.png)

Infinite banking versus Dave Ramsey is a debate about whether whole life insurance belongs in a wealth plan. Ramsey scores the policy as an investment and rejects it. The strategy treats the policy as a capital base you borrow against to deploy elsewhere, which is a different question entirely.

A man named Jim called the Ramsey Show to say Dave was wrong about infinite banking. He had set up a policy on his five-year-old son, a $500,000 face value funded at $5,373 a year for thirteen years. Within ninety seconds the conversation had become what those conversations always become: a host with the dominant microphone and three decades of reps, and a caller who was never going to get out of the gate.

The whole exchange circled one question. When you die, do you lose your cash value and collect only the death benefit? They argued it for ten minutes. Both of them missed the point.

A properly designed whole life policy is not an investment competing with a mutual fund. It is a capital base you borrow against to deploy into assets that live outside the policy. Score it as an investment and Dave Ramsey is right. The rate of return on the cash value alone is unimpressive. That was never the argument worth having.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we are openly critical of how this strategy gets sold. Marketers have ruined the way it should be explained. This piece walks through the four real claims in that debate, separates what is true from what is theater, and shows where The And Asset framework actually fits. We will also tell you, plainly, who this is not for.

- Dave Ramsey is right that whole life is a poor investment, because a properly designed policy is not an investment at all.

- The cash value funds the death benefit through paid-up additions; on a designed policy the family collects the larger number, not nothing.

- Banks do hold bank-owned life insurance as a tier-one capital asset, though that fact alone does not make it right for you.

- Buy term and invest the difference wins on paper for anyone who actually invests the difference and never touches it.

- The And Asset rule governs everything: only borrow when the deployed return clears the carrier's loan cost.

- For most people, this strategy is the wrong tool, and we say so directly rather than selling around it.

Watching the original call is the fastest way to see why neither side landed a punch. In the full response, we stop the debate at each claim and show where the real disagreement should have been:

01 / The problemWhy did this debate go nowhere?

This debate went nowhere because both men were answering the wrong question. Jim wanted to defend his cash value. Dave wanted to bury the policy as an investment. Neither one stepped back to ask what the policy is actually for, which is the only question that produces a useful answer.

Watch the structure of it. The caller opens by telling a man with three decades on air that he is wrong. The power dynamic is set before a single number gets discussed. From there it is not a conversation, it is a host running his talking points and a caller getting defensive. The audience learns nothing about whether the strategy works, because nobody is talking about the strategy.

The whole exchange majored in a minor. Whether cash value dies with the death benefit is a side issue. The heart of the matter is what you do with the capital, and nobody touched it.

