.png)

A "Super Roth" is a nickname for using an overfunded whole life insurance policy as tax-exempt retirement cash flow. Unlike a Roth IRA, it carries no income limit and no annual contribution cap, plus a death benefit. The cash flow comes from policy loans, which are not reportable as taxable income.

Most high earners run out of tax-advantaged room long before they run out of income. The 401(k) is maxed, the backdoor Roth is a few thousand dollars, the HSA is full, and the rest piles into a taxable brokerage account that gets taxed every year on the way up and again on the way out. The question that follows is not how to earn a higher return. It is how to keep more of what you already earn when you finally spend it.

The retirement that fails quietly is the one where every dollar of income triggers a chain of taxes the plan never modeled. Federal tax, state tax, a possible local tax, tax on Social Security, a Medicare premium surcharge, and the advisor's fee. Spend from a traditional account and you are paid last in that line. The "Super Roth" framing is a response to that problem, and it is one of the most oversold ideas in personal finance.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the tax-exempt income strategy is real when it is built correctly. It is also misunderstood, dressed up as "tax-free" when it is not, and pitched to people it does not fit. This guide covers what the strategy actually is, how the tax-exempt cash flow works mechanically, the math that decides whether borrowing makes sense, and the two structural risks nobody markets. We will also tell you who should walk away.

The frame comes from a conversation between BetterWealth founder Caleb Guilliams and Tom Love, a five-decade insurance veteran who built a training group, the Breakaway League, around exactly this distribution strategy. We have tightened his on-camera shorthand into precise language, because a YouTube conversation tolerates loose phrasing and a financial publication does not.

- A "Super Roth" uses overfunded whole life for tax-exempt cash flow, with no income limit and no annual contribution cap.

- The income is tax-exempt, not tax-free: it is a policy loan, not reportable income, as long as the policy stays in force.

- Policy loans are non-recourse: no credit check, no income verification, no fixed repayment schedule, and the cash value keeps compounding.

- The And Asset rule still governs: only borrow when the deployed return beats the carrier's loan cost.

- Two structural risks: you may not qualify on health, and the tax code can change, though it has changed rarely and grandfathers existing policies.

- This strategy uses mutual whole life, not indexed universal life, because ongoing internal costs can erode an IUL later in life.

Tom Love spent 29 years figuring out the one distinction at the center of this strategy. In the full conversation, he walks through the language he uses with clients and the audit story that makes the tax mechanics concrete:

01 / The problemWhat this strategy actually solves

The strategy solves a spending problem, not an accumulation problem. Most people with money have done a competent job building accounts. What they have not solved is how to pull income out efficiently once the saving is done. A million dollars in a traditional IRA is not a million dollars to you. It is a balance you share with a future tax bill you cannot yet size.

Tom Love put a number on the inefficiency. To spend the same after-tax amount that a well-built tax-exempt structure delivers, he argues a retiree relying on a taxable brokerage account would have to earn an outsized return every year for life. The figure is directional, not a guarantee, and it depends on your bracket and state. The underlying point holds: taxes on distributions are a drag that compounds against you precisely when you can least afford it.

There is a second cost most plans ignore. Money locked in a retirement account to fund a distribution cannot also be used as opportunity capital. If you have a million dollars generating $40,000 of income, you cannot pull from that million to seize a deal without unwinding the engine that produces the income.

"The city and state you live in and where your money is parked can have more impact on your retirement than your rate of return.", Tom Love

02 / The frameworkWhat is a "Super Roth," and how does The And Asset fit?

A "Super Roth" is a marketing nickname for using a properly structured, overfunded whole life policy as a source of tax-exempt cash flow. The comparison to a Roth is useful because both can deliver income that does not show up as taxable. The comparison breaks down where it matters most: a Roth caps your contributions and phases out as your income rises, while a permanent life policy does neither.

