.png)

Dynasty trust life insurance places a permanent policy inside an irrevocable trust that can last for centuries, so the death benefit passes to heirs outside the taxable estate while the trustee borrows against cash value for opportunities. It protects wealth from the two destroyers: tax erosion and family division.

Most families plan their money to the edge of one lifetime. They save for retirement, hope the account outlives them, and leave whatever is left to their children in a lump sum. Wealthy families plan on a different clock. They think in generations, and they build structure to survive the forces that quietly erase a fortune between the first generation that made it and the third that inherits it.

Generational wealth is almost never destroyed by bad investments. It is destroyed by bad structure: tax erosion that grinds the balance down, and division that scatters it into the wrong hands at the wrong time. A dynasty trust funded with life insurance is the tool the ultra-wealthy use to defend against both at once. The trust supplies the guardrails. The life insurance supplies the guaranteed liquidity that keeps the plan from ever being forced into a fire sale.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and this legacy conversation shows up constantly once a family has real assets to protect. For this piece, Caleb sat down with an estate-planning and advanced-life-insurance specialist who advises family offices, and the two worked through what family offices actually do, how the Rockefellers kept money together for a century, how a dynasty trust holds a policy, the math that decides whether borrowing against it makes sense, and the premium-finance pitches that create risk instead of shifting it.

This covers the structure, the honest tradeoffs, and how a family worth far less than the estate-tax threshold can still borrow the same principles. It also names, plainly, who this is not for.

- A dynasty trust is an irrevocable trust that can last centuries, keeping wealth together and outside each generation's taxable estate.

- The two real wealth destroyers are tax erosion and division, not bad investments. Structure protects against both.

- Life insurance inside the trust creates guaranteed liquidity that pays estate taxes without a forced sale of illiquid assets.

- The And Asset rule still governs: the trustee only borrows when the deployed return clears the carrier's loan cost.

- Premium finance fits only when the client could write the check, services the interest, and can exit the bank loan.

- You do not need an estate-tax problem to use guardrails and a max-funded policy. The principles scale down.

The full conversation goes deeper on grantor-trust taxation and the premium-finance failure modes than any summary can. Watch it for the back-and-forth on where these strategies quietly add risk:

01 / The problemWhat actually destroys generational wealth?

Generational wealth is destroyed by structure, not by returns. Families that lose everything by the third generation rarely lose it to a bad stock or a failed deal. They lose it to two forces that compound quietly in the background: erosion and division. Erosion is the drag of taxes, income tax and estate tax, chipping away at the balance every year and every transfer. Division is the money reaching the wrong hands at the wrong time, split across heirs with no guardrails and no plan.

The Vanderbilts are the cautionary tale. A fortune that dwarfed most of its era was scattered within a few generations, not because the investments failed, but because the structure did. The Rockefellers ran the opposite playbook. They kept the money together, protected it from erosion and division, and treated the family like a single enterprise rather than a set of independent branches. The difference was never the returns. It was the structure holding the returns in place.

The biggest wealth destroyer is not bad investments. It is bad structure. That is why families go broke across generations, and it is the one variable most people never plan for.

02 / The structureWhat is a dynasty trust, and how does it work?

A dynasty trust is an irrevocable trust built to last far beyond your lifetime, in some states more than a thousand years, so wealth passes down multiple generations while staying outside each generation's taxable estate. The name sounds like marketing. It is actually just a description of what the trust does: it endures, and it keeps the money together.

Underneath the label sit real legal mechanics. The trust is typically an intentionally defective grantor trust, drafted in a state whose rule against perpetuities allows a very long or perpetual term. It has a trustee who administers it, and often a trust protector and other roles who can direct the trustee on behalf of the beneficiaries. When the trust includes the grantor's spouse as a potential beneficiary, it is a SLAT, a spousal lifetime access trust, and a SLAT can itself be a dynasty trust.

Irrevocable versus revocable, and why it matters

The trust removes assets from your taxable estate only because it is irrevocable, and irrevocability is the tradeoff. You give up flexibility now in exchange for the estate-tax benefit later. Families without an estate-tax concern often do not want that complexity. They can use a revocable or testamentary trust instead, one you control and can change during your life, that springs into an irrevocable trust at death and accepts your estate with guardrails already in place. Same division control. No estate-tax removal, because none was needed.