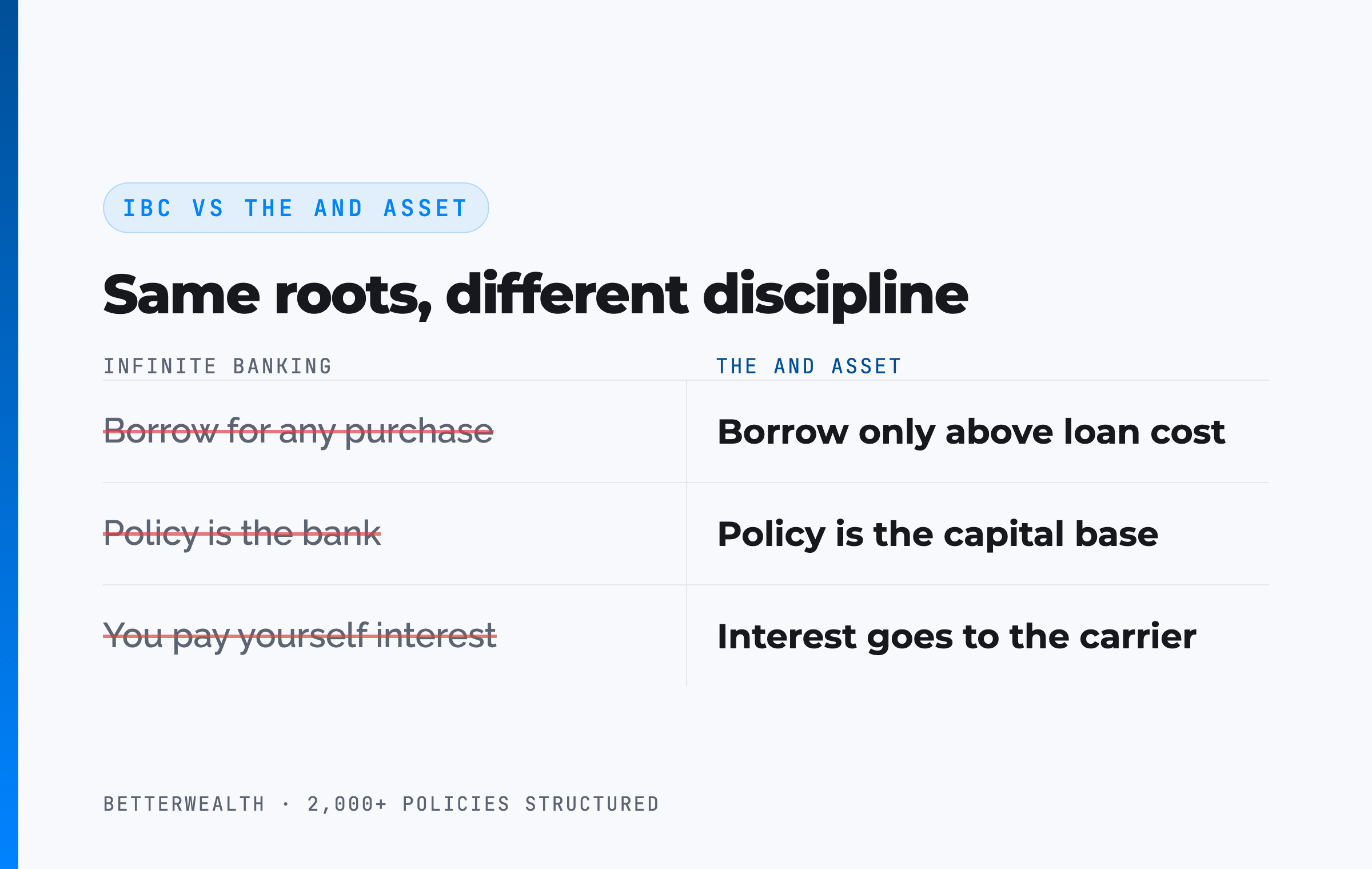

02 / The frameworkWhat is infinite banking really, and how does The And Asset differ?

Infinite banking is using a properly structured whole life policy as a personal capital base you borrow against, while the policy keeps compounding net of mortality and expense charges. That is the mechanical definition. The discipline we layer on top of it is what we call The And Asset.

Nelson Nash pioneered the idea in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase, including the car and the vacation. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The distinction matters here because the entire Ramsey objection assumes the casual version. He is right to attack it. We attack it too.

One correction that neither side made cleanly: you are not paying yourself interest. The interest on a policy loan goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy compounds uninterrupted. Marketers who promise you are your own bank earning your own interest have ruined how this should be explained.

The math has to work. Every time.

This is not infinite banking the way most people teach it. The policy is the capital base. The value is created in what you deploy that capital into.

03 / Claim oneDo you really lose your cash value when you die?

You do not get the cash value paid on top of the death benefit, and on a well-designed policy that is not the loss it sounds like. Here is what Dave got technically right and what he framed misleadingly. On a traditional policy, the death benefit is paid and the cash value is absorbed into it. So far, so accurate.

What he glossed over is the design the caller was describing. When you overfund a policy and reinvest dividends into paid-up additions, the death benefit grows year after year. Those paid-up additions are small chunks of fully paid-up insurance, and they push both the cash value and the death benefit higher. The family does not collect nothing extra. They collect a death benefit that grew precisely because the cash value was working.

