Sequence of returns risk is the danger that the order of your investment returns, not just the average, decides whether your retirement income lasts. The same average return can fund a 26-year retirement or run you dry in year 11, depending purely on which years are bad and when.

Most retirement advice answers one question: how do I accumulate a bigger number? Save more, lower your fees, capture the market's average return, watch net worth climb. That advice is not wrong, but it solves the easy half of the problem and ignores the half that actually ends retirements. The hard half is distribution: turning a pile of money into a paycheck that survives whatever the market does in the years you can least afford a bad one.

The order of your returns, not your average return, is the single highest-magnitude variable in whether your retirement income lasts. A portfolio that averages nearly 10% can still fail if the wrong years land first. Saving more does not fix that, because a larger account run through a bad sequence still fails. The fix is structural.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, almost always as one piece of a larger capital and income plan. In a recent conversation, Caleb sat down with Jason Sanger, a Retirement Income Certified Professional who ran the math live on 26 years of real S&P 500 data. This article rebuilds that conversation into a practitioner's guide: why accumulation and distribution follow different rules, what the two economic powers are, how a volatility buffer works, and where The And Asset fits into all of it.

- Sequence of returns risk, not average return, determines whether retirement income survives a full 26 to 30 year drawdown.

- The same 9.8% average S&P return funded $1.4 million in one order and went broke by year 11 in another.

- The 3 to 4% rule exists because you cannot know your return sequence before you start drawing income.

- An efficient plan uses two economic powers: investments for accumulation, insurance pooling for guaranteed distribution.

- A three to six year volatility buffer of uncorrelated cash value keeps you from selling equities into a down market.

- The And Asset rule still governs: only deploy borrowed capital when the return clears its cost.

If you want to watch Jason run the live spreadsheet, reversing 26 years of returns to show one account thriving and an identical one failing, the full demonstration is on screen here:

01 / The problemWhy doesn't saving more solve retirement?

Saving more does not solve retirement because it only addresses accumulation, and accumulation is the side of the mountain that follows forgiving rules. Climbing the mountain is building the lump sum. Coming back down is turning it into income. On Everest, roughly 80% of deaths happen on the descent, because people plan the climb and not the way down. Retirement works the same way.

Here is the part almost nobody internalizes: the day you retire, the rules of your money change 180 degrees. For 40 working years, the order of your returns was irrelevant. The moment you start pulling income, the order becomes the thing that decides everything. You spent four decades mastering one set of rules. On a single day, a different set takes over, and most people never learned it existed.

Rate of return is a component of a plan. It is not the plan. Until you measure the actual paycheck your assets produce, you do not really know what is going on.

02 / The mathHow can the same returns make you rich or broke?

The same returns can make you rich or leave you broke because withdrawals interact with the order of returns in a way a lump sum never does. This is the demonstration worth sitting with.