Guardrails now. Estate benefit only if you need it.

03 / The frameworkHow families use life insurance inside the trust (and where The And Asset fits)

Families use a trust-owned life insurance policy as a private opportunity fund with a death benefit attached, and the discipline that makes it work is what we call The And Asset. Inside the trust, the trustee owns a cash value whole life policy. When an opportunity appears, the trustee reviews the trust documents, takes a policy loan, invests on behalf of the trust, and all the proceeds flow back into the same pool. At the end, the death benefit pays in and perpetuates it. The mechanics mirror how an individual uses a policy. The trust just adds a layer so the growth stays outside the taxable estate.

Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose it to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule that Nash's broader teaching does not enforce.

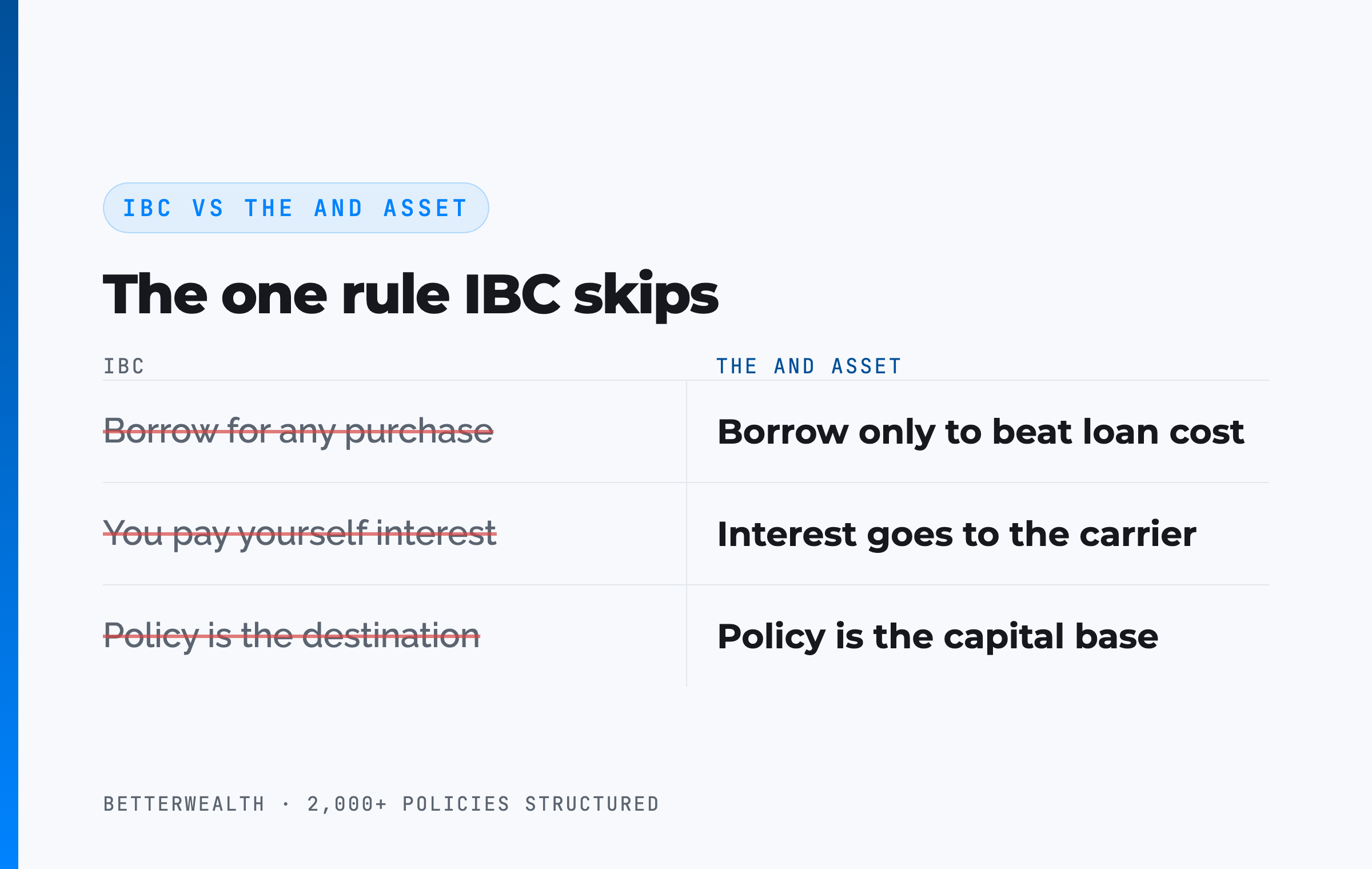

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal bank for any purchase. The And Asset says you only deploy capital when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy keeps compounding on its full value.

Notice how naturally the family-office model already obeys this rule. The trustee does not borrow to consume. The trustee borrows to invest in things the family understands and believes in, at a return that beats the cost. The wealthy have been running the disciplined version all along. Most retail infinite-banking content sells the undisciplined one.

You are not paying yourself interest. The interest goes to the carrier. Your return comes from what you deploy the capital into, while the policy compounds uninterrupted.

04 / How it worksHow to build a dynasty trust using life insurance, step by step

Building a dynasty trust funded with life insurance follows six steps, and the order matters as much as any single piece. This is the sequence a family and its advisors move through, with the attorney drafting the structure and the insurance designed to fund it.

- Define the legacy and the time horizon. Decide what the wealth is for across generations, financial and non-financial. Most people plan to the end of retirement. This planning looks past it. The horizon drives every decision that follows, and it does not happen by accident.

- Establish the irrevocable trust in the right state. With an estate attorney, draft the trust in a jurisdiction whose rule against perpetuities allows a long or perpetual term. Name the trustee, trust protector, and the distribution guardrails that prevent division.

- Fund the trust and file the gift tax return. Gift assets into the trust using your lifetime gift and estate tax exemption, and file a gift tax return documenting the exemption used. Funding with illiquid assets eligible for a valuation discount stretches the exemption further.

