.png)

The reverse mortgage tax strategy converts idle home equity into usable capital with no required monthly payment, then times voluntary interest payments to capture a deduction when the debt qualifies. The drawn dollars are loan proceeds, so they are not taxable income, but deductibility depends on current law and how the funds were used.

For most American households over 60, the largest single position on the balance sheet is the house, and it is the one asset they cannot spend. Equity sits in the walls. It pays no income, it cannot be partially sold to fund a year of long-term care, and it disappears in a down market at exactly the moment heirs are forced to sell it. A paid-off home feels like safety. Structurally, it is concentration risk dressed up as peace of mind.

Concentrating your net worth in home equity is the same mistake as putting your entire portfolio into one stock, and almost nobody treats it that way. A reverse mortgage is one tool for unlocking that capital without selling the house or losing ownership. Used carelessly, it is the expensive, last-resort product the television ads have made it look like. Used with discipline, it can lower the cost of a retirement and leave heirs more than the home itself would.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we do not sell reverse mortgages. We do build the life insurance side of the plan that often pairs with one. This breakdown comes from a conversation between our founder, Caleb Guilliams, and reverse mortgage specialist Harlan Accola. It covers how the strategy works, how the tax piece actually functions once you strip out the hype, the real costs, and where it fits inside The And Asset framework. We will also name who should not do it.

- A reverse mortgage turns idle home equity into usable capital without a required monthly payment or loss of ownership.

- An FHA-insured HECM is non-recourse: you and your heirs never owe more than the home is worth at sale.

