.png)

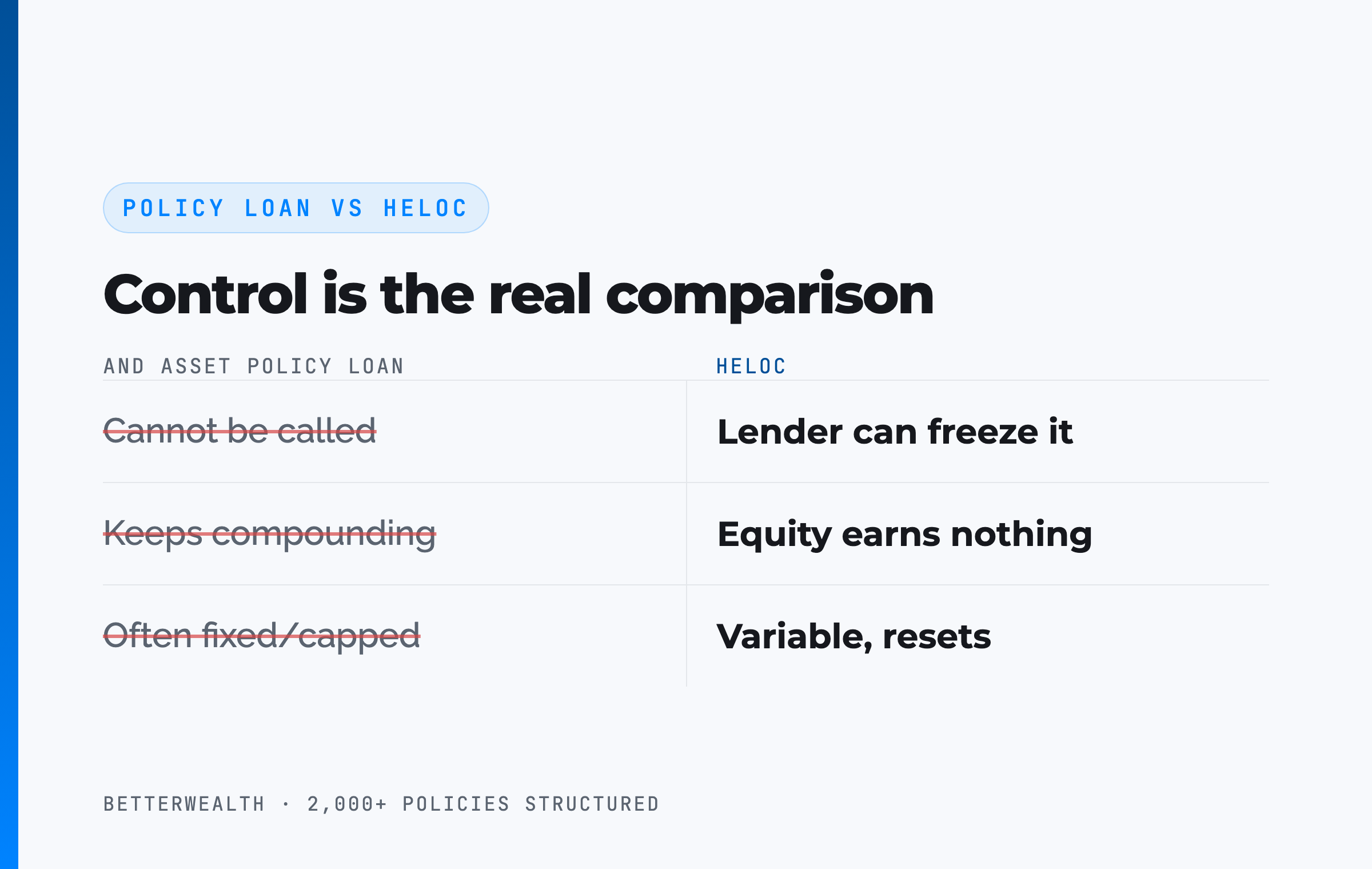

Infinite banking versus a HELOC comes down to control. A HELOC is a callable credit line a lender can freeze; borrowing against a whole life policy is collateralized access that cannot be called, and the policy keeps compounding on its full value while the loan is outstanding.

