.png)

Limited-pay whole life insurance is a whole life policy you fund over a fixed, compressed period (commonly 7, 10, or 20 years, or to age 65) instead of for life. After the final payment the policy is paid up, requiring no further premium while it continues to build cash value.

The appeal of limited-pay whole life is obvious before anyone explains the mechanics. Stop writing premium checks after a decade, keep the policy for life. To a high earner with a finite income runway, that sounds like the disciplined choice, and sometimes it is. The problem is that the number on the front of the brochure (7-pay, 10-pay) is treated as a feature when it is really a constraint.

A shorter pay schedule is not a better policy. It is a different set of trade-offs, and the shortest schedules collide with the tax rule that governs how much you can fund a policy at all. Most people who ask for a 7-pay or 10-pay are reaching for an instinct, which is to get the obligation behind them. That instinct is sound. The execution is where designs go wrong.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and limited-pay comes up constantly with business owners planning an exit and professionals who want premiums gone before retirement. This piece covers what limited-pay actually means, how 7-pay, 10-pay, 20-pay, and paid-up-at-65 differ, how the pay schedule changes cash value growth, the Modified Endowment Contract line that short schedules run into, and where limited-pay earns its place in The And Asset framework. We will also name the buyer it does not fit.

- Limited-pay whole life funds a policy over a fixed window (7, 10, 20 years, or to age 65) then requires no further premium for life.

- Shorter schedules mean higher annual premiums for the same death benefit, because you compress the full cost into fewer years.

- The shorter the pay window, the closer the design sits to the MEC line under the 7-pay test in IRC Section 7702A.

- Short pay schedules carry more base premium, which leaves less room for paid-up additions and dampens early cash value efficiency.

- Paid-up means premiums stop, not growth stops: cash value keeps compounding net of mortality and expense charges.

- The And Asset rule still governs: only borrow against the policy when the deployed return clears the carrier's loan cost.

01 / The problemWhat limited-pay actually solves (and what it doesn't)

Limited-pay solves for a finite obligation, not for better policy performance. The structural question it answers is simple: do you want premium payments to end on a known date? For a business owner who expects to sell in twelve years, or a surgeon who wants the policy fully funded before slowing down, ending the obligation on schedule has real value. The commitment is bounded.

What limited-pay does not solve is cash value efficiency. People assume a shorter pay window means a stronger asset. It does not. A shorter window forces more base premium and a higher death benefit per dollar to satisfy the carrier and the tax code, which is the opposite of what maximizes early cash value. The number on the brochure is a payment plan, not a performance rating.

Most people who ask for a 7-pay want premiums gone fast. What they actually want is a policy that builds capital efficiently. Those are not the same design, and they often point in opposite directions.

02 / The frameworkWhat does limited-pay whole life actually mean?

Limited-pay whole life means you pay the full cost of a permanent policy over a set number of years, after which it is paid up and stays in force for life with no further premium. Continuous-pay (sometimes called whole-life-to-100) spreads premium across your lifetime. Limited-pay compresses it. The death benefit is permanent either way. The only thing changing is how the bill is scheduled.

