.png)

Premium financing life insurance is borrowing from a bank to pay the premiums on a large policy instead of paying out of pocket. Wealthy families use it so their own capital stays deployed in higher-returning assets while the death benefit covers a future estate-tax bill.

The objection sounds reasonable: if you are wealthy enough, you do not need life insurance at all. The people who say it are almost never the ones who have actually faced a multi-million-dollar estate-tax bill. Once a family crosses into real wealth, the question stops being whether they can afford a premium and becomes a question of opportunity cost. Every dollar pulled out of a business or a real estate portfolio to pay a premium is a dollar that stops earning its real return.

For the ultra-wealthy, paying cash for a large policy is frequently the most expensive way to fund it, because the capital they would spend is already working harder than the bank's loan costs. That single insight is why premium financing exists. It lets a family borrow the premium, leave their capital deployed, and use the policy to solve a liquidity problem that would otherwise force a fire sale.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we sit at the intersection of two strategies that get confused constantly. One is premium financing, which uses a bank's money. The other is The And Asset, which uses your own policy's cash value. This guide covers how premium financing actually works for high-net-worth families, the estate-tax problem it solves, why whole life beats indexed universal life for financing, the four conditions that decide whether it succeeds, and where it sits beside The And Asset. We will also tell you, plainly, who should never use it.

- Premium financing borrows a bank's money to pay policy premiums, so your own capital stays deployed at a higher return.

- The real problem it solves is future liquidity: a death benefit pays the estate tax instead of forcing a fire sale.

- It works only for someone who could write the check anyway, understands the structure, and uses the right product.

- Whole life beats IUL for financing because its guaranteed component does not blow up in a weak year.

- The failure point is always the loan: you still have to pay the bank back, and rising rates can force collateral.

- Premium financing is external leverage; The And Asset is internal leverage. Both rest on the same spread logic.

In the full interview, Kuldeep Madan walks through the exact client conversations behind these cases, including the IUL versus whole life debate that the blog can only summarize:

01 / The problemWhat problem does premium-financed life insurance actually solve?

It solves a future liquidity problem, not a present income problem. When a large estate owes federal estate tax above the exemption, the heirs often have to come up with cash quickly, and the assets are not cash. They are a business, a building, a portfolio of real estate. Paying the tax can mean selling one of those assets, sometimes in a year when the market is not in their favor.

A death benefit is the cleanest source of that cash. It arrives at the moment the tax is due, in the right amount, without a forced sale. The wrinkle is the premium. A family worth $74 million may have the money to pay a large premium and still not want to, because that money is currently growing inside their business or real estate at a rate the bank cannot match. Financing the premium keeps the capital deployed and still buys the liquidity.

Kuldeep Madan, on the people who claim the wealthy do not need insurance: "Just think about who it is that would say something like that. It is people who are not ultra-wealthy."

