.png)

IUL and whole life are both permanent insurance, but they behave differently as a capital base. IUL credits a variable rate tied to an index, capped and subject to change. Whole life credits a contractual rate plus non-guaranteed dividends. For a disciplined infinite banking strategy, whole life's predictability is why The And Asset uses it.

A public challenge ran for years with a simple promise: show an index universal life policy at least 10 years old, out of its surrender period, whose in-force performance matched or exceeded the illustration it was sold on, and collect a cash prize. The premise was that no one could do it, that IUL by its nature cannot keep the promises it is sold on. Then an advisor produced exactly such a policy, and the submission was rejected on a clause buried in the terms.

The episode is not really about who wins a contest. It is about the difference between whether a product can function and whether it was the right product to begin with. Those two questions get blended together constantly in the life insurance debate, and blending them is how buyers end up with a policy that technically works but was never suited to what they wanted.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the carrier and product choice is downstream of one thing: what are you trying to do with the capital? This piece walks through what the challenge actually proved, why IUL gets missold for accumulation, the honest case for whole life as the capital base, and where the variable products belong. The guest who submitted that policy, advisor Jonathan Bell, is a self-described insurance purist who builds death-benefit-first, and his discipline frames the whole conversation.

- An IUL can outperform its original illustration, especially one that was illustrated conservatively rather than at the maximum allowed rate.

- Product function (can it perform) and product suitability (was it right for the buyer) are separate questions that get blurred constantly.

- IUL is most often missold for overfunded accumulation, illustrated at aggressive crediting and 100% loan assumptions projected in a straight line.

- Whole life trades higher premium for contractual certainty, which is why The And Asset uses it as the capital base you borrow against.

- Insurance is not an investment, except registered VUL and private placement, which carry real market risk of loss.

- Whatever the product, run it 100 to 150 basis points below the max rate and model zero-return years before you trust it.

Watching the full conversation gives you the back-and-forth on how the policy was designed and why it still got disqualified, detail no summary fully captures:

01 / The challengeWhat did the IUL challenge actually prove?

The challenge proved that an IUL can outperform its own illustration, which is a narrower and more important point than it sounds. The stated criteria were short: a full original illustration, a current in-force illustration, a policy at least 10 years old and out of surrender, and the in-force numbers matching or exceeding the original. An advisor confirmed those criteria in writing, then submitted a policy that met them. The policy had credited a higher rate than originally modeled and held more cash value 12 years in than the day it was sold.

The submission was rejected. The reason was a clause in the published terms and conditions requiring the policy to have been illustrated at the maximum index crediting rate available at issue. This policy was illustrated conservatively, well below the ceiling, and it was sold before 2015, when carriers could legally illustrate at rates that rarely came true.

"If you are going to say that a product in force for 10 years or greater simply cannot perform greater than as sold, you are not attacking the sale. You are attacking the ability for the product to function.", Jonathan Bell

02 / The real distinctionFunction versus suitability, and why it matters

Function and suitability are two different questions, and almost every argument about life insurance products collapses them into one. Function asks whether a product can do what it is built to do across different rate environments. Suitability asks whether that product was the right tool for a particular person's goal.

On suitability, the advisor who beat the challenge largely agreed with the challenger: IUL is overused and oversold for accumulation. On function, he disagreed, because the policy plainly performed. Both things are true at once. A protection-designed IUL can credit well and beat its illustration while still being the wrong product for someone who was sold it as a tax-free income machine.

The policy in question was a clean example. It was a 1035 exchange with no further funding, built to maximize death benefit for an estate, not to accumulate cash value. A client had bought whole life in his 30s, no longer needed the cash value for retirement income in his later years, and wanted as much guaranteed death benefit as possible. The IUL fit that goal. It would have been a poor fit for an aggressive accumulation pitch, which is the use the challenge was really built to attack.

Right product, right job. That is the whole game.

Imagine arguing that a whole life sold in 1983 at an 18% dividend assumption proves whole life is broken because it cannot beat that today. That is a reflection of the rate environment, not the product. The same logic applies to a pre-2015 IUL.

03 / The missellingWhy is IUL so often sold the wrong way?