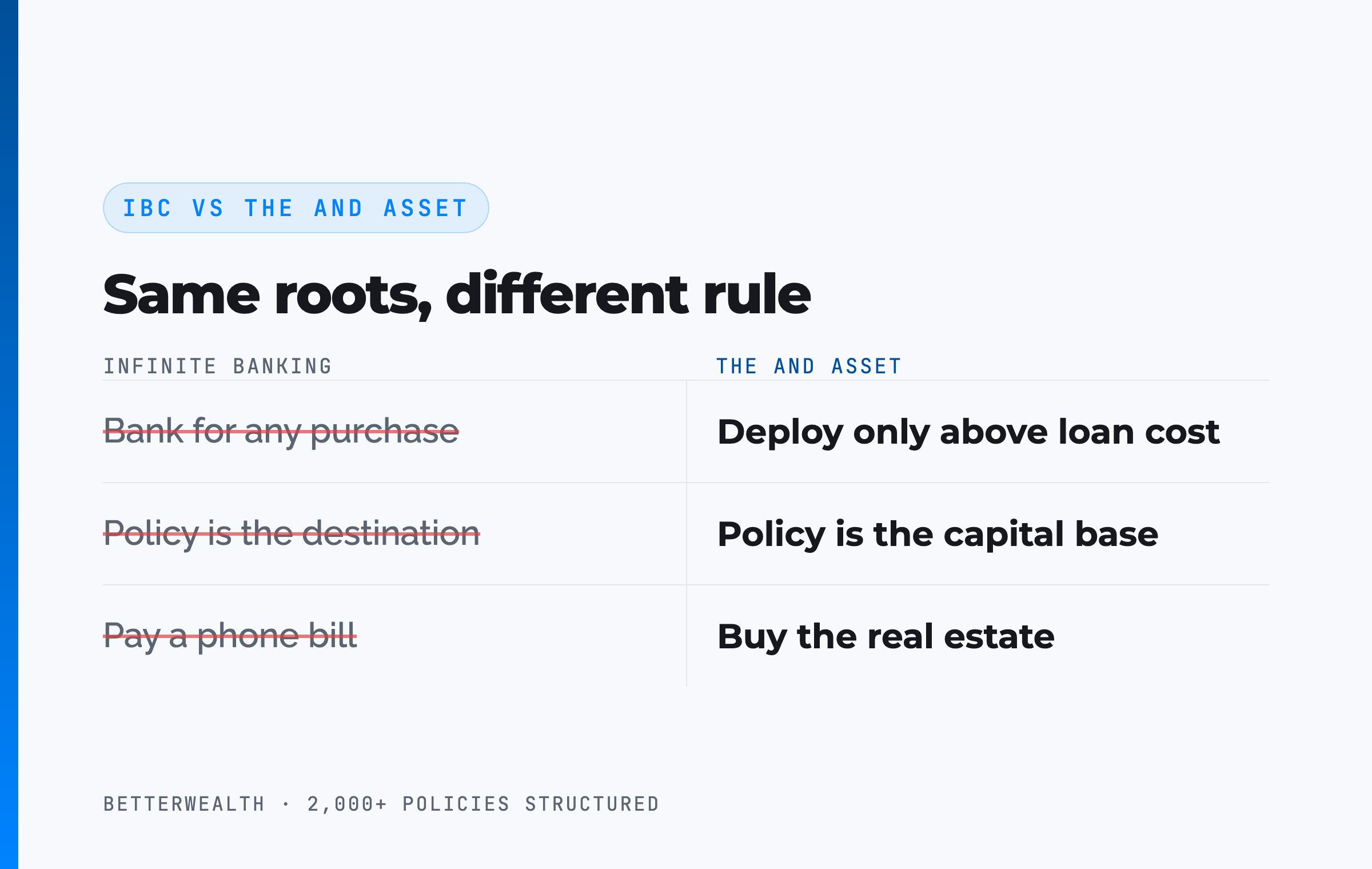

This is where we draw a line that the video did not. Caleb Guilliams, who wrote The And Asset, calls the approach "infinite banking on steroids" on camera. On the page, we are precise about it. The And Asset is BetterWealth's framework, built on Nelson Nash's foundation, and it operates on a different principle than most infinite banking teaching.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Tom Love draws the same line himself: he will never use a policy to pay a phone bill, but he will use the cash value as collateral to buy real estate. That is the discipline. The policy is the capital base. The value is created in what you deploy it into.