02 / The frameworkHow premium financing relates to The And Asset

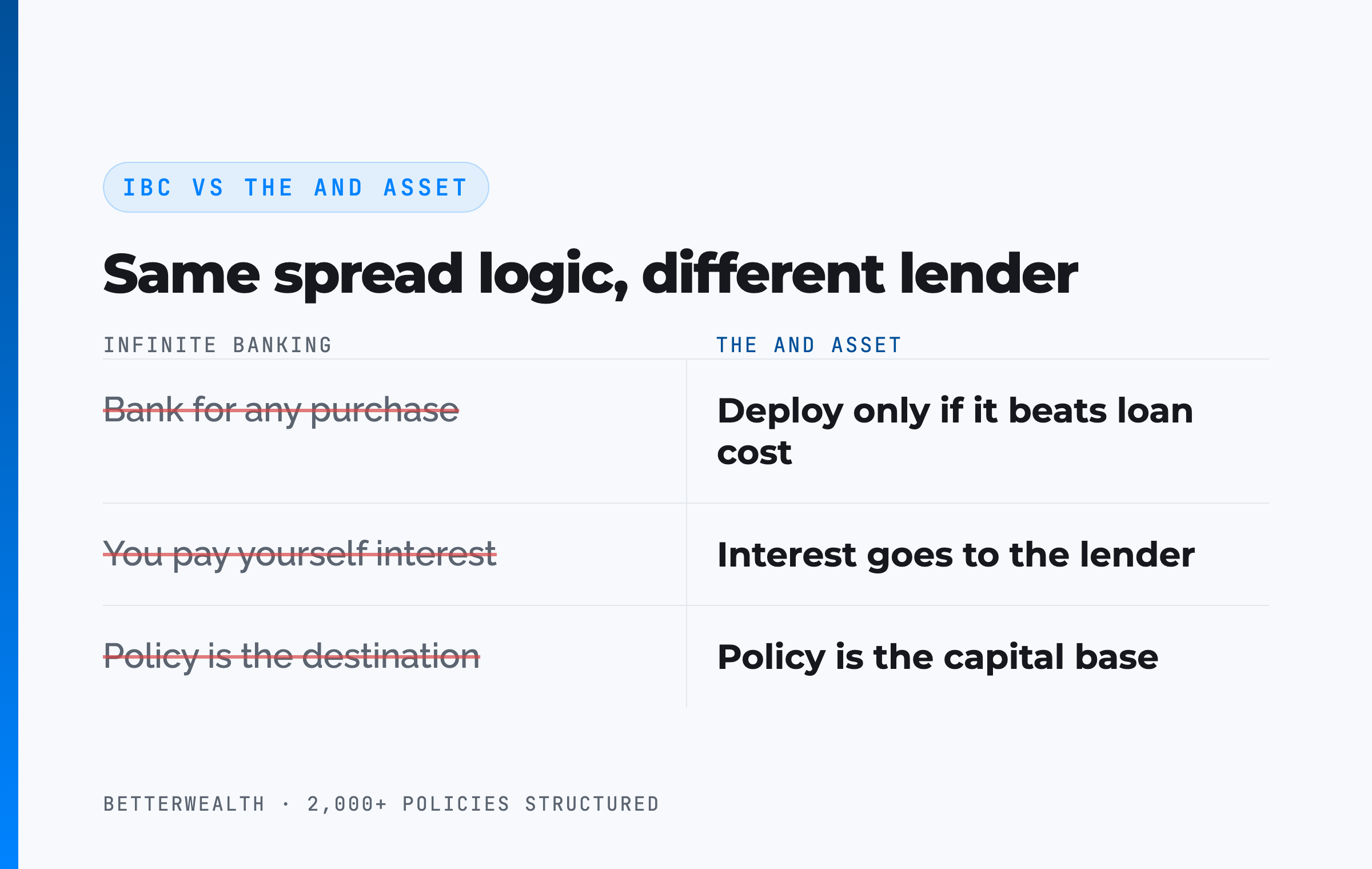

Premium financing and The And Asset are cousins, not twins, and the difference is the source of the leverage. Premium financing uses a bank's capital to pay your premiums. The And Asset uses your own policy's cash value as the capital base you borrow against. The guest in the interview called premium financing "infinite banking squared," and the instinct behind that phrase is right even though the labels need cleaning up.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with a rule that the broader infinite banking teaching does not enforce.

Where infinite banking ends and The And Asset begins

Infinite banking says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital when the borrowed dollars produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Premium financing applies the same test to a different lender. You borrow from a bank, you keep your capital deployed at a higher return, and the spread is the entire point.

So the two strategies share one logic. Keep your highest-returning capital where it is. Borrow only when the spread works. The And Asset borrows internally against the policy. Premium financing borrows externally from a bank. There are times a bank does this better than you can, and there are times you do not want to be your own bank. This is one of them.

The spread has to work. Every time.

Many marketers say you are paying yourself interest. You are not. The interest goes to the lender. Your return is what your capital earns while it stays deployed.

03 / Opportunity costWhy do the ultra-rich borrow instead of paying cash?

The ultra-rich borrow because their capital is already earning more than the loan costs. A wealthy owner whose business compounds at 12 to 18% does not want to strip seven figures out of it to hand an insurer a premium. The mortgage analogy is exact. Carrying a 30-year loan on a $10 million home does not mean you are broke. It means you chose to keep your liquidity and options instead of locking your cash into the walls.

Premium financing applies the same choice to insurance. The family could write the check. They decide their opportunity cost is higher than the bank's loan cost, so they take the loan, leave their capital working, and let the policy do its job. The estate tax is paid with the insurer's money, and the premium for that insurance is paid with the bank's money. It is deliberately cyclical, and it holds together as long as the exit is real.

04 / How it worksHow whole life premium financing works, step by step

Whole life premium financing works through five steps, and the order is not optional. Skipping the first two is how cases end up in court. Here is the sequence a disciplined practitioner follows.

- Qualify the client profile. Confirm the client could pay the premium outright, with or without a bank. This is the gate. If you cannot write the check, you do not finance the policy. The bank is a convenience, not a crutch.

