.png)

Dangerous tax advice online usually promises a legal way to pay zero taxes, and almost all of it is fraud. Tactics like checking a W-4 exempt box, the 12411 "lawful money" process, or routing income through a spendthrift trust carry civil penalties, and in many cases criminal charges and prison time.

Every tax season, the same promise goes viral. A confident person, often filming next to an expensive car, explains a "process" the wealthy supposedly use and your accountant supposedly hides from you. The vocabulary sounds technical. The screenshots look official. And the conclusion is always the same: you never have to pay taxes again.

The strategies that actually reduce taxes are real, narrow, and unglamorous. The ones that promise to erase taxes entirely are usually fraud wearing the vocabulary of tax law. The gap between those two things has sent ordinary people to federal prison, while the promoters who sold them the idea collect clicks and course fees.

We brought Toby Mathis, a tax attorney and founding partner of Anderson Business Advisors, onto the show to react to a series of these clips. His read on most of them was fast and unambiguous. Words have meaning, the schemes ignore the fine print, and the people who follow them are the ones who pay.

At BetterWealth, this matters to us for a specific reason. We have structured more than 2,000 policies for entrepreneurs and high-income earners, and we have watched the life insurance world get oversold in exactly the same way. The line between a real strategy and a pitch is honesty about the limits. This piece covers the most common viral tax claims, what the law actually says, and what a legitimate, tax-aware life insurance strategy looks like by comparison.

- Filing taxes is self-assessed, which the IRS calls voluntary compliance, but payment of tax owed is mandatory under federal statute.

- Checking the W-4 exempt box while you actually owe tax is a false statement under penalty of perjury, with civil and criminal exposure.

- The "lawful money" and "voluntary tax" arguments are frivolous, have never won, and have put both promoters and followers in prison.

- Real strategies like Section 121, cost segregation, and the Augusta rule work, but only inside strict limits the viral clips ignore.

- Legitimate planning lowers a graduated tax bill, it does not zero it out, and any promise of zero is a red flag.

- The And Asset uses real tax treatment under the code, with one honest rule: only borrow when the return beats the loan cost.

Watching a tax attorney react in real time is the fastest way to learn the tells. Toby reads each clip, names the exact code section, and shows where the argument collapses:

01 / The problemWhy "tax-free" advice goes viral, and who pays for it

The advice goes viral because it sells a feeling, not a strategy, and the people most likely to act on it are high earners who feel overtaxed. The format rewards confidence over accuracy. A creator who says something outrageous and certain earns more attention than a CPA explaining limits and exceptions, so the loudest voices are often the least reliable.

The cost lands on the follower, not the promoter. Toby's framing throughout the conversation was consistent: it does not matter what sounds clever on camera, it matters what the courts have already decided and what happens to you when your return is examined. The promoter keeps the course revenue. The follower keeps the liability.

"It doesn't matter what you and I think. It matters what the Supreme Court thinks and what's going to happen to you. You're looking at jail time. That's who matters.", Toby Mathis

02 / The mythIs paying taxes actually voluntary?

No. Filing your return is self-assessed, which the IRS describes as voluntary compliance, but paying tax you owe is mandatory under federal statute. The whole "taxes are voluntary" movement hangs on misreading that one word. Voluntary compliance means you prepare and submit your own return rather than waiting for the government to bill you. It does not mean payment is optional.

The filing requirement itself sits in Section 6012 of the code. If you have a tax liability and choose not to file, that is a crime. It starts as a misdemeanor and escalates to a felony with repeated years or larger dollar amounts. Toby put the test simply: nobody walked up and held a gun to your head to make you file, so the filing is yours to do. The ramifications for skipping it are what the law makes compulsory.

Self-assessed filing. Mandatory payment. Two different things.

"They see one thing, and they're like a dog with a bone, and they quit reading. The IRS is telling you the truth, but it's not what you think.", Toby Mathis

03 / The schemesCan the W-4 exempt box and the "12411 process" make income non-taxable?

No to both, and both carry criminal exposure. These are two of the most-shared "live tax-free" clips, and they share a structure: take a narrow, real provision and stretch it into a blanket exemption it was never meant to support.