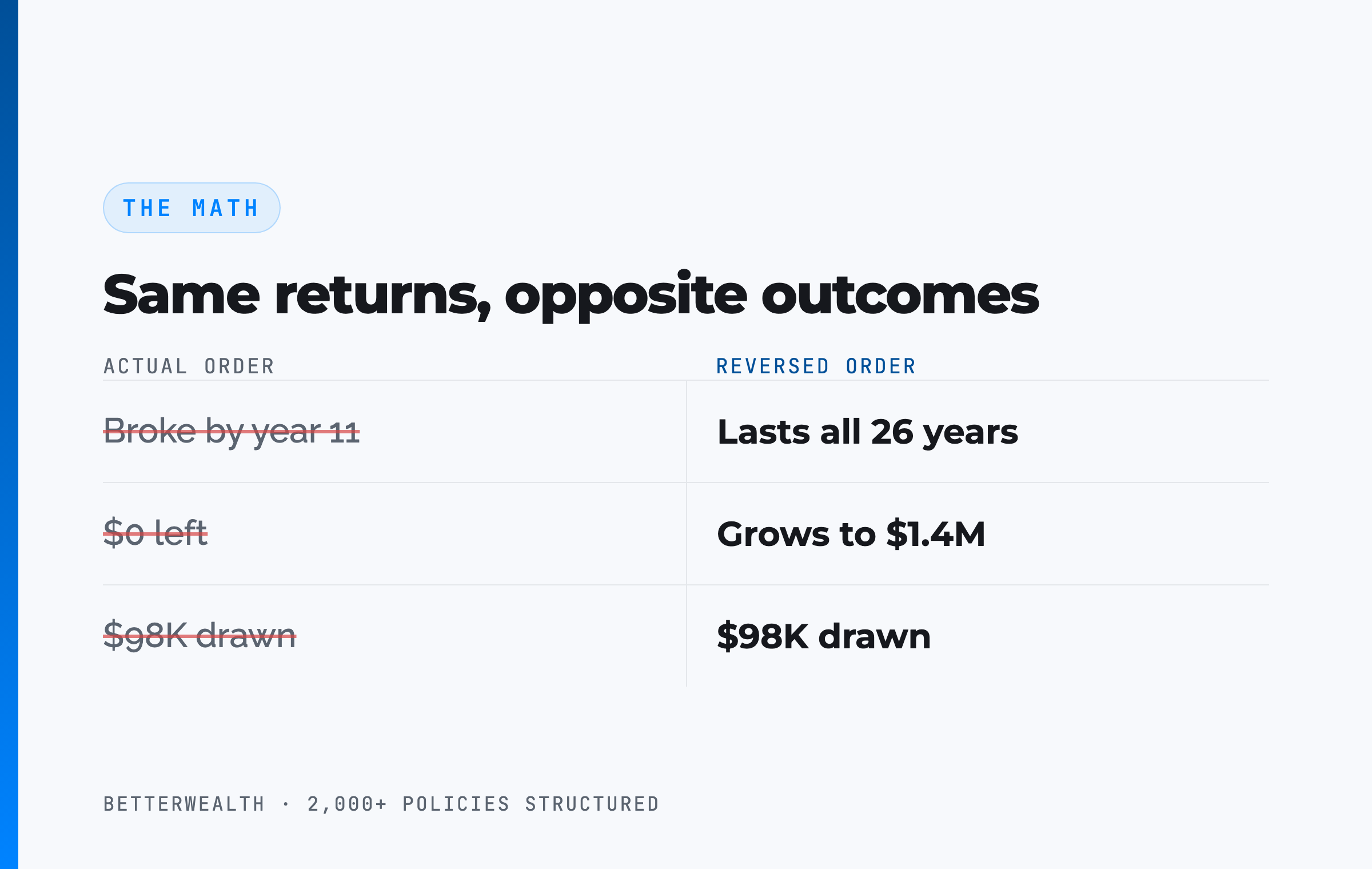

Take the S&P 500 from 1999 through 2024, a 26-year stretch. Add the annual returns, divide by 26, and you get a 9.8% average. Start with $1,000,000 and make no withdrawals: after 26 years you have $7.7 million. Now reverse the order of those exact same 26 returns. The ending value is identical. $7.7 million again. You can jumble all 26 years into any order you like and always land on $7.7 million, because during pure accumulation the sequence is inconsequential.

Now turn on income. Draw $98,000 a year, which is 9.8% of the starting balance, the average return itself. Run the years in their actual 1999-forward order and the account is exhausted in year 11. Run the identical returns in reverse, drawing the same $98,000, and it never runs out. The balance actually grows to roughly $1.4 million while paying full income for all 26 years.

Same average. Same dollars out. Opposite outcomes.

That gap is sequence of returns risk. A run of poor years early in retirement, while you are also withdrawing, permanently shrinks the base that the later good years compound on. The recovery never catches up because there is less money left to recover with.

03 / The 4% ruleWhere does the 3 to 4% rule actually come from?

