.png)

Whole life insurance as an asset class is the idea that a properly structured policy behaves like a private, tax-advantaged bond: it lowers portfolio volatility, compounds net of internal costs, and can be borrowed against without interrupting growth. The smartest minds in life insurance now treat it as capital, not a product.

Most people file whole life insurance under the wrong heading. They put it next to term insurance, or next to a savings account, or next to a mutual fund, and then they judge it on the return number. Judged that way, it loses every time, because it was never built to win a growth contest. The category is the mistake, not the product.

Every year a room of the most analytical people in this industry meets to compare notes. This year, across two and a half days and more than thirty speakers, a pattern kept surfacing. A PhD who studies portfolio construction, a calculator builder who has spent decades modeling this math, a CPA-turned-tax-strategist, and an entrepreneur who funds private deals all arrived at the same conclusion from different starting points.

The point they kept circling is that a properly structured whole life policy is best understood as an asset class, a stable, tax-advantaged bucket of capital that improves how everything else in a portfolio performs. Not a thing you buy for the death benefit and forget. A holding with a job.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and this is the exact reframe we build every design around. It is also the reframe that separates The And Asset from how most people teach infinite banking. This piece covers the convergent thesis from the summit, the portfolio math behind it, the tax case, how to actually use a policy as a portfolio asset, and the honest limits of the strategy.

- Whole life belongs in the asset-allocation conversation, sitting closer to a private bond than to a growth investment or a savings account.

