the real prize is the checking and savings deposits that follow. Sam Kwak confirmed it live: his mortgage servicer called the morning of the recording offering a discounted promo line.

The strategy is real, and it is also work. It depends on actively shopping lenders, tracking renewal dates, and the continued existence of promo offers. Fixed introductory periods commonly run 12 months, sometimes longer, and a few lines fix for several years. Treat a multi-year fixed HELOC as still variable next to a 30-year mortgage, because once the period ends, the rate resets.

Lush reports averaging a new line every 18 to 24 months over 14 years and says he has never carried a HELOC rate near a mortgage rate. That is one disciplined operator's experience, not a guarantee you will replicate it. If promo availability dried up, the cost case would change, and the optionality case would have to carry the strategy on its own.

06 / How it worksHow does the flow of money work, step by step?

The flow of money works by treating a first lien line of credit as the hub that all your income passes through, so dollars are always working against a balance instead of sitting idle. Here is the sequence, expanded beyond the video and tied to the discipline that makes it worth doing.

- Route income through the line. Deposit your full income into the first lien HELOC rather than a checking account. Every dollar lowers the average daily balance the moment it lands, where a checking account does nothing for you.

- Pay expenses on a delay. Cover monthly spending with a card you pay in full each statement. Your income sits against the line longer, cutting accrued interest before the money leaves.

- Watch the daily balance fall. Because the line charges interest on the daily balance, parking income against it reduces interest cost compared with a mortgage that charges on a fixed amortized figure.

- Deploy capital that beats the loan cost. Draw from the line, or borrow against a whole life policy, only to fund an activity that returns more than the loan rate. This is the step velocity banking leaves optional and The And Asset makes mandatory.

- Repay from the cash flow. Let the income the deployed capital produces flow back against the line. As the balance drops, liquidity opens up to deploy again.

Lush describes his own version running income to the line, then to insurance policies, then borrowing against those policies to buy cash-flowing assets like laundromats. As the assets produce income, the line falls and liquidity returns. That is The And Asset logic in practice: the borrowed dollar does two jobs, provided the asset clears the loan cost.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to model whether borrowed capital, from a line of credit or a policy loan, actually clears the loan cost. Free, email-gated, no spam.

Open the Vault07 / The 30-year mortgageWhy is a 30-year mortgage still defensible?

A 30-year mortgage is defensible because it locks a rate for three decades and produces the lowest required payment, which frees cash flow to invest or deploy elsewhere. For a borrower who holds a sub-3% rate from 2021, exposing that mortgage to a potentially higher line of credit makes no sense, and even the velocity banking advocates say so.

The honest counterweight is total cost and locked equity. Over a full term, the interest paid can equal more than half the home's price, and every dollar of principal you build is inaccessible until you sell or borrow against it. The investing argument cuts the other way: pay the minimum, deploy the difference at a higher return, and the spread can outrun the interest. That math depends on actually deploying the difference, which most people do not do.

Here is the resolution both sides quietly reach. A first lien line lets you make a 30-year-style payment, invest the rest, and keep access to the principal you pay down. You get the low-payment optionality of the mortgage without locking the equity away. The interest rate is the only variable left to compare, and that is a numbers question, not a philosophy one.

"I'm not anti 30-year mortgage. I'm anti keeping a 30-year mortgage for 30 years." The tool is fine. Using it on autopilot for three decades is the expensive part.

08 / Where people get this wrongThe marketing traps to avoid

People get burned when the marketing outruns the math, and the failure modes are predictable. The first is rate blindness: using a high-cost line to attack a low-cost mortgage because someone sold the mechanism without the spread. If the line costs more than the debt and you have no productive deployment, you are paying more to feel busy.

The second is the high-yield-savings fantasy. Plans that assume a 5% savings rate forever, or 5% on millions of dollars across a single insured account, are modeling a world that does not exist. Real rates move, federal insurance caps at the per-bank limit, and large balances get spread thin. Build the plan on rates that float, not on a number from a slide.

The third is the belief that a whole life policy is a math arbitrage against a checking account. It is not, and we say so plainly. Strip out the optionality, the control, and the uninterrupted compounding, and a bare cost comparison can favor the checking account. The value shows up when you add back what the policy gives you that cash does not, and when you deploy the capital into something that beats the loan cost.

Marketers have ruined how these strategies get explained. The honest version is less exciting and far more durable: reduce principal, mind the spread, deploy capital that out-earns the loan, and stay disciplined.

A composite: the contractor who ran the flow of money

Consider a 44-year-old contractor, cash-flow positive, with a first lien HELOC limit of $327,000 against a paid-down home. This is a representative composite, not a single named client.

He routes his full income through the line and pays expenses on a card he clears monthly, which holds the average daily balance down and cuts accrued interest before the money leaves. That alone is a modest, real gain.