The 3 to 4% rule comes from sequence risk, not from a bank interest rate. Many people assume the logic is simple: if my portfolio averages near 10%, surely I can safely pull 8% and still come out ahead, or treat 3 to 4% like a savings yield I skim while the principal stays intact. The S&P demonstration shows why that reasoning fails. Pull the average and you can be broke in a decade.

Because you have to start withdrawing today, years before you know what your 26 or 30 year sequence will be, you are forced to plan for a bad one. Withdrawal-rate research and Monte Carlo simulations exist to answer exactly that. They land most plans in a 3 to 4% withdrawal range, with somewhere between a 5% and 25% chance of failure over 30 to 35 years depending on the assumptions. The low number is not caution for its own sake. It is the price of not knowing your sequence in advance.

If you don't know your sequence, your money is almost held hostage. You have to assume the worst, which means living on far less income than your average return suggests you earned.

04 / The frameworkWhat are the two economic powers?

The two economic powers are the investment power and the distribution power, and an efficient plan uses both instead of forcing one to do both jobs. The investment power is the rate-of-return engine. Over time, markets are strong at accumulation. They are also, as the demonstration proved, fragile in distribution, because nobody controls the sequence.

The distribution power is the other half of the industry: the law of large numbers, actuarial science, and the pooling that insurance companies do. Pooling creates certainty that no individual can manufacture alone. Through it, a retiree can secure guaranteed lifetime income payout rates that an unprotected portfolio cannot promise. Those payout rates are not investment returns. They blend interest, return of your own principal, and mortality credits, and the tradeoff is reduced liquidity on the dedicated portion. Stated honestly, that is the deal: you give up access to that slice of capital in exchange for income that cannot be outlived or knocked out by a bad sequence.

The pension that quietly disappeared

Before the 1980s, most workers got both powers automatically through a pension. They did not contribute, did not choose investments, and still received guaranteed income for life, because pensions blend market growth and actuarial pooling by design. Defined contribution plans then largely replaced pensions. The 401(k) and 403(b) are regulated retirement accounts with real advantages, including employer matches, but they are investment plans, not income plans. The risk of producing lifetime income transferred from the employer to you, usually with no explanation that the rules had changed.

A 401(k) is an investment plan. It is not a retirement income plan.

05 / How it worksHow do you build a plan that survives the sequence?

You build a sequence-proof plan by starting at the top of the mountain and reverse-engineering from the paycheck you need. The order of these steps is the whole point.

- Define the paycheck first. Decide the annual income you want in retirement before you decide how much to save or where to put it. Plan around income, not net worth. A million dollars feels like a number; the real question is what reliable income it produces.

- Separate the two phases. Accept that accumulation and distribution follow different rules. While building a lump sum, sequence does not matter. While drawing income, it matters more than anything else.

- Engage both powers. Pair the investment power for growth with the distribution power for guaranteed income. The balance is a personal choice, anywhere from a 50/50 split to a 75/25 tilt toward one, but using only one power is the inefficient default most people fall into without choosing it.

- Run the functions waterfall. Fund the income function first. Whatever capital is not needed to produce your paycheck waterfalls down into liquidity, legacy, and growth. The more efficiently you generate income, the more spills over for everything else.

- Hold a volatility buffer. Keep three to six years of spending in an uncorrelated, accessible asset such as whole life cash value, so a bad early sequence is something you ride out rather than sell into.

This is why the discipline matters: money dedicated to producing your paycheck is, by definition, not truly liquid. If you raid it for something else, you put the income itself at risk. Decide what each dollar's job is, then do not give it a second job it cannot hold.

How many years of buffer is enough?

A volatility buffer protects the first three to ten years of retirement, where a bad sequence does the most permanent damage, and three to six years of spending is the practical range. The first year's return in retirement is the highest-magnitude year of all, because every later year compounds off what it leaves behind. Below three years of buffer, you stay exposed. Above six or seven, the incremental protection shrinks while the opportunity cost of parking that money grows. There is a sweet spot, not a maximum.