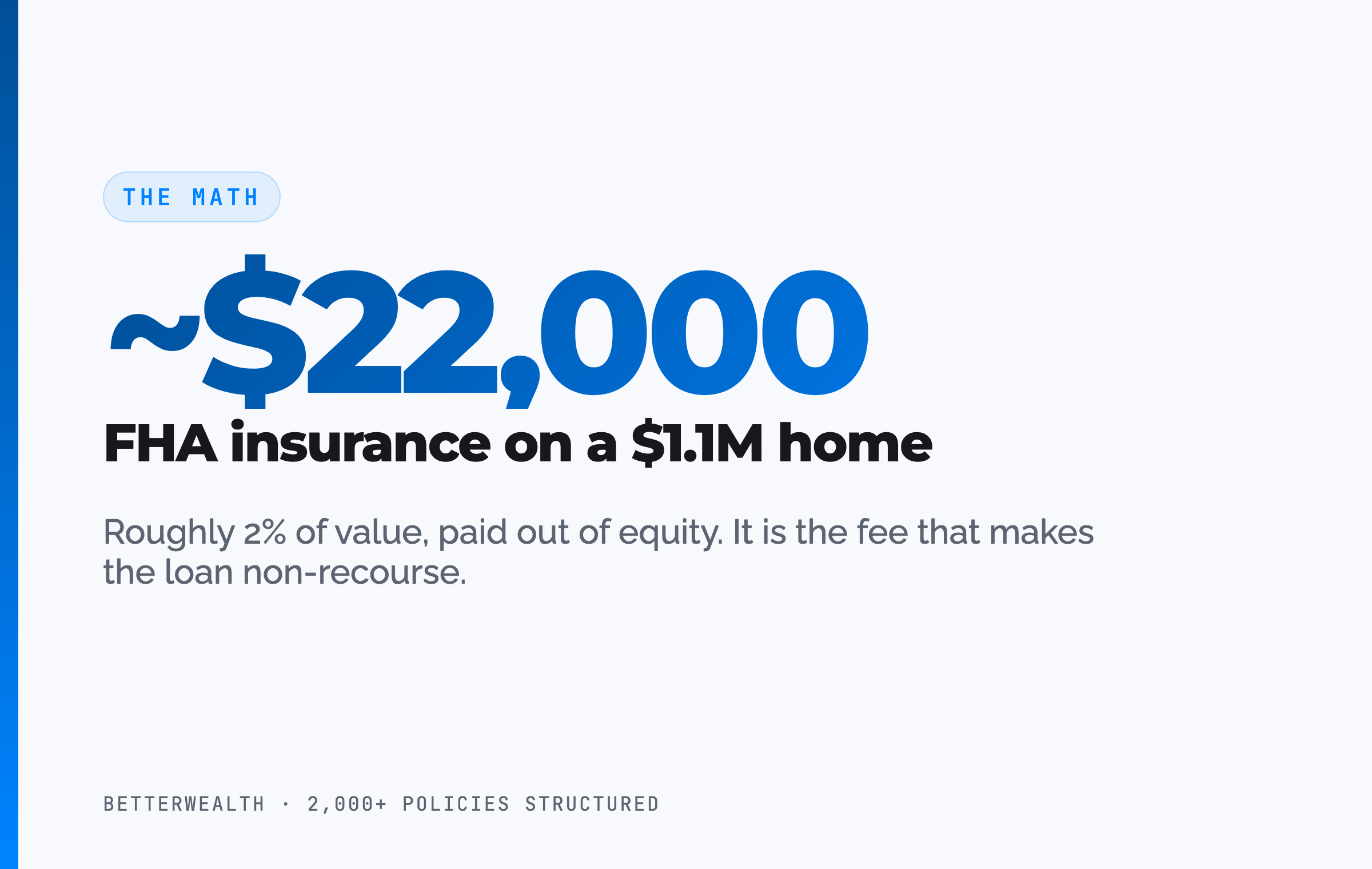

- The cost is real. An FHA insurance fee near 2% of value plus closing costs comes out of your equity, not your pocket.

- Interest is deductible only when actually paid, only as home acquisition debt, and only if you itemize.

- The And Asset rule still governs: only deploy freed capital into a use that beats the loan's full cost.

- Freed equity can fund life insurance, creating a fixed legacy independent of the housing market.

Harlan runs live software on screen with real client numbers, including the year-by-year equity and line-of-credit projections that are hard to picture in prose. Watch the full conversation:

01 / The problemWhy is a paid-off house an inefficient asset?

A paid-off house is inefficient because it locks a large share of your net worth into an illiquid asset you cannot spend, partially sell, or redeploy when a better use of capital appears. Equity in a home produces no income on its own. Harlan describes trying to pay for gas with a million-dollar house and getting waved off by the clerk. The point lands: equity is not money until you convert it.

The fear runs the other way. People worry that a reverse mortgage means losing the house. The structural truth is that you carry more risk of losing a home with a forward mortgage, because a forward mortgage demands a payment every month and a missed run of payments triggers foreclosure. A reverse mortgage carries no required payment at all.

"It is not stupid to pay off your house. It is just incredibly inefficient.", Harlan Accola

02 / How it worksHow does a reverse mortgage actually work?

A reverse mortgage lets a homeowner aged 62 or older borrow against home equity with repayment deferred until the home is sold or the last borrower passes away. You keep title and ownership. The most common version is the Home Equity Conversion Mortgage, insured by the Federal Housing Administration. That FHA insurance is what makes the rest of the strategy possible.

Here is the sequence we see when the tool is used well.

- Establish the line of credit. Qualify for a HECM and set up a line of credit against your equity. You can take a lump sum, a monthly check, a growing line you leave untouched, or a mix.

- Eliminate the required payment. Use the loan to pay off any existing forward mortgage. The mandatory monthly payment disappears, which frees cash flow on a fixed income.

- Let the unused line grow. An untouched HECM line of credit grows over time at the current rate, so the capital available at 86 can be far larger than the equity available today.

- Deploy with discipline. Draw and deploy only when the freed capital can do something productive. This is where The And Asset rule applies, and it is the step most marketers skip.

- Model the tax piece with a CPA. Payments are optional, and a voluntary interest payment can produce a deduction in the years it qualifies. Run it with a tax professional before relying on it.

Repayment is not forgiven, it is deferred. At the end, you or your heirs repay what was borrowed plus accrued interest, almost always from the sale of the home, and keep whatever equity remains. Because most homes appreciate over time, the remaining equity can stay flat or even grow for years despite a rising loan balance.

Marketers have made this product look slimy, the same way they oversold infinite banking. The mechanics are not the problem. The pitch is.

03 / The costWhat does a reverse mortgage really cost?

A reverse mortgage is not too good to be true, it is too good to be free, and the cost is real. The largest piece is the FHA insurance fee, roughly 2% of the home's value. On a $1.1 million home that is about $22,000. There is also an origination fee and standard closing costs: appraisal, title, and the rest. You do not write a check for these. They come out of your equity.

That insurance fee is not a junk charge. It is what guarantees the loan is non-recourse, meaning you can never be forced to repay more than the home is worth at sale, no matter how long you live or how far the housing market falls. Some advisors call it a put fee, because you are effectively buying a guaranteed floor under your home's future value. The cost is the price of that guarantee.