The capital decision is where the strategy earns its name. He draws $146,500 to buy equipment that returns an estimated 13.6% IRR against a line cost near 6.5%, a spread of roughly seven points. The equipment's cash flow runs back against the line on a 41-month schedule, reopening liquidity as it pays down. He pairs this with a properly structured And Asset policy funded at $38,000 a year. Through the first three years its cash value trails cumulative contributions, exactly as a real policy should, and it crosses break-even in year five. No earlier.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your capital structure and tells you whether a whole life policy adds anything to a line-of-credit strategy you may already run, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call09 / Head to headVelocity banking, the 30-year mortgage, and The And Asset

Compared to the tools entrepreneurs actually use, each option trades something different. A first lien line trades a fixed rate for daily-balance efficiency and access. A 30-year mortgage trades equity access for rate certainty. The And Asset trades day-one liquidity for uninterrupted compounding and control. The table sets them side by side on the dimensions that matter for life insurance strategy.

| Dimension | First Lien HELOC | 30-Year Mortgage | The And Asset |

|---|---|---|---|

| Interest mechanics | Charged on the average daily balance; income parked against it cuts cost | Charged on a fixed amortized balance, front-loaded with interest | Policy compounds net of internal charges; loan interest goes to the carrier |

| Liquidity / access | Keep access to equity you pay down; draw anytime | Principal is locked until you sell or borrow against it | Loans against cash value, typically after the early funding window |

| Rate certainty | Promo or variable; resets at period end | Fixed for the full 30 years | Loan rate varies by carrier; spread structure set in the contract |

| Control | More options to fight or move if terms change | Acceleration clause lets the lender call it under set conditions | Loan cannot be called; you set repayment terms |

Interest mechanics. The line's daily-balance accrual is its structural edge, and the mortgage's amortized, front-loaded interest is its structural cost. The policy plays a different game entirely, compounding on its full value while you borrow against it.

Liquidity and control. The mortgage builds equity you cannot touch without unwinding the loan. The line and the policy both keep your capital reachable, which is the whole point for someone deploying into deals. For a deeper side-by-side on the insurance angle, see our breakdown of infinite banking versus a HELOC.

The common thread. None of these tools creates value on its own. Value comes from what you deploy the freed capital into, measured against what that capital costs. That is the test, regardless of which row you pick.

FAQVelocity banking questions

What is velocity banking?

Velocity banking is a strategy that routes your income through a line of credit, usually a HELOC, to lower the average daily balance and pay down debt faster than a standard mortgage schedule. The only thing that reduces a balance is principal reduction. The line of credit changes how and when that principal gets reduced, and it preserves access to the equity you pay down.

Is velocity banking a scam?

Velocity banking is not a scam, but it has been oversold. There is no magic that erases debt without paying down principal. The strategy works when the line of credit costs less than or close to the mortgage, you route income through it, and you stay disciplined. It fails when someone uses a high-rate line to chase a low-rate mortgage or treats it as a shortcut instead of a system.

Does paying a mortgage with a HELOC actually save money?

It can, for two reasons. A HELOC charges interest on the average daily balance, so parking income against it reduces accrued interest versus a mortgage that charges on a fixed amortized balance. And many HELOCs carry low introductory promo rates. If the line costs more than the mortgage, the savings shrink or disappear, which is why the rate comparison matters.

What is a first lien HELOC?

A first lien HELOC replaces your mortgage entirely and sits in first position against your home, the same position a mortgage holds. It combines a line of credit with the role of a primary mortgage, so you can route income through it, draw against equity, and pay interest only on the outstanding daily balance.

First lien vs second lien HELOC: which is safer?

First lien HELOCs are rarely frozen because the bank holds first claim on the home and has strong collateral protection. Second lien HELOCs sit behind a mortgage with no guaranteed collateral if the home is foreclosed, so they were the lines most often frozen or reduced during the 2008 downturn, mainly in markets that saw severe price drops.

Can a HELOC be frozen or called like in 2008?

A HELOC can be frozen or reduced, but it is uncommon for first lien lines and usually requires a severe drop in the home's value. Most freezes in 2008 hit second lien lines in markets with steep declines. A mortgage carries its own risk many people overlook: an acceleration clause that lets the lender call the loan due under conditions spelled out in the closing documents.

What is promo rate stacking?

Promo rate stacking is renewing or refinancing into a new introductory HELOC rate as each promotional period ends. Banks use low promo rates to win deposits, so a disciplined borrower can roll from one promo rate to the next. It requires actively shopping lines and tracking renewal dates, and the strategy depends on promo rates continuing to exist.

Is a 30-year mortgage bad?

A 30-year mortgage is not inherently bad. It locks a rate, offers the lowest required payment, and can free cash flow to invest or deploy elsewhere. The tradeoffs are total interest paid over the full term and the loss of access to the equity you build, since that capital is locked until you sell or borrow against it.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that returns more than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding net of mortality and expense charges while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the loan cost. The policy is the capital base, not the destination. It shares roots with IBC but operates on different principles.

Does velocity banking work if HELOC rates are higher than my mortgage?

When the HELOC rate sits above the mortgage rate, the pure debt-payoff math weakens, and a low fixed mortgage paired with disciplined investing can win. The case for the line of credit then rests on optionality: you keep access to your equity and can deploy capital into returns that beat the higher loan cost. That only holds if you actually deploy it productively.

Should I use a HELOC or just make extra mortgage payments?

Extra mortgage payments reduce your balance but lock that money away, since you cannot reclaim it without selling or borrowing. A HELOC lets you pay down principal while keeping access to the equity. Behaviorally it matters too: most people never make consistent extra payments, so a system that routes income automatically tends to produce results a manual plan does not.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- CFPB: Understanding the Loan Estimate, including the total interest percentage disclosed on page three.

- CFPB on HELOC freezes and reductions, the conditions under which a line can be cut.

- IRC Section 7702 (Cornell Law), the tax treatment of life insurance cash value and loans.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

A former mortgage professional and bank board member who teaches a line-of-credit "flow of money" approach built around optionality. He walks through promo rate stacking and first lien risk in the source video.

Co-founder of the Kwak Brothers and a coaching practice focused on accelerated debt payoff through home equity lines of credit. He frames the strategy as implementation and accountability, not a product.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a policy belongs alongside a line-of-credit strategy, book a discovery call. We will tell you if it does not.