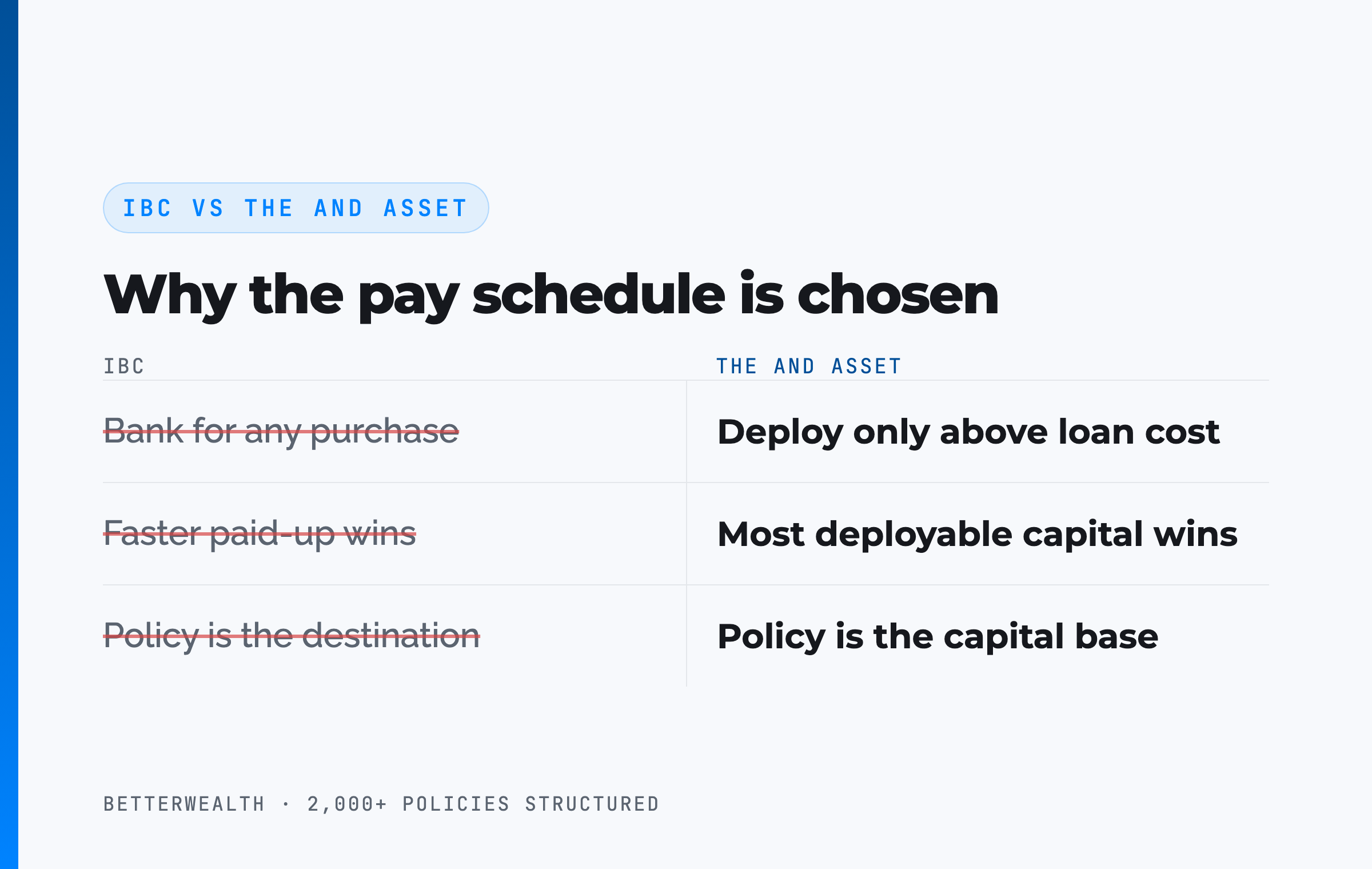

That scheduling decision is where The And Asset framework comes in. Nelson Nash pioneered using whole life as a personal banking system in Becoming Your Own Banker, built on the insight that you either lose money paying interest to outside lenders or lose it to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce, and that rule changes how we choose a pay schedule.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase, so a faster-funded, paid-up policy looks like an unambiguous win. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. That changes the pay-schedule math: a short window that starves your paid-up additions can leave you with less accessible capital in the exact years you want to deploy it. The policy is the capital base, not the destination.

The schedule serves the strategy. Not the reverse.

Marketers sell the short pay window as a finish line. The discipline is not finishing premiums faster. It is funding the policy in the way that leaves the most capital available to deploy.

03 / The schedules7-pay, 10-pay, 20-pay, and paid-up-at-65

The four common limited-pay schedules differ in one variable: how many years you fund before the policy is paid up. Each one moves the annual premium and the funding room in a predictable direction. Shorter means higher premium per year and tighter tax room. Longer means lower premium per year and more flexibility.

- 7-pay. The shortest standard schedule and the most tax-sensitive. The federal 7-pay test measures exactly this window, so a heavily funded 7-pay design sits right at the MEC line. It demands the highest annual premium of the four.

- 10-pay. A 10-pay whole life policy is funded over ten years, then paid up. It is the most popular limited-pay choice because it clears the obligation inside a decade while leaving more design room than a 7-pay.

- 20-pay. Funded over twenty years. The lower annual premium and the wider tax room make it the most flexible limited-pay schedule for building cash value, while still ending well before a typical lifetime.

- Paid-up-at-65. Premiums are scheduled to end at age 65. The length of the window depends on your age at issue, and the design aligns the last payment with the end of your working years.