Nelson Nash pioneered using whole life as a personal banking system in Becoming Your Own Banker. We credit that foundation. The And Asset adds the one rule that turns a clever tax structure into a life insurance strategy: the math has to clear the loan rate.

The policy is the base. The deployment is the point.

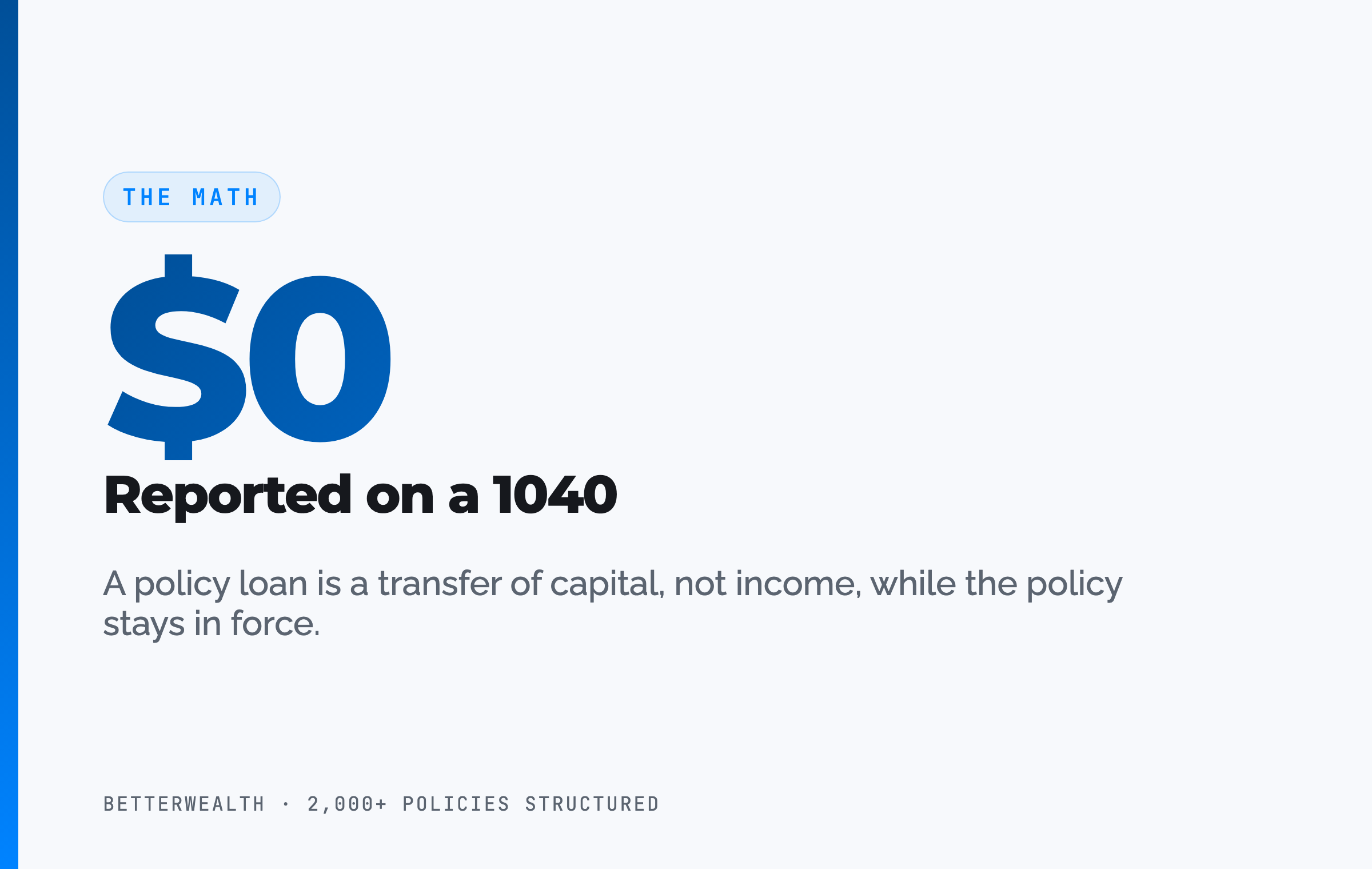

It is not tax-free. It is tax-exempt. A policy loan is a loan, not income, so it never lands on a 1040. The constraint is that you have to keep the policy in force.