Liquidity that disappears under stress was never liquidity. That is the lesson thousands of homeowners learned in 2008 and again in 2020, when banks froze and slashed home equity lines of credit in the exact months that capital was hardest to find and most valuable to deploy. The line was open right up until the moment it mattered.

The comparison between a HELOC and borrowing against a whole life policy is not really about interest rates. It is about who controls access to the capital and whether the underlying asset keeps working while you use it. A HELOC is a credit product secured by your house. A whole life policy structured for cash value is an asset you own and borrow against. Those are different things, and the difference shows up at the worst possible time.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the HELOC comparison comes up on almost every call with a real estate investor or business owner. They already use a line of credit. They want to know whether a policy does something a HELOC cannot. This comparison covers four dimensions that decide the answer: control, callability, continued compounding, and rate behavior. It also covers where a HELOC still wins, because sometimes it does.

- A HELOC can be frozen, reduced, or called by the lender. A policy loan cannot be called while the policy stays in force.

- A whole life policy keeps compounding on its full cash value, net of internal costs, even while you borrow against it.

- HELOC rates are usually variable and reset with prime; policy loan rates are often fixed or capped by the carrier.

- A HELOC wins on speed today if you already hold equity; a policy is a multi-year capital base, not an instant fix.

- The And Asset rule governs either tool: only borrow when the deployed return clears the loan cost.

- The two are not mutually exclusive. Many entrepreneurs run a HELOC now and build a policy for the long horizon.

01 / The problemThe line of credit that vanished when it mattered

The core problem with a HELOC is that its availability is conditional, and the conditions tighten exactly when you need capital most. A home equity line is a revolving credit facility secured by your house. The bank extends it based on your home's value and your credit profile, and the bank reserves the right to freeze it, reduce it, or suspend draws if either of those changes.

That is not a hypothetical. In the 2008 housing collapse, lenders cut off home equity access for hundreds of thousands of borrowers as appraisals fell. In 2020, several major banks stopped accepting new HELOC applications entirely. The pattern repeats because a HELOC is the lender's asset, not yours. You are renting access to your own equity, and the landlord can change the terms.

For an entrepreneur or real estate investor, that is the whole problem. Opportunities cluster in downturns, when sellers are motivated and prices are soft. A capital source that disappears in a downturn is useless precisely when it would create the most value.

A HELOC feels like access to your capital. It is access to the bank's willingness to lend, and that willingness evaporates in the conditions where capital is worth the most.

02 / The frameworkWhat does it mean to borrow against a policy instead of a HELOC?

Borrowing against a policy means taking a loan collateralized by the cash value of a whole life policy you own, rather than drawing on a credit line secured by your house. The mechanical difference is ownership. With a HELOC, the bank lends against an asset and controls the terms. With a policy loan, the carrier lends against your contractual cash value, and the contract protects your access.

The discipline layered on top of that mechanism is what we call The And Asset. If the framework is new to you, start with What Is Infinite Banking? The And Asset Guide, which lays out the borrowing principle in full. The short version is that you only borrow against the policy for an activity that produces a return greater than the carrier's loan cost. Your dollars do two jobs at once. That is the AND.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule the broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase, including the ones a HELOC usually funds. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many marketers also say you are paying yourself interest when you repay a policy loan. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding uninterrupted.

The math has to work. Every time.

03 / CallabilityCan a HELOC be frozen or called?

Yes, a HELOC can be frozen, reduced, or suspended by the lender, and that is the single largest difference between the two tools. A bank can cut your available credit if your home value drops, your credit score slips, or the institution simply decides to tighten its risk exposure across the board. The loan agreement gives the lender that right, and history shows lenders use it during downturns.