The W-4 exempt box

Checking exempt on your W-4 is legitimate only in a narrow case. If you had no tax liability last year and reasonably expect none this year, because your income falls under the standard deduction, you can claim it. The viral version tells everyone to check it. Doing that while you actually owe tax is a false statement made under penalty of perjury. Toby noted the IRS tied up more than 700,000 refunds in a recent year auditing exactly this kind of claim. The downside is civil penalties at minimum and criminal fraud exposure at worst.

The "12411 lawful money" process

This one tells you to "redeem" your income as non-taxable United States notes rather than taxable Federal Reserve notes, using a software product to claim a 100% refund. It is a frivolous argument, and Toby was blunt: no taxpayer has ever won it. The Supreme Court has been unequivocal that anything of value transferred to you is taxable, whether you are paid in dollars, gold, Bitcoin, or chickens. The currency label is irrelevant to the tax.

The clip in question featured a promoter holding a stack of cash and claiming he had paid nothing since 2020. Toby's response named the real risk. There is a long history of promoters and followers in this space who were prosecuted and went to prison, including a famous actor who served time on counts of willful failure to file after relying on this kind of advice. Believing the argument sincerely does not make it legal.

"Your filing is voluntary. If you don't file and you have a liability, that's a crime. You can hold a big stack of cash, but there's no such thing as cash that's non-taxable and cash that is.", Toby Mathis

04 / The half-truthCan you build a house every two years and live tax-free?

No, not the way the clip describes it, because building homes to sell makes you a dealer rather than a homeowner. The real provision is Section 121. It excludes up to $250,000 of gain for a single filer and $500,000 for a married couple on the sale of a primary residence, as long as you lived in it for two of the last five years. That is a genuine benefit, and Toby has used it himself.

The viral version breaks it. The creator said to build a house, live in it, sell it, and repeat every two years as a job. The moment your intent is to build and sell, the IRS treats you as a dealer in a trade or business. Dealer profit is ordinary income, not capital gain, and it can face employment taxes on top. Intent is what the agency examines, and the creator stated his intent on camera.

Toby's neighbor framing makes the principle clear. If you and a neighbor own identical houses, but you live in yours and the neighbor rents theirs as an investment, the tax code treats the two of you very differently. Section 121 exists to reward homeowners who improve and eventually sell a residence, not to hand a developer a permanent exemption.

05 / The big oneDoes cost segregation make your W-2 and 1099 income tax-free?

Rarely, because rental depreciation losses are passive and most people cannot use them against active income. Cost segregation itself is a real and useful tool. It accelerates depreciation by breaking a property into its components: carpeting and appliances as five-year property, landscaping and fencing as fifteen-year land improvements, much of it eligible for bonus depreciation under Section 168(k). On a typical home, the accelerated piece runs around 30% of the improvement value.

The viral promise is where it falls apart. The clip claimed a cost segregation study creates a loss big enough to wipe out your W-2, 1099, stock, and crypto income. For an ordinary real estate investor, those losses are passive, so they can only offset passive income, not your salary or business profit. There are only two doors out of that limit.

- Real estate professional status. One spouse must spend at least 750 hours and more than half of their working time in a real estate trade or business, and the couple together must materially participate in the rentals. That is construction, brokerage, or property management, not a side investment.

- Short-term rentals. An average guest stay of seven days or less, with material participation, can move the activity out of the passive bucket because it behaves more like a hotel than a rental.

Even when a loss is unlocked, more limits apply. There is an excess business loss limitation that caps how much you can use in a year, indexed for inflation and in the low six figures for a single filer at the time of writing. There is depreciation recapture later, taxed as ordinary income under Section 1245 on personal property. And state conformity varies. Toby pointed out that California does not conform to bonus depreciation and caps Section 179, so a strategy that looks great on the federal side can collapse at the state level. People often discover this a year later, when the penalties for underpayment arrive.

A paper loss you cannot use is not a tax strategy.

"Cost segs are powerful for the right person. But you're conflating federal and state, conflating investor and active business, and ignoring that the loss is passive. That's where the harm starts.", Toby Mathis (paraphrased)

Tax-aware life insurance strategy fits a specific person.