IUL is missold because it lends itself to an attractive story that the math does not always support. The product has a cool narrative: upside tied to an index, a floor that protects against negative years, the ability to show arbitrage between a low loan rate and a higher crediting rate. Put those together in an illustration and you can make it look like an investment with upside and no downside.

The trouble is in how those illustrations get built. Too often they assume the most aggressive crediting rate, the most favorable loan assumptions, and they project that paper arbitrage in a straight line for 30 or 40 years. Crediting is not linear. Caps move, participation rates move, cost of insurance moves. A policy shown at a flat maximum rate every year for decades is a marketing artifact, not a forecast.

What disciplined modeling looks like

The honest version stress tests the policy. You run the illustration 100 to 150 basis points below the maximum rate. You drop in 0% crediting years every five, seven, or ten years to see how the contract holds up when the index does nothing. For distributions, you show withdrawals to basis first and loans only when you actually need them, rather than 100% participating loans forever. This is less exciting on a sales call. It is far more honest about what the buyer will live through.

Aggressive illustrations sell. They also set people up to fail.

"There are horrific practices in the selling of permanent life insurance and IUL specifically today. It makes me ashamed in many respects to be in the same business as some of these people.", Jonathan Bell

04 / The frameworkWhere does The And Asset fit, and why whole life?