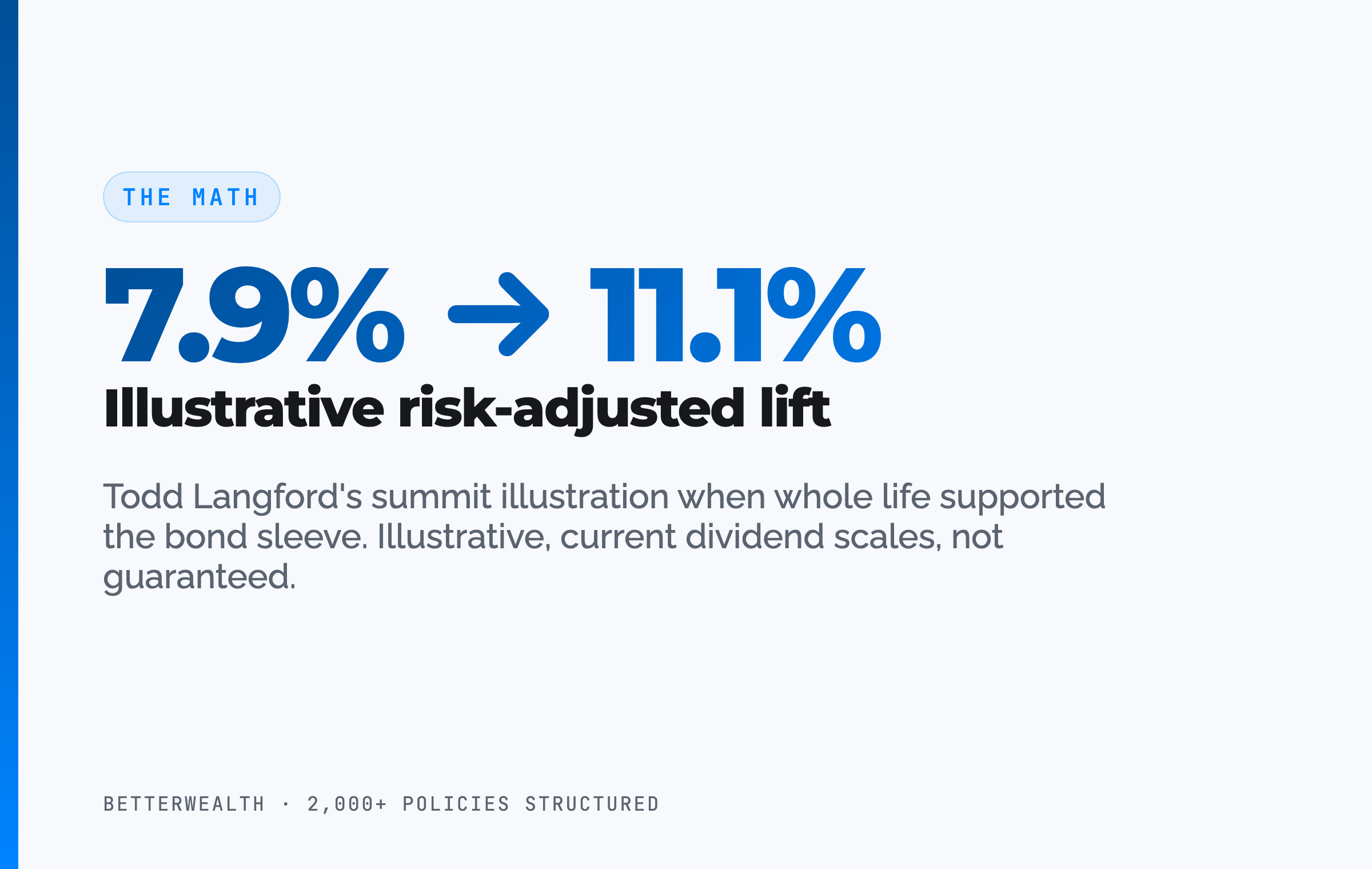

- Substituting a policy for part of a bond sleeve can raise a portfolio's risk-adjusted return, illustrated at the summit as roughly 7.9% to 11.1%.

- The cash value compounds at the dividend net of mortality and expense charges, and it grows without annual taxation under current law.

- Policy loans are not taxable income under IRC Section 7702, giving the asset a tax profile a 401(k) and a brokerage account cannot match.

- The And Asset rule governs the whole thing: only borrow when the deployed return clears the carrier's loan cost.

- Vet the carrier's surplus and financial strength, not just its dividend rate. The company behind the contract matters over 30 years.

In the full recap, we walk speaker by speaker through the summit and pull the specific nuggets, including the portfolio numbers and the tax rules that reframe how whole life should be used:

01 / The problemWhy most people misjudge whole life insurance

People misjudge whole life because they file it in the wrong category and then measure it against the wrong benchmark. Put a policy next to an S&P 500 index fund and it looks slow. Put it next to a savings account and it looks illiquid early. Both comparisons are category errors, because a whole life policy is not trying to be either of those things.

The right question is not "does this beat the market." The right question is "what job does this do in a portfolio that nothing else does as well." The answer is stability, tax treatment, and access to capital that keeps compounding while you use it. When you frame it that way, the return number stops being the headline and starts being one input among several.

Stop selling life insurance so people can buy life insurance. The product is fine. The category people file it under is the problem.

02 / The convergenceWhat did the smartest minds in life insurance actually agree on?

They agreed that whole life should be treated as a strategic asset, not a transaction. Different speakers said it in different vocabularies, and that is what made the pattern convincing. Nobody coordinated it. It surfaced on its own.

Tom Wall, who holds a PhD and studies portfolio construction, framed it through the Sharpe ratio: blend life insurance in as an asset class and you can hold the same expected return while cutting volatility, which improves the risk-adjusted result. Todd Langford, who has spent a career building financial calculators, put concrete numbers on that same idea. Justin Donald, who funds private deals, told the room the classic 60/40 portfolio is dead and described using policy loans to fund acquisitions. Revan Vega put the mindset shift bluntly: stop selling life insurance, get the philosophy right, and people buy it because it solves a real problem.

Different words. One thesis. It is an asset class.

The through-line matters because these are not marketers. They are the technicians, the modelers, and the operators. When the people who run the math and the people who deploy the capital land in the same place, the conclusion is worth taking seriously.

03 / The frameworkWhat does it mean to treat whole life as an asset class?

Treating whole life as an asset class means giving the policy a defined role in your capital structure and holding it to that role, the same way you would a bond allocation or a cash reserve. That is the mechanical part. The discipline layered on top is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