In the readout Dave himself cited, at age 80 the cash value was about $2 million and the death benefit about $2.6 million. The death benefit is larger because the policy was designed to grow, not shrink. Calling that a stolen cash value is rhetoric, not math.

If your death benefit is not increasing by more than you contribute, Dave is right and you have a badly designed policy. On a real And Asset design, it does increase. That is the whole point of the paid-up additions rider.

04 / How it worksHow a policy functions as an And Asset, step by step

A whole life policy functions as an And Asset through five steps, and the order is what the debate never reached. The product is a whole life policy designed for maximum cash value rather than maximum death benefit. Here is the sequence we use when we structure one.

- Separate the insurance from the strategy. Stop scoring the policy against the S&P 500. It is a capital base, not a fund. This single reframe ends most of the Ramsey debate before it starts.

- Design for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows without triggering a Modified Endowment Contract. The base/PUA split is the design decision that determines early cash value. A common structure runs 40/60 or more aggressive.

- Let the early years capitalize. Cash value does not exceed cumulative contributions before year four. Break-even lands at year five or later for a healthy individual. Any illustration showing day-one break-even is fiction, and Dave is right to mock it.

- Borrow against the policy. Take a policy loan collateralized by your cash value. The full cash value continues to compound net of mortality and expense charges while the loan is outstanding. You are borrowing against the asset, not draining it.

- Deploy where the return beats the loan cost. Put the borrowed capital into real estate, a business, or another activity whose return exceeds the carrier's loan rate. If you cannot name one, do not borrow.

That fifth step is where Dave and the strategy actually agree, and neither realized it. Dave preaches opportunity cost. So do we. The disagreement is only whether a disciplined investor can capture a spread between the loan cost and a real return. For the right person, doing real things with capital, the answer is yes.

If you want the full mechanics of how the loan and the compounding interact, we walk through them claim by claim in the response:

This strategy fits a specific person doing specific things.

It fits you if

- You are an entrepreneur or investor already deploying capital

- You can name a use that beats the loan cost

- You have a 10-year-plus capital horizon

- You understand IRR and opportunity cost

It does not fit you if

- You are early in building wealth

- You want a savings account alternative

- You are in high-interest debt seeking a quick fix

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether this belongs in your plan. If you are in the second, we will tell you that too, and Dave Ramsey's advice may serve you better.

Book a Discovery Call05 / Claim twoIs buy term and invest the difference simply better?