Three years minimum. Six is usually plenty.

A buffer asset can do more than absorb shocks. If it also grows and stays accessible, the same dollars protect your income and stay available for opportunities. That dual role is exactly where our framework comes in.

This approach fits a specific person doing specific things.

It fits you if

- You are 5 to 20 years from retirement and planning ahead

- You think in income and opportunity cost, not just net worth

- You want control over your capital and your tax brackets

- You can name a productive use for capital that beats its cost

It does not fit you if

- You are early in building wealth with little saved yet

- You want a single product to solve everything

- You are looking for a savings account, not a strategy

- You are in a high-interest debt crisis needing a quick fix

If you are in the first column, a 30-minute conversation will show you how the two powers fit your numbers. If you are in the second, we will tell you that plainly.

Book a Discovery Call06 / The And AssetWhere does whole life and The And Asset fit?

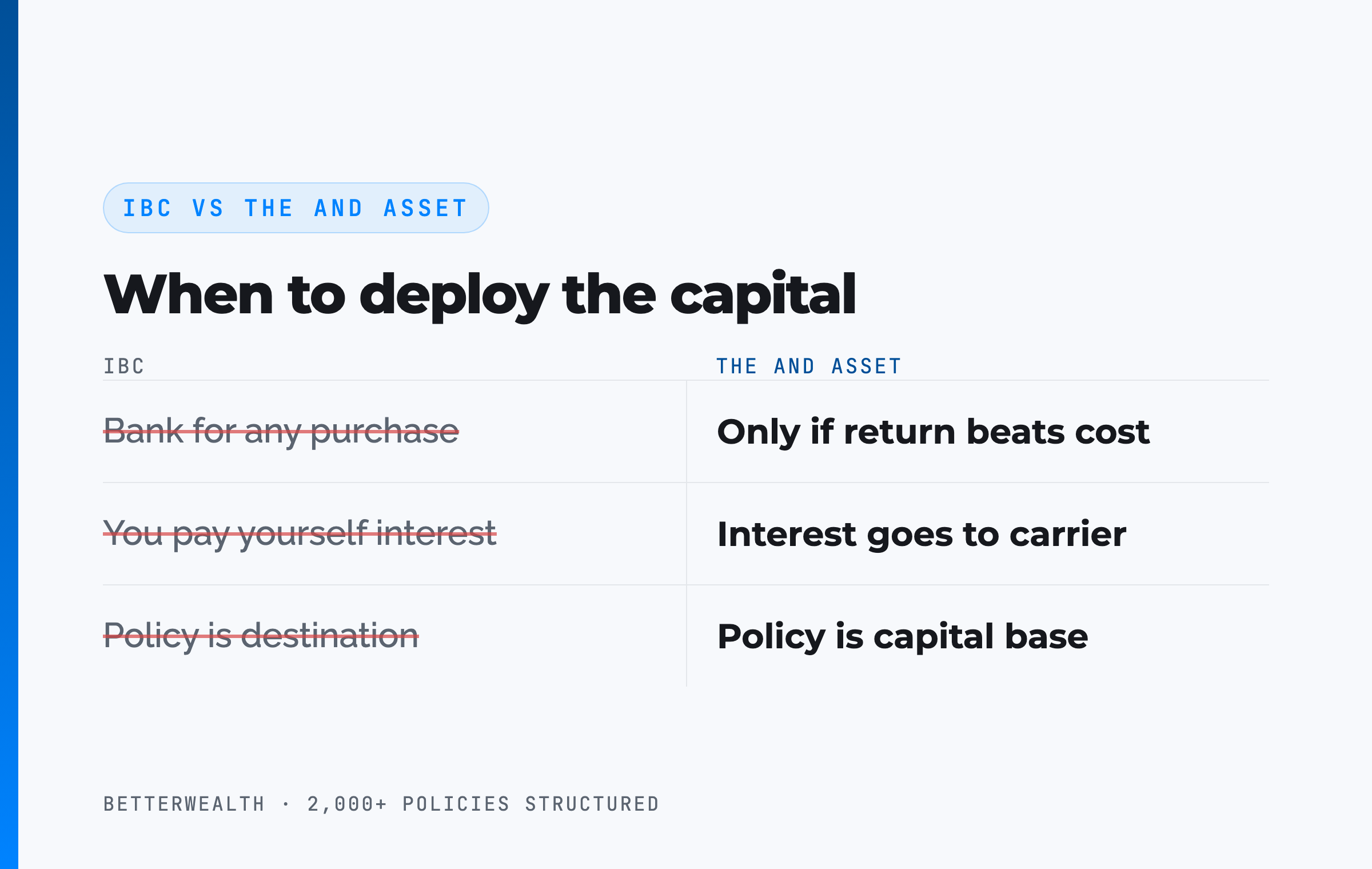

Whole life fits as the distribution-power and buffer asset, and The And Asset is the discipline that decides when to put its capital to work. Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker. His core insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the return on what you do with it clears the cost of accessing it. Anything less is an expensive way to spend money. Many IBC marketers also say you are paying yourself interest. You are not. The interest on a policy loan goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of mortality and expense charges. The policy is the capital base, not the destination.

In retirement, that discipline has a clean application. A whole life policy is uncorrelated to the stock market, so its cash value makes a strong volatility buffer. In a down year, you spend or borrow from the policy instead of selling equities at a loss. The "return" on that move is the sequence-risk loss you avoid, which can easily clear the cost of accessing the cash. Whole life is also the simpler platform for this job: guaranteed premiums, guaranteed cash value growth, and non-guaranteed dividends layered on top, with no risk the policy collapses if dividends fall. The same dollars protect income and stay available for opportunity. That is the And.