The cost is also why timing matters. Paying $22,000 to set up a loan you exit two years later makes no sense. The expense only amortizes over a long horizon, the same way an overfunded life insurance policy only makes sense if you intend to keep it.

Too good to be free, not too good to be true.

This strategy fits a specific person doing specific things.

It fits you if

- You are 62 or older with meaningful home equity

- You plan to stay in the home, or buy your next one, for years

- You can name a productive use for freed capital

- You care about an efficient retirement and a planned legacy

It does not fit you if

- You lack meaningful equity to draw on

- You expect to sell or move within a few years

- You would spend the capital with no plan behind it

- You want certainty above all and will not keep the loan

The reverse mortgage itself is handled by a licensed mortgage professional. The capital and legacy strategy around it, especially the life insurance piece, is the conversation we have. We will tell you honestly whether it fits.

Book a Discovery Call04 / The frameworkWhere The And Asset comes in: capital is an AND, not an OR

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base you borrow against, while the policy keeps compounding net of internal charges. The reverse mortgage connects to it through one shared idea: your dollars should do more than one job, and you should never lock all of them into a single asset.

Asked whether a retiree should get a reverse mortgage or buy an annuity, Harlan answers with one word: "and." Use the house, and the annuity, and cash value life insurance. The mistake is treating capital as a series of either-or choices. Every dollar buried in a paid-off home is a dollar that cannot work anywhere else.