None of these is "best." A 38-year-old funding for an exit at 50 has a different right answer than a 52-year-old who wants the policy clear before retirement. The schedule is chosen against your income horizon, not against the lowest number available.

04 / How it worksHow a limited-pay policy is set up as an And Asset

A limited-pay policy is set up as an And Asset through five steps, and the order is what keeps a short schedule from quietly working against you. The product is an overfunded whole life policy designed for cash value, not maximum death benefit. Here is the sequence we use.

- Choose the pay window. Pick the schedule against your income horizon and the date you want premiums to stop, not against the shortest number on offer. The window drives every decision that follows.

- Set the base-to-PUA ratio. Design the base premium and the paid-up additions rider together. The shorter the window, the higher the required base premium, which leaves less room for PUAs. A heavily PUA-weighted design, like 40/60 or 10/90, is harder to maintain on a 7-pay than on a 20-pay.

- Check the 7-pay MEC test. Run the design against the 7-pay test under IRC Section 7702A before anything is signed. Short schedules compress premium into fewer years, so they verify against the MEC limit first, every time.

- Fund the schedule and let it capitalize. Pay the required premium every year of the window. Allow the early years to capitalize. A healthy policy does not break even on day one, and any illustration showing year-two break-even is fiction.

- Borrow, deploy, and let it sit paid-up. Borrow against cash value for an activity that beats the carrier's loan cost, repay from the cash flow that activity generates, and after the final premium the policy stays paid up and keeps compounding with no further payment.

How aggressively you can run step two is the whole game, because the base-to-PUA split is what determines early cash value. We walk through exactly how the pay schedule changes the curve in our breakdown of how whole life insurance cash value works, which is worth reading alongside this one if you want to see the mechanics behind the numbers.

Why short schedules dampen early cash value

A short pay window forces a higher base premium, and base premium is the least cash-value-efficient dollar in the policy. The engine of early cash value is the paid-up additions rider, and a 7-pay or 10-pay leaves less of the MEC budget for it. You can still build a strong policy on a 10-pay. You just have less room to optimize than on a 20-pay, and you are paying more per year to have it. That is the trade hiding inside the shorter number.

Fewer years in. Less room to optimize.

Limited-pay fits a specific person with a specific horizon.

It fits you if

- You have a finite income runway (an exit, a retirement date)

- You want premiums to end on a known date

- You can fund the higher annual premium comfortably

- You can name a use for capital that beats the loan cost

It does not fit you if

- Maximum early cash value is your top priority

- You want the lowest possible annual premium

- You are reaching for the shortest schedule on instinct

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you which pay schedule fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The MEC lineDoes a short pay schedule turn the policy into a MEC?

A short pay schedule does not automatically create a Modified Endowment Contract, but it sits closest to the line, and that is the single most important thing to understand about limited-pay. The 7-pay test, enacted by Congress in TAMRA in 1988 and codified in IRC Section 7702A, measures cumulative premium across a policy's first seven years against the amount a true 7-pay paid-up policy would require. Pay in more than that limit and the policy becomes a MEC.

The reason short schedules are dangerous here is mechanical. A 7-pay or 10-pay crams premium into fewer years, which pushes the design toward the exact window the test scrutinizes. Add an aggressive paid-up additions rider on top, which is what you want for cash value, and a poorly engineered short-pay design can cross the line. A 20-pay spreads the same money across more years and breathes easier under the test.

What crossing the line actually costs

A MEC is still a valid life insurance policy, but it loses the favorable tax treatment of distributions. Gains come out on a last-in-first-out basis, taxed as ordinary income, and anything taken before age 59½ carries an extra 10% penalty. For an And Asset strategy that depends on tax-advantaged access to cash value, that is a structural failure, not a footnote. The discipline is to design under the limit on purpose, with margin, not to flirt with it. This is why the schedule and the funding level are engineered together, never separately.

The shortest pay schedule and the most aggressive funding are the two things people want most, and they pull against each other under the 7-pay test. Pick the wrong combination and you build a MEC by accident.

06 / The mathDoes the return clear the carrier's loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow, and a paid-up policy does not change that test. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with the carrier, not a constant.