03 / How it worksHow does tax-exempt cash flow actually work?

Tax-exempt cash flow works because you borrow against your cash value rather than withdraw it, and a loan is not income. The whole strategy turns on a single distinction Tom Love says took him 29 years to internalize: when you borrow from an insurance company, you are not borrowing your money, you are borrowing the carrier's money against your cash value as collateral. Your cash value never leaves the policy. It keeps compounding net of mortality and expense charges the entire time the loan is outstanding.

Here is the sequence we use when we structure a policy for this purpose.

- Structure an overfunded policy. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows, pushing cash value toward the limit without creating a Modified Endowment Contract. The base/PUA split is the design decision that drives early cash value. Designs range widely, from a high-PUA build to a base-heavy 10/90 or a more conservative 25/75, and the right ratio depends on how much guaranteed growth you want on each dollar.

- Fund and let it capitalize. Fund consistently, whether on a level schedule or a limited-pay design like a 10-pay. Cash value trails cumulative contributions in the early years. Break-even, where total cash value catches total contributions, arrives at year 5 or later for a healthy individual. Any illustration showing day-one break-even is fiction.

- Borrow against the policy. Request a policy loan collateralized by your cash value. There is no credit bureau pull, no tax return, and no fixed payment schedule. The carrier already holds the collateral, so there is no underwriting on the loan itself.

- Deploy or distribute. Put the borrowed capital into an activity that beats the loan cost, or take it as retirement cash flow. Because the loan is a transfer of capital and not a realization of income, it is not reportable as taxable income under current tax treatment. This mirrors how a mortgage check to a seller is not taxed to you.

- Repay and keep it in force. Repay from the cash flow the activity generates, or let the death benefit settle the loan balance at death. Keep the policy in force. A policy that lapses with a gain still owed becomes a taxable event, which is the failure mode to avoid.

The carrier sends an annual interest bill. You can pay it, or it can be added to the loan balance. That flexibility is the feature and the trap. Unmanaged, a growing loan can erode a poorly built policy. Built correctly with a mutual carrier, the guaranteed cash value and the dividend keep the contract healthy.

You borrow against it, not from it.

The audit that makes it concrete

Tom Love tells a story about a client audited by the IRS. The auditor asked where a large deposit in his checking account came from. The answer was a loan against a cash value life insurance policy under Section 7702 of the tax code. The auditor had to call a supervisor to confirm there was no income tax due on it. The lesson is not that you outsmart the IRS. The lesson is that this treatment is long-standing and written into the code, and most people, including some tax professionals, have simply never read it.

The Super Roth fits a specific person, not everyone.

It fits you if

- You have maxed your tax-advantaged accounts and want more tax-exempt room

- You have a long horizon and stable cash flow to fund it

- You can name a use for capital that beats the loan cost

- You are insurable on health

It does not fit you if

- You are early in building wealth or carrying high-interest debt

- You want a savings account, not a life insurance strategy

- You need the highest possible return, not tax efficiency

- You cannot fund it consistently for years

If you are in the first column, a 30-minute conversation will tell you whether this structure earns a place in your plan. If you are in the second, we will tell you that too.

Book a Discovery Call04 / The mathDoes the spendable cash flow beat the alternative?

The strategy wins on spendable, tax-exempt cash flow, not on raw rate of return, and that is the math people get backward. A whole life policy will not out-return the stock market. Tom Love concedes the rate of return is lower and does not argue the point. What he argues is the capital equivalent value: because the distributions are not taxed and the policy keeps compounding while borrowed against, a smaller tax-exempt base can fund more after-tax spending than a larger taxable account.