A policy loan works the other way. As long as the policy stays in force, the carrier cannot call the loan, cannot demand repayment on a schedule, and cannot reduce your access because of market conditions or your credit. The loan is collateralized by a contractual cash value the carrier already owes you. You decide when and how much to repay.

For a life insurance strategy that depends on access being there in year seven or year fifteen, that distinction is the entire game. Control of access is worth more than a few tenths of a percent on the rate.

The bank can take back a HELOC. The carrier cannot take back your policy loan. If you are deploying capital into deals, that is not a footnote. It is the headline.

04 / CompoundingWhy does the policy keep growing while a HELOC sits idle?

The policy keeps growing because a policy loan is collateralized by your cash value, not a withdrawal from it. The carrier lends you its money and uses your cash value as security, so your full cash value continues to compound net of mortality and expense charges while the loan is outstanding. The home equity behind a HELOC, by contrast, earns nothing. It tracks the housing market whether you borrow against it or not, so there is no compounding to interrupt and none to preserve.

This is the structural feature that lets the same dollar do two jobs. When you borrow against the policy and deploy the capital into a deal, the deal earns its own return, and the policy keeps compounding on the full value as if you had not touched it. With a HELOC, you get the deal's return and nothing on the equity, because equity is dead money sitting in a house.

Uninterrupted compounding is the point.

The honest qualifier: this advantage only exists once the policy has meaningful cash value, which takes years to build. A HELOC requires home equity you already have. The policy requires capital you fund over a decade or more. The compounding edge is real, but it is a long-horizon edge, not a day-one one.

05 / Rate behaviorHow do the rates actually compare?

The rates are not directly comparable, because they behave differently and sit on top of different risks. HELOC rates are usually variable. They float with the prime rate, reset monthly, and have climbed sharply in tightening cycles. The rate you sign up for is not the rate you keep. Policy loan rates vary by carrier and the rate environment, and many carriers offer a fixed or capped rate, which removes a variable from your planning.

At the time of writing, many carriers fall in the 5 to 6 percent range on policy loans, but treat any specific number as a variable to verify with the carrier, not a constant. A HELOC's introductory rate can look lower today and end up higher in two years. The fixed or capped structure on the policy side is worth real money to anyone planning capital deployment across a full rate cycle.

Rate alone is still the wrong place to anchor the decision. A slightly cheaper HELOC that can be frozen is not cheaper in any meaningful sense if it disappears in the downturn when you planned to use it. Price the optionality, not just the coupon.

Comparing the headline rates is comparing the wrong thing. A callable variable-rate line and a non-callable fixed-rate one are not the same product at different prices. They are different products.

06 / The mathDoes the return clear the loan cost?

The return on whatever you deploy must exceed the loan cost, or you should not borrow against either tool. This is the entire test, and it applies identically to a HELOC and a policy loan. You borrow at the loan rate. You deploy the capital into an activity that earns its own return. If that return is higher than the cost of the loan, you are ahead on the spread. If it is lower, you have borrowed money to lose money slowly.

The policy adds one term the HELOC does not. While the loan is outstanding, the policy keeps compounding on its full value, so the policy's growth stacks on top of the deal's return. With a HELOC, you get the spread between the deal and the loan, and nothing more. The compounding term is the structural reason the same dollar does two jobs in The And Asset and only one job behind a HELOC.

If the deal does not clear the loan rate, do not borrow.

A policy fits a specific person. So does a HELOC.

The policy route fits if

- You have a long capital horizon (10+ years)

- You value access that cannot be frozen or called

- You can name a use that beats the loan cost

- You want the asset to keep compounding while borrowed against

A HELOC fits better if

- You need capital this month, not this decade

- You already hold substantial home equity

- You have no funded policy yet

- The need is one-time, not a repeating strategy

If you are in the first column, a 30-minute conversation will tell you whether a properly designed policy fits your plan. If you are in the second, we will tell you that too.