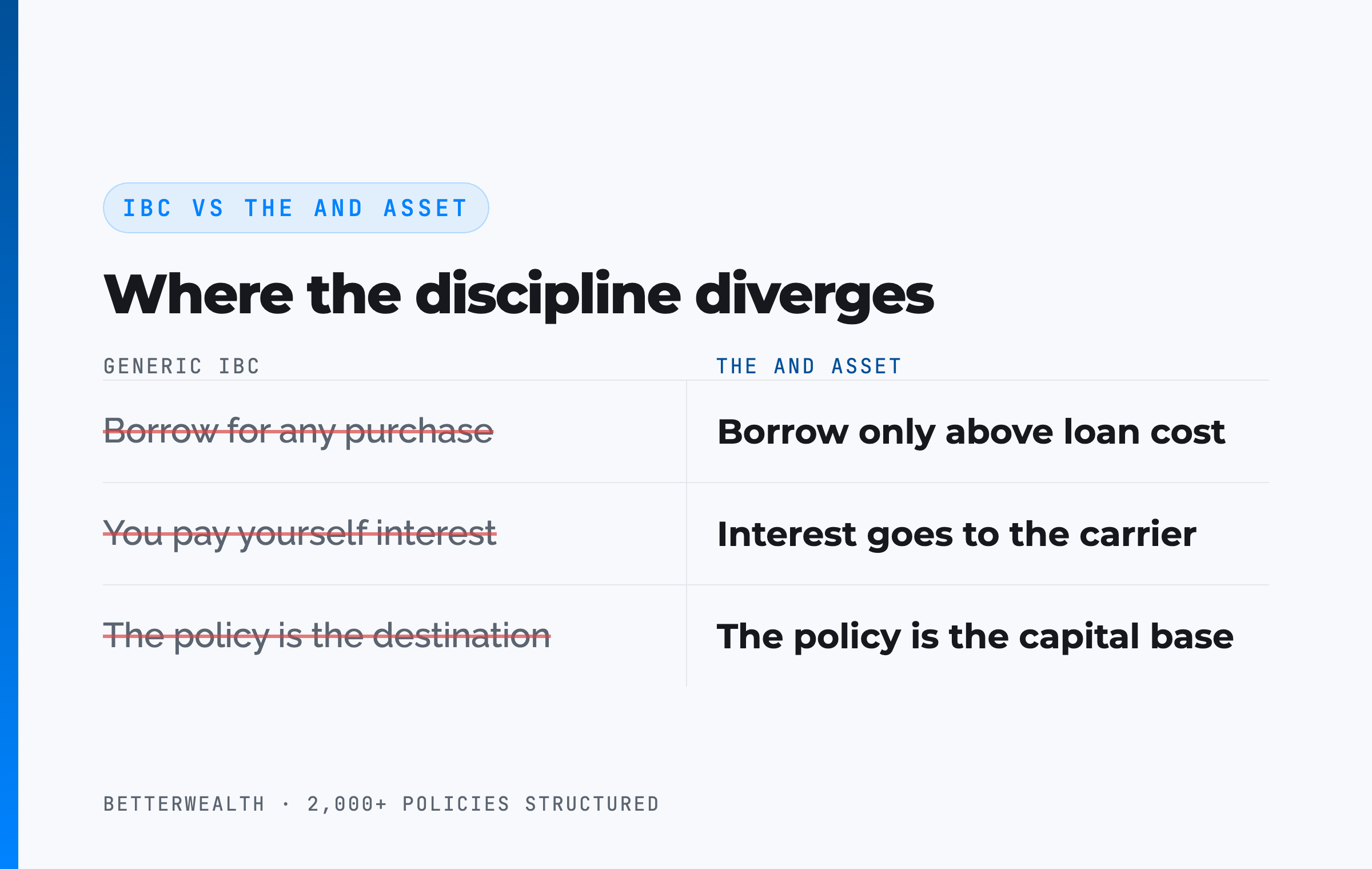

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers also say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy keeps compounding.

That distinction is exactly why the asset-class framing fits us and not the generic pitch. An asset class earns its place through the job it does inside a portfolio. It does not earn its place by being sold as a cure-all. The policy is the capital base. The value is created in what you deploy that capital into and in how the asset steadies everything around it.

Marketers have ruined how this strategy gets explained. The policy is not the destination. It is the stable base you build the rest of the plan on top of.

04 / How it worksHow do you actually use a policy as a portfolio asset?

You use a policy as a portfolio asset through five steps, and the order matters. The design is an overfunded whole life policy built for cash value, not for maximum death benefit. Here is the sequence we follow when we structure one.

- Assign the policy a job. Decide what role it plays. For most of our clients it takes over part of the work a bond allocation used to do: the stable, low-volatility bucket, plus a capital base to borrow against. A clear job keeps the design honest.

- Structure for cash value. Minimize base premium and load the paid-up additions rider as heavily as the IRS allows without triggering a Modified Endowment Contract. The PUA rider is the engine. The base/PUA split is the single design decision that determines early cash value.