- Structure a max-funded whole life policy owned by the trust. The trustee owns an overfunded whole life policy built for cash value, with a heavy paid-up additions rider and minimal base premium, kept under the MEC limit. On the children and grandchildren who are trust beneficiaries, this builds a liquidity pool and a death benefit over decades.

- Let cash value capitalize, then deploy through the trustee. Early years build slowly. A healthy policy reaches break-even at year 5 or later, and any illustration showing break-even in year one or two is fiction. Once cash value is available, the trustee borrows only for an opportunity that returns more than the loan cost, and the proceeds flow back into the trust.

- Replenish at death and repeat. When the insured dies, the income-tax-free death benefit pays into the trust outside the taxable estate. It replenishes the capital pool and can fund the next generation's policies. The cycle continues past any single lifetime.

The trust holds it. The policy funds it. The discipline keeps it.

The grantor-pays-tax move, in plain terms

The word "defective" in intentionally defective grantor trust is deliberate, and it is the quiet engine of the whole structure. It means the grantor, not the trust, pays the income tax on the trust's assets. That sounds like a burden. It is a gift. Trusts hit the top income-tax bracket fast, so paying the tax personally can cost less. More importantly, paying it yourself removes tax drag from the trust, so the assets compound without peeling off money each year to cover taxes. And the IRS does not treat those tax payments as an additional gift. For a family already facing estate tax, the grantor paying the income tax also shrinks their own estate a little more each year.

Think of it the way a Roth compares to a traditional account. Paying the tax from outside the vehicle lets more money work inside it. Over 40 years, two identical portfolios grow to very different places depending on whether the trust or the grantor absorbed the tax drag. It is one of the few moments in planning where paying the tax is the efficient choice.

This structure fits a specific person doing specific things.

It fits you if

- You think generationally, not just to retirement

- You face, or expect to face, federal estate tax

- You can name uses for capital that beat the loan cost

- You want guardrails against division, at any net worth

It does not fit you if

- You want a savings account, not a capital strategy

- You are still building your first foundation of wealth

- You are buying insurance that adds risk instead of shifting it

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether a properly designed policy belongs in your plan, inside a trust or in your own name. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The logicWhy do wealthy families buy life insurance when they could self-insure?