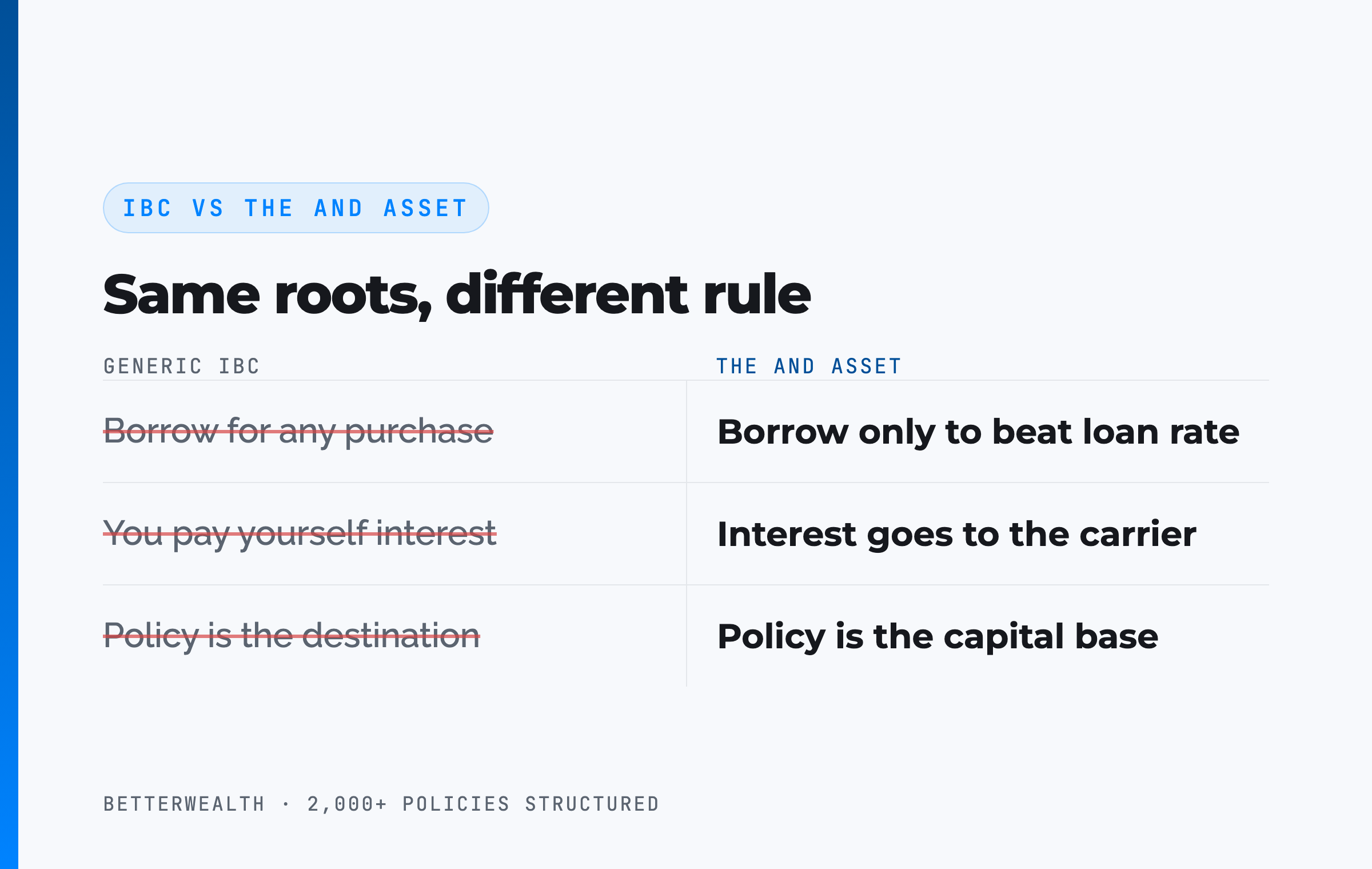

The And Asset uses whole life as the capital base because the strategy depends on a predictable asset you can borrow against with confidence. The And Asset is BetterWealth's framework, built on Nelson Nash's foundation. Nash pioneered using whole life as a personal banking system in Becoming Your Own Banker, and his insight holds: you either lose money paying interest to outside lenders or lose it to the opportunity cost of idle capital. We respect that foundation. The And Asset adds one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The IUL debate sharpens why the chassis matters. If the cash value you borrow against can be reduced by a cap change or a flat index year, the foundation of the whole strategy is moving under you. Whole life's contractual guarantees and uninterrupted compounding, net of mortality and expense charges, give you a base that does not shift while a loan is outstanding.

Many IUL marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what your deployed capital earns elsewhere while the policy keeps compounding. That correction matters more on a variable product, where the temptation to assume a permanent positive loan spread is built into the sales illustration.

The And Asset is not IUL with discipline and it is not generic infinite banking. It is whole life used as a capital base, where the dollars only move when the deployed return beats the loan rate.

The And Asset fits a specific person doing specific things.

It fits you if

- You are an entrepreneur or investor who deploys capital

- You want a predictable base you can borrow against

- You can name a use for capital that beats the loan cost

- You have a long horizon and value certainty over hype

It does not fit you if

- You want a market investment inside a policy

- You are chasing the highest illustrated number

- You have no plan to deploy borrowed capital

- You need a savings account, not a capital strategy

If you are in the first column, a 30-minute conversation will tell you whether a whole life And Asset policy fits your design. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The mathDoes the deployed return clear the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow. This is the test, and it does not change whether the chassis is whole life or anything else. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify, not a constant.

Here is why the chassis still matters to the math. With whole life, the cash value compounds on its full value while you borrow, on a contractual basis you can count on. With an IUL, the amount your borrowed-against cash value credits depends on the index that year, the cap, and the participation rate. A strategy that assumes a positive spread between a fixed loan cost and a variable crediting rate is assuming away the exact risk that makes the product variable. If the deployed activity clears the loan cost on its own, you do not need to lean on that spread at all.

If the deal does not clear the loan rate, do not borrow.

06 / The case for whole lifeWhen is whole life the better chassis?

Whole life is the better chassis when you want safety, stability, and the fewest moving parts in the asset you borrow against. The dividend, the guaranteed cash value, and the death benefit move slowly and predictably, not subject to changing caps, participation rates, spreads, or cost-of-insurance adjustments. You give something up for that: the required premium to fund a given death benefit is higher than on a universal life chassis. That premium buys certainty.

For a capital strategy, certainty is the point. You are not trying to win a side-by-side contest for the biggest number 40 years out. You are trying to know, within a tight range, what your capital base will be worth when an opportunity shows up and you need to borrow against it. A policy whose value can be marked down by a flat index year is a weaker foundation for that, even if it might post a higher number in a strong decade.

Whole life is the more expensive way to lock in a death benefit. It is also the more certain way to hold a capital base you intend to borrow against. You are paying for predictability, on purpose.

