Whole life insurance versus investing is the wrong comparison. The honest one is whole life integrated into your plan against the same dollars split between term insurance and a separate account. Over a 55-year horizon, the integrated path often produces a similar or larger after-tax balance plus a death benefit the other no longer has.

The most common objection to whole life insurance is that you would do better buying cheap term and investing the difference. It is a clean story and it survives because almost no one runs the full math. They compare a whole life policy in isolation to a brokerage account in isolation, ignore taxes and term premiums on the investment side, and stop counting at age 65.

The real comparison is not whole life versus an investment account. It is the same total cash flow run two ways, one with permanent insurance integrated and one with term plus a separate account, measured all the way to life expectancy. Run that way, with the same dollars and the same time horizon, the result is not what the buy-term crowd assumes.

This breakdown is built from a BetterWealth conversation with Trent Fortner, who has spent 37 years working with clients and the last several decades training advisors to read these contracts honestly. He walked through a real (anonymized) case using the LEAP planning model and a live Penn Mutual illustration, and he did something most agents avoid: he unbundled the policy to show its true cost.

At BetterWealth, we have structured more than 2,000 policies across all 50 states. We use a framework we call The And Asset, and it changes how this comparison should end. We will cover the cost of insurance line by line, the after-tax 55-year result, where whole life still loses, and the discipline that decides whether any of it is worth doing.

- Comparing a whole life policy to an investment account in isolation is the wrong frame; compare the same total cash flow run two ways.

- In the reviewed case, nearly all policy cost was absorbed in the first four years, then each premium dollar added more than a dollar of cash value.