- Design the whole life policy. Structure a participating whole life contract with a guaranteed component and a death benefit sized to the projected estate-tax liability. The guarantee is what makes the policy behave predictably for the lender and for you.

- Arrange the bank loan. A lender finances the annual premium. In the early years the policy's cash value is lower than the loan balance, so the client posts outside collateral to cover the gap. That collateral requirement shrinks as cash value builds.

- Keep your own capital deployed. Leave your capital in the business, real estate, or fund where it earns more than the loan costs. This is the whole reason to finance rather than pay cash. The deployed return has to clear the loan rate.

- Plan the exit. Decide in advance how the bank gets repaid: from accumulated cash value, a future liquidity event, or the death benefit through a properly designed trust. Bring in estate attorneys early. The exit is the strategy.

On a well-designed whole life policy, cash value trails cumulative premiums in the early years, which is exactly why outside collateral is required at the start. Cash value catches up to and then passes cumulative premiums later, typically several years in, and a financed policy reaches that point even later than a policy paid in cash. Any illustration that shows a financed policy breaking even in year one or two is fiction.

Why product choice decides the outcome

The product you finance matters more than almost any other variable. Whole life is built on a guaranteed floor that does not vanish in a weak year, so the contract keeps working even when a dividend comes in lower than projected. A lower dividend slows the policy. It does not detonate it. That predictability is what a lender and a 30-year plan both need.

Complex products behave differently under financing, and the failures cluster there. When a product depends on crediting assumptions that can swing, layering a bank loan on top multiplies the risk. The strategy is only as stable as the contract underneath it.

Finance the predictable thing.

For the deeper mechanics of how a whole life policy is structured for cash value, see How to Structure an And Asset Policy, which covers the design decisions that make a financed policy behave predictably.

Premium financing fits a narrow profile, on purpose.

It fits you if

- You could pay the premium without the bank

- Your capital is earning more than the loan costs

- You face a real future estate-tax liability

- You understand the structure well enough to explain it back

It does not fit you if

- You need the bank to afford the premium at all

- Your only repayment plan is the death benefit

- You want a hands-off product you never manage

- You cannot name a return that beats the loan cost

If you are in the first column, a 30-minute conversation will tell you whether financing, a paid-up policy, or The And Asset fits your situation. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the deployed return clear the bank's loan cost?

The return on the capital you keep deployed must exceed the bank's loan cost, or financing makes no sense. This is the entire test, and it is the same test The And Asset applies internally. Loan rates vary by lender and rate environment. Treat any specific number as a variable to verify with the bank, not a constant to build a plan around.

Here is the structure of the decision. The bank lends you the premium at its loan rate. Your capital stays invested in the asset that is already compounding faster than that rate. The policy builds its guaranteed and dividend-driven value, with growth credited net of the policy's internal mortality and expense charges, not at the headline dividend rate. If your deployed capital earns more than the loan costs, you are ahead on the spread, and the same wealth has done two jobs. If it earns less, you have borrowed money to lose ground slowly.

If the return does not beat the loan, do not borrow.

06 / Whole life vs IULWhy does financed IUL go belly up more often?

Financed indexed universal life fails more often because it stacks a complex, assumption-sensitive product underneath a bank loan. IUL is not an inherently bad product. It is a complicated one, and complexity plus leverage is a fragile combination. When the crediting assumptions that hold an IUL together do not perform, the loan does not care, and the gap has to be covered by someone.

There is a quieter argument that matters even more. A perfectly executed IUL tends to land near where a whole life policy would have landed anyway. So you take on more moving parts, more management, and more downside scenarios for a result that is, at best, marginally better. Most wealthy families, once they see that trade clearly, choose the simpler contract they can actually understand.

The control argument

The end goal of estate planning is control: getting your money to the right people, on your terms, while keeping access along the way. A product you cannot follow undermines that goal. Whole life is complicated too, but it has a track record of behaving the way the contract promises. When a family has finally built a clean estate plan, they tend to want less risk layered on top, not more.

High-profile lawsuits over complex and financed policies almost always trace back to the same root. Something went wrong, it kept going wrong, and no one fixed it in time. That is a management failure on a fragile structure, not a reason to fear insurance itself. It is a reason to choose the predictable contract and to run it with discipline.

Simpler survives leverage. Complex often does not.

07 / The guaranteesWhat about guaranteed universal life for the estate-tax need?