- Fund and capitalize. Fund consistently, ideally for 10 or more years, and let the early years capitalize. Cash value grows at the dividend net of mortality and expense charges. Do not expect day-one break-even. A healthy policy reaches break-even at year 5 or later.

- Borrow against it. Take a policy loan collateralized by cash value. The death benefit and cash value still belong to you. You are borrowing against them, not withdrawing from a separate account, so the full value keeps compounding.

- Deploy and repay. Put the borrowed capital into an activity that beats the carrier's loan cost, then repay from the cash flow that activity throws off. The dollar does two jobs at once.

There are two catches, and Tom Wall summed them up in three words: health and patience. You have to be healthy enough to qualify for a well-priced policy, and patient enough to let the cash value build. Miss either and this is the wrong tool. Meet both and you have an asset that funds itself over time.

Health gets you in. Patience makes it work.

Whole life as an asset class fits a specific person.

It fits you if

- You already deploy capital and think in IRR and opportunity cost

- You have a long horizon (10+ years)

- You want a stable bucket that keeps compounding while you use it

- You can name a use for capital that beats the loan cost

It does not fit you if

- You are early in building wealth

- You need maximum liquidity in year one

- You are carrying high-interest debt

- You want a market alternative or a savings account

If you are in the first column, a 30-minute conversation will tell you whether this belongs in your capital structure. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes whole life really improve a portfolio's returns?

It can improve a portfolio's risk-adjusted return, which is a different claim than a higher headline yield. This is the part of the summit that made the technicians lean in, so it is worth stating precisely.

Todd Langford illustrated a familiar 60/40 portfolio paired with a buy-term-and-invest-the-difference approach, landing at roughly a 7.9% blended return. He then reworked the same portfolio so that a whole life allocation supported the role the bonds were playing, letting the bond sleeve effectively fund the premium. In his illustration, the blended return moved to about 11.1%. Those numbers are illustrative. They assume current dividend scales hold, and dividend scales are declared annually and are not guaranteed. The mechanism, though, is real: whole life carries low volatility and a contractual floor, so substituting it for part of the volatile bond sleeve can lift the risk-adjusted result. That is the Sharpe ratio point Tom Wall made from the academic side.

Here is the discipline that keeps this from becoming a sales slide. When you borrow against the asset to deploy capital, the return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow. Loan rates vary by carrier and rate environment. At the time of writing many carriers fall in the 5 to 6 percent range, but treat any specific number as a variable to verify, not a constant. If the deployed return clears the loan cost, the dollar does two jobs. If it does not, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

06 / The tax caseWhy the tax treatment matters more every year

The tax treatment is a large part of why this asset class earns its place, and the case for it strengthens as tax uncertainty grows. Ed Slott, one of the country's most respected voices on retirement tax planning, put it simply at the summit: tax preparation costs you money, tax planning saves you money, and tax deferral just means not yet.

Deferred accounts like a 401(k) postpone the bill to a future rate you do not control. David McKnight, who built the Power of Zero framework, argued that with rates historically low, paying the tax now at a known rate often beats deferring into an unknown one. Whole life sits in a different bucket entirely. It is funded with after-tax dollars, the cash value grows without annual taxation under current law, and policy loans are not taxable income under IRC Section 7702. There is no upfront deduction, which is the honest tradeoff. In exchange you get a bucket that a future rate change cannot reach the same way.

Slott's example landed the point. A client received a $5 million death benefit, income-tax-free, at the exact moment their family needed it. No deferred account delivers capital that way. The tax code treats life insurance as its own category, and that category is worth understanding before you assume every dollar should go into the deferred bucket.

The best tax rate is zero. A deferred account is a bill you have not opened yet, at a rate someone else will set later.

07 / Where people get this wrongThe oversell that ruins the strategy

People get this wrong when they let a marketer sell whole life as a product with no downside, which is the fastest way to end up with a badly designed policy doing a job it was never structured for. The summit was refreshingly free of that pitch, and that was the point. Van Miller, a 74-year-old legend in the business, told the room to be as invisible as possible in the presentation, because the strategy is not about the person selling it.

The oversell shows up in three ways. First, the return comparison, where an agent stacks cash value growth against the stock market as if they were competing for the same job. Second, the "pay yourself interest" line, which is factually wrong, because the interest on a policy loan goes to the carrier. Third, the universal pitch, where whole life is presented as right for everyone. It is not. An asset class is right for the portfolio that needs the job it does. It is wrong for the portfolio that does not.

If someone tells you it has no downside, close the laptop.