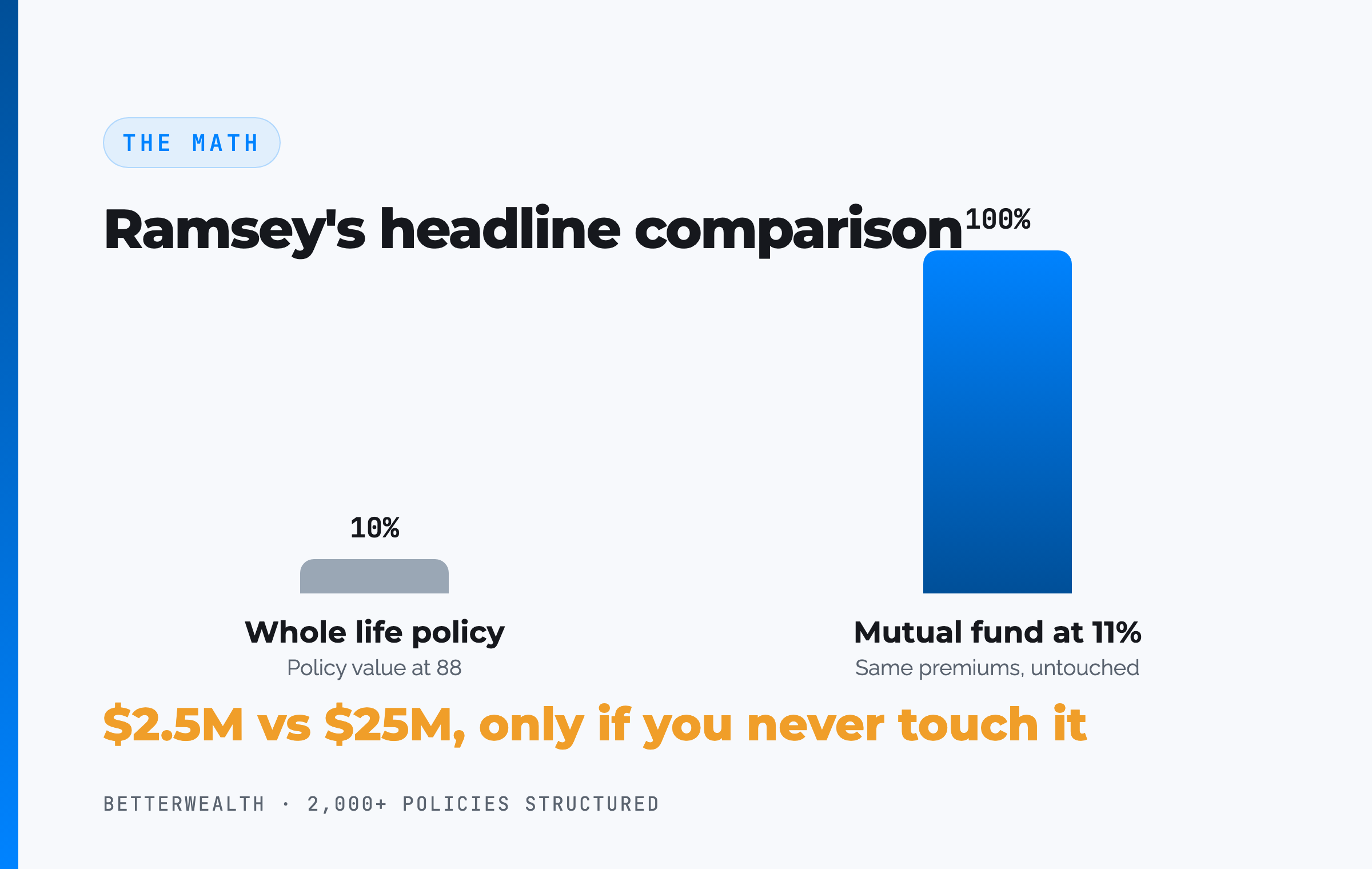

Buy term and invest the difference produces a larger paper number for anyone who actually invests the difference and never touches it. That is the honest answer, and pretending otherwise is how agents lose credibility. Dave's $25 million versus $2.5 million comparison is real arithmetic at 11% compounded over a lifetime.

Two things break the comparison in practice. First, almost nobody leaves money invested and untouched for decades. People pull capital out for college, cars, homes, and opportunities, and every withdrawal interrupts the compounding Dave's number depends on. Second, term insurance becomes expensive and often unavailable in the years when the likelihood of death is highest. The plan that assumes cheap term at 75 is assuming something that rarely exists.

The deeper flaw is the framing. Dave compares the policy, doing nothing, against a mutual fund doing everything. That is not an apples-to-apples comparison. The strategy was never to leave money sitting in the policy. It was to borrow against it and deploy. Compare a deployed And Asset to an untouched mutual fund and you are comparing two different strategies, not two different products.

The number assumes you never touch it. Almost nobody never touches it.

06 / Claim threeDo banks actually use whole life insurance?

Yes, banks hold whole life insurance, and Dave was simply wrong on this point. The asset is called bank-owned life insurance, or BOLI, and thousands of US banks carry it as a tier-one capital asset, primarily to fund employee benefit obligations. It shows up on call reports. This is verifiable, not a TikTok claim.

What it is not is a bond replacement or an investment account, and it does not prove the strategy is right for an individual. Banks use BOLI for tax-advantaged, stable cash value against a long obligation. That an institution finds the asset class useful tells you the asset class is real. It does not tell you it fits your situation. We hold both of those truths at once, which is more than either side of the call managed.

