.png)

The wealthy use life insurance as a capital and estate tool, not a death benefit product. SEC chairman Paul Atkins disclosed 54 policies in 2025, mostly universal life, structured for estate planning, business buy-sell agreements, and tax-efficient legacy transfer rather than pure protection.

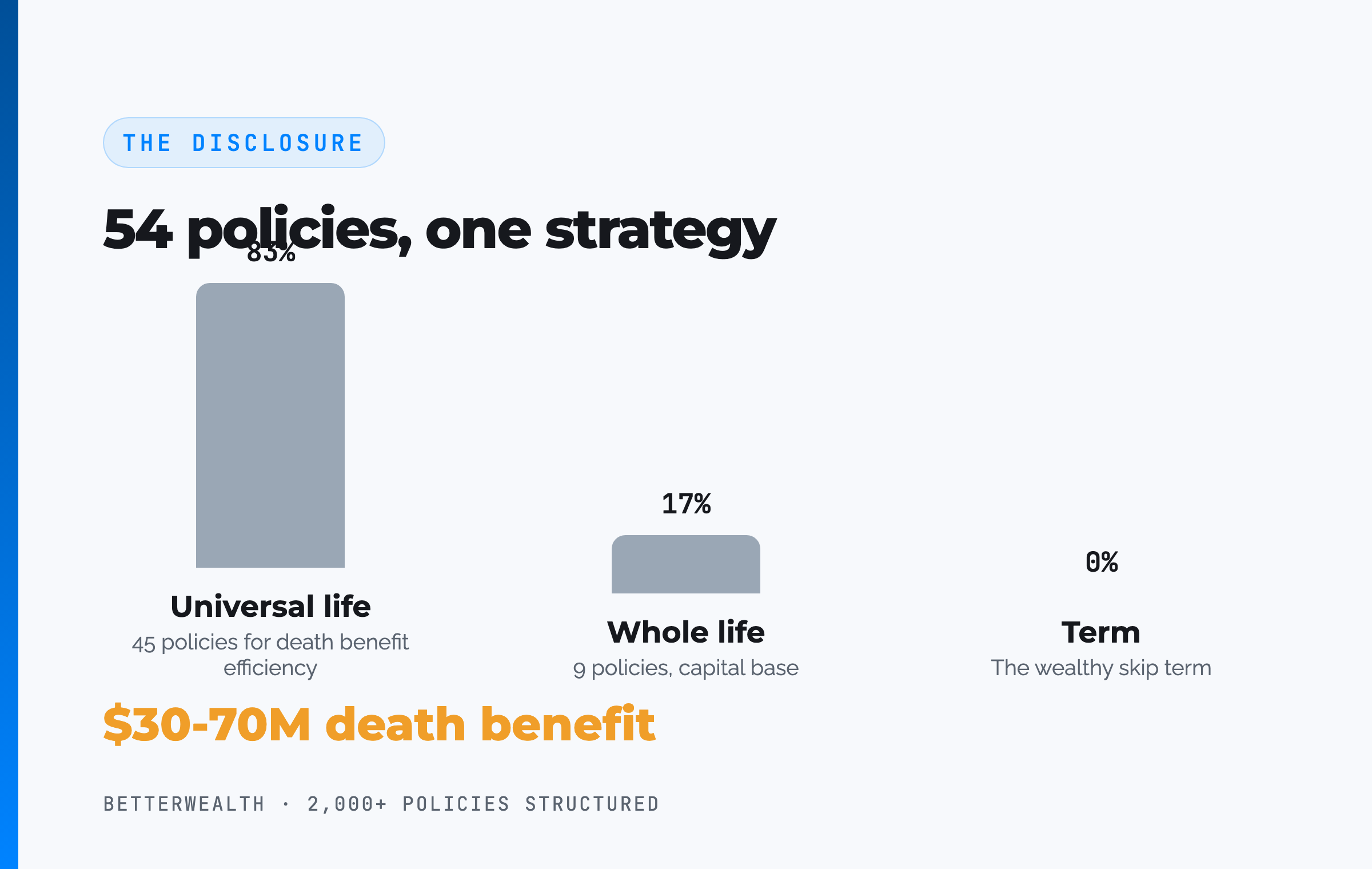

A mandatory ethics disclosure put a number on something practitioners already knew. Paul Atkins, the chairman of the SEC, holds 54 life insurance policies with an estimated $30 to $70 million of death benefit. Nine are whole life. Forty-five are universal life. None are term. The financial press treated it as a curiosity. It is not a curiosity. It is a window into how serious capital actually treats life insurance.