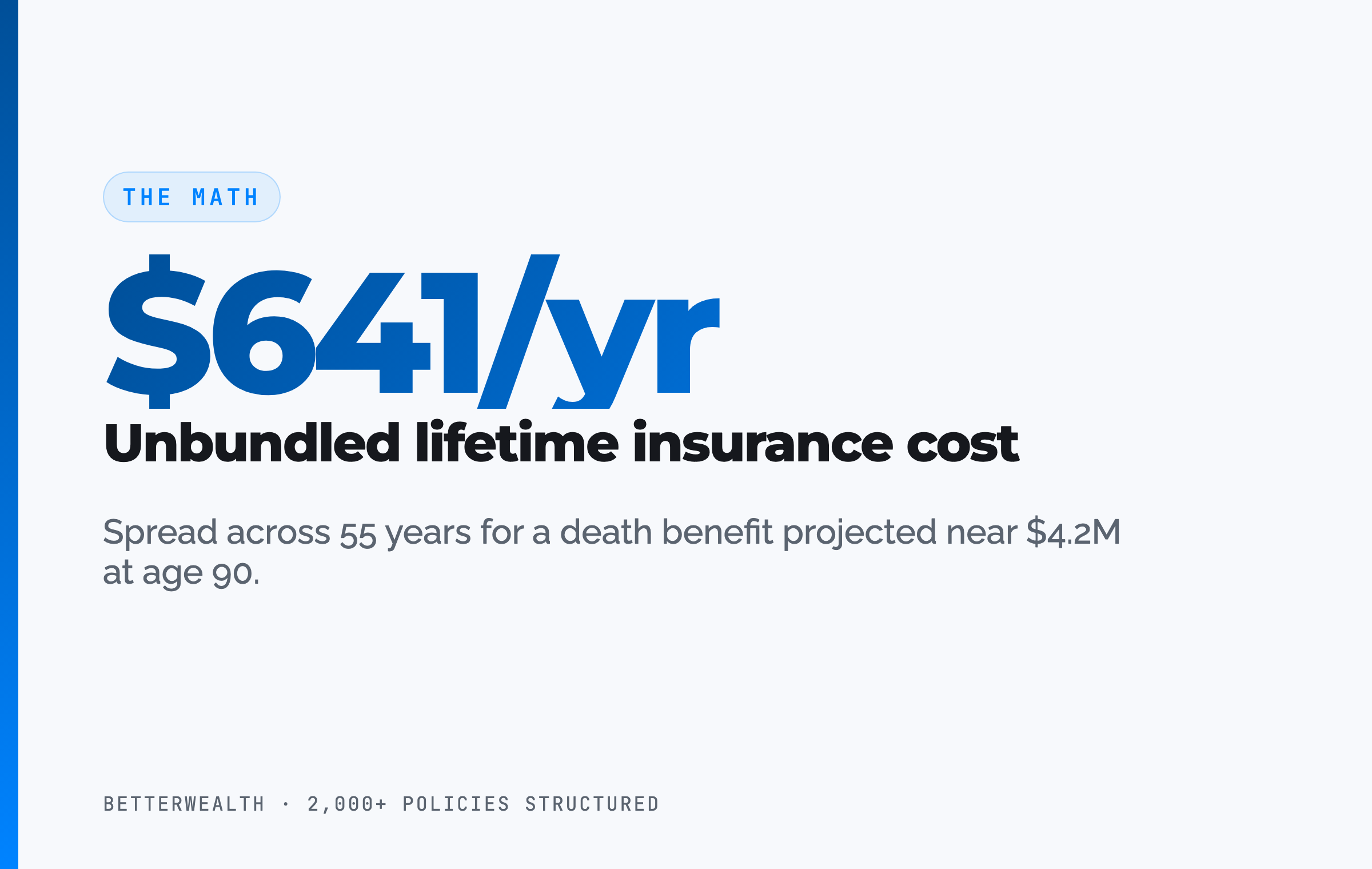

- Unbundled, the lifetime insurance cost worked out to roughly $641 per year for a death benefit projected near $4.2 million at age 90.

- Cash value grows at the dividend credited net of mortality and expense charges, not at the gross dividend rate carriers advertise.

- The And Asset rule still governs: only borrow against the policy when the deployed return clears the carrier's loan cost.

- Whole life is wrong for someone who needs maximum liquidity early or has no use for capital that beats the loan rate.

Watching Trent run the numbers live is worth it: he does the division on screen, year by year, so you can see exactly where each premium dollar goes before any opinion enters the room.

01 / The wrong frameWhy is "whole life vs investing" the wrong question?

It is the wrong question because the two products do different jobs, so isolating one against the other guarantees a misleading answer. A brokerage account is built to grow money at market risk. A whole life policy is built to deliver a guaranteed death benefit, a contractually guaranteed cash value floor, and a non-guaranteed dividend on top. Comparing their growth rates alone is like comparing a car's top speed to a house's square footage.

The comparison that means something holds the cash flow constant. Take one person who needs $1 million of coverage and buys term, then invests the rest. Take a second person who routes the same total dollars into a permanent policy and a smaller term bridge. Now you are comparing two complete plans, not two cherry-picked line items. That is the only version of this question worth answering.

"We are not comparing life insurance by itself to an investment account by itself. Those are not apples to apples. We are comparing two plans built from the same cash flow.", the framing from Trent Fortner's walk-through

02 / The costHow do you unbundle what a whole life policy actually costs?

You unbundle it by separating the front-loaded cost of insurance from the long-run growth, because a base whole life policy concentrates almost all of its internal cost in the first few years. In the illustration, a 35-year-old paid $14,162 a year for a $1 million policy with no paid-up additions rider, just base. Here is what the cash value did, year by year.

- Year 1: $0 cash value. Every dollar of premium went to the cost of insurance, administration, and the commission the carrier pays from its general fund.

- Year 3: $6,380 of guaranteed cash value showed up against the $14,162 premium, about 45% of the deposit.

- Year 4: the in-year cash value increase reached roughly 96% of the premium. Almost the entire deposit now stayed as cash value.

- Year 5 and beyond: every year, the cash value increase exceeded the premium paid. By year 15, the annual increase ran near twice the premium.

So the cost is real, and it is concentrated. Across the first four years, premiums totaled $56,648. Cash value at the end of year four, including posted dividends, was $21,361. The difference, $35,287, is the total cost of insurance, administration, and commission absorbed in those years. From year five on, there is no further drag of that kind, because each premium dollar adds more than a dollar of value.

Now spread that $35,287 across the years the death benefit stays in force. A preferred-plus 35-year-old projected to age 90 carries the policy 55 years. Divide: about $641 per year. That is the term-equivalent annual cost of a death benefit projected near $4.2 million at age 90.