07 / The variable productsWhere do IUL and VUL actually belong?

IUL and VUL belong with buyers whose objective and time horizon match the product's structure, starting from a real death benefit need. A guaranteed IUL with an extended no-lapse rider can deliver a permanent death benefit at a lower premium than whole life, which suits the premium-sensitive buyer who wants maximum death benefit per dollar and accepts performance risk. That is a death-benefit play, not an accumulation play.

VUL is the honest investment of the three, because it is a registered security with sub-accounts and direct market risk, including the risk of loss. For a young buyer with a 30- or 40-year horizon and real risk tolerance, an accumulation-focused VUL can be allocated to equities inside the contract, with the tax treatment of life insurance wrapped around it. The cost is volatility and the genuine possibility of underperformance. In a long flat or down market, a whole life policy would have produced the better net outcome.

The one thing every chassis shares

Buy life insurance as life insurance first. Start with the death benefit you need, then decide how to fund it. The designs that get people into trouble almost always start from the cash value or the income illustration and back into a tiny death benefit, which is exactly backwards. Insurance is not an investment, except for the registered variable products, and pretending otherwise is how the industry earns its worst reputation.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to compare whole life, IUL, and VUL for a real capital strategy. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsBenefits and the honest tradeoffs of each chassis

Every chassis carries a real tradeoff, and any advisor who hides it should lose your trust. Whole life gives you guarantees and predictability, but a higher premium and slower headline growth. IUL gives you a lower premium for a death benefit and some upside, but variable crediting and ongoing exposure to caps and cost-of-insurance changes. VUL gives you genuine market exposure and the highest potential long-term death benefit IRR, but direct risk of loss and the need for active monitoring.

There is also a carrier-risk wrinkle worth naming. VUL sub-accounts are held in segregated accounts, which insulates them from the insurer's general account. IUL and other general-account universal life products are not segregated, so if a carrier mismanages risk and comes under strain, general-account policyholders are more exposed. Whole life is also a general-account product, which is part of why working with highly rated, conservatively run mutual carriers matters.

No chassis is free. Pick the tradeoff that fits the job.

09 / The lessonWhat every buyer should take from this

The clearest lesson is that language and assumptions decide outcomes, so make both explicit before you sign. The challenge fell apart over a clause about maximum illustrated rates. Most policies fall apart over the same kind of ambiguity: an income number shown at an aggressive rate, a loan spread assumed to be permanent, a death benefit minimized to inflate cash value.

You guard against all of it the same way. Demand the conservative version of the illustration. Ask what the policy does in a 0% year. Ask whether the income is shown as loans or withdrawals. Treat the policy like a portfolio you review every year, not a plan you set once and forget. The product that survives that scrutiny is the one worth owning, whatever the label on it.

10 / Head to headWhole life, IUL, VUL, and GUL compared

Across the four permanent chassis, whole life trades cost for certainty, the universal life products trade certainty for lower premium or upside, and your objective decides which tradeoff is right. The table sets them against each other on the dimensions that matter for a capital strategy.

| Dimension | Whole Life | IUL | VUL | Guaranteed UL |

|---|---|---|---|---|

| Cash value growth | Contractual rate plus non-guaranteed dividends, net of internal costs | Index-linked with a cap and a floor; varies year to year | Sub-account market returns; real risk of loss | Minimal to none; built for death benefit |

| Premium for the same death benefit | Highest of the four | Lower than whole life | Lower than whole life, varies with performance | Often the lowest for a guaranteed death benefit |

| Predictability | High; few moving parts | Moderate; caps, participation, COI can change | Low; tied to markets | High on death benefit, no cash value upside |

| Best fit | Capital base for The And Asset; safety and stability | Lower-cost permanent death benefit with some upside | Long-horizon accumulation with market risk tolerance | Lowest-cost guaranteed death benefit, estate transfer |

Growth and predictability. Whole life's value moves slowly and on contract, which is what makes it a stable base to borrow against. IUL can outperform in a strong decade, but its variability is exactly what a capital strategy does not want under it.