Wealthy families buy life insurance to outsource risk and manufacture liquidity, not just for peace of mind. This is the part that confuses the "buy term and self-insure" crowd. The ultra-wealthy are the definition of self-insured, and they buy more life insurance than anyone. They do it because insurance is a way to shift risk to a third party in exchange for a guaranteed, tax-advantaged benefit that shows up exactly when the family needs cash.

All insurance is outsourcing risk. With auto and home coverage, you never really get a choice. With life, disability, and long-term care, you do. Doing nothing is a decision to retain the risk. Families with real assets choose to shift it because the alternative is concentration. If everything sits in the market, a downturn at the wrong moment forces you to sell low, compounding the loss and the stress. A policy is the buffer that lets you pull from one bucket while the others recover. It buys options.

The liquidity is the point, more than the growth

For these families, the death benefit does the heavy lifting. It creates liquidity at the end of a life that does not care what happened to the other assets. Maybe the real estate was consumed, maybe a business had a bad decade, maybe taxes took a bite. The death benefit still pays. That liquidity swaps into the trust, covers estate taxes, and keeps the family from dumping an illiquid asset at a terrible valuation right when the founder is gone and no one is thinking clearly.

The everyday version is the family home. Liquidity means you get to choose whether to sell it, instead of being forced to. Scale that up to a business or a real estate portfolio, and the death benefit is the difference between an orderly transition and a distressed sale.

The death benefit does not care what the market did.

If you do not care about outsourcing any risk at all, insurance is not for you in any form. But most people who say that are quietly living in scarcity, afraid of outliving their money.

06 / The mathDoes the deployed return clear the loan cost?

The return on whatever the trustee deploys must exceed the carrier's loan cost, or the loan should not happen. This is the entire test, whether the policy is owned by a trust or by you. Policy loan rates vary by carrier and by the rate environment. At the time of writing, many carriers fall in the 5 to 6 percent range, but treat any specific number as a variable to verify with the carrier, not a constant to build a plan around.

Here is the decision, stripped down. You borrow at the loan rate. The policy keeps compounding on its full cash value while the loan is outstanding. Your deployed capital earns its own return. If that return beats the loan cost, you are ahead on the spread, and the dollar has done two jobs at once. If it does not, you borrowed money to lose money slowly. There is no arbitrage in the policy itself that makes borrowing automatically profitable. The profit lives entirely in what you do with the capital.

One correction the numbers demand: a 6 percent dividend does not mean a 6 percent bump in your cash value this year. The policy compounds at the dividend rate net of mortality and expense charges, which is a different, lower figure in the early years. Anyone modeling a guaranteed spread between a gross dividend and a borrowing rate is selling a story the last three years have already disproven.

If the deal does not clear the loan rate, do not borrow.

07 / Where people get this wrongThe premium-finance pitch that creates risk

The most common way this strategy goes wrong is premium finance sold to people who should never touch it. Premium finance is real, and in the right hands it is powerful. You borrow to fund the premiums instead of paying them out of pocket, the policy collateralizes the loan, and you free your own capital for opportunities you understand. Used correctly, it is a version of the same idea: the dollar does more than one job.

The failure mode is the pitch. Marketers dress premium finance up as a retirement-income shortcut and aim it at people who could not fund the policy themselves, then gaslight anyone who questions the moving parts. So here is the standard that separates healthy from reckless.

- Could the client write the check and simply choose not to? If they could not afford the premium in the first place, the structure is already broken.

- Is the client servicing the interest, not accruing it? When interest compounds into the loan and future premiums pile on top, the debt grows into a number that has to be paid back before any cash is accessible.

- Can they exit the bank loan on a reasonable timeline, regardless of what rates do? If the plan only works when rates cooperate, it is not a plan.

The arbitrage story is the tell. Salespeople point to a roughly 2 percent historical gap between borrowing rates and crediting rates over the last few decades and treat it as a law of nature. It is not. Over the last three years that gap flipped negative: borrowing cost more than the policy credited. Put that negative spread on a growing pile of debt for a decade, and compounding works against you until the plan fails. The moment insurance introduces risk instead of shifting it, the whole reason to own it is gone.