Book a Discovery Call07 / Where people get this wrongThe oversell in both directions

The most common mistake is treating this as a contest with one universal winner, which is exactly how marketers on both sides sell it. The insurance marketer claims a policy beats a HELOC on every dimension and skips the part where it takes years to fund. The HELOC advocate fixates on the lower introductory rate and ignores callability and the dead equity. Both are selling, and neither is doing the math honestly.

The second mistake is the "pay yourself interest" line, which gets applied to policy loans constantly and is simply wrong. When you repay a policy loan, the interest goes to the carrier, the same way HELOC interest goes to the bank. The advantage of the policy is not that the interest comes back to you. It is that the cash value keeps compounding and the access cannot be revoked.

Liquidity is not the same as available credit

A HELOC shows a large available balance on a statement, which feels like liquidity. It is conditional credit, and the condition is the lender's continued willingness to lend. Real liquidity is access that holds under stress. Cash value you can borrow against without approval is closer to that standard than a credit line that can be cut. Know which one you actually have.

Marketers have ruined how this gets explained. A policy is not free money and a HELOC is not a trap. They are different tools with different failure modes. Pick for your timeline and your tolerance for callability.

08 / Head to headThe And Asset policy against a HELOC

Across the four dimensions that matter for life insurance strategy, a policy trades day-one speed for control, continued compounding, and rate stability. The table sets a properly designed And Asset policy against a HELOC on access, callability, what happens to the underlying asset, and rate behavior.

| Dimension | The And Asset policy loan | HELOC |

|---|---|---|

| Callability | Cannot be called or frozen while the policy is in force; you set repayment | Lender can freeze, reduce, or suspend draws, especially in a downturn |

| Underlying asset | Cash value keeps compounding on its full value, net of internal costs, while borrowed against | Home equity earns nothing; it tracks the housing market whether borrowed against or not |

| Rate behavior | Often fixed or capped by the carrier; a known cost across the rate cycle | Usually variable, resets with prime; the cost can climb with no notice |

| Access & setup | No approval, appraisal, or credit check once cash value exists; takes years to build | Fast to draw once open, but requires underwriting, appraisal, and approval first |

| Tax treatment | Loans on a non-MEC policy are not treated as taxable income; cash value grows tax-deferred | Loan proceeds are not income; interest deductible only in limited cases |

Callability and control. This is the dimension that decides the comparison for most capital deployers. A HELOC can be cut at the moment you planned to use it. A policy loan cannot. If your strategy depends on access being there in a downturn, the policy is built for it and the HELOC is not.

The underlying asset. A policy keeps compounding on its full value while you borrow, which is the structural reason the same dollar can do two jobs. Home equity behind a HELOC is dead money that earns nothing, so the HELOC gives you the deal's return and nothing else.

Speed versus horizon. The HELOC's honest advantage is speed against equity you already hold. A policy takes years to build a cash value worth borrowing against. The right answer for many entrepreneurs is to use a HELOC for today's need while funding a policy for the next decade of needs.

A composite: the investor whose HELOC froze, and what changed

Consider a 43-year-old real estate investor, preferred non-tobacco, who funds a whole life policy designed for maximum cash value at $48,000 per year on a cashflow design. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