No 55-year level term exists at that price. None.

One precision point the video keeps honest, and the page must too: cash value does not grow at the headline dividend rate. It grows at the dividend credited net of mortality and expense charges. The guaranteed column assumes the carrier pays no dividend at all and still holds, because reserves are regulated. The dividend is the upside on top.

03 / The 55-year resultWhat happens when you run both plans to life expectancy?

Run to age 90 with the same cash flow, the integrated whole life plan finished ahead of buy-term-and-invest in this case, and it did so while also carrying a seven-figure death benefit the other side had lost. Here is the actual head-to-head from the illustration.

The buy-term-and-invest side: a $1,662 annual term premium plus $12,500 a year into a mutual fund portfolio at an assumed 8% with a 1% management fee and no down years. Over 30 years the portfolio grew to $1,244,000 net of fees. But taxes paid along the way, plus the opportunity cost on those taxes, ran another $470,441. The term premiums, with opportunity cost, ran $139,278. And at age 66 the term coverage was gone.

The whole life side used the same total dollars, $14,162 a year, into the base policy. At age 65 it held $887,508 of cash value. Because the policy's tax treatment meant no annual tax bill, the $470,441 those taxes would have consumed stayed in the checking account, where at a 6% assumed return it became real recoverable money. Add it up: $1,357,949 against the portfolio's $1,244,000. Plus a $1,775,539 death benefit at 65, against zero.

This was a plain vanilla base policy from a strong carrier, not an engineered design. Same cash flow, longer life, more certainty, and a legacy the buy-term path no longer has.

One caveat worth stating, because we will not pretend the assumptions are neutral. The 8% with no down years flatters the investment side. The whole life numbers are guaranteed plus a non-guaranteed dividend that can change. The comparison hedges on both sides, and even hedged, the integrated plan held its ground.

Whole life is a fit for a specific person, not everyone.

It fits you if

- You have a long horizon and stable cash flow

- You want guaranteed access to capital without liquidating

- You can name a use for capital that beats the loan cost

- A death benefit and asset protection matter to your plan

It does not fit you if

- You need maximum cash in the first year or two

- You are still digging out of high-interest debt

- You want a pure market growth vehicle

- You have no productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether this belongs in your plan. If you are in the second, we will tell you that too.

Book a Discovery Call04 / The And AssetWhere does The And Asset change this comparison?

The And Asset changes the comparison by refusing to treat the policy as the finish line. In the math above, whole life already held its own as a savings-and-protection vehicle. The And Asset is what you do with the cash value once it is there, and it is where the strategy stops being a defensive choice and becomes a capital tool.