For the deployment side, the test is sharper and it is the heart of The And Asset. You borrow at the carrier's loan rate. Your cash value keeps compounding. Your deployed capital earns its own return. If that return is higher than the loan cost, the same dollar has done two jobs and you are ahead on the spread. If it is lower, you have borrowed money to lose money slowly. Loan rates vary by carrier and rate environment. At the time of writing many fall in the 5 to 6% range, but treat any specific number as a variable to verify, not a constant.

If the deal does not clear the loan rate, do not borrow.

05 / Why entrepreneurs use itWhy do high earners use this approach?

High earners use this approach for control and collateral capacity, not just the tax treatment. Tom Love asks prospects a single question that exposes the gap: how much capital can you put your hands on in 48 hours without selling something or being declined? One investor with 30 rental properties and a strong net worth answered $27,000. That is not capital efficiency. That is exposure.

Cash value in a whole life policy is collateral the carrier already holds, so a policy loan is never subject to credit approval or market timing. During the 2008 credit freeze, borrowers with 850 credit scores were turned down by banks, and landlords who had never missed a payment watched lenders call their loans. A policy loan does not behave that way. This is the structural difference between a recourse loan, which a bank can revoke, and a non-recourse policy loan, which it cannot.

The same features power the "buy, borrow, die" pattern that gets attached to names like Bezos and Musk. You hold an appreciating asset, you borrow against it for liquidity rather than selling and triggering tax, and at death the structure settles. A whole life policy completes that loop cleanly, because the death benefit pays off any outstanding loan and the remainder passes to your family income-tax-free.

06 / Where people get this wrongWhere does the Super Roth pitch go wrong?

The pitch goes wrong when "tax-free" replaces "tax-exempt" and when the product gets oversold to people it does not fit. The marketing version promises tax-free income and skips the constraint that the policy must stay in force. Income is always taxable. What is not taxable is a loan. Blur that line and you set a client up for a surprise the day a policy lapses with a gain still owed.

It also goes wrong at the carrier and product level. Tom Love describes policies where the issuing company effectively exited the whole life business and let dividends collapse. In one, a $2 million cash value paid a dividend of $163 in a year it was illustrated to pay tens of thousands. The base policy survived on its guarantee, but the engine that made it useful for distribution was gone. This is why we use mutual carriers with long, unbroken dividend histories, and why guarantees matter more than a headline dividend rate.

The third error is treating the policy as a checking account. Borrowing against it to pay a phone bill is not strategy, it is an expensive way to spend money. The discipline is the strategy.

If you got a standard insurance license-holder selling whatever pays, you would be closer to the Dave Ramsey camp. Bad actors are real. That does not make the structure wrong, it makes the practitioner matter.

One more correction worth making, because it shows up in nearly every version of this pitch. You will hear that these tax codes have existed for "113 years" or that "Senator Roth copied the life insurance code." The defensible facts are narrower and stronger. Section 7702 was added in 1984. The Roth IRA arrived in 1997. Permanent life insurance's favorable treatment predates the Roth. We do not need a manufactured origin story when the real one already makes the case.

07 / The tradeoffsThe benefits and the two honest risks

The benefits come with two structural risks, and pretending otherwise is how the industry loses trust. Tom Love names them directly when asked for the cons.

First, you may not qualify. The policy depends on your health and insurability. Not everyone can get one, and a substandard health rating changes the math. Second, the tax code could change. A life insurance policy is a legal contract, not a unilateral government program like a 401(k), so the rules governing existing contracts are harder to alter. Historically, when life insurance tax treatment has changed, lawmakers have grandfathered policies already in force and applied new rules going forward. That history is reassuring, not a guarantee. The honest framing is that the older your policy, the more insulated it tends to be.

A third risk is operational rather than structural: a loan left to grow unmanaged until the policy lapses creates a taxable event. The fix is design and discipline, including carriers with strong guarantees and, in some plans, a small allocation to a deferred annuity as a backstop against outliving the cash value.

Two real risks. Name them first.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to pressure-test a tax-exempt income plan before anyone funds a policy. Free, email-gated, no spam.