It fits you if

- You are a high earner already paying real tax and deploying capital

- You want legitimate planning, verified by a professional

- You can name a use for capital that beats the loan cost

- You value control and clean tax treatment over a flashy promise

It does not fit you if

- You are chasing a way to pay zero taxes

- You want a savings account, not a life insurance strategy

- You will not run the strategy through a credentialed advisor

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether The And Asset adds anything to what you already do. If you are in the second, we will tell you that too.

Book a Discovery Call06 / The everyday trapsThe vehicle write-off, the Augusta rule, and the 20% claim

These are the half-truths most likely to reach a legitimate business owner, because each one starts from a real provision and then overstates it. They are worth understanding precisely.

You cannot write off the car and take mileage

One clip claimed a car deducted as a business expense plus the standard mileage deduction. You have to choose one method. Actual expenses, which includes depreciation on the vehicle, or the standard mileage rate, not both. To take bonus depreciation on a vehicle, it must be used more than 50% for business, supported by a mileage log. Drop below 50% in a later year, and you recapture the bonus you took. Toby's practical advice was to keep it simple and reimburse mileage rather than chase a large write-off on an expensive vehicle that loses value the moment you drive it off the lot.

The Augusta rule is real and small

Under Section 280A(g), you can rent your personal residence to a third party for up to 14 days a year and not recognize the income. Your own business can be that third party if it holds an actual meeting in the home at a fair market rate, documented with comparable quotes. It is a legitimate move that Toby has written about for more than two decades. It is also a few thousand dollars, not a path to zero.

The 20% deduction is on net income, not your whole bill

A clip claimed that because the business is an S corp, "20% of my net income is not taxable," and concluded the tax owed was a dollar. The Section 199A deduction is 20% of net business income, with phase-outs, wage and asset tests, and exclusions for specified service businesses. Twenty percent of a positive number is not zero. A deduction reduces taxable income, it is not a credit that erases the tax.

07 / The dangerous oneDoes an irrevocable spendthrift trust eliminate business taxes?

No, and this is the scheme Toby flagged as the most misleading of the set. The pitch claims you route business income through an irrevocable spendthrift trust, allocate it to the "corpus," and defer tax on every penny while spending the money on personal expenses. It collapses on the most basic rule in the code.

Section 61 says an ascension of wealth is taxable unless a specific exemption or exclusion applies. Someone always pays the tax on trust income. The provision the promoters misuse is Section 643, which deals with distributable net income. When a trust distributes income to a beneficiary, the beneficiary is taxed and the trust gets a deduction for the distribution. When the trust retains income, the trust pays the tax, and trusts reach the top tax bracket at a far lower income threshold than individuals do. There is no version where the income simply disappears.

The "spend it through the trust" claim is the same error in a different costume. If a trust or a business pays your personal expenses or buys you a car, that transfer of value is income to you, subject to withholding and employment taxes. Wealthy families use trusts constantly, but for estate planning and asset protection, not to make business profit vanish. Treating personal spending as a deductible trust expense is, in Toby's words, plainly misleading.

If value moved to you, someone owes tax on it.

08 / The honest versionWhat does a legitimate, tax-aware life insurance strategy look like?

A legitimate strategy works inside the code, names its limits up front, and lowers a tax bill rather than promising to erase it. This is the standard every claim in the video failed, and it is the standard The And Asset is built to meet.

Here is the connection to what we do. Permanent life insurance has a defined place in the tax code. Cash value in a properly structured, non-MEC whole life policy grows tax-deferred, and a policy loan is generally not treated as taxable income because you are borrowing against your own cash value rather than receiving a distribution. That treatment is real, and the tax framework for life insurance predates most of the retirement accounts people compare it to. It is also not magic, and it is not "tax-free wealth."