Banks holding life insurance is a fact, not an endorsement of your policy. The question is never whether the asset class exists. It is whether you can deploy capital well enough to justify it.

07 / The deeper pointWhy is net worth on paper the wrong scoreboard?

A bigger number on paper does not always mean a better outcome, which is the idea the whole debate needed and never reached. Dave's scoreboard is accumulation: the largest possible balance at 88. It is a clean metric and it is not wrong for most savers. It is also incomplete for someone whose goal is usable capital and cash flow across a lifetime.

Consider two portfolios. One shows a larger balance but throws off less spendable cash flow. The other shows less on paper but produces more usable income and more control over when and how you access it. For an entrepreneur or value creator, the second can be the better asset even though it loses the net-worth contest. Liquidity, control, and tax treatment do not show up in a single compounding number.

This is why we keep returning to cash flow rather than balance. The end result that matters is what your capital can do for you, now and into the future, not the largest figure on an illustration.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and the actual math behind the loan-versus-deploy decision the Ramsey debate never reached. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsWhere Dave Ramsey is right, and where he stops short

Dave Ramsey is right about more than his critics admit, and pretending he is a fool is its own credibility failure. He is right that whole life is oversold. He is right that most people who buy it would be better off with term insurance and disciplined investing. He is right that an illustration promising early break-even is garbage. He knows the terminology cold, which is more than most agents arguing with him can say.

Where he stops short is the assumption that everyone is the same buyer. His framework is built for the person climbing out of debt and building a first nest egg, and for that person it is excellent advice. It does not account for the entrepreneur who already deploys capital, who values control and liquidity, and who can capture a spread between the loan cost and a real return. For that person, a different tool applies. The mistake is universalizing one answer to every situation.

The honest tradeoffs of the strategy are real. Low early cash value. A long horizon before it works. A discipline requirement most people will not meet. We lead with those, because the discipline of repayment is the whole strategy.

He is right for most people. He is wrong that there is only one kind of person.

09 / The fitWho is this actually for, and who is it not?

This strategy is for the entrepreneur, business owner, real estate investor, or high-income earner who already deploys capital and can name a use that beats the loan cost. It fits the value creator with a long horizon who understands that idle capital carries an opportunity cost and wants control over when and how they access money.

It is the wrong tool for someone early in building wealth, someone who wants a savings vehicle, someone in high-interest debt looking for a quick fix, or anyone who cannot identify a productive use for borrowed dollars. For that person, Dave Ramsey's advice is the better advice, and we will say so on the call. If you cannot find a use that beats the loan cost, do not borrow, and probably do not buy the policy.

10 / Head to headThe And Asset against the alternatives

Compared to the tools in the Ramsey debate, an And Asset policy trades the highest paper balance for control, tax treatment, and uninterrupted compounding. The table sets it against buy term and invest the difference, a 401(k), and a taxable brokerage account on the dimensions that matter for life insurance strategy.

| Dimension | The And Asset | Buy Term + Invest | 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Growth | Compounds net of internal costs, even while borrowed against | Full market growth if never touched | Market growth, tax-deferred | Market growth, taxed annually on gains |

| Liquidity | Policy loans after capitalization; cannot be called | Brokerage is liquid; term has no cash value | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

| Tax treatment | Policy loans are not taxable income under IRC 7702 | Capital gains taxed on sale | Deferred now, taxed as ordinary income later | Capital gains and dividends taxed yearly |

| Discipline required | High: must deploy above the loan cost | High: must actually invest and never touch it | Low: payroll-automated | Medium: self-directed |

Growth. A policy keeps compounding on its full value while you borrow, which an untouched brokerage cannot do because withdrawing capital stops it from compounding. That is the structural feature that lets one dollar do two jobs.