Open the Vault08 / The fitHow this fits into a broader life insurance strategy

This belongs as the tax-exempt and capital-base layer of a plan, not as the whole plan. Tom Love is candid that you cannot move everything into life insurance. You still need a house, furnishings, and a car. The assets that belong in the strategy are the investable ones that would otherwise generate taxable income and trigger the chain of downstream costs.

A common structure pairs the policy with a deferred annuity. If a dollar of investable capital goes toward the strategy, the bulk funds the policy and a smaller slice funds a deferred annuity that can be triggered later, if the policy's cash value is ever drawn down in advanced age. The two work together: the policy delivers tax-exempt cash flow for decades, and the annuity backstops longevity.

The carrier choice is deliberate. The strategy uses mutual whole life, where you participate in the company's profits through dividends, rather than indexed universal life. An IUL keeps charging mortality and expense costs for life, so a stretch of poor market years can let the costs eat the account. For a structure whose entire job is reliable tax-exempt income in retirement, that lapse risk is the wrong risk to carry.

09 / Head to headSuper Roth life insurance vs the alternatives

Against the accounts high earners actually use, an overfunded whole life policy trades raw return for tax treatment, access, and control. The table sets it against a Roth IRA, a traditional 401(k), and a taxable brokerage account on the dimensions that decide a distribution plan.

| Dimension | Super Roth (Whole Life) | Roth IRA | Traditional 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Contribution limits | No fixed annual cap; bounded only by the MEC limit relative to death benefit | Low annual cap; phases out at higher incomes | Annual cap set by the IRS | Unlimited |

| Access to capital | Policy loans anytime, no credit check, no age gate | Contributions accessible; earnings restricted before 59½ | Restricted before 59½ (penalty plus tax) | Fully liquid |

| Tax on distributions | Policy loans are not reportable income while the policy stays in force | Qualified withdrawals tax-free federally | Taxed as ordinary income | Capital gains and dividends taxed yearly |

| Use as collateral | Built-in; cash value is non-recourse collateral the carrier holds | Cannot be pledged without triggering a distribution | Cannot be pledged without triggering a distribution | Margin available, but subject to calls |

| Death benefit | Income-tax-free death benefit, reduced by any loan | Account balance passes to heirs | Taxable to heirs as ordinary income | Steps up in basis at death |

Limits. The Roth's strength, tax-free growth, comes wrapped in two ceilings: a small annual contribution and an income phase-out that shuts high earners out entirely. The whole life structure has neither, though the Modified Endowment Contract rules cap how fast you can fund it relative to the death benefit.

Access and collateral. A retirement account cannot be pledged as collateral without becoming a taxable distribution. It is the one asset in the tax code that cannot be collateralized. Cash value is the opposite: it is collateral by design, which is what makes the non-recourse policy loan possible.

Tax and legacy. Policy loans are not reportable income while the policy is in force, and the death benefit passes income-tax-free. A traditional 401(k) defers tax now and hands heirs a taxable balance later. The Super Roth structure trades the highest possible return for tax treatment you keep on both ends.

A composite: the physician who built a tax-exempt base

Consider a 48-year-old physician, preferred non-tobacco, funding an overfunded whole life policy with a mutual carrier at $75,000 per year on a high-PUA design. This is a representative composite, not a single named client.

Through the early years, cash value trails cumulative contributions, exactly as a real policy should. By year six, total cash value crosses total contributions. No earlier. Any illustration promising year-two break-even is marketing fiction.

In year eight, with roughly $548,000 of accessible cash value, the physician borrows $182,000 against the policy to fund the down payment on a rental property. The property returns an estimated 11.8% IRR, while the illustrative loan cost runs around 6%, so the spread works in the owner's favor by nearly six points. The cash value keeps compounding net of mortality and expense charges the entire time. Repayment runs on a 44-month schedule funded by the property's own cash flow.

In retirement, the same policy becomes the tax-exempt income layer. Annual policy loans deliver spendable cash flow that does not appear on a 1040, with a small deferred annuity held alongside as a longevity backstop. The dollar that bought the rental and the dollar that funds retirement income are the same dollar, working twice.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and we have watched this strategy work as designed and watched it fail. On a discovery call, a practitioner looks at your tax picture and time horizon and tells you whether a tax-exempt income structure belongs in your plan, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQSuper Roth life insurance questions

What is a Super Roth life insurance strategy?