The wealthy do not buy life insurance to replace an income. They use it as a capital base, an estate vehicle, and a tax-efficient way to move wealth, and the product itself is almost beside the point. Banks call it BOLI. Corporations call it COLI. The mechanics are the same: park capital somewhere it grows on a tax-advantaged basis, stays accessible, and pays out efficiently to the next generation or the next venture.

At BetterWealth, we have structured more than 2,000 policies across all 50 states. We see this pattern at the high end constantly, and we see it misread constantly. The skeptics call it a scam. The marketers call it free money. Both are wrong, and the truth is more useful than either. This breakdown covers what Atkins' disclosure actually shows, why high-net-worth families stack policies the way he has, where The And Asset framework diverges from generic infinite banking, and the one objection that confuses almost everyone: what happens to your cash value when you die.

- Paul Atkins disclosed 54 policies: 9 whole life, 45 universal life, 0 term, worth an estimated $30 to $70 million.

- That death benefit is roughly 10% of his $327 million net worth, which suggests he may be underinsured for his estate.

- The wealthy use life insurance for estate planning, trusts, business buy-sell agreements, key-person coverage, and capital access.

- Universal life is common at the high end because it holds a large death benefit efficiently when early cash value is not the goal.

- The And Asset rule still governs: only borrow against a policy when the deployed return beats the carrier's loan cost.

- You borrow against the death benefit, with cash value setting the ceiling, which is why the cash-value-disappears objection misreads the asset.

Caleb and Dom read the full disclosure on screen, company by company, and answer live viewer questions on the death benefit versus cash value debate that the article summarizes below:

01 / The problemWhat the headline gets wrong about wealthy life insurance

The headline frames 54 policies as excess, and that framing is the error. Most coverage of the Atkins disclosure counted the policies, multiplied by the death benefit range, and stopped there. The interesting question is not how much insurance he owns. It is why someone worth $327 million would structure his affairs around dozens of separate contracts instead of one large policy.

The answer is that he almost certainly is not the only insured. A single individual rarely passes underwriting on 54 policies. As we noted on the show, it is hard to imagine anyone taking 54 health exams. Far more likely, these contracts cover business partners, family members, and key people across his many entities, with Atkins retaining an ownership interest he was required to disclose. Ownership and insured are not the same thing, and conflating them is how the headline misleads.

"It is such a scam that the chairman of the SEC has it. It is such a scam that most corporations utilize this." The sarcasm is the point. Serious capital has used this tool for a century.

02 / The factsWhat did Paul Atkins actually disclose?

Atkins disclosed 54 life insurance policies spread across at least 17 carriers, dominated by universal life rather than the whole life most people associate with this strategy. The roster runs from household names to insurers even practitioners rarely encounter. He holds policies with MassMutual, Penn Mutual, Pacific Life, John Hancock, Prudential, Lincoln Financial, and Equitable, alongside National Life Group, Zurich American Life, Security Life of Denver, Brighthouse, Sun Life, Genworth, Talcott Resolution, Principal, American General, and a single policy with Jackson National.

The split tells the story. Forty-five universal life contracts against nine whole life suggests the priority is death benefit efficiency, not early cash value. The range on individual policies is wide, from one National Life Group policy estimated as high as $26 million of death benefit down to contracts under $1 million. That spread is what you would expect from a portfolio assembled over decades for different purposes, not a single planning event.

Fifty-four policies. One coherent strategy underneath.

03 / The reasonsWhy do the wealthy own this much life insurance?

The wealthy own this much life insurance because a single policy can solve estate, business, and tax problems that no other asset solves at once. Strip the disclosure down and you find four recurring jobs, and most high-net-worth portfolios use the tool for several of them simultaneously.

Estate and legacy transfer

Life insurance moves wealth to heirs and causes with unusual efficiency. The death benefit is generally received income-tax-free by the beneficiary under IRC Section 101, and held inside an irrevocable life insurance trust it can pass outside the taxable estate while providing liquidity to cover estate taxes. For someone with illiquid holdings in operating companies, that liquidity prevents heirs from having to sell the business to pay the IRS. This is the play most experts assume drives the Atkins portfolio.

Business continuity

Buy-sell agreements funded with life insurance let surviving partners buy out a deceased owner's stake without scrambling for cash. Key-person coverage protects a company against the loss of someone whose departure would impair its value. Atkins founded or backed multiple ventures across crypto, tokenization, and financial services, and each partnership is a candidate for exactly this structure. One reason to hold many small policies is simple discipline: a separate contract for each agreement and each partner.