Marketers have ruined how this strategy gets explained. You are not paying yourself interest. The policy's job here is to be the uncorrelated buffer that lets your investments recover instead of forcing you to sell low.

07 / The cost testDoes the use clear the cost of the capital?

Every dollar you access has to do something that beats the cost of accessing it, or you should leave it alone. This is the rate-of-return test that governs The And Asset, and it survives into retirement unchanged. When you borrow against a policy, you pay the carrier's loan rate. Those rates vary by carrier and rate environment. At the time of writing many carriers fall in the 5 to 6% range, but treat any specific number as a variable to verify, not a constant.

The structure of the decision is simple. The policy keeps compounding on its full cash value while the loan is outstanding. If the capital you deploy, or the sequence-risk loss you avoid, produces more value than the loan costs, you are ahead on the spread and the dollar has done two jobs. If it does not, you borrowed money to lose ground slowly. The discipline of that test, applied honestly, is the strategy. There is no free lunch in this game, and anyone who tells you otherwise is selling.

If the use doesn't clear the cost, don't borrow.

08 / Whole life vs IULShould you use whole life or indexed universal life?

Whole life is the lower-variable platform for a long-horizon income and buffer role, while indexed universal life chases higher returns by shifting risk onto the policyholder. Whole life guarantees the premium and a baseline cash value growth, then adds non-guaranteed dividends. If the carrier paid nothing, the policy still cannot evaporate. It is the bulletproof platform when the job is safety and certainty.

Indexed universal life sits on a universal life chassis with more moving parts. Mortality charges and interest-rate assumptions are live calculations, and the carrier can require more premium later if those assumptions do not hold. The per-unit cost of insurance also rises with age. Used for a long-term role, IUL demands in-force illustrations reviewed regularly, especially as you age, so a problem does not quietly develop and surface at 75 or 80 when it is expensive to fix. The pitch for IUL is often that it can do both accumulation and distribution, an investment with an insurance wrapper. The honest read: to project better than guaranteed whole life, you accept downside risk that many buyers do not fully see. You never get the upside for free.