There are people buying life insurance who are literally creating more risk by buying it. That should be the biggest red flag there is. The upside is never worth that kind of downside.

The Kai-Zen and MPI style structures usually fail this test on multiple counts. Premiums are borrowed rather than paid, interest accrues instead of being serviced, and exiting the bank on a fixed timeline is far from guaranteed. Ultra-wealthy families doing estate planning do not use those designs, because they insist on understanding their guarantees, their collateral, and how the moving parts behave when rates move the wrong way.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to pressure-test policies, premium-finance proposals, and how a policy fits inside a trust. Free, email-gated, no spam.

Open the Vault08 / Bringing it downHow does this apply if you are worth less than $20 million?

Most of the framework survives even when the estate-tax problem does not. If you are not going to owe federal estate tax, you probably skip the irrevocable dynasty structure and its complexity, but you keep the thinking that makes it work. Start by defining what you want your legacy to do, past retirement, financial and otherwise. Then look at risk the way these families do: not just the risk of running out of money, but sequence-of-returns risk and the risk of holding everything in one asset class.

From there, three moves translate directly. You can use a simple trust for guardrails, so wealth reaches your heirs with structure instead of as a lump sum that invites the exact behavior people blame on "trust fund kids." You can own a max-funded whole life policy as your own And Asset, borrowing against it for opportunities that beat the loan cost. And you can have the conversations, transparently, with the next generation, because stewardship is taught over a lifetime, not handed over on a deathbed.

One reframe worth keeping: in the wealthiest country in the world, you are wealthy, and if you are healthy, you are wealthy. Protecting and perpetuating that does not require a family office. It requires intention and structure.

Stewardship cannot be passed along on the deathbed. It has to be taught during the lifetime, alongside the structure and the assets. That part costs nothing and matters most.

A composite: the business owner who deployed through the trust

Consider a 47-year-old business owner, preferred non-tobacco, with an estate large enough to face federal estate tax. With counsel, he and his spouse each fund a SLAT structured as a dynasty trust. Inside one trust, the trustee owns a max-funded whole life policy at $84,000 per year, base/PUA split 20/80, on a cashflow design. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar begins adding more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing a year-two break-even is marketing fiction.