Premium. For the same guaranteed death benefit, a guaranteed IUL can run several percentage points of premium cheaper than whole life. That savings is real, and it is the reason most brokerage carriers have dropped standalone GUL in favor of cash-value designs with future flexibility.

Fit. The right chassis is the one whose tradeoff matches your objective. For an entrepreneur building a capital base to deploy and repay, that is whole life. For a young accumulator with risk tolerance, VUL can fit. For a premium-sensitive estate need, a guaranteed IUL or GUL can win.

A composite: the business owner who borrowed against a whole life base

Consider a 41-year-old business owner, preferred non-tobacco, funding a whole life And Asset policy at $50,000 per year on a cashflow design, structured with a heavy paid-up additions rider at roughly a 40/60 base-to-PUA split. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is fiction, whatever the chassis.

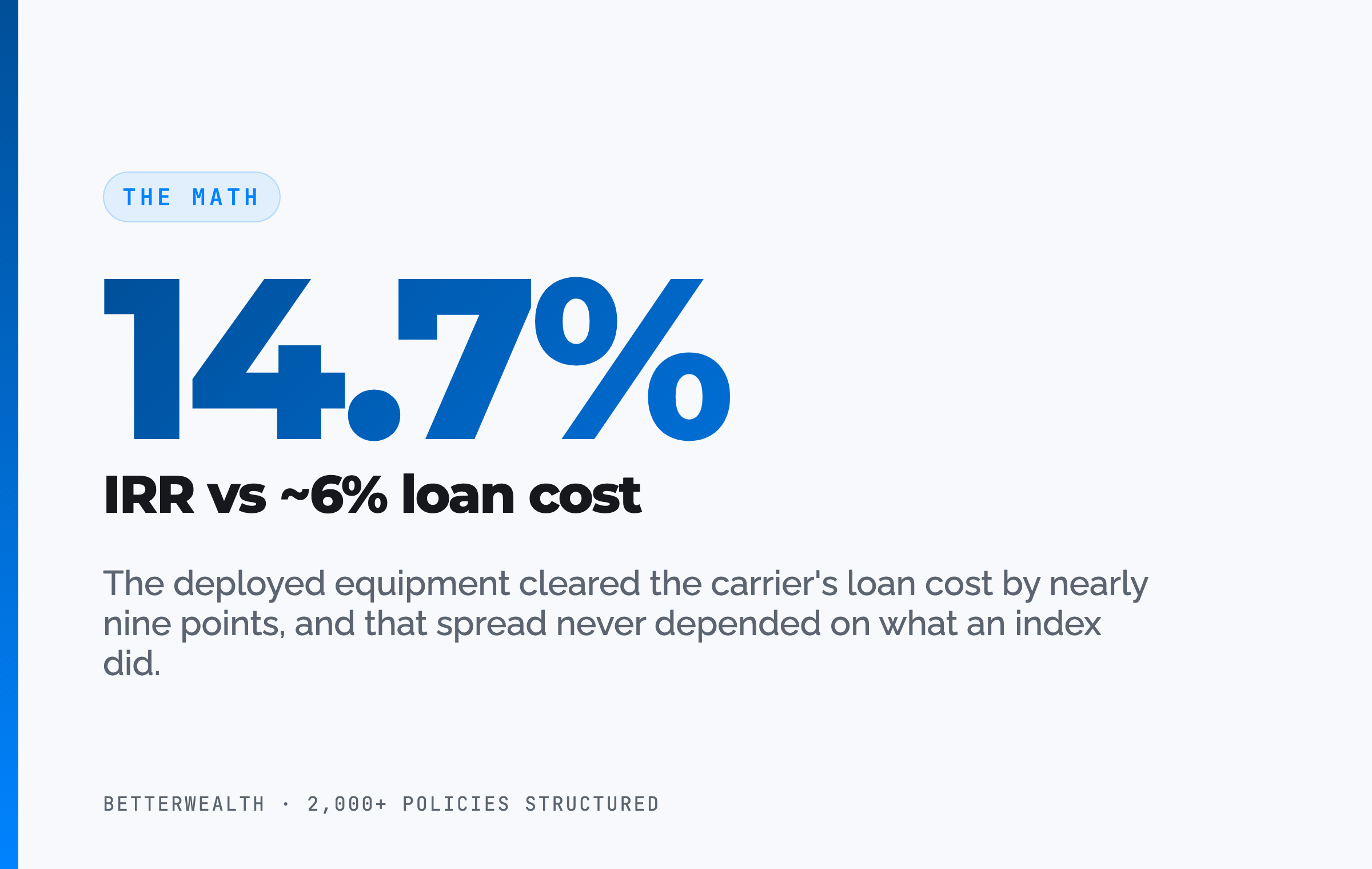

In year seven, with roughly $361,000 of accessible cash value, the owner borrows $187,500 against the policy to buy revenue-producing equipment. The equipment returns an estimated 14.7% IRR. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by nearly nine points, and that spread does not depend on what an index did that year. The policy keeps compounding on its full value the entire time. Repayment runs on a 41-month schedule funded by the equipment's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about which chassis fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen this work and seen it fail. On a discovery call, a practitioner looks at your situation and tells you whether a whole life And Asset policy, a different product, or no policy at all belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQIUL vs whole life questions

Can an IUL outperform its original illustration?

Yes. An index universal life policy can credit more than its originally illustrated rate and hold more cash value years later, especially when it was illustrated conservatively at issue. A policy outperforming its illustration is a question of product function, which is separate from whether IUL was the right product for that buyer.

What is the LIFE180 IUL challenge?

It is a public challenge to produce an index universal life policy at least 10 years in force, out of its surrender period, whose in-force illustration matches or exceeds the original as-sold illustration. The stated criteria are simple, but the written terms also require the policy to have been illustrated at the maximum index crediting rate available at issue, which disqualifies most conservatively illustrated policies.

Is IUL good for infinite banking?

IUL is generally not the chassis we use for a disciplined infinite banking strategy. Its crediting is variable and subject to caps, participation rates, and cost-of-insurance changes, which makes the capital base you borrow against less predictable. The And Asset uses whole life because its guarantees and contractual cash value give you a stable base to borrow against.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is IUL an investment?