08 / The tradeoffsBenefits and the real limits

The benefits are real and so are the limits, and honest treatment of both is what separates an asset-class conversation from a sales pitch. The benefits: low volatility, tax-advantaged growth, access to capital that does not interrupt compounding, and a death benefit that transfers efficiently. Those are the jobs the asset does well.

The limits are just as concrete. Early liquidity is lower than a savings account or a brokerage position, because a healthy policy does not reach break-even until year 5 or later. It requires health to qualify at a good price. It rewards a long horizon and punishes a short one. And it does nothing for someone in a high-interest-debt crunch, because it compounds advantages over time rather than solving an immediate cash problem. If liquidity in year one is your top priority, this is not your asset.

Weigh those against each other honestly and the asset sorts itself. It is a patient, stable, tax-advantaged holding for someone who already has capital in motion. It is not a rescue, a market substitute, or a savings account.

09 / Due diligenceHow do you vet the company behind the policy?

You vet the carrier by looking past the dividend rate at its surplus, its ownership, and its financial strength ratings, because a multi-decade strategy exposes you to the company's staying power. Two researchers at the summit, Tom Gober and Barry Dyke, made this the uncomfortable centerpiece of their sessions.

Gober, who maintains a database of insurer financials, pointed out that surplus is the cushion a carrier draws on when claims spike, and that surplus is declining at some companies while private equity has moved aggressively into insurance ownership. With roughly 700 carriers in the market, the company behind the contract is a variable, not a given. Dyke, whose research exposed how banks and corporations quietly use this asset, reminded the room that the United States ranked last, 30 of 30, in a measure of retirement preparedness. The safe money still flows to well-capitalized mutual insurers for a reason.

The practical filter is straightforward. Favor a mutual carrier with a long, unbroken dividend record, strong surplus, and top ratings from AM Best and COMDEX. The dividend rate is one input. Financial strength over 30 years is the one that actually protects the strategy.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and carrier due-diligence tools we use to decide how a policy fits into a portfolio. Free, email-gated, no spam.

Open the VaultA composite: the business owner who used the policy as his bond sleeve

Consider a 44-year-old business owner, preferred non-tobacco, who reallocates part of his conservative capital into an overfunded whole life policy at $63,500 per year, split 25/75 base to PUA. This is a representative composite, not a single named client.

Through the first several years, cash value trails cumulative contributions, exactly as a real policy should. By year four each premium dollar starts adding more than a dollar of cash value. At year six, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year nine, with roughly $623,000 of accessible cash value, he borrows $214,000 against the policy to take down a piece of income-producing real estate. The property returns an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread works in his favor by nearly eight points. The policy keeps compounding on its full value the entire time, still doing the stable-bucket job in his portfolio. Repayment runs on a 44-month schedule funded by the property's own cash flow.

The portfolio effect is the quieter win. By holding this asset in place of part of his bond allocation, his overall mix carries less volatility for the same expected return, and he has a capital base he can borrow against on his terms instead of a lender's.

One dollar. Two jobs. That is the And.

10 / Head to headWhole life against the other places capital sits

Compared to the other buckets an entrepreneur uses, whole life as an asset class trades day-one liquidity for stability, tax treatment, and control. The table sets it against a bond allocation, a 401(k), and a taxable brokerage account on the dimensions that matter for capital strategy.

| Dimension | Whole Life (And Asset) | Bond Allocation | 401(k) | Taxable Brokerage |

|---|---|---|---|---|

| Role in portfolio | Stable, low-volatility bucket plus a borrowable capital base | Stability and income, but no borrowable base | Long-term retirement growth, tax-deferred | Growth and full liquidity |

| Growth | Dividend net of internal costs; compounds even while borrowed against | Yield, currently modest; rate-sensitive price risk | Market growth, tax-deferred | Market growth, taxed annually on gains |

| Tax treatment | No annual tax; loans not taxable income under IRC 7702; no upfront deduction | Interest taxed as ordinary income yearly | Deferred now, taxed as ordinary income later | Capital gains and dividends taxed yearly |

| Access / control | Loans after ~30 days; you set repayment; loan cannot be called | Liquid, but selling to raise cash locks in price risk | Restricted before 59½ (penalty plus tax) | Fully liquid, settles in days |

Role. A bond allocation gives you stability but no capital base to borrow against. Whole life does both jobs at once, which is why substituting it for part of the bond sleeve can improve the portfolio's risk-adjusted return rather than just duplicating a holding.