Tax-efficient accumulation

For high earners who have already maxed their 401(k) and Roth options, cash value life insurance offers another bucket of tax-advantaged growth. Cash value compounds on a tax-deferred basis, policy loans are not treated as taxable income while the policy stays in force, and the death benefit pays out income-tax-free. A professor quoted in the coverage put it bluntly: these vehicles are not the first stop, but for someone who has exhausted the traditional accounts, they earn their place.

Relationship and giving capital

As Caleb noted on the show, the wealthy increasingly earmark a death benefit for foundations, churches, and nonprofits. Naming an institution as a beneficiary is a legacy decision and a network decision at once. The Rockefellers built durable influence partly by directing capital toward institutions, and a life insurance death benefit is one of the cleanest ways to fund that kind of giving across generations.

He holds death benefit equal to about 10% of his net worth. For his estate and business obligations, that may make him underinsured, not over-insured.

04 / The frameworkWhere does The And Asset diverge from infinite banking?

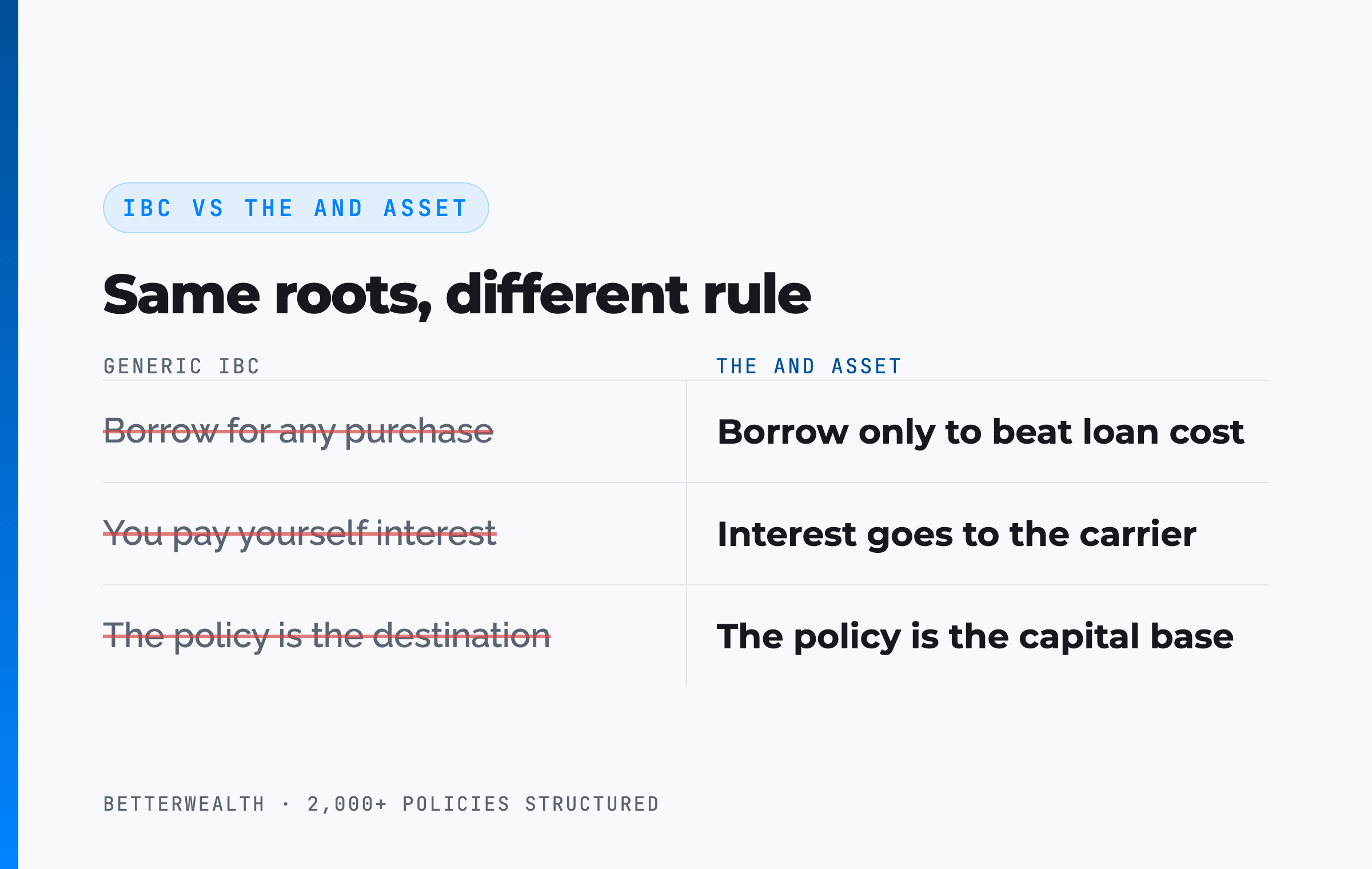

The And Asset diverges from infinite banking at the point of discipline: you only borrow against a policy when the deployed capital out-earns the carrier's loan cost. Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds. You either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule the broader teaching does not enforce.

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges.

The Atkins disclosure is a useful reminder of where this fits. His universal life holdings look like an estate and death-benefit play, which is a legitimate use of insurance but a different use than The And Asset. The And Asset is a capital-deployment strategy for entrepreneurs and value creators who will actually borrow and redeploy. It shares roots with IBC but operates on different principles.

The math has to work. Every time.

This strategy fits a specific person doing specific things.

It fits you if

- You are an entrepreneur or high-income earner with capital to deploy

- You have estate, business, or legacy obligations beyond income replacement

- You can name a use for borrowed capital that beats the loan cost

- You think in IRR and opportunity cost, not just savings

It does not fit you if

- You are early in building wealth and need every dollar liquid

- You want a savings account, not a life insurance strategy

- You are looking for a quick fix for high-interest debt

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether this belongs in your capital structure. If you are in the second, we will tell you that too.

Book a Discovery Call05 / How it worksHow a policy actually functions as a capital base

A properly structured whole life policy functions as a capital base through five mechanical steps, and the order matters. This is the design we use when the goal is capital access rather than the death-benefit-first design that likely dominates the Atkins portfolio.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows without tipping the policy into a Modified Endowment Contract. The PUA rider is the engine. Without it, this is an expensive death benefit.