On max-funding with PUAs

Whether to heavily overfund a policy with paid-up additions depends on the job you are asking the policy to do. Permanent life insurance is a long-term asset, not a short-term one. Maximizing year-eight cash value can come at the cost of long-term death benefit, because the pie is a fixed size and emphasizing one area pulls from another. For a pure income-and-legacy role, some designs lean less on aggressive PUA loading. For a capital-access role under The And Asset, a heavier paid-up additions structure (often a 30/70 or 40/60 base/PUA split) accelerates early cash value. The right answer is the design that matches the job, and that requires a real conversation, not a default.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to model income efficiency, volatility buffers, and the two-powers balance for real situations. Free, email-gated, no spam.

Open the Vault09 / The tax questionShould all your money be tax-free?

Concentrating everything into a single tax treatment is a bet on unknown future tax brackets, and it is the kind of one-size answer this whole approach rejects. Some marketers argue that any dollar in a taxable market account is a disservice to you because of taxes. That sounds clean and can be quietly damaging. Whether tax-free wins depends on your time horizon, how aggressive you are, your future income, the bracket you actually retire into, and effects on items like Medicare premiums.

Tax brackets in 20 or 30 years are genuinely unknown. Many assume they must rise. They might not. Policy and administration can move either direction. Planning your entire structure around that single guess is letting the tail wag the dog. Build the efficient big-picture strategy first across taxable, tax-deferred, and tax-free buckets, then use tax positioning to refine at the edges. Diversifying your tax exposure gives you control over your bracket each year, which is worth more than chasing a single label.

Be agnostic. Every tool has a purpose, like building a house. Do not use a hammer to do a saw's job, and do not let one product, or one tax theory, pretend to be the whole plan.

A composite: the pre-retiree who freed $189,000 for legacy

Consider a 61-year-old business owner approaching retirement with $1,475,000 across a 401(k) and a brokerage account, wanting $90,000 a year of income. This is a representative composite, not a single named client, and the figures are illustrative.

On the one-power path, a 3.5% safe withdrawal rate means $90,000 of income requires roughly $2,571,429 of dedicated capital. He has $1,475,000. He is short, so he would either spend far less than he hoped or expose the whole account to sequence risk.

On the two-power path, he moves $1,285,714 into a guaranteed lifetime income source paying a 7% payout rate, which produces the full $90,000 a year regardless of market sequence. That payout blends interest, return of principal, and mortality credits, and the tradeoff is that the dedicated portion is no longer liquid. The math frees $189,286 of his $1,475,000 for liquidity and legacy, money the one-power plan had to lock up entirely.

The buffer comes from a whole life policy he began funding at age 49 at $24,000 a year. Through the first three years cash value trailed his cumulative premiums, exactly as a real policy should. It crossed break-even in year five, and by retirement held about $214,700 of accessible cash value, net of internal charges. In a down market year, he spends from that buffer instead of selling equities, then refills it when markets recover. The avoided sequence-risk loss is the return that justifies the move.

Same income. Half the locked-up capital. That is efficiency.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen this approach work and seen it misused. On a discovery call, a practitioner looks at your numbers and tells you whether the two-powers approach, a whole life buffer, or nothing at all belongs in your plan. To learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call10 / Head to headThe tools, and what each is actually good at

No single tool produces income, growth, and certainty equally well, so the efficient plan assigns each tool the job it is built for. The table sets the main retirement-income tools side by side on the dimensions that decide whether your paycheck lasts.

| Dimension | Invested portfolio (401k / brokerage) | Guaranteed lifetime income | Whole life cash value |

|---|---|---|---|

| Best at | Accumulation and growth over time | Producing income that cannot be outlived | Uncorrelated buffer plus tax-favored access |

| Sequence risk | Fully exposed in the drawdown phase | Eliminated on the dedicated portion | Reduces it by replacing down-year withdrawals |

| Income example | $90,000 needs about $2.57M at a 3.5% rate | $90,000 needs about $1.29M at a 7% payout | Not a primary income source; a support asset |

| Liquidity | Fully liquid, settles in days | Dedicated capital gives up liquidity for certainty | Loans against cash value, typically after funding |

Growth. An invested portfolio is hard to beat for accumulation over decades, which is exactly why you do not abandon it. Its weakness is the drawdown phase, where sequence risk runs unchecked.