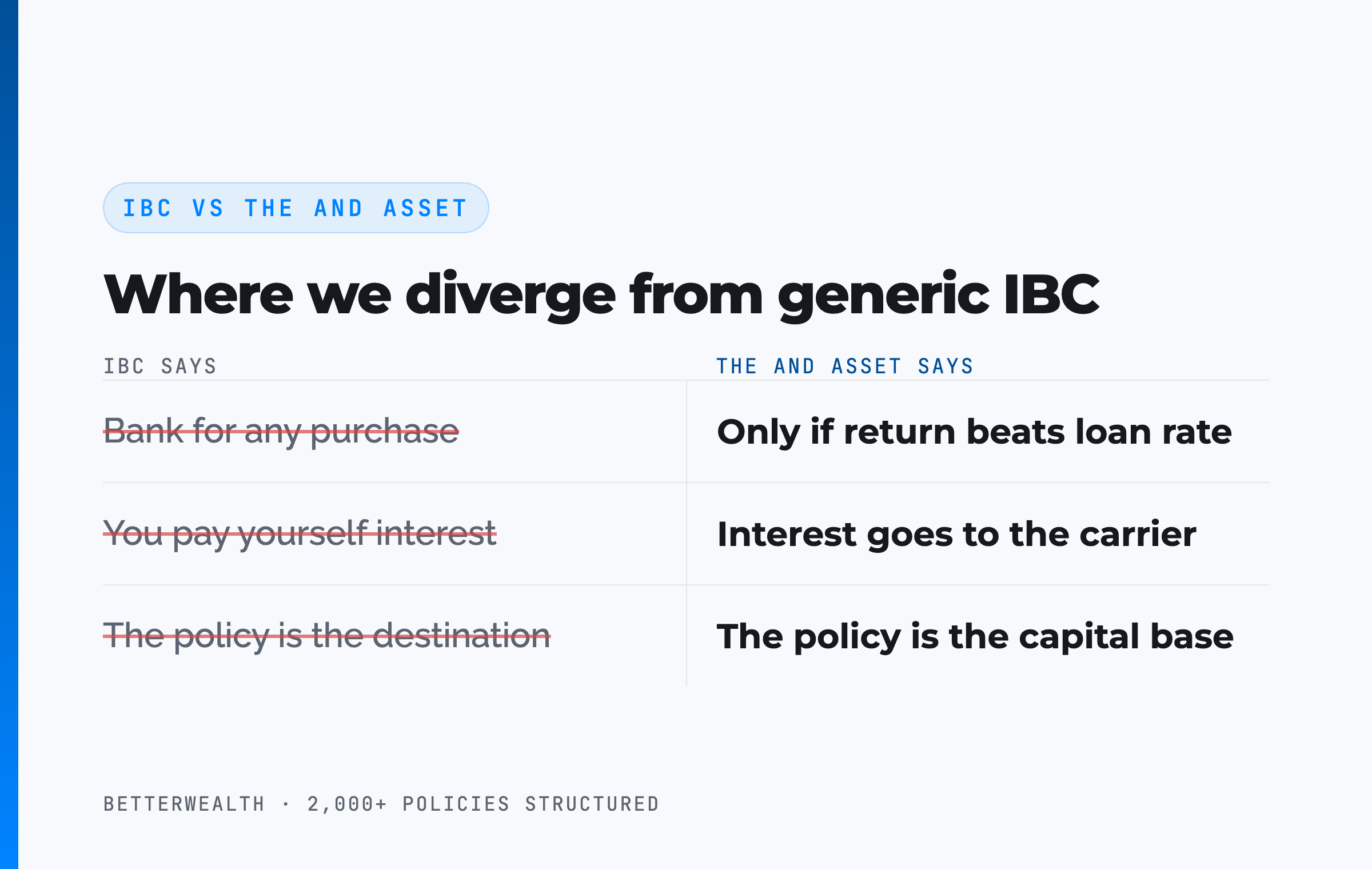

Nelson Nash pioneered the idea of using whole life as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose it to the opportunity cost of idle capital. We credit that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal bank for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will earn a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of its internal charges. The policy is the capital base, not the destination.

Trent gets to the heart of it on camera when he asks why you would ever create a policy loan in the first place. The answer: to buy another asset that produces more cash flow, lifting the total return on the same dollar. That is the AND. The policy grows. The deployed capital grows. One dollar, two jobs.

The math has to work. Every time.

05 / The mathDoes the deployed return beat the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow at all. This is the entire test, and it is the line that separates The And Asset from a marketing pitch. Policy loan rates vary by carrier and rate environment. At the time of writing many carriers fall in the 5 to 6% range, but treat any specific number as a variable to verify, not a constant.

The structure is simple. You borrow against the cash value at the carrier's loan rate. The policy keeps compounding on its full value, including the borrowed portion, adjusted by the carrier's recognition method. Your deployed capital earns its own return. If that return clears the loan cost, you are ahead on the spread and the dollar has done two jobs. If it does not, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

06 / DesignWhy did the video use a base policy when BetterWealth uses PUAs?

The video used a base-only policy on purpose, to prove the mechanics hold even without optimization. Trent's point was that the cost structure and the long-run result work from the base alone, so no one can claim the numbers depend on a clever rider. That is an honest teaching move.

For The And Asset, we design differently. We minimize the base premium and load a paid-up additions rider as heavily as the IRS allows, pushing cash value toward the limit without creating a Modified Endowment Contract. The base/PUA split is the single design decision that determines how much capital is accessible in the early years. A heavy PUA design does not produce day-one break-even; cash value still trails contributions through the first few years. What it does is get more capital working sooner, which matters when the whole point is to deploy against the loan cost.