Liquidity and discipline. Buy term and invest the difference wins on paper, but only under a discipline most people never sustain. Both strategies demand discipline. One demands you never touch the money. The other demands you only borrow when the return clears the loan cost.

Tax and control. Policy loans are not taxable income under Section 7702, and a 401(k) restricts access until 59½ under rules set by Congress. The And Asset trades the largest possible paper balance for control and tax treatment you keep.

A composite: the operator who answered the question the call never asked

Consider a 43-year-old business owner, preferred non-tobacco, funding an overfunded whole life policy at $48,000 per year on a maximum-cash-value design. This is a representative composite, not a single named client, and it is the answer to the question the Ramsey debate never reached: what do you actually do with the capital?

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year four, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is the marketing fiction Dave Ramsey rightly attacks.

In year six, with roughly $312,000 of accessible cash value, the owner borrows $164,000 against the policy to acquire a rental property at a discount. The property and its rents return an estimated 13.8% IRR. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by nearly eight points. The policy keeps compounding net of mortality and expense charges the entire time. Repayment runs on a 41-month schedule funded by the property's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes the caller never got.

We have structured more than 2,000 policies across all 50 states. We have seen this strategy work exactly as designed, and we have seen it fail. On a discovery call, a practitioner looks at your specific situation and tells you whether this belongs in your plan or whether Dave Ramsey's advice fits you better. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQInfinite banking vs Dave Ramsey questions

Is infinite banking a scam, as Dave Ramsey says?

Infinite banking is not a scam, but it is widely oversold. Dave Ramsey is right that whole life is a poor investment when scored as one, because it is not an investment. It is a capital base you borrow against to deploy elsewhere. The strategy creates value only when the deployed capital out-earns the carrier's loan cost.

Do you lose your cash value when you die with whole life insurance?

The beneficiary receives the death benefit, which on a properly designed policy already includes the growth your cash value funded through paid-up additions. The cash value is not paid on top of the death benefit, but it is not lost either, because it built the larger death benefit your family collects.

Do banks actually use whole life insurance?

Yes. Banks hold bank-owned life insurance (BOLI) as a tier-one capital asset, primarily to fund employee benefit obligations. It is not a bond replacement or an investment account, and it does not prove the strategy is right for an individual. It does show the asset class is used at institutional scale.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding net of mortality and expense charges while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds one discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is buy term and invest the difference better than whole life?

For most people who will actually invest the difference consistently and never touch it, buy term and invest the difference produces a larger paper number. The gap is that few people leave money untouched for decades, and term insurance becomes expensive or unavailable in the years when the likelihood of death is highest. The right answer depends on whether you will deploy capital with discipline.

What are paid-up additions?

Paid-up additions are small chunks of fully paid-up whole life insurance you purchase with extra premium or with dividends. They are the engine of early cash value in a policy designed for the infinite banking or And Asset strategy. The base-to-PUA ratio, often 40/60 or 10/90, determines how fast cash value builds.

Why did neither side win the Dave Ramsey debate?

Both sides argued whether cash value dies with the death benefit, which is a side issue. Neither addressed the heart of the matter: a whole life policy is a place to warehouse capital that you then deploy into assets outside the policy. The debate compared the policy to a mutual fund as if they were the same category. They are not.

Does a whole life policy really only earn around 4%?

Cash value grows at the dividend rate net of mortality and expense charges, which on many policies lands in the low single digits as an internal rate of return over the long term. That number is not the point of the strategy. The return comes from what you deploy the borrowed capital into, on top of the policy continuing to compound.

Who should not use infinite banking or The And Asset?

Anyone in the early stages of building wealth, anyone looking for a savings account alternative, anyone in high-interest debt looking for a quick fix, and anyone who cannot identify a use for borrowed capital that beats the loan cost. For most people, this is not the right strategy, and we say so directly.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- FDIC, bank call-report data on bank-owned life insurance (BOLI) holdings.

- LIMRA, life insurance industry data on persistency and ownership.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether this strategy fits you, or whether it does not, book a discovery call. We will give you the real answer either way.