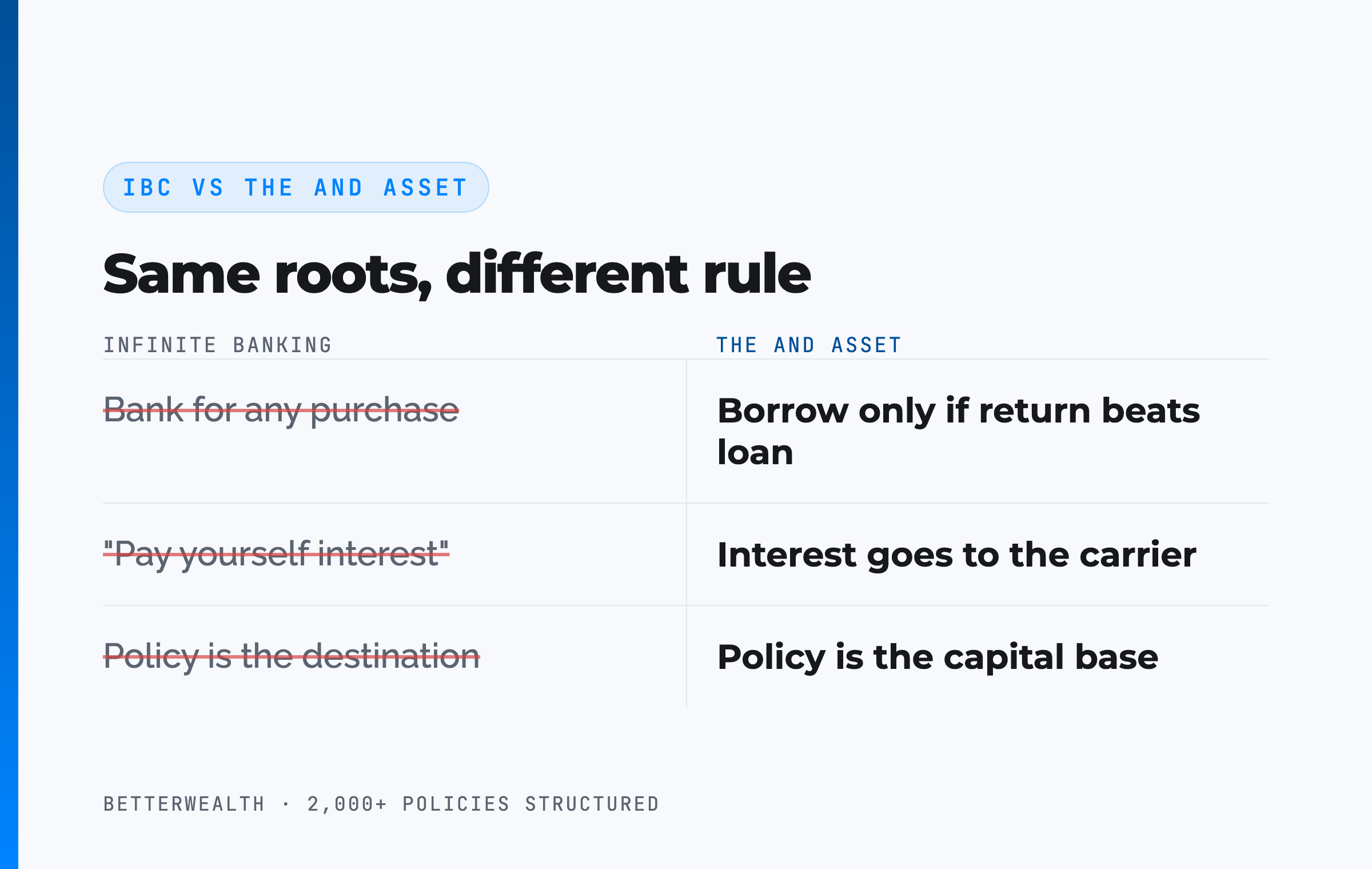

Where IBC marketing ends and The And Asset begins

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system, and we credit that foundation. Many infinite banking marketers then oversold it, promising a self-contained bank where you "pay yourself interest" and never owe taxes again. That is the same overselling energy as the TikTok clips above, applied to a different product.