Here is the structure of the decision on a limited-pay policy. You borrow against cash value at the carrier's loan rate. The policy keeps compounding on its full value, including the borrowed portion, even after it is paid up. Your deployed capital earns its own return. If that return clears the loan cost, you are ahead on the spread, and the same dollar has done two jobs. If it does not, you have borrowed money to lose money slowly. Paid-up status is convenient. It is not a reason to borrow when the math does not work.

If the deal does not clear the loan rate, do not borrow.

07 / The trade-offsBenefits and the four honest trade-offs of limited-pay

Limited-pay's benefits come with four trade-offs that disqualify it for some buyers, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, higher annual premium. You pay the full cost of the policy over fewer years, so a 10-pay premium runs well above a 20-pay or continuous-pay premium for the same death benefit. Second, lower early cash value efficiency, because the higher base premium leaves less room for the paid-up additions that drive early growth. Third, the MEC proximity covered above: short schedules demand careful engineering and leave less funding flexibility. Fourth, less room to flex contributions in a bad year, since the schedule assumes you keep funding the higher premium on time.

Against those trade-offs sits the benefit that defines limited-pay. The obligation ends on a date you choose, and after it ends the policy keeps working. Once paid up, the cash value continues to grow at the dividend rate net of mortality and expense charges, dividends keep getting credited, and the death benefit stays in force for life with nothing further owed. Paid up means no more premiums. It does not mean no more growth.

Higher per year. Fewer years. Then it runs on its own.

The value of limited-pay is not speed. It is certainty: a known end date on the obligation, matched to a known end date on your income. If your income is open-ended, the case for it weakens.

08 / Where people get this wrongThe mistakes that cost capital

The most common mistake is choosing the pay schedule before the design, which gets the order exactly backward. Someone hears "10-pay" at a conference, asks for it by name, and an agent writes it without checking whether a 20-pay would leave more room for the cash value the buyer actually wants. The schedule should fall out of the strategy, not lead it.

The second mistake is overfunding a short schedule into a MEC. The instinct to "max it out" collides with the 7-pay test, and a policy that should have been a clean capital base becomes a tax problem. The third is treating paid-up as the goal. A paid-up policy with little accessible cash value is a finished obligation, not a working asset. For the full picture of where this strategy delivers and where it disappoints, our honest assessment of the pros and cons covers the failure modes in detail, and our breakdown of how to structure a policy shows why design beats schedule selection every time.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we choose between 10-pay, 20-pay, and continuous-pay, and check every design against the MEC line. Free, email-gated, no spam.

Open the Vault09 / The fitWho is limited-pay right for, and who isn't it?

Limited-pay is right for the entrepreneur or high-income earner with a finite income runway who wants the premium obligation to end on a known date and can fund the higher annual cost comfortably. It fits the business owner planning an exit, the professional who wants the policy clear before retirement, and the value creator who has the cash flow to compress payments without straining other deployments. For that profile, a known finish line has genuine value.

It is the wrong choice for someone whose top priority is maximum early cash value, who wants the lowest possible annual premium, or who is simply reaching for the shortest number on instinct. If you cannot name an activity that beats the loan cost, no pay schedule changes the answer, and limited-pay will not change it either.

10 / Head to headLimited-pay against continuous-pay

Compared on the four dimensions that decide a life insurance strategy, limited-pay trades a higher annual premium and tighter tax room for an obligation that ends on schedule. The table sets a 10-pay, a 20-pay, paid-up-at-65, and continuous-pay side by side so the trade is visible at a glance.

| Dimension | 10-Pay | 20-Pay | Paid-Up at 65 | Continuous-Pay |

|---|---|---|---|---|

| Annual premium | Highest of the four for the same death benefit | Moderate; lower than 10-pay | Depends on age at issue | Lowest per year |

| Years you pay | 10, then paid up | 20, then paid up | Until age 65, then paid up | For life (or to 100) |

| PUA / cash value room | Tightest; high base premium crowds out PUAs | Widest of the limited-pay options | Varies with the window length | Most flexible funding room |

| MEC proximity | Closest to the 7-pay line; engineer with margin | More breathing room under the test | Generally comfortable, window-dependent | Furthest from the line |

Annual premium. A 10-pay carries the highest annual premium because the full cost is compressed into a decade. Continuous-pay carries the lowest because it is spread across a lifetime. You are not paying less or more in total so much as deciding how fast to pay it.

Cash value room. The 20-pay leaves the widest room for paid-up additions among the limited-pay schedules, which is why it often wins for buyers who want both a finite obligation and strong early cash value. The 10-pay's higher base premium crowds out the PUA rider.