So read the 55-year comparison as the floor, not the ceiling. The base policy already competed with buy-term-and-invest. A properly structured paid-up additions design changes the early-year liquidity, which is the part that makes The And Asset usable rather than merely sound.

07 / The protection layerWhat does whole life include that an investment account never will?

Whole life carries contractual features a brokerage account cannot replicate, and they belong in any honest comparison. The headline is the death benefit, permanent rather than expiring, but the structural features matter just as much over a lifetime.

Guarantees, access, and the disability waiver

The guaranteed cash value column holds even if the carrier never pays another dividend, because reserves are regulated and the contract is enforceable. Loans against cash value are guaranteed access; you are not underwritten for them and they cannot be called, so the capital is available when you decide, not when a lender allows. The disability waiver of premium rider, if you qualify, keeps the policy funded by the carrier while you stay disabled. No 401(k) administrator will keep funding your account if you cannot work. That single feature has no investment-account equivalent.

None of this makes whole life a market alternative. It makes it a different instrument with a floor, a benefit, and access guarantees that a pure growth account does not offer. The cost of those features is the early-year drag you already saw. Whether they are worth it depends on whether you value certainty and access over maximum day-one liquidity.

08 / Where it losesWhere does whole life genuinely lose to investing?

Whole life loses in several real situations, and pretending otherwise is how agents destroy trust. Here they are, plainly.

It loses on early liquidity. A base policy can show zero cash value in year one and still trail cumulative contributions through year four. If you need maximum access immediately, this is the wrong vehicle. It loses for someone carrying high-interest debt. A 22% credit card balance is a guaranteed loss that no policy dividend will outrun; clear that first. It loses on raw growth potential against equities over a long bull run, because guaranteed-plus-dividend is not built to match market returns, and we will not claim it is. And it loses for anyone who has no productive use for borrowed capital, because then The And Asset has nothing to deploy into and you are left with an expensive savings account.

It is not for everyone. We mean that.

If you are early in building wealth, sitting on high-interest debt, or chasing the highest possible market return, whole life is not where to start. Say it before the benefits, not after.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to run exactly this kind of comparison: policy versus investment, base versus PUA, deploy versus hold. Free, email-gated, no spam.

Open the Vault09 / Head to headWhole life integrated vs buy-term-and-invest

Holding the cash flow constant, the integrated whole life plan and the buy-term-and-invest plan diverge most on taxes, the death benefit, and what happens after age 65. The table below uses the illustration figures from the reviewed case.

| Dimension | Whole life integrated | Buy term + invest |

|---|---|---|

| Annual cash flow | $14,162 into the policy | $1,662 term + $12,500 invested |

| Balance at 30 years | $887,508 cash value + $470,441 in recovered, untaxed dollars = $1,357,949 | $1,244,000 portfolio, after $470,441 lost to taxes and opportunity cost |

| Death benefit at 65 | $1,775,539, permanent | $0, the 30-year term has expired |

| Tax on growth | No annual tax; loans not taxable income under IRC 7702 | Capital gains and dividends taxed along the way |

| Access & control | Guaranteed loan access, not callable, plus disability waiver | Fully liquid, but no protection features or guarantees |

Balance. The portfolio's headline $1,244,000 looks larger until you account for the $470,441 the investor paid in taxes and lost opportunity cost. The policy's tax treatment left those dollars in hand, which is why the integrated plan finished at $1,357,949 on the same cash flow.

Death benefit. At 65 the term coverage is gone and the estate drops by $1 million the day after. The whole life estate is larger and permanent, which also frees the other assets to be spent rather than held in reserve for survivors.

Taxes and control. Policy loans are not taxable income under Section 7702, and the loan cannot be called. The buy-term path keeps full liquidity but carries an annual tax bill and no access guarantees. The integrated plan trades a little early liquidity for tax treatment and control it keeps for life.

A composite: the investor who deployed at year seven

Consider a 39-year-old real estate investor, preferred non-tobacco, funding an overfunded whole life policy at $48,500 per year on a 30/70 base/PUA design. This is a representative composite, not a single named client, and it layers the deployment step the video did not cover onto a properly structured policy.