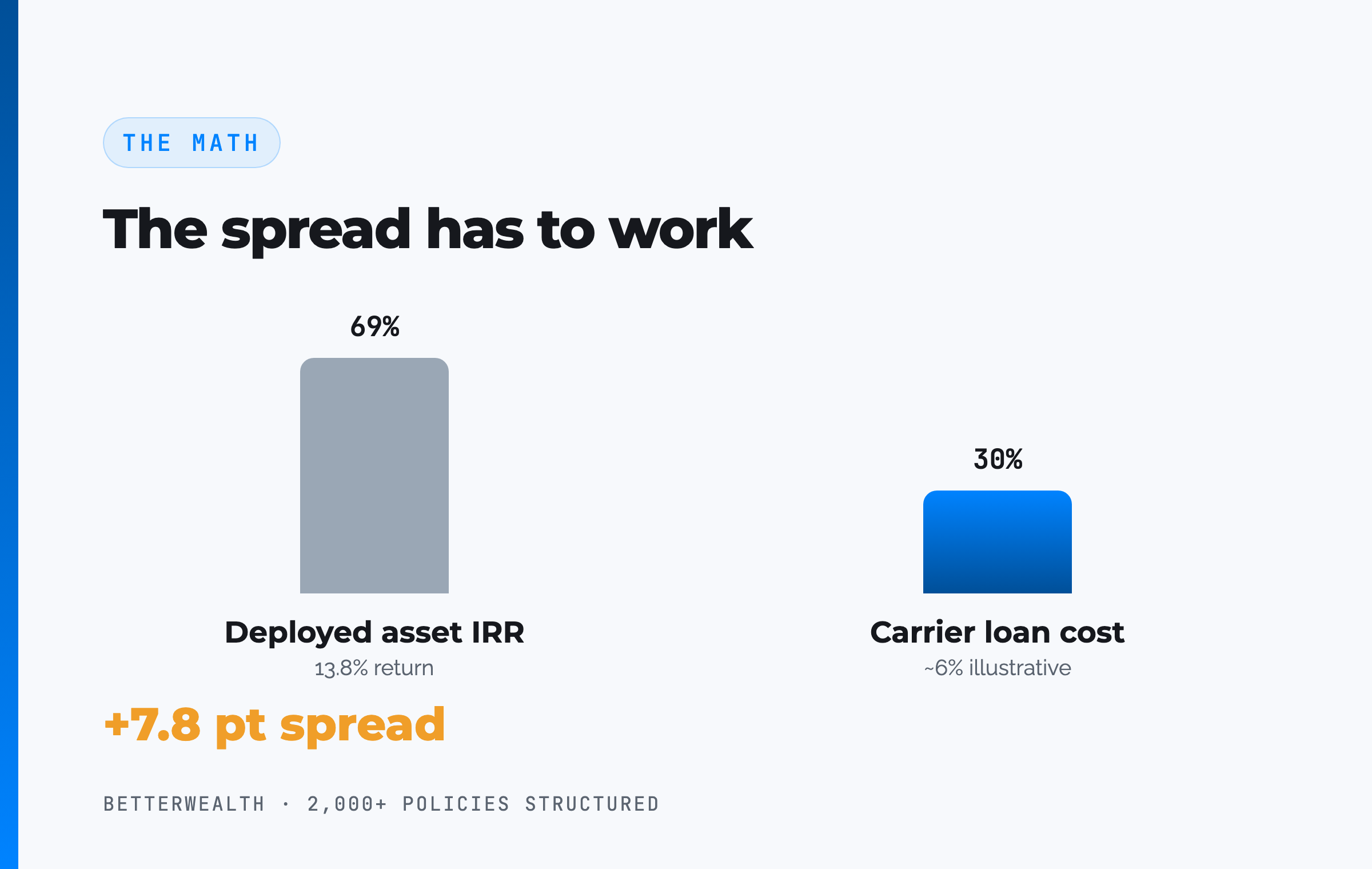

In year eight, with roughly $583,000 of accessible cash value inside the trust, the trustee borrows $291,000 against the policy to invest in a cash-flowing asset the family understands. The asset returns an estimated 13.8% IRR against an illustrative loan cost near 6%, so the spread works in the family's favor by nearly eight points. The policy keeps compounding on its full value the entire time. Repayment runs on a 44-month schedule funded by the asset's own cash flow, and every dollar of proceeds stays inside the trust.

At the insured's death, the policy pays a $2.85 million death benefit into the trust, income-tax-free and outside the taxable estate. It clears any outstanding loans, replenishes the family pool, and funds the next generation's coverage. The capital never left the family, and it never touched the estate-tax line.

One dollar. Two jobs. Outside the estate.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a properly designed policy, inside a trust or in your own name, belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery Call09 / Head to headDynasty trust versus the alternatives

Compared to the other ways families pass wealth down, a dynasty trust funded with life insurance trades lifetime flexibility for estate-tax removal, division control, and guaranteed liquidity. The table sets it against a revocable or testamentary trust and an outright inheritance on the four dimensions that decide whether wealth survives the transfer.

| Dimension | Dynasty Trust (irrevocable) + Life Insurance | Revocable / Testamentary Trust | Outright Inheritance |

|---|---|---|---|

| Estate tax | Assets and death benefit pass outside the taxable estate; defends against the 40% top rate above ~$15M | No estate-tax removal during life; assets stay in the estate until death | Full estate exposure; heirs may face a 40% bite above the exemption |

| Division control | Strong guardrails; distributes via loans and directed investments, wealth stays pooled | Guardrails available once it springs into effect at death | None; money is split and can scatter into the wrong hands |

| Access during life | Indirect, through the trustee and (with a SLAT) a spouse; less personal flexibility | Full control during your lifetime; you can change the terms | Not applicable; nothing exists until death |

| Liquidity at death | Guaranteed, income-tax-free death benefit pays taxes without a forced sale | Only if a policy is separately in place; otherwise assets may be sold | Heirs may be forced to sell illiquid assets at a bad valuation |

Estate tax. The irrevocable dynasty trust is the only column that removes assets from the taxable estate during your life, which is exactly why the complexity is worth it for families above the exemption and pointless for families below it.