A Super Roth is a nickname for using a properly structured, overfunded whole life insurance policy as a source of tax-exempt cash flow in retirement. Unlike a Roth IRA, it has no income limits and no annual contribution cap, and it carries a death benefit. The cash flow comes from policy loans, which are not reportable as taxable income under current tax treatment.

Is life insurance income really tax-free?

It is tax-exempt cash flow, not tax-free income, and the distinction matters. Money taken from the policy is a loan against your cash value, not income, so it does not appear on a Form 1040. The constraint is that you must keep the policy in force. A policy that lapses with an outstanding gain triggers a taxable event.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. You would use the policy as collateral to buy real estate, not to pay a phone bill. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

How does a policy loan avoid income tax?

A policy loan is treated as a transfer of capital, not a realization of income, the same way a mortgage or auto loan is not taxable when you receive it. Because it is debt against your own cash value, it is not reportable as taxable income. If you die with a loan outstanding, the death benefit is simply reduced by the loan balance.

Does the Super Roth have income or contribution limits like a Roth IRA?

No. A Roth IRA caps annual contributions and phases out entirely at higher incomes, which is why high earners often use a backdoor Roth. A permanent life insurance policy has no income ceiling and no fixed annual contribution limit, though the IRS Modified Endowment Contract rules cap how fast you can fund it relative to the death benefit.

What are the real downsides of this strategy?

There are two structural risks. First, you may not qualify, because the policy depends on your health and insurability. Second, the tax code could change, although life insurance tax treatment has been changed rarely and historically grandfathers existing policies. A third practical risk is letting a loan grow unmanaged until the policy lapses, which creates a taxable event.

Should I move Roth IRA money into life insurance?

That is a decision for you and a qualified advisor, not a blanket recommendation. Roth funds are already tax-advantaged, so repositioning them is rarely the first move and is not right for everyone. It can make sense in specific situations, but only after weighing your tax picture, time horizon, and what you give up. This is education, not personalized advice.

Why does the strategy require a mutual whole life policy instead of indexed universal life?

A mutual whole life policy has guaranteed cash value and level internal costs that end when the policy is paid up, which protects the distribution phase. Indexed universal life carries ongoing mortality and expense charges that can erode cash value in poor market years, raising the risk that the policy lapses later in life. For a tax-exempt income strategy, that lapse risk is the concern.

What is collateral capacity and why does it matter?

Collateral capacity is how much capital you can access in 48 hours without selling an asset or being declined. Cash value in a whole life policy is collateral the carrier already holds, so a policy loan is not subject to credit approval or market conditions. During the 2008 credit freeze, borrowers with high credit scores were still turned down by banks, while policy loans kept functioning.

How is the rate-of-return math different from chasing investment returns?

The strategy reframes the question from rate of return to spendable, tax-exempt cash flow. Because distributions are not taxed and the policy keeps compounding while borrowed against, a smaller tax-exempt base can fund more spending than a larger taxable account. The And Asset rule still applies: only borrow when the deployed return clears the carrier's loan cost.

Did Senator Roth copy the life insurance tax code?

There is no need to claim that, and we do not. The verifiable facts are that IRC Section 7702, which defines life insurance for tax purposes, was added to the code in 1984, and the Roth IRA was created in 1997. Permanent life insurance's tax treatment predates the Roth. The point is that life insurance's favorable treatment is long-standing, not newly invented.

- IRC Section 7702 (Cornell Law), the tax code provision defining life insurance and the tax treatment of cash value and loans.

- IRS: Roth IRAs, contribution limits and income phase-outs for comparison.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- U.S. Government Accountability Office, the agency behind the 1990 report on single-premium life insurance tax treatment referenced in the video.

- LIMRA, life insurance industry data, including persistency and product benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

A five-decade veteran of the insurance and financial advisory business who trains advisors on tax-exempt distribution strategy using permanent life insurance. He appears as the guest in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a tax-exempt income structure fits your plan, book a discovery call. We will tell you if it does not.