Through the first four years, cash value trails cumulative contributions, exactly as a real policy should, even with a heavy PUA rider. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year seven, with roughly $367,000 of accessible cash value, the investor borrows $142,000 against the policy to fund the rehab and refinance on a rental acquisition. The stabilized deal returns an estimated 13.8% IRR. The loan cost is illustrative at around 6%, so the spread works in the investor's favor by nearly eight points. The policy keeps compounding on its full value, net of mortality and expense charges, the entire time. Repayment runs on a 43-month schedule funded by the property's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen this strategy work exactly as designed and fail when there was nothing to deploy into. On a discovery call, a practitioner runs your actual numbers and tells you whether whole life belongs in your plan, or whether you are better off investing the difference. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQWhole life vs investing questions

Is whole life insurance better than investing?

Whole life insurance and investing answer different questions, so comparing them directly is the wrong frame. The honest comparison is whole life integrated into your plan versus the same dollars spent on term insurance plus a separate account. Over a full lifetime, the integrated version often produces a similar or larger after-tax balance plus a death benefit the buy-term-and-invest path no longer has.

Why is there no cash value in year one of a whole life policy?

In year one of a base whole life policy, most or all of the premium goes to the cost of insurance, administration, and the commission paid from the carrier's general fund, so cash value can be zero or near zero. Cash value builds quickly after the early years, and from roughly year five on, each premium dollar adds more than a dollar of cash value.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does whole life insurance really cost less than term over a lifetime?

In the illustration reviewed here, the internal cost absorbed in the first four years, spread across 55 years to age 90, worked out to about $641 per year for a death benefit projected near $4.2 million. No 55-year level term policy at that price exists for a 35-year-old. Term is cheaper for a fixed period; permanent coverage that never expires is the comparison whole life wins on cost.

Are whole life dividends taxable?

Whole life dividends are treated by the tax code as a return of premium, so they are not taxable while inside the policy and remain tax-free when taken in cash until you exceed your cost basis (total premiums paid). Amounts taken beyond cost basis can be taxable, and a Modified Endowment Contract changes this treatment, so design matters.

What does "net of mortality and expense" mean for cash value growth?

Cash value does not grow at the headline dividend rate. It grows at the dividend credited net of mortality and expense charges, which is the figure that actually compounds inside the policy. Any agent quoting the gross dividend rate as your growth rate is overstating the return.

When does a whole life policy break even?

For a healthy individual, a well-designed whole life policy reaches break-even, where total cash value catches total contributions, around year five or later. Any illustration showing break-even in year one or two is not realistic. Adding a paid-up additions rider accelerates early cash value but does not produce day-one break-even.

What is a disability waiver of premium rider?

A disability waiver of premium is a rider where, if you become disabled and qualify, the carrier pays your premiums for you while you keep every benefit of the policy. A 401(k) or brokerage account has no equivalent feature, which is part of why permanent insurance behaves differently from a pure investment.

Should I use dividends for paid-up additions or take them in cash?

It depends on your goal. If you are still building death benefit and cash value, directing dividends to paid-up additions compounds the policy faster. If you have insured to your target and want capital elsewhere, taking dividends in cash can make sense. You can change the dividend option on the policy anniversary, so the choice is not permanent.

Why does BetterWealth use a paid-up additions rider when the video showed a base policy?

The video used a base-only policy to prove the mechanics work even unoptimized. For The And Asset, BetterWealth designs the policy with a heavy paid-up additions rider to push early cash value to the IRS limit without creating a Modified Endowment Contract, so more capital is accessible sooner to deploy against the loan cost.

- Nelson Nash, Becoming Your Own Banker, the origin of using whole life as a personal banking system.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- LIMRA, life insurance industry data, including persistency and product benchmarks.

- Penn Mutual, the carrier behind the illustration reviewed in the source video.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Has spent decades working with clients and training advisors to read life insurance contracts honestly. He runs the LEAP planning model and the live Penn Mutual illustration in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether whole life beats investing the difference in your situation, book a discovery call. We will tell you if it does not.