Division and access. A revocable trust keeps your flexibility and still delivers guardrails at death, which makes it the right tool for most families without an estate-tax problem. The dynasty trust trades that flexibility for removing the assets now.

Liquidity. Outright inheritance is where fortunes get sold at fire-sale prices. Life insurance inside a trust is the guaranteed cash that lets heirs keep the business, the real estate, or the home instead of dumping it to cover a tax bill.

FAQDynasty trust and life insurance questions

What is a dynasty trust?

A dynasty trust is an irrevocable trust designed to last far beyond your lifetime, in some states over a thousand years, so wealth passes to multiple generations while staying outside each generation's taxable estate. Its purpose is to protect capital from tax erosion and from division into the wrong hands at the wrong time.

How do you build a dynasty trust using life insurance?

You establish an irrevocable trust with an estate attorney, fund it using your lifetime gift and estate tax exemption, and have the trustee own a max-funded whole life policy. The trustee borrows against the cash value for opportunities that beat the loan cost, and the death benefit later replenishes the trust income-tax-free and outside the estate.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Do I need to be ultra-wealthy to use a dynasty trust?

No. Full dynasty and estate-tax structures fit families facing federal estate tax, but the principles apply well below that. Families without an estate-tax concern can still use a simpler trust for guardrails and division control, and can use a max-funded whole life policy as an And Asset in their own name.

What is an intentionally defective grantor trust (IDGT)?

An intentionally defective grantor trust is an irrevocable trust structured so the grantor, not the trust, pays the income tax on the trust's assets. That is intentional: the grantor paying the tax lets the trust assets grow without income-tax drag, and the IRS does not treat those tax payments as an additional gift.

What is a SLAT?

A SLAT, or spousal lifetime access trust, is an irrevocable grantor trust that names the grantor's spouse as a potential beneficiary. It moves assets out of the taxable estate while keeping indirect access to the funds through the spouse, and it can also be structured as a dynasty trust.

Why do wealthy families buy life insurance if they can self-insure?

Wealthy families buy life insurance to outsource risk and create guaranteed liquidity, not just for peace of mind. The death benefit pays estate taxes and replenishes the family's capital without forcing a fire sale of illiquid assets, and it diversifies away the sequence-of-returns risk of holding everything in the market.

Is premium finance a good way to fund a dynasty trust policy?

Premium finance fits only when the client could write the premium check but chooses to borrow for opportunity cost, services the interest rather than accruing it, and can exit the bank loan on a reasonable timeline. When it is pitched as a retirement-income shortcut to people who could not fund the policy themselves, it usually adds risk instead of shifting it.

Can beneficiaries access money from a dynasty trust before they inherit?

Yes. A well-designed dynasty trust typically distributes to beneficiaries through loans and directed investments rather than outright checks, so heirs can access capital for education, a business, or a home while the wealth stays inside the trust and protected from division.

Does a dynasty trust avoid income tax?

No. A dynasty trust addresses estate tax and division, not income tax. Income earned on trust assets is still taxed. In a grantor trust the grantor pays that income tax, which is the point, because it removes tax drag from the trust while further reducing the grantor's own estate.

What is the difference between a revocable and irrevocable trust for legacy?

A revocable trust can be changed during your lifetime and can spring into an irrevocable trust at death, giving you guardrails and division control without estate-tax benefits. An irrevocable trust removes assets from your taxable estate now, which matters only if you face estate tax, but it is far less flexible during your lifetime.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRS, Estate Tax, federal estate tax rules, exemption, and rates.

- IRS, Gift Tax FAQ, the lifetime exemption and gift tax return basics.

- IRC Section 7702 (Cornell Law), the tax treatment of life insurance cash value and loans.

- Garrett Gunderson, What Would the Rockefellers Do, a widely read look at the family-office legacy mindset referenced in the interview.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Advises family offices on dynasty trusts, grantor-trust taxation, premium finance, and estate-tax strategy, and joined Caleb on the show to break down how the ultra-wealthy actually integrate insurance and trust planning.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a policy, inside a trust or in your own name, fits your plan, book a discovery call. We will tell you if it does not.