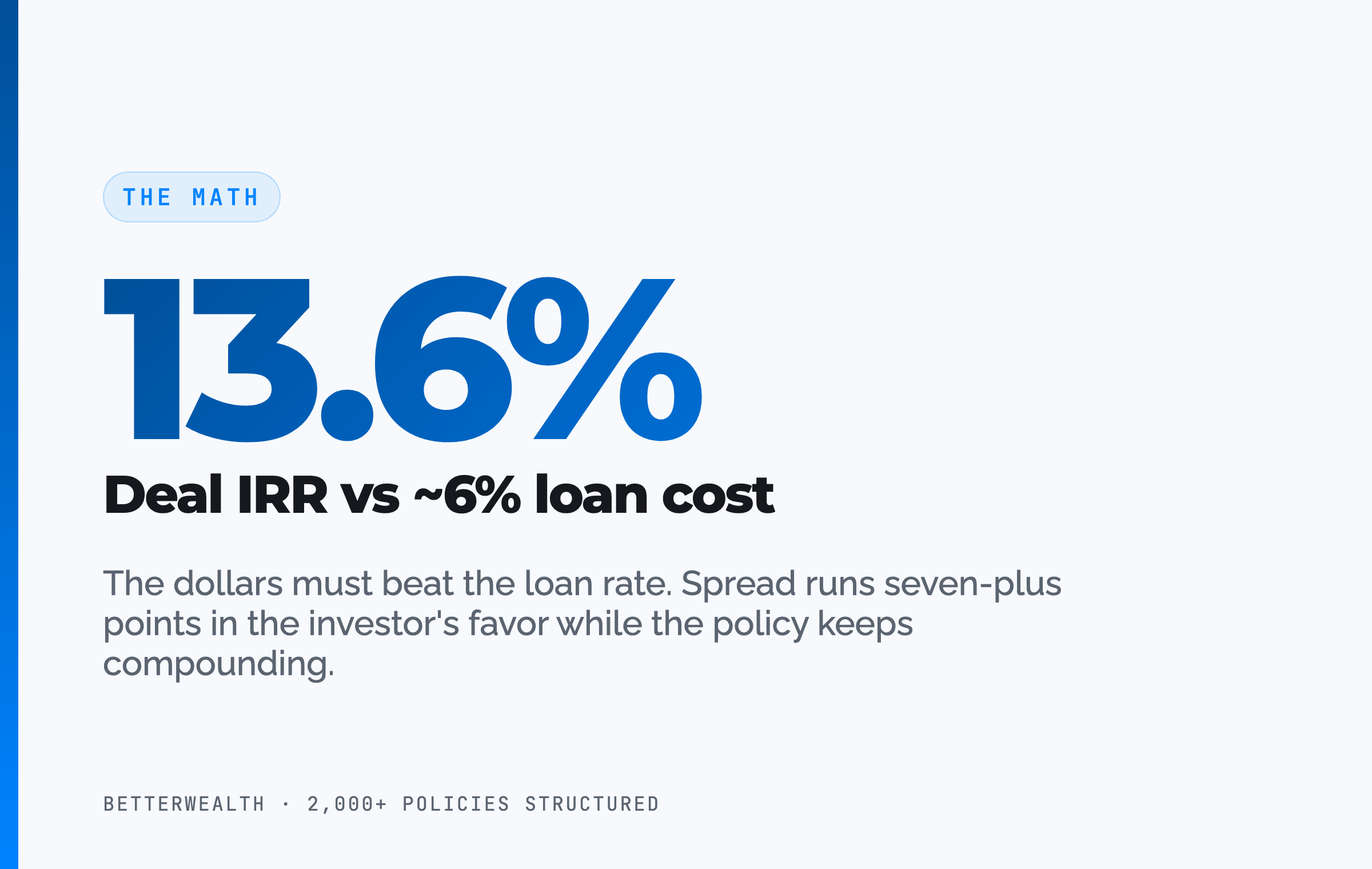

The reason this investor built the policy at all: in an earlier downturn, the bank had frozen his $150,000 HELOC right as a distressed duplex came to market, and he watched the deal go to a cash buyer. In year seven, with roughly $347,000 of accessible cash value, he borrows $174,300 against the policy to acquire a comparable property. No approval, no appraisal delay, no risk of the access being cut. The property returns an estimated 13.6% IRR against an illustrative loan cost near 6 percent, so the spread runs in his favor by more than seven points. The policy keeps compounding on its full value the entire time. Repayment runs on a 38-month schedule funded by the property's own cash flow.

One dollar. Two jobs. That is the And.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and decision tools we use when we compare a policy strategy against a HELOC or a line of credit for a specific situation. Free, email-gated, no spam.

Open the Vault09 / The fitWho should use which, and can you use both?