Guaranteed universal life is the cheapest way to fund a pure death benefit, but it is the wrong tool for financing. A GUL policy, designed properly, pays a death benefit at the insured's passing, which can cover an estate-tax bill at the lowest possible premium. The catch is that it builds little or no cash value.

That missing cash value is exactly what makes GUL impractical to finance. With no asset building inside the policy, there is nothing to repay the bank from except the death benefit, which means rising outside collateral every single year and no graceful exit. GUL is also static. It does not grow with inflation or give the family room to adapt. Families who choose it for its low cost often discover, years later, that they would have valued the flexibility and access a whole life policy provides.

Do you know for certain what you will want at 70? No one does. That is the case for the contract that gives you options, not the one that locks them away.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use when we weigh paying cash against financing, and whole life against the alternatives. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsThe four conditions, and the real risks

Premium financing works when four conditions hold, and it fails when any one of them breaks. Pretending the risks do not exist is how advisors lose the trust of a family office. Here they are, plainly.

First, the client must be able to afford the premium without the bank. If the financing is the only way the policy happens, the structure is built on sand. Second, the client must understand what they are doing. The education gap in this strategy is wide, and people who do not understand the risk cannot manage it. Third, the product must be the right one, which in almost every case means whole life with its guaranteed component rather than a volatile alternative. Fourth, the exit must be planned before funding, because you still have to pay the bank back, and that repayment is where everything either holds or falls apart.

The risks live inside those conditions. Rising interest rates can raise the loan cost and trigger demands for more collateral. A policy that underperforms can widen the gap between cash value and loan balance. A vague exit plan turns a sound idea into a slow-motion problem. None of these are reasons to avoid financing. They are reasons to do it only with the right person, the right product, and the right plan.

You still have to pay the bank. That is where it fails.

This is not for everyone, and that is the point. The discipline of qualifying the client and planning the exit is the strategy, not the financing itself.

09 / The fitWho is premium financing right for, and who isn't it?

Premium financing is right for the high-net-worth entrepreneur or family with a real estate-tax liability, capital that earns more than the loan costs, and the discipline to plan the exit. It fits the value creator who would rather keep money compounding inside a business than strip it out to pay premiums, and who understands the structure well enough to explain it back. For that profile, financing can be the most efficient way to fund the liquidity their heirs will need.

It is wrong for anyone who needs the bank to afford the premium, whose only repayment plan is the death benefit, or who wants a product they never have to think about. Premium financing is an actively managed strategy on a long horizon. If you cannot name a return that beats the loan cost, no amount of structuring will make the math work, and a simpler approach will serve you better.

10 / Head to headFour ways to fund a large life insurance need

Compared to the alternatives, premium-financed whole life trades simplicity for capital efficiency and keeps your money deployed. The table sets it against paying premiums in cash, financing an IUL, and the do-nothing default of selling assets at death, on the dimensions that matter for an estate plan.

| Dimension | Financed Whole Life | Pay Premiums in Cash | Financed IUL | Sell Assets at Death |

|---|---|---|---|---|

| Capital efficiency | Keeps your capital deployed at its higher return | Diverts capital from higher-returning assets | Keeps capital deployed, but on a fragile contract | No premium cost, but assets sold at a discount |

| Predictability | Guaranteed component does not blow up in a weak year | Fully predictable, no loan involved | Sensitive to crediting assumptions; higher failure rate | Depends entirely on the market at time of death |

| Liquidity at death | Death benefit pays the tax without a forced sale | Death benefit pays the tax without a forced sale | Death benefit can pay the tax if it performs | Heirs scramble for cash, often at a bad time |

| Control and risk | Active management; you still must repay the bank | Lowest risk; highest opportunity cost | Most moving parts; most ways to go wrong | Lowest control; the market sets the terms |

Capital efficiency. Financed whole life and financed IUL both keep your capital deployed, which paying cash cannot do. The difference is the contract underneath. Financing rewards the predictable one and punishes the fragile one.

Liquidity at death. Any funded policy beats selling assets to pay the tax, because the family is not forced to liquidate a business or a building when the market may not cooperate. That forced sale is the exact outcome the strategy is built to avoid.

Control and risk. Paying cash is the simplest path and carries the least risk, at the cost of the return your capital could have earned. Financing keeps that return in play, but you take on an active obligation: the loan does not forgive itself, and the exit has to be real.