The And Asset operates on different principles. IBC says use the policy as a personal bank for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. The interest on a loan goes to the carrier, not to yourself. Your return is what the deployed capital earns elsewhere while the policy keeps compounding at the dividend rate net of mortality and expense charges. The tax treatment is a real feature of the code, used honestly, with a hard rule attached. It is built on Nash's foundation but operates on different principles.

Marketers have ruined how this strategy gets explained, the same way social media ruined tax advice. The fix is the same in both cases: name the real rule, state the limit, and do the math.

A composite: the practice owner who was pitched a trust scheme first

Consider a 44-year-old practice owner, preferred non-tobacco, who was first sold on an irrevocable spendthrift trust promising near-zero tax. After a second opinion killed that idea, the owner kept the legitimate planning and funded an overfunded whole life policy at $63,000 per year on a cashflow design. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing a year-two break-even is marketing fiction, the same overpromising the tax clips run on.

In year eight, with roughly $392,000 of accessible cash value, the owner borrows $214,500 against the policy to buy into the building that houses the practice. The buy-in returns an estimated 13.8% IRR through rent the practice already pays. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by nearly eight points, and the policy keeps compounding on its full value the entire time. Repayment runs on a 44-month schedule funded by the rent. No fraud, no frivolous argument, real tax treatment used as designed.

One dollar. Two jobs. That is the And.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and the math we use to test whether borrowing against a policy actually beats the loan cost. Free, email-gated, no spam, and no promises of zero tax.

Open the Vault09 / The fixWhat should you do if you already followed bad advice?

Come forward and file before the IRS finds you, because voluntarily correcting the record changes the outcome dramatically. Toby's framing was that you do not unwind these situations, you wind them. If you have unfiled years or fraudulent claims, pull your transcripts, work with a credentialed professional, and file the corrected returns.

The reason this matters is the discretion the agency holds. A failure to file is a misdemeanor that becomes a felony with multiple years or larger liabilities. If you initiate the conversation, state what you owe, and make a good-faith effort to pay or set up a plan, the matter is far more likely to stay civil. If the IRS catches you first, especially after you posted videos advocating the conduct, the odds shift toward a referral to the Criminal Investigation Division. Starting the discourse yourself is a different story than getting caught.

10 / The filterHow do you pressure-test tax advice before you act?

Run it through a disinterested professional and the actual code section before you act on anything you saw online. Toby's recommended filter is simple and worth following step by step.

- Identify who profits. If the person earns from clicks, a course, or software rather than from defensible tax work, treat the content as entertainment. The loudest voices are usually the ones to ignore.

- Find the actual code section. Make the strategy name the statute it relies on, then read the limits. A real strategy survives the fine print. A scheme falls apart in it.

- Get a second opinion from someone with nothing to gain. A tax attorney or CPA who is not selling you the strategy can flag the missing pieces in minutes. Anderson's free Tax Tuesday is one place Toby pointed people for that kind of read.

- Model the real after-tax math. Account for employment taxes, recapture, passive activity limits, excess business loss caps, and state conformity. The headline deduction is rarely the number that lands.

- Treat any promise of zero as a red flag. Legitimate planning lowers a graduated bill. It does not erase it.

Scheme versus strategy, side by side

The viral clips and legitimate planning often borrow the same words. The difference is in the limits each one respects. The table sets the most common claims against what the law actually allows.

| Claim | What the clip promises | What the law actually allows | The real risk |

|---|---|---|---|

| W-4 exempt box | Check it and stop paying tax | Only valid with no prior and no expected liability | Perjury, civil penalties, criminal exposure |

| "Lawful money" 12411 | 100% refund of all taxes | Frivolous, never won in court | Prosecution and prison |

| Build and sell homes | $250K / $500K tax-free every 2 years | Section 121 for a genuine primary residence only | Dealer status, ordinary income, employment tax |

| Cost segregation | Wipes out W-2 and 1099 income | Passive loss unless REPS or short-term rental | Suspended losses, recapture, state non-conformity |

| Spendthrift trust | Defer tax on every penny, spend freely | Trust or beneficiary is taxed under §61 and §643 | Compressed trust brackets, disallowance, penalties |

The pattern. Every row starts from a real concept and then deletes the constraint. Section 121, cost segregation, and trusts are all legitimate. The fraud is in the word "every," in the word "all," and in the promise of zero.