Income. Guaranteed lifetime income from actuarial pooling can require roughly half the dedicated capital to produce the same paycheck, in the example $1,285,714 at a 7% payout versus $2,571,429 at 3.5%. The payout includes return of your own principal and mortality credits, and you trade liquidity on that slice for certainty.

Buffer and access. Whole life cash value grows uncorrelated to markets and is accessible through policy loans, so it can absorb down years and keep capital available for opportunity. It is a support asset, not the primary income engine.

FAQSequence risk and retirement income questions

What is sequence of returns risk?

Sequence of returns risk is the danger that the order of your investment returns, not just the average, determines whether your retirement income lasts. While you accumulate a lump sum the order is irrelevant, but once you withdraw income, a few bad years early in retirement can drain the account decades sooner than the average return would suggest.

Why doesn't saving more fix the problem?

Saving more grows the lump sum, but it does not change how that lump sum behaves once you draw income from it. A larger account run through a bad return sequence still fails. The fix is structuring the plan around income and reducing sequence risk, not only accumulating a bigger number.

Where does the 4% rule come from?

The 4% rule, now often cited as 3 to 4%, comes from withdrawal-rate research and Monte Carlo simulations that account for sequence of returns risk. It is not a bank interest rate. It is a conservative withdrawal rate set low because you cannot know your future return sequence before you start drawing income.

What are the two economic powers?

The two economic powers are the investment power and the distribution power. The investment power, driven by rate of return, is strong at accumulation. The distribution power, driven by the law of large numbers and actuarial pooling inside insurance products, is strong at turning a lump sum into guaranteed lifetime income. An efficient plan uses both.

What is a volatility buffer?

A volatility buffer is a pool of uncorrelated, accessible money, such as whole life cash value or a cash reserve, that you spend from during down-market years so you do not sell investments at a loss. Three to six years of spending is the practical range. It directly reduces sequence of returns risk in the first years of retirement.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only deploy capital from it when the use produces a return greater than the cost, so your dollars do two jobs at once: the policy keeps compounding net of internal charges while the capital does work elsewhere.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy capital when the return clears the cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is whole life or IUL better for retirement income?

Whole life is the simpler platform: guaranteed premiums, guaranteed cash value growth, and non-guaranteed dividends on top, with no risk the policy collapses if dividends fall. Indexed universal life chases higher returns but shifts mortality-charge and interest-rate risk to the policyholder, so it requires in-force illustrations and ongoing monitoring. Neither is universally better; it depends on the job.

Should all my retirement money be tax-free?

Concentrating everything in a single tax treatment is a bet on unknown future tax brackets and your own future income. Tax diversification across taxable, tax-deferred, and tax-free buckets gives you control over your bracket each year. Tax strategy should refine an efficient plan, not drive the whole plan.

How much of a volatility buffer should I hold?

Three years is a practical minimum and six years is a practical maximum for most plans. Below three you stay exposed to early-retirement sequence risk; above six or seven the incremental protection shrinks while the opportunity cost of holding the buffer grows.

Is a 401(k) a retirement income plan?

No. A 401(k) is a regulated investment plan with real advantages, including employer matches and tax deferral, but it is built for accumulation. It does not produce guaranteed income on its own. You have to build the income plan yourself, which is the job most people never realize transferred to them when pensions faded.

- Wade Pfau, retirement income research, academic work on sequence of returns risk and combining investments with insurance for sustainable income.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- LIMRA, annuity, retirement income, and persistency data.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

A Retirement Income Certified Professional who built a planning system focused on one question: will your retirement income last. He ran the live 26-year market demonstration in the source video.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on how the two powers and a whole life buffer fit your retirement, book a discovery call. We will tell you if they do not.