The right tool depends on your timeline and your tolerance for callability, and for many entrepreneurs the answer is both. A HELOC is the better choice when you need capital now, you already hold home equity, and you do not yet have a funded policy. It solves this month's problem. A whole life policy is the better choice for the next decade of capital needs, when you want a base that cannot be frozen and that keeps compounding while you deploy.

Running them together is common and sensible. Use the HELOC for an immediate opportunity today while you fund a policy on the side. Over ten to fifteen years, the policy becomes a callability-proof capital base that does not depend on a lender's willingness to keep the line open, and the HELOC becomes a backup rather than the foundation. If you cannot identify an activity that beats the loan cost, neither tool is right for you, and no amount of structure changes that.

FAQInfinite banking vs HELOC questions

What is the difference between infinite banking and a HELOC?

A HELOC is a revolving credit line secured by your home equity that a lender can freeze, reduce, or call. Borrowing against a whole life policy is collateralized access to your own cash value that cannot be called, and the policy keeps compounding on its full value while the loan is outstanding. The HELOC is a credit product; the policy is an asset you borrow against.

Can a HELOC be frozen or called?

Yes. A lender can freeze, reduce, or suspend a HELOC if home values fall, your credit profile changes, or the bank tightens its risk posture. Hundreds of thousands of HELOCs were frozen in 2008 and 2009 and again during 2020. A policy loan cannot be called as long as the policy remains in force.

Does a whole life policy keep growing if you borrow against it?

Yes. A policy loan is collateralized by your cash value, not a withdrawal from it, so the full cash value continues to compound net of mortality and expense charges while the loan is outstanding. Home equity behind a HELOC earns nothing, so borrowing against it has no compounding cost and no compounding benefit.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is a HELOC cheaper than a policy loan?

Sometimes the HELOC's stated rate is lower, sometimes higher. HELOC rates are usually variable and reset with the prime rate, so the cost can climb with no warning. Policy loan rates vary by carrier and are often fixed or capped. The honest answer is that rate alone is the wrong comparison, because the HELOC can also be frozen and the policy keeps compounding.

Can you use both a HELOC and an And Asset policy?

Yes, and many entrepreneurs do. A HELOC can cover an immediate need today while a whole life policy is funded for the long horizon. Over time the policy becomes a callability-proof capital base that does not depend on a lender's willingness to keep the line open. The tools are not mutually exclusive.

Why do real estate investors compare infinite banking to a HELOC?

Real estate investors compare the two because both let you access capital for deals without selling assets. The difference that matters to them is control: a HELOC can be frozen in the exact downturn when deals appear, while a policy loan stays available and the policy keeps compounding. Liquidity that disappears under stress is not real liquidity.

How fast can you access cash from each?

A HELOC can fund within days once it is open, but opening it requires underwriting, an appraisal, and approval that can take weeks. A policy loan typically requires no approval or credit check; once the policy has cash value, you request a loan against it and funds are sent directly, often within days.

Is borrowing against life insurance taxable?

Policy loans against a properly structured, non-MEC whole life policy are not treated as taxable income under current tax rules for life insurance. HELOC proceeds are also not taxable income because they are a loan. The tax difference shows up at the asset level, not the loan: cash value grows tax-deferred, while home equity simply tracks the housing market.

When is a HELOC the better choice?

A HELOC is the better choice when you need capital now, you already hold home equity, and you do not have a funded policy yet. A whole life policy takes years to build a meaningful cash value, so it solves the next decade of capital needs, not this month's. If the need is immediate and the equity exists, the HELOC wins on speed.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- Consumer Financial Protection Bureau, how HELOCs work, including the lender's right to freeze or reduce a line.

- IRC Section 7702 (Cornell Law), the tax code provision behind the treatment of life insurance cash value and loans.

- LIMRA, life insurance industry data and persistency benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a policy, a HELOC, or both belong in your plan, book a discovery call. We will tell you if it does not fit.