The lesson for life insurance strategy. The same discipline applies to life insurance. A policy has real, defined tax treatment, and a strategy built on it works only when you respect the limits and the loan math. That is the entire difference between a tool and a pitch.

The honest 30 minutes about whether this fits you.

We have structured more than 2,000 policies across all 50 states, and we have seen this strategy work and seen it fail. On a discovery call, a practitioner looks at your specific situation and tells you whether The And Asset belongs in your capital structure, or whether it does not. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQDangerous tax advice, answered

Is paying taxes voluntary in the United States?

No. Filing is self-assessed, which the IRS calls voluntary compliance, but payment of tax owed is mandatory under federal statute. You prepare your own return rather than receiving a bill, but if you have a tax liability and fail to file or pay, that is a crime that starts as a misdemeanor and escalates to a felony.

Can you check the exempt box on your W-4 to stop paying taxes?

Only if you had no tax liability last year and expect none this year. Claiming exempt while you actually owe tax is a false statement made under penalty of perjury, exposing you to civil penalties and possible criminal charges. The IRS has tied up hundreds of thousands of refunds auditing fraudulent exemption claims.

Does the 12411 "lawful money" process make your income non-taxable?

No. The claim that you can redeem Federal Reserve notes for non-taxable "lawful money" is a frivolous argument that no taxpayer has ever won. The Supreme Court has been clear that anything of value transferred to you is taxable, regardless of the form of currency. Promoters and followers of this scheme have gone to prison.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return. Its tax treatment is real and grounded in the tax code, not a loophole.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Can you build a house every two years and live tax-free?

No, not the way the viral version describes it. Section 121 excludes up to $250,000 of gain for a single filer and $500,000 for a married couple on a primary residence lived in for two of the last five years. Building homes to sell repeatedly makes you a dealer, which converts the profit into ordinary income that can also face employment taxes.

Does cost segregation make your W-2 or 1099 income tax-free?

Rarely. Cost segregation accelerates depreciation on a rental, but those losses are passive and can only offset passive income unless you qualify for real estate professional status or run a short-term rental with material participation. Excess business loss limits and state non-conformity, such as California's, shrink the benefit further.

Can a car write-off and the standard mileage deduction be claimed together?

No. You choose either actual expenses, which includes depreciation on the vehicle, or the standard mileage rate. You cannot take both. A vehicle must be used more than 50% for business to claim bonus depreciation, and dropping below that threshold triggers recapture of the deduction you took.

Does an irrevocable spendthrift trust eliminate business taxes?

No. Under Section 61, an ascension of wealth is taxable, and someone has to pay the tax on trust income. If the trust distributes income, the beneficiary is taxed. If the trust retains it, the trust is taxed, and trusts hit the top bracket at a far lower income threshold than individuals. Spending trust funds on personal expenses does not make the value non-taxable.

How should you vet tax advice you see on social media?

Take it to a disinterested credentialed professional who is not trying to sell you anything. Ask a tax attorney or CPA to identify what the strategy gets right, what it leaves out, and where the risk sits. Treat social media tax content as entertainment, and remember that legitimate planning lowers a tax bill rather than erasing it.

- IRC Section 61 (Cornell Law), gross income, the rule that an ascension of wealth is taxable.

- IRC Section 121 (Cornell Law), the primary-residence gain exclusion.

- IRC Section 280A (Cornell Law), the basis for the Augusta rule on short-term home rental.

- IRS, The Truth About Frivolous Tax Arguments, the agency's own catalog of "voluntary" and "lawful money" claims.

- Anderson Business Advisors, Toby Mathis and the firm's free Tax Tuesday Q&A sessions.

- IRC Section 7702 (Cornell Law), the provision behind the tax treatment of life insurance cash value and loans.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

A tax attorney who has advised business owners and real estate investors for nearly three decades, and the host of Anderson's free Tax Tuesday sessions. He provided the legal analysis throughout the source video. andersonadvisors.com →

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a tax-aware life insurance strategy fits your plan, book a discovery call. We will tell you if it does not.