No. Index universal life is an insurance contract, not a registered security. Its cash value can lose ground to charges and weak crediting, but it is not a market investment. Variable universal life and private placement life insurance are the only permanent policies that are actually registered investments with direct market risk.

Why is IUL so often missold?

IUL is frequently illustrated at the most aggressive crediting and loan assumptions, projecting paper arbitrage in a straight line for decades. This makes it look like an investment with upside and no downside. Conservative practitioners reduce the crediting assumption, model zero-return years, and show withdrawals before loans to set realistic expectations.

What is AG49 and why does it matter?

Actuarial Guideline 49 took effect in 2015 and set limits on the maximum rate insurers could use to illustrate index universal life. Before it, carriers could illustrate at 9, 10, or 11%, rates that often did not materialize. Policies sold before 2015 were frequently illustrated above today's allowable ceilings.

When does whole life make more sense than IUL?

Whole life makes more sense when you want safety, stability, contractual guarantees, and a predictable cash value you can borrow against without worrying about caps or crediting changes. It carries a higher required premium for the same death benefit, and that premium buys certainty.

Should you borrow aggressively against an IUL the way some borrow against whole life?

No. Aggressive borrowing against an IUL assumes positive arbitrage between the loan rate and the crediting rate that may not hold in a flat or down index year. The disciplined approach takes withdrawals to basis before loans and never assumes the spread will be positive every year.

What should I ask before I trust any policy illustration?

Ask for the illustration re-run 100 to 150 basis points below the maximum rate, ask how it performs with 0% crediting years inserted, and ask whether income is shown as withdrawals to basis or as loans. Then commit to reviewing the in-force illustration every year, because crediting, caps, and your goals all change.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- NAIC, Actuarial Guideline 49 and the rules governing index universal life illustrations.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- LIMRA, life insurance industry data, including persistency and product-mix benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

A death-benefit-first practitioner who works extensively with whole life, IUL, and VUL, and who submitted the policy that beat the IUL challenge. His framing of product function versus suitability anchors this review.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on which chassis fits your plan, book a discovery call. We will tell you if it does not.