Where IBC ends and The And Asset begins

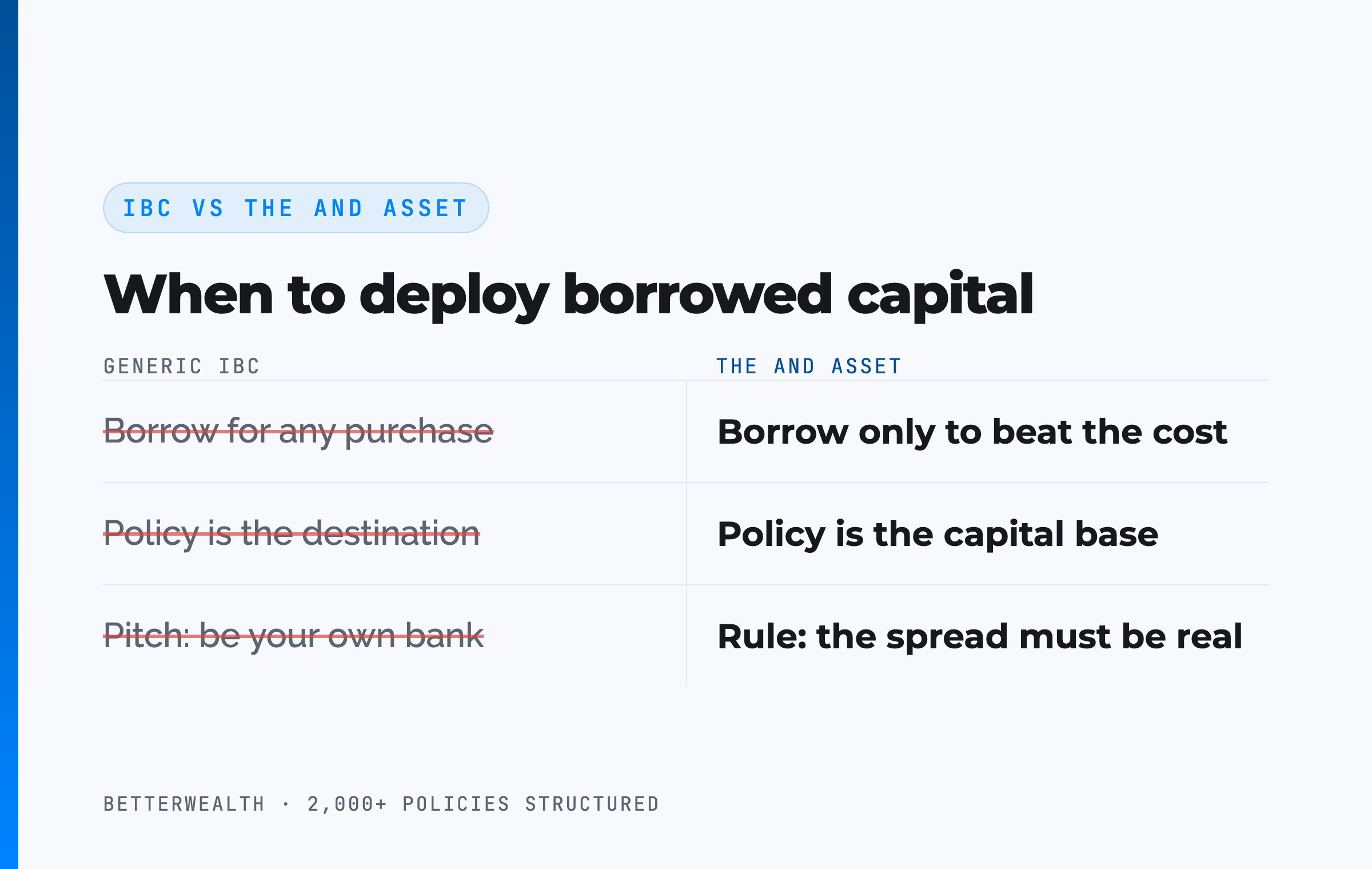

Infinite banking, as Nelson Nash taught it in Becoming Your Own Banker, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a rule Nash's broader teaching does not enforce: you only deploy borrowed capital when the return clears the borrowing cost. We credit Nash's foundation. We operate on different principles.

That same discipline is the honest test for a reverse mortgage. A HECM line of credit you draw and then spend on consumption is just an expensive way to spend money. A line you draw to fund an activity that out-earns the loan's full cost, including interest and the insurance fee, is capital doing two jobs. The house keeps appreciating while the borrowed dollars work elsewhere. That is the AND.

The math has to work. Every time.

A line of credit you never deploy productively is not a strategy. It is an option you paid for and never exercised. Borrow only when the return beats the cost.

05 / The tax pieceHow does the reverse mortgage tax deduction actually work?

The drawn proceeds from a reverse mortgage are not taxable income, because they are borrowed money, not a sale or a withdrawal. That part is simple and it is the foundation of the strategy. You can convert equity to cash without triggering capital gains or ordinary income.

The deduction piece is where the hype outruns the rules, so here is the precise version. Reverse mortgage interest is generally deductible only when it is actually paid, not as it accrues. It is deductible only to the extent the loan is home acquisition indebtedness, meaning funds used to buy, build, or substantially improve the home. It is deductible only if you itemize. A line of credit drawn for other purposes is not acquisition debt, and its interest is not deductible.

Inside those limits, the timing strategy is real. Because payments are optional, a borrower can make a large voluntary payment in a high-income year, apply it to interest first, and capture a deduction shown on a Form 1098, then re-borrow the same amount later as tax-free loan proceeds. Harlan also points to a 2026 tax change he says restored the deductibility of mortgage insurance premiums, which would expand what qualifies. Treat that as a claim to verify, not a settled fact. Tax law shifts, and the deductibility of any specific payment depends on your facts.

This is exactly the kind of strategy that should be modeled by a CPA against your actual return, not run off a YouTube clip. When the arbitrage works, it works because you are borrowing at a modest rate while deploying into something that earns more, and the deduction sweetens an already-positive spread. When it does not work, you have borrowed money to chase a deduction you could not actually use.

"Zero tax because it's borrowed money" is true for the loan proceeds. It is not a blanket promise. The deduction has rules, and the spread has to be real before the tax benefit means anything.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to decide when borrowing against an asset actually pays, the same discipline this strategy depends on. Free, email-gated, no spam.

Open the Vault06 / SafetyIs a reverse mortgage actually safe, or is that a sales line?

A HECM is safer than its reputation on the dimensions that scare people most, and it is not free of tradeoffs, so both halves of that sentence matter. The FHA insurance makes it non-recourse. You cannot be forced out for owing more than the home is worth, and your heirs never inherit the shortfall. If you outlive the loan math and the balance passes the home's value, the FHA insurance, not your family, covers the gap.

Harlan tells the story of a 94-year-old still receiving monthly checks on a home she is technically underwater on. That is the design working as intended, not a loophole. She outlived the actuarial assumptions, and the insurance she paid for absorbs the difference.

The tradeoffs are equally real, and an honest practitioner names them. You give up equity through interest and the insurance fee. Your heirs inherit less of the home. You must keep up with property taxes, homeowner's insurance, and maintenance to stay in good standing, just as with any mortgage. Calling it "no risk" is the kind of overselling that earns the whole product its bad name. The accurate statement is narrower and stronger: the downside most people fear, being forced out or saddling heirs with debt, is the specific risk this structure is built to remove.