- Fund consistently. Choose a cashflow design (level premium) or a front-load design (more in year one, then level). A 10 to 25 year funding horizon is typical for this structure.

- Let the early years capitalize. Early cash value trails cumulative contributions on purpose. Do not expect day-one break-even. Any illustration that shows it is fiction.

- Borrow against the policy. Take a policy loan collateralized by the death benefit, with cash value setting how much you can access. The death benefit and cash value still belong to you.

- Deploy and repay. Put the borrowed capital into an activity that beats the carrier's loan cost, then repay from the cash flow that activity throws off. The policy compounds on its full value the entire time.

The capitalization point, where a dollar of premium adds more than a dollar of cash value, typically arrives around year three on a well-designed policy. Break-even, where total cash value catches total contributions, lands at year five or later for a healthy individual. No earlier.

06 / The objectionDo your heirs really lose the cash value when you die?

Your heirs receive the death benefit, not the death benefit plus a separate cash value, because cash value and death benefit are one asset, not two. This is the single most repeated objection to permanent life insurance, and critics like Dave Ramsey lean on it hard. It sounds damning until you look at the actual numbers on a policy with a growing death benefit.

Take a simplified example. Bobby has a $1 million death benefit and over his life contributes $400,000, which grows to roughly $500,000 of cash value. If both passed separately, his heirs would receive $1.5 million. Now take Susan, who runs a properly designed policy. Her $500,000 of cash value is part of her death benefit, and her death benefit has grown from $1 million to $2 million. Susan's heirs receive $2 million income-tax-free, more than Bobby's supposed $1.5 million. The cash value did not vanish. It was always one component of a death benefit that grew past it.

The honest exception

This is not universal, and pretending it is would be the kind of overselling we criticize. When a policy uses a term rider, common on front-load designs and on carriers like a Guardian Q-Term structure, the death benefit can start level and step down once the rider drops off. In those cases the throw-a-dart-at-any-year logic does not hold cleanly. With a carrier like Penn Mutual, where the blended paid-up additions design drives a permanent death benefit that grows as additions are paid, the increasing-death-benefit case is real. Design determines the answer.

The death benefit is almost like a cosigner that lets you borrow against your cash value at favorable rates with no fixed repayment schedule. Remove it and that access would not exist.

07 / The productsWhat is the difference between whole life and universal life?