Tax. A 401(k) defers roughly $23,000 of income today but taxes every dollar of withdrawal later as ordinary income at a rate Congress sets. Whole life takes after-tax dollars now, grows without annual tax, and returns capital through loans that are not taxable income. Different bucket, different rules, not a replacement.

Control. A bond you sell to raise cash is gone, and you may sell at the wrong price. A policy loan leaves the asset intact and compounding, cannot be called by the carrier, and lets you set the repayment terms. That control is the feature the growth-versus-growth comparison always misses.

FAQWhole life as an asset class, answered

What does it mean to use whole life insurance as an asset class?

It means treating a properly structured whole life policy as a distinct holding in your portfolio, like a private, tax-advantaged bond, rather than as insurance you buy and forget. The cash value compounds net of internal costs, carries low volatility, and can be borrowed against without interrupting that growth.

Is whole life insurance a good investment?

Whole life is not an investment in the way a stock or a syndication is, and comparing its cash value growth to market returns is the wrong test. It is an asset class with a specific job: stability, tax treatment, and access to capital. For entrepreneurs and high-income earners who already deploy capital, that job has real value. For someone seeking maximum growth, it is the wrong tool.

Can whole life insurance replace bonds in a portfolio?

For some investors it can fill part of the role a bond allocation plays. Whole life offers low volatility and a contractual floor, and substituting it for a portion of the bond sleeve can improve a portfolio's risk-adjusted return. It is less liquid in the first few years, so it complements bonds rather than replacing them outright.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Why do the wealthy use whole life insurance?

The wealthy use whole life for control, tax treatment, and access to capital, not for growth. It gives them a stable place to hold capital that keeps compounding while they borrow against it to fund deals. Banks and large corporations use the same asset for the same structural reasons.

Does whole life insurance really improve portfolio returns?

It can improve risk-adjusted returns. Analysis presented by Todd Langford at the 2026 summit illustrated a blended portfolio moving from roughly 7.9% to 11.1% when a whole life allocation supported the bond sleeve. Those figures are illustrative and assume current dividend scales, which are not guaranteed. The point is volatility reduction, not a higher headline yield.

How does whole life compare to a 401(k) for tax treatment?

A 401(k) defers tax now and taxes withdrawals later as ordinary income, at rates you cannot control. Whole life is funded with after-tax dollars, grows without annual taxation, and policy loans are not taxable income under IRC Section 7702. The tradeoff is no upfront deduction. It is a different tax bucket, not a replacement.

Can you use a whole life policy to pay for college?

Yes. A policy can fund college through loans against its cash value, and because it is life insurance, its value is not counted as a parent asset on the FAFSA the way a 529 or brokerage account is. One example presented at the summit funded four years of tuition from a policy and still projected a return of the capital over time.

How do I vet the insurance company behind the policy?

Look past the dividend rate at the carrier's surplus, its ownership structure, and its financial strength ratings from AM Best and COMDEX. Private equity has moved into insurance ownership, and declining surplus is a real concern raised by industry researchers. A mutual carrier with a long, unbroken dividend record and strong surplus is the conservative choice for a multi-decade strategy.

When should you not use whole life insurance as an asset class?

Do not use it if you are early in building wealth, if you need maximum liquidity in year one, if you are carrying high-interest debt, or if you cannot identify a productive use for borrowed capital that beats the loan cost. The strategy rewards a long horizon and discipline. Without both, it is an expensive way to hold money.

What is the health and patience rule for whole life?

It is a summary offered by Tom Wall: whole life has two catches. You have to be healthy enough to qualify for a well-priced policy, and you have to be patient enough to let the cash value capitalize. A policy does not reach break-even until year 5 or later for a healthy individual, so it rewards people who fund it and leave it alone.

- Nelson Nash, Becoming Your Own Banker, the origin of using whole life as a personal banking system.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, insurer financial strength ratings and surplus data used in carrier due diligence.

- LIMRA, life insurance industry data, including persistency and agent-retention benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Twenty-plus years in the life insurance business, Dave joined Caleb for the speaker-by-speaker breakdown in the source video and contributed many of the takeaways referenced above.

The honest 30 minutes about whether this belongs in your portfolio.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your capital structure and tells you whether whole life earns a place in it, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallI founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether whole life belongs in your portfolio, book a discovery call. We will tell you if it does not.