What about Medicaid and long-term care planning?

Reverse mortgages do come up in long-term care and Medicaid planning, because the freed capital can fund care or insurance and because of how home equity is sometimes treated. The rules here are complex and state-specific, and they change. There is no single move that solves a Medicaid eligibility question, and the lookback and asset-treatment rules vary by state. Anyone planning around Medicaid should work with an elder-law attorney rather than rely on a general rule. The defensible version is simpler: having accessible capital, instead of equity frozen in a wall, gives a family more options when care becomes the issue.

07 / The legacyWhy life insurance is the natural partner

Life insurance is the natural partner to a reverse mortgage because it solves the exact objection the strategy creates: "I want to leave my house to my kids." Most heirs do not move into the house. They sell it, often at a bad price, while they are grieving and checked out. Leaving them the home frequently means leaving them the burden of liquidating it.

A death benefit is cleaner. It is a fixed dollar amount, paid in cash, independent of what the housing market is doing in the year you die. Caleb's own framing makes the point: his house might be worth $1.6 million, but the value on the day his heirs need it is unknowable, while a $3 million life insurance policy pays $3 million regardless of the market. You cannot time your death to optimize a home sale. You can fix a legacy in advance with a policy.

Put the two together and the AND becomes concrete. Free idle equity with a reverse mortgage, redirect a portion of that freed capital into a permanent policy, and you have improved cash flow today and a larger, more predictable inheritance later. For a healthy person who can qualify for coverage and whose main goal is legacy, routing equity through life insurance typically beats leaving it in the house. The numbers should be run for the specific case, not assumed.

The ultimate gift card is not a house your kids have to sell during the worst week of their lives. It is a death benefit that arrives in cash, on a number you chose.

The North Carolina widow with $300,000 and a $1.1 million house

A widow in North Carolina lost her husband and was left with about $300,000 in savings, no life insurance, and a $1.1 million home carrying a $200,000 mortgage. Her income was roughly $2,500 a month. Her mortgage payment was $2,000 of it. The numbers below are her actual figures, shared anonymously.

Staying put, the reverse mortgage paid off her $200,000 mortgage and left a loan balance near $232,000 after first-year interest and costs. That single move erased the $2,000 monthly payment. Without it, ten years of payments would have run about $240,000, money she did not have, which means she would have drained her entire $300,000 just to keep the house.

She is instead leaning toward a 55-plus community. Selling the $1.1 million home and paying roughly $77,000 in real estate and moving costs leaves about $823,000. On a $600,000 next home, rather than paying all cash, she puts $386,000 down and the reverse mortgage covers the remaining $213,000, with no required payment for life. That keeps $436,000 liquid. Added to her existing $300,000, her advisor now manages close to $700,000 instead of $300,000, and she carries no housing payment.

If she passes in her mid-80s owing around $718,000 on a home appreciating near 4% a year, her heirs still net roughly $400,000 after 16 years of no payments. The tradeoff is plain: the kids inherit less of the house, and she lived a far more liquid, lower-stress retirement. That is the trade, stated honestly.

Equity, or actual cash. Pick the one you can use.

08 / Head to headReverse mortgage against the alternatives

Against the other ways a 62-plus homeowner can access home equity, a reverse mortgage trades upfront cost and a slower setup for the removal of a required payment and the removal of recourse. The table sets it beside keeping a forward mortgage, selling the home, and a HELOC on the dimensions that decide a retirement.

| Dimension | Reverse Mortgage (HECM) | Forward Mortgage | Sell the Home | HELOC |

|---|---|---|---|---|

| Required payment | None; payments optional until sale or death | Mandatory monthly (e.g. $2,000/mo) | None, but you no longer own the home | Mandatory once drawn |

| Taxable event | No; proceeds are loan dollars, not income | No; but no equity is freed | Possible capital gains above the exclusion | No; proceeds are loan dollars |

| Downside protection | Non-recourse; never owe more than sale value | Full recourse; missed payments risk foreclosure | You absorb whatever the market gives that year | Can be frozen or reduced by the lender |

| Cost to set up | ~2% FHA insurance plus closing costs (~$22K on $1.1M) | Standard closing costs | ~7% in agent and moving costs ($77K on $1.1M) | Low or no upfront cost |

Required payment. The reverse mortgage is the only option here that removes the monthly payment entirely while keeping you in the home. For the widow in the case study, that single feature freed $2,000 a month on a $2,500 income.