MEC proximity. The shorter the window, the closer the design sits to the 7-pay test, so the 10-pay demands the most careful engineering and the most margin. Continuous-pay sits furthest from the line and offers the most funding flexibility year to year.

A composite: the founder who chose 20-pay over 7-pay

Consider a 43-year-old business owner, preferred non-tobacco, who came in asking for a 7-pay because he wanted premiums gone before a planned exit. This is a representative composite, not a single named client. He could fund roughly $63,000 a year either way.

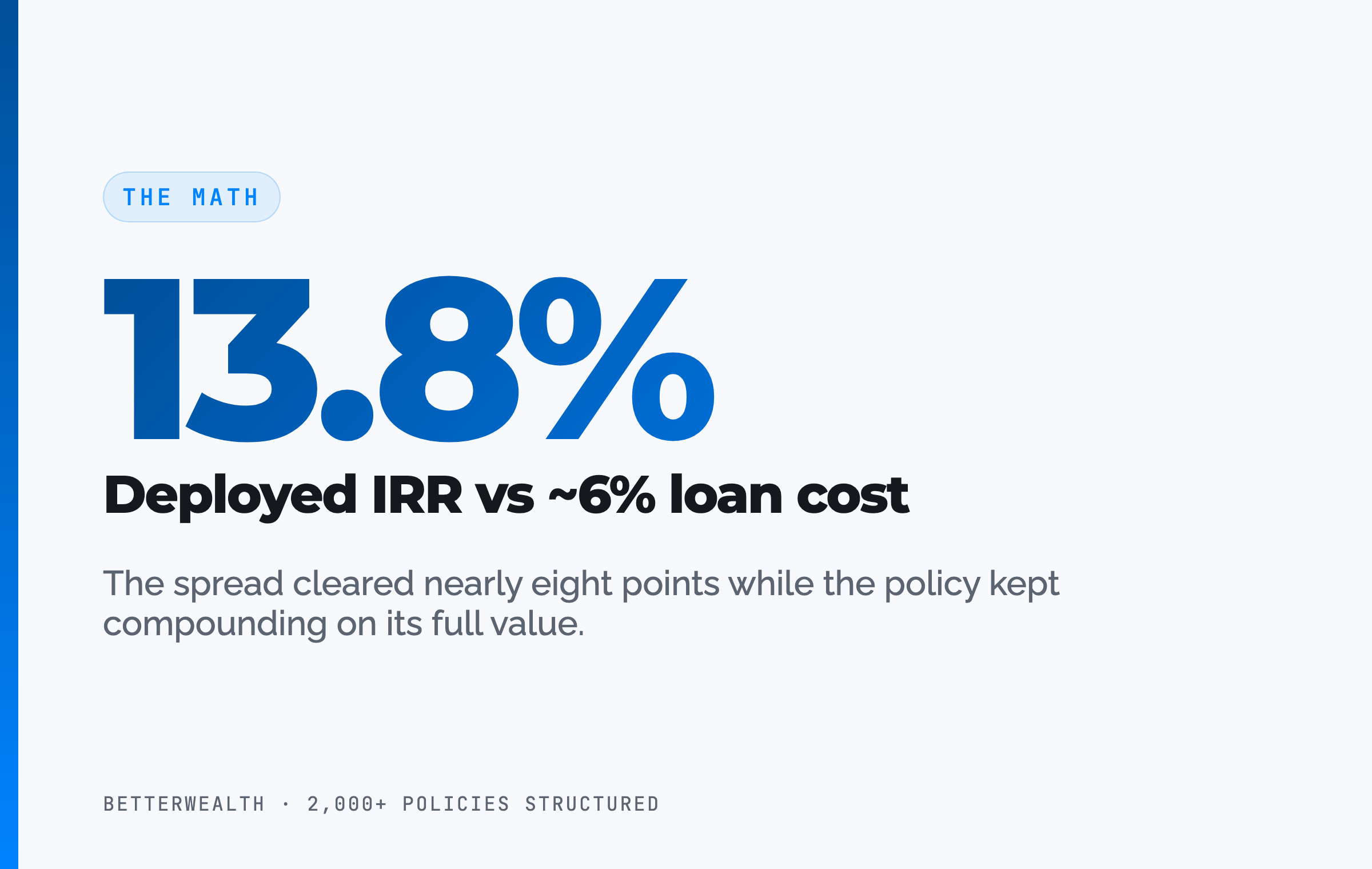

On the 7-pay he asked for, the higher base premium would have consumed most of the MEC budget, leaving thin room for paid-up additions and pushing the design uncomfortably close to the 7-pay line. We modeled a 20-pay instead. Same annual outlay, far more PUA room, more accessible cash value in the years he planned to deploy. Through the first three years cash value trailed cumulative contributions, exactly as a real policy should. At year five it crossed. No earlier.