Whole life carries fixed premiums and guaranteed cash value growth plus non-guaranteed dividends, while universal life offers premium flexibility and is often used to hold a large death benefit at lower internal cost. That difference explains why Atkins holds 45 universal life policies and only 9 whole life. When the objective is maximum death benefit for estate and trust planning, universal life frequently carries that death benefit more cheaply than whole life, especially when early cash value is not a priority.

For The And Asset, the calculus is different. We build on whole life because the guaranteed cash value growth and dividend structure create a stable, predictable capital base you can borrow against decade after decade. A high-net-worth estate plan and a working life insurance strategy are not the same job, and they do not always use the same chassis. Both are legitimate. The mistake is assuming one product fits every goal.

A note on age, since the show fielded this question. For a 69-year-old whose goal is death benefit, the cost of insurance inside whole life runs high, so an indexed universal life or a single-premium MEC design can sometimes fit better. The answer depends on the goal, the health rating, and the carrier, which is why the numbers should be run and stress-tested rather than assumed.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to compare whole life and universal life designs across carriers. Free, email-gated, no spam.

Open the Vault08 / The mathDoes the deployed return clear the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow. This is the entire test, and it is what separates a life insurance strategy from an expensive habit. Policy loan rates vary by carrier and rate environment. At the time of writing many carriers fall in the 5 to 6% range, but treat any specific number as a variable to verify with the carrier, not a constant.

The structure of the decision is simple. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, including the borrowed portion, net of mortality and expense charges and adjusted by the carrier's loan recognition method. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread and the same dollar has done two jobs. If it is lower, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

09 / Where people go wrongThe two errors that ruin this strategy

People go wrong in two opposite directions, and both come from treating life insurance as a product rather than a strategy. The first error is the skeptic's: dismissing the entire category as a scam because a death benefit is not a stock-market return. That comparison is a category mistake. Life insurance is a capital and estate tool, and judging it against an equity index is like judging a moving truck against a sports car.

The second error is the marketer's: selling the strategy as free money, promising you can pay yourself interest, and implying everyone should own one. Marketers have ruined how this strategy gets explained. You are not paying yourself interest. The interest goes to the carrier. The strategy is not for everyone, and the honest version says so up front. Both errors skip the only question that matters, which is whether the structure fits your specific situation and whether borrowed capital can clear the loan cost.

People cannot help themselves. The skeptic calls it a scam, the marketer calls it magic, and the disciplined entrepreneur quietly uses it the way Atkins and the corporations do.

A composite: the business owner who funded a buy-sell and a capital base at once

Consider a 47-year-old business owner, preferred non-tobacco, with two operating partners. He funds a Penn Mutual whole life policy at $52,000 per year on a cashflow design, structured to serve double duty: a buy-sell funding source and a capital base he can borrow against. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. Any illustration showing year-two break-even is marketing fiction.

In year eight, with roughly $384,000 of accessible cash value, he borrows $214,000 against the policy to fund an equipment purchase for the business. The deployed capital returns an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread works in his favor by nearly eight points. The policy keeps compounding on its full value the entire time, and the death benefit still backs the partners' buy-sell agreement. Repayment runs on a 43-month schedule funded by the equipment's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a properly designed policy, an estate structure, or nothing at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call10 / Head to headWhole life, universal life, and term for the wealthy

Compared on the jobs the wealthy actually hire insurance to do, the three policy types solve different problems, and the right one depends on the goal. The table sets them against the four dimensions that decide which contract fits which purpose.

| Dimension | Whole Life | Universal Life | Term |

|---|---|---|---|

| Primary job | Capital base you borrow against (The And Asset) | Large death benefit held efficiently for estate planning | Temporary income replacement for a fixed period |

| Cash value | Guaranteed growth plus non-guaranteed dividends, net of charges | Interest or index-linked, more variable, often lower early | None |

| Premium | Fixed and contractual | Flexible within limits | Fixed, low, for the term only |

| Best for | Entrepreneurs deploying capital with discipline | High-net-worth estate and legacy transfer | Young families covering a defined obligation |

Whole life. The guaranteed cash value and dividend structure make whole life the stable base The And Asset is built on, because you can borrow against it predictably for decades. The tradeoff is higher cost than universal life when the only goal is death benefit.

Universal life. When the objective is to hold a large death benefit at lower internal cost, as the Atkins portfolio appears to, universal life often wins. It is an estate tool more than a capital-deployment tool, and indexed versions add market-linked growth with their own caps and risks.