Downside protection. A HELOC is cheaper to open, but a lender can freeze or cut it exactly when you need it, as many borrowers learned in past downturns. A reverse mortgage line cannot be called, and the FHA insurance caps what you ever owe at the home's sale value.

Cost. The HECM's upfront fee is its real drawback, near $22,000 on a $1.1 million home. Selling outright often costs more in agent and moving fees, around $77,000 on the same home, and ends your ownership. The right answer depends on your horizon, not the sticker price alone.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your situation and tells you whether freeing equity and funding life insurance belongs in your plan, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQReverse mortgage tax strategy questions

What is a reverse mortgage tax strategy?

A reverse mortgage tax strategy uses an FHA-insured Home Equity Conversion Mortgage to convert idle home equity into usable capital without a required monthly payment, then manages the timing of voluntary interest payments to capture a tax deduction when the debt qualifies as home acquisition indebtedness and you itemize. The proceeds you draw are loan dollars, so they are not taxable income. Deductibility depends on how the funds were used and current tax law, so model it with a CPA.

Is a reverse mortgage safe?

A Home Equity Conversion Mortgage is FHA-insured and non-recourse, so you cannot be forced out for owing more than the home is worth, and your heirs never owe the shortfall. It is not free of tradeoffs. You give up equity through interest and an insurance fee, your heirs inherit less of the home, and you must keep up with taxes, insurance, and maintenance to stay in good standing.

Do you have to pay back a reverse mortgage?

Repayment of a reverse mortgage is deferred until the last borrower sells the home, moves out permanently, or passes away. Monthly payments are optional. At payoff, you or your heirs repay the amount borrowed plus accrued interest, usually from the sale of the home, and keep any remaining equity.

Can reverse mortgage interest be tax deductible?

Reverse mortgage interest is generally deductible only when it is actually paid, only to the extent the loan is home acquisition indebtedness used to buy, build, or substantially improve the home, and only if you itemize. A line of credit used for other purposes is not acquisition debt, so its interest is not deductible. Confirm your specific situation with a tax professional.

Will a reverse mortgage leave my kids with debt?

No. A Home Equity Conversion Mortgage is non-recourse, so your heirs never owe more than the home's value at sale. They can sell the home to repay the loan and keep any remaining equity, or buy out the loan if they want to keep the house. The tradeoff is that they inherit less of the home than if it were unencumbered.

What does a reverse mortgage cost?

A reverse mortgage carries an FHA insurance fee of roughly 2% of the home's value, plus an origination fee and standard closing costs like appraisal and title. On a $1.1 million home, the upfront FHA insurance alone runs about $22,000, paid out of equity rather than out of pocket. Costs make a short holding period a poor fit.

Should I pay off my house before retirement?

Paying off a house is not reckless, but it can be inefficient because it locks a large share of net worth into a single illiquid asset you cannot spend. Concentrating capital in home equity is the same mistake as putting your whole portfolio in one stock. The question is whether that equity could do more working elsewhere, net of borrowing costs.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the borrowing cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

How does life insurance pair with a reverse mortgage?

A reverse mortgage frees equity that would otherwise sit idle in the home, and a portion of that freed capital can fund a permanent life insurance policy. The result is a death benefit that is fixed and independent of the housing market, which can leave heirs a larger and more predictable legacy than the home itself would. The math should be run for your specific case.

Who is a reverse mortgage not right for?

A reverse mortgage is the wrong tool for someone who lacks meaningful equity, who plans to sell or move within a few years, or who would draw the capital and spend it on consumption with no productive use. The upfront cost only makes sense over a long horizon, and the freed capital should be deployed with discipline.

At what age can you get a reverse mortgage?

The minimum age for an FHA-insured Home Equity Conversion Mortgage is 62. Establishing a line of credit earlier rather than waiting tends to produce more available capital later, because the unused line grows over time. Waiting until funds run out is the least efficient way to use the tool.

- HUD / FHA Home Equity Conversion Mortgage program, the rules behind the insured, non-recourse reverse mortgage.

- Consumer Financial Protection Bureau, borrower protections, costs, and counseling requirements.

- IRS Publication 936, home mortgage interest deduction, acquisition indebtedness, and when interest is deductible.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Has worked in reverse mortgages for 20 years and built the planning software used to model the client scenarios in the source video. Reverse mortgages are handled by his licensed team, not by BetterWealth. movement.com/reverse →

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether freeing equity and funding a policy fits your plan, book a discovery call. We will tell you if it does not.