In year six, with roughly $347,000 of accessible cash value, he borrowed $214,000 against the policy to fund a bulk inventory purchase at a supplier discount. The deployment returned an estimated 13.8% IRR. The loan cost was illustrative at around 6%, so the spread worked in his favor by nearly eight points, and the policy kept compounding on its full value the entire time. Repayment ran on a 29-month schedule funded by the margin the inventory threw off. The 20-pay still pays up before his exit. He just did not need the 7-pay to get there.

One dollar. Two jobs. That is the And.

The honest 30 minutes about which schedule fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your income horizon and tells you whether a 10-pay, a 20-pay, paid-up-at-65, continuous-pay, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQLimited-pay whole life questions

What is limited-pay whole life insurance?

Limited-pay whole life insurance is a whole life policy you fund over a fixed, compressed period (commonly 7, 10, or 20 years, or to age 65) instead of for life. After the final payment the policy is paid up, requiring no further premium while it continues to build cash value and carry a death benefit for life.

What does 10-pay whole life mean?

A 10-pay whole life policy is funded over exactly 10 years. After the tenth payment the policy is paid up, with no further premium owed. The death benefit and cash value continue for life. Each annual premium is higher than a continuous-pay policy for the same death benefit because you are compressing the cost into a decade.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does a short pay schedule make a whole life policy a MEC?

A short pay schedule does not automatically create a Modified Endowment Contract, but it sits closest to the line. The 7-pay test under IRC Section 7702A measures cumulative premium in the first seven years. The shorter the pay window, the more premium is compressed into those years, so a heavily funded 7-pay design is the most likely to cross the MEC limit if it is not engineered carefully.

Is limited-pay or continuous-pay better for cash value?

For maximum cash value efficiency, a longer pay window usually wins because it leaves more room for paid-up additions before the MEC limit. Limited-pay buys more base death benefit per dollar, which is less cash-value efficient early on. Limited-pay's advantage is that premiums stop, which suits a finite income runway, not a goal of maximizing early liquidity.

What does paid-up-at-65 whole life mean?

Paid-up-at-65 whole life is a limited-pay design where premiums are scheduled to end at age 65. It aligns the last payment with the end of your working years, so the policy is fully funded going into retirement. The annual premium falls between a 20-pay and a continuous-pay policy, depending on your age at issue.

Are limited-pay premiums higher than continuous-pay?

Yes. Limited-pay premiums are higher per year than continuous-pay premiums for the same death benefit because you are paying the full cost of the policy over fewer years. A 10-pay premium is higher than a 20-pay premium, which is higher than a continuous-pay premium. You pay more per year but for fewer years, and you stop sooner.

Does the policy still grow after it is paid up?

Yes. Once a limited-pay policy is paid up, no further premium is owed, but the cash value continues to grow at the dividend rate net of mortality and expense charges, and dividends continue to be credited. The death benefit remains in force for life. Paid up means no more premiums, not no more growth.

Who should consider limited-pay whole life?

Limited-pay whole life fits an entrepreneur or high-income earner with a finite income runway who wants premiums to end by a known date, such as a business owner planning an exit or someone who wants the policy paid up before retirement. It is a poor fit for anyone whose main goal is maximum early cash value or the lowest possible annual outlay.

Can I overfund a limited-pay policy with paid-up additions?

You can, but with less room than on a longer schedule. A short pay window carries a higher base premium that consumes more of the MEC budget, leaving less space for the paid-up additions rider. A 20-pay generally allows a more aggressive PUA weighting than a 7-pay or 10-pay while staying under the 7-pay test.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702A (Cornell Law), the 7-pay test and the Modified Endowment Contract definition.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- LIMRA, life insurance industry data, including persistency and product benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you are weighing a 10-pay against a 20-pay or wondering whether limited-pay fits at all, book a discovery call. We will tell you if it does not.