Term. Term has no cash value and expires. It is the right tool for covering a defined obligation cheaply, which is exactly why a portfolio built for estate and life insurance strategy, like Atkins', holds zero term.

For the deeper walkthrough of how a paid-up additions rider and base premium split drive cash value, we broke down policy structure here:

FAQWhy the wealthy use life insurance: common questions

Why do wealthy people own so many life insurance policies?

Wealthy people use life insurance for estate planning, business buy-sell agreements, key-person coverage, tax-efficient legacy transfer, and as a capital base they can borrow against. A single individual may hold dozens of policies because each one serves a different entity, partner, or purpose, not because they need that much personal protection.

Why does Paul Atkins own 54 life insurance policies?

Paul Atkins, the SEC chairman, disclosed 54 policies (9 whole life, 45 universal life, 0 term) in his 2025 ethics filing, with an estimated $30 to $70 million of death benefit. The most likely explanation is a mix of estate planning, trusts, and business uses across his many entities and partnerships, not a single policy on his own life. The death benefit is roughly 10% of his reported net worth.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Do your heirs lose the cash value when you die?

Your heirs receive the death benefit, not the death benefit plus a separate cash value, because cash value and death benefit are one asset, not two. In a properly designed policy with a growing death benefit, the death benefit increases by more than the cash value over time, so heirs receive more than the cash value would have been on its own.

What is the difference between whole life and universal life insurance?

Whole life has fixed premiums and guaranteed cash value growth plus non-guaranteed dividends, which suits a capital base you borrow against. Universal life offers flexible premiums and is often used to hold a large death benefit efficiently for estate planning. The wealthy frequently use universal life when the goal is maximum death benefit rather than early cash value.

Is life insurance a good investment?

Life insurance is not an investment, it is a strategy and a capital tool. Comparing its internal return to the stock market is the wrong frame. The value comes from tax-advantaged growth, the ability to borrow against the policy while it keeps compounding, and an income-tax-free death benefit, used with discipline.

Are life insurance death benefits tax-free?

Life insurance death benefits are generally received income-tax-free by the beneficiary under IRC Section 101. They can still be included in the taxable estate unless the policy is owned by an irrevocable life insurance trust. Cash value grows tax-deferred, and policy loans are not treated as taxable income while the policy stays in force.

Do you borrow against cash value or against the death benefit?

Technically you borrow against the death benefit, with the policy as collateral, and the cash value sets the ceiling on how much you can access. That collateral is why policy loans carry favorable rates and no fixed repayment schedule. An outstanding loan reduces the death benefit dollar for dollar until it is repaid.

Why do wealthy people use universal life for estate planning?

Universal life can hold a large death benefit at a lower internal cost than whole life when early cash value is not the goal, which fits estate and legacy planning. Held inside a trust, the death benefit can pass to heirs or charitable causes efficiently and provide liquidity to cover estate taxes without forcing the sale of other assets.

How much life insurance should a high-net-worth person own?

There is no fixed percentage. Paul Atkins' disclosed death benefit is roughly 10% of his net worth, and researchers quoted in the coverage suggested he may even be underinsured for his estate and business needs. The right amount depends on estate tax exposure, business obligations, and legacy goals, not a rule of thumb.

Should I buy whole life or IUL at age 69?

Neither is automatically right. At older ages the cost of insurance inside whole life is high, so when the goal is death benefit, an indexed universal life or a single-premium design can sometimes fit better. The answer depends on your goal, your health, and the carrier, so the numbers should be run and stress-tested before deciding.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 101 (Cornell Law), the income-tax exclusion for life insurance death benefits.

- IRC Section 7702 (Cornell Law), the tax treatment of life insurance cash value and loans.

- U.S. Securities and Exchange Commission, leadership and the ethics disclosure process.

- LIMRA, life insurance industry ownership and product data.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Co-hosts The And Asset Show and walks through the full Paul Atkins disclosure on screen, breaking down the whole life and universal life split and the death benefit versus cash value question.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a policy fits your plan, book a discovery call. We will tell you if it does not.

1. "What Is Infinite Banking?" (Pillar / Blog 1) → wire from the framework section (H2 04) anchor "The And Asset."

2. "How to Structure an And Asset Policy" (Blog 8) → wire from the step-by-step section (H2 05, PUA / base split).

3. "Infinite Banking Pros and Cons" (Blog 10) → wire from the where-people-go-wrong section (H2 09).

4. Pillar (Blog 1) must appear on every blog, included above.