A composite: the $74M owner who would not sell the business

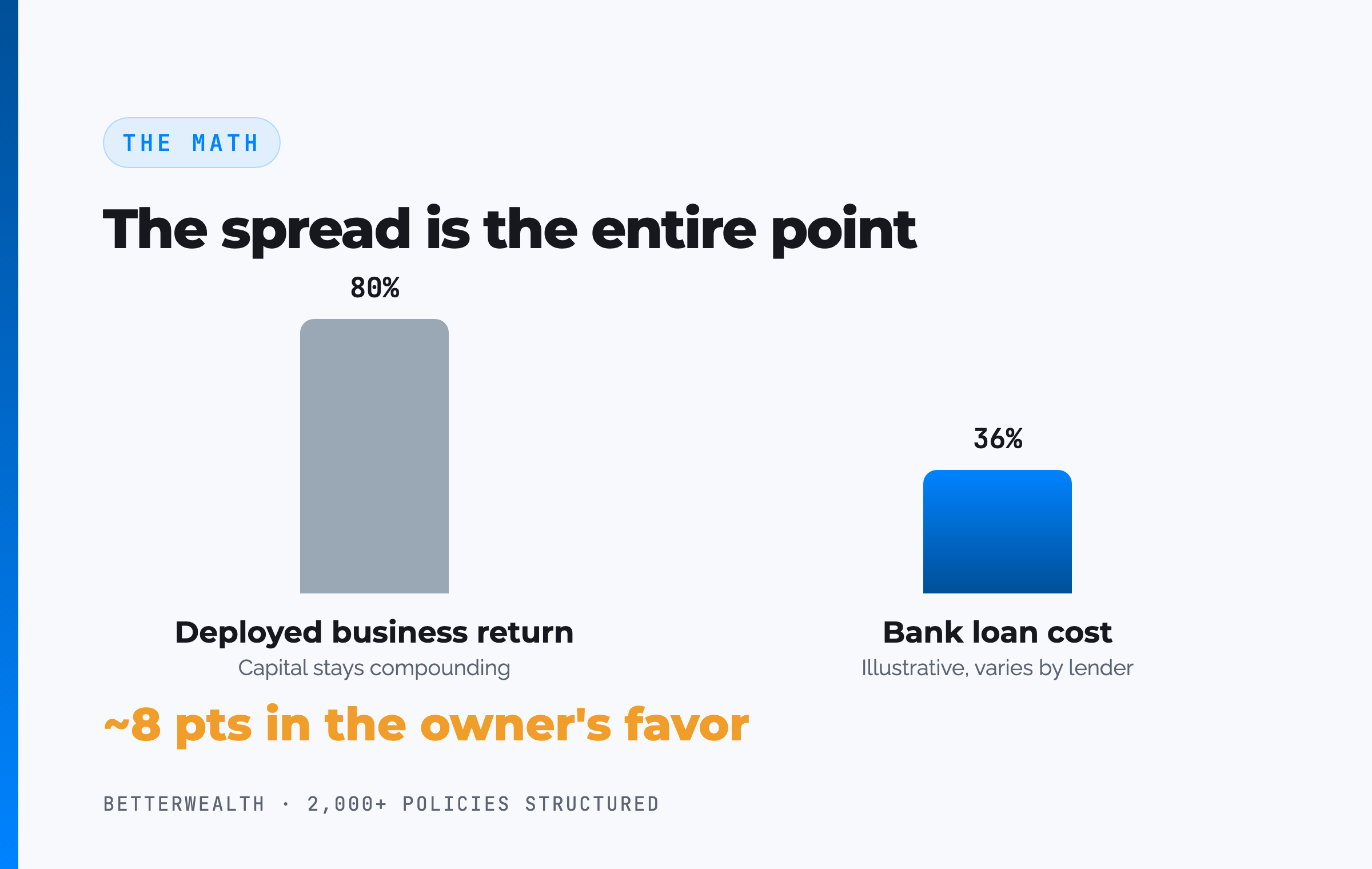

Consider a 54-year-old business owner, preferred non-tobacco, with a net worth around $74 million concentrated in an operating company that compounds near 14.6% a year. This is a representative composite, not a single named client.

Pulling $387,000 a year out of the company to pay the premium in cash would have cost the owner the company's return on that money, roughly twice the bank's loan cost. So the premium is financed. The capital stays in the business. In the early years the policy's cash value sits below the loan balance, so the owner posts outside collateral to cover the gap, exactly as a real financing case requires. By year seven, cash value catches cumulative premiums and the outside collateral is released. No earlier. Any illustration showing the financed policy even by year two is marketing fiction.

The death benefit, structured inside an irrevocable trust, is sized to the projected federal estate-tax liability so the heirs never have to sell the company to pay the tax. The spread between the 14.6% the business earns and the roughly 6.5% the loan costs works in the owner's favor by about eight points on the financed amount, while the policy compounds on its guaranteed and dividend value the entire time. The exit is defined up front: cash value and a planned liquidity event repay the bank, with the death benefit as the backstop.

The bank's money buys the time. The business keeps the return.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen financing work exactly as designed and seen it fail. On a discovery call, a practitioner looks at your specific situation and tells you whether premium financing, a paid-up policy, The And Asset, or none of them belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFor the full breakdown of how the same leverage logic works inside your own policy rather than through a bank, the The And Asset YouTube channel picks up where this leaves off.

FAQPremium financing life insurance questions

What is premium financing for life insurance?

Premium financing is borrowing from a bank to pay the premiums on a large life insurance policy instead of paying out of pocket. High-net-worth families use it so their own capital stays deployed in higher-returning assets while the policy provides liquidity to cover a future estate-tax bill.

Why do the ultra-rich use other people's money to buy life insurance?

The ultra-rich use other people's money because their capital is already working at a higher return than the bank's loan cost. Pulling millions out of a business or real estate to pay premiums would cost them more in lost return than the financing costs, so they borrow the premium and leave their capital deployed.

Does premium financing always work?

Premium financing works when it is done correctly for the right client: someone who could write the check anyway, who understands the structure, and who uses whole life rather than a more volatile product. It fails when the borrower cannot repay the bank, when rising interest rates trigger collateral calls, or when the policy itself underperforms.

Why is whole life better than IUL for premium financing?

Whole life is built on a guaranteed component that does not disappear if dividends are lower in a given year, so a financed whole life policy behaves predictably. Indexed universal life is more complex and more sensitive to crediting assumptions, which is why financed IUL cases fail more often. A perfectly run IUL ends up roughly where whole life lands anyway, with more risk along the way.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

How is premium financing different from The And Asset?

The And Asset uses internal leverage: you borrow against your own policy's cash value. Premium financing uses external leverage: a bank lends you the premium. Both rest on the same principle, which is keeping your highest-returning capital deployed and only borrowing when the spread works in your favor.

What problem does premium-financed life insurance actually solve?

It solves a future liquidity problem. When a wealthy estate owes federal estate tax above the exemption, the family often has to sell a business or real estate to pay it, sometimes at a bad time. A death benefit provides the cash to pay the tax, and financing the premium means the family does not divert capital from higher-returning investments today.

Who should not use premium financing?

Anyone who could not pay the premium without the bank should not use premium financing. It is also wrong for someone who does not understand the structure well enough to explain it back, and for anyone whose only repayment plan is the death benefit with no cash value or liquidity event behind it.

Can you finance a guaranteed universal life (GUL) policy?

Financing a guaranteed universal life policy is generally impractical because GUL builds little or no cash value, so there is no asset to repay the bank from other than the death benefit. That forces rising outside collateral every year. GUL is the cheapest way to fund a death benefit, but it is not designed for financing.

What is the biggest risk in premium financing?

The biggest risk is the loan itself, because you still have to pay the bank back. Rising interest rates can raise the loan cost and trigger demands for more collateral, and a policy that underperforms can widen the gap. Managing and mitigating these risks up front is what separates a financing case that works from one that fails.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRS, Estate Tax, the federal estate-tax rate and exemption rules behind the liquidity problem.

- IRC Section 7702 (Cornell Law), the tax-code provision governing life insurance cash value and policy loans.

- LIMRA, life insurance industry data on product performance and persistency.

- Kuldeep Madan, the premium-financing specialist featured in the source interview.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Works with family offices and ultra-high-net-worth families on whole life premium financing and estate-planning cases, and breaks down the IUL versus whole life debate in the source video. Profile →

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether premium financing or The And Asset fits your plan, book a discovery call. We will tell you if it does not.

1. "What Is Infinite Banking?" (Pillar / Blog 1) → wire from the framework section (H2 02) anchor "The And Asset."

2. "How to Structure an And Asset Policy" (Blog 8) → wire from the step-by-step structure section (H2 04, policy design step).

3. "Infinite Banking Pros and Cons" (Blog 10) → wire from the tradeoffs section (H2 08).

4. "Whole Life Insurance for Estate Planning" (Cluster bonus) → wire from the problem section (H2 01).

5. Pillar (Blog 1) must appear on every blog, included above.