.png)

The best life insurance company for infinite banking in 2026 depends on what you value. Penn Mutual leads on long-term growth, Guardian and Lafayette Life lead on early cash value, and Penn Mutual leads on funding flexibility. All 10 top mutual carriers sit in the top 1 to 2% of US insurers for this strategy.

There is no single winner, and any guide that crowns one is selling you something. The right carrier is the one that fits your goal, your state, and your funding style. Here is who leads each category.

The most common question we get is also the hardest to answer honestly: what is the best insurance company for infinite banking? Most content answers it by comparing dividend rates, crowning whoever posts the biggest number, and moving on. That answer is wrong, and it is wrong in a way that costs people real money over thirty years.

Among top mutual carriers, the design of the policy and your discipline in using it matter far more than which company name is on the contract. The carrier refines the result. It does not determine success. Once you accept that, the real question changes from "who is best" to "who is best for my goal, my state, and my funding style."

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we just finished reviewing 10 mutual carriers one at a time: Ameritas, Foresters, Penn Mutual, Guardian, Lafayette Life, MassMutual, New York Life, OneAmerica, Pan-American, and Security Mutual. There are more than 700 life insurers in the United States. These 10 are the 1 to 2% worth using for an infinite banking style policy.

This guide pulls all of it into one place. We will cover how to actually compare carriers, why the dividend rate misleads you, what direct versus non-direct recognition really changes, which company leads each category, and how this fits The And Asset framework. We will not hand you a single name, because the honest answer has conditions attached.

- No single carrier wins every category. The best company depends on whether you value growth, early access, strength, or flexibility.

- The dividend interest rate is the most overhyped metric. It is gross, before mortality and expense charges, and a higher rate does not mean better growth.

- Penn Mutual leads long-term performance and PUA flexibility; Guardian and Lafayette Life lead early cash value.

- Direct versus non-direct recognition matters less than policy design and early cash value over a long horizon.

- New York residents are limited to Ameritas, Guardian, MassMutual, New York Life, and Security Mutual.

- The And Asset rule still governs every carrier: only borrow when the deployed return clears the loan cost.

If you want to watch Alden walk the actual cash value and death benefit numbers across all 10 carriers, year by year, the full comparison is on screen here:

01 / The problemWhy "what's the best company?" has no clean answer

The question has no single answer because the right carrier depends entirely on what you are optimizing for. Where you live, your health rating, your funding style, and whether you care about year five or year forty all change the answer. A company that looks average on one metric can be the clear winner on the metric you actually care about.

That is why every carrier in our series got a pros section and a considerations section. None of them is all upside. Foresters comes out of the gate with the highest early cash value, then slows down over time. Penn Mutual starts lower and pulls ahead for decades. Reading only one of those numbers gives you the wrong company.

"It's impossible to answer what the best insurance company is, mainly because it depends on what you value, where you live, and your health rating. There are a lot of factors.", Caleb Guilliams

02 / The frameworkWhat does infinite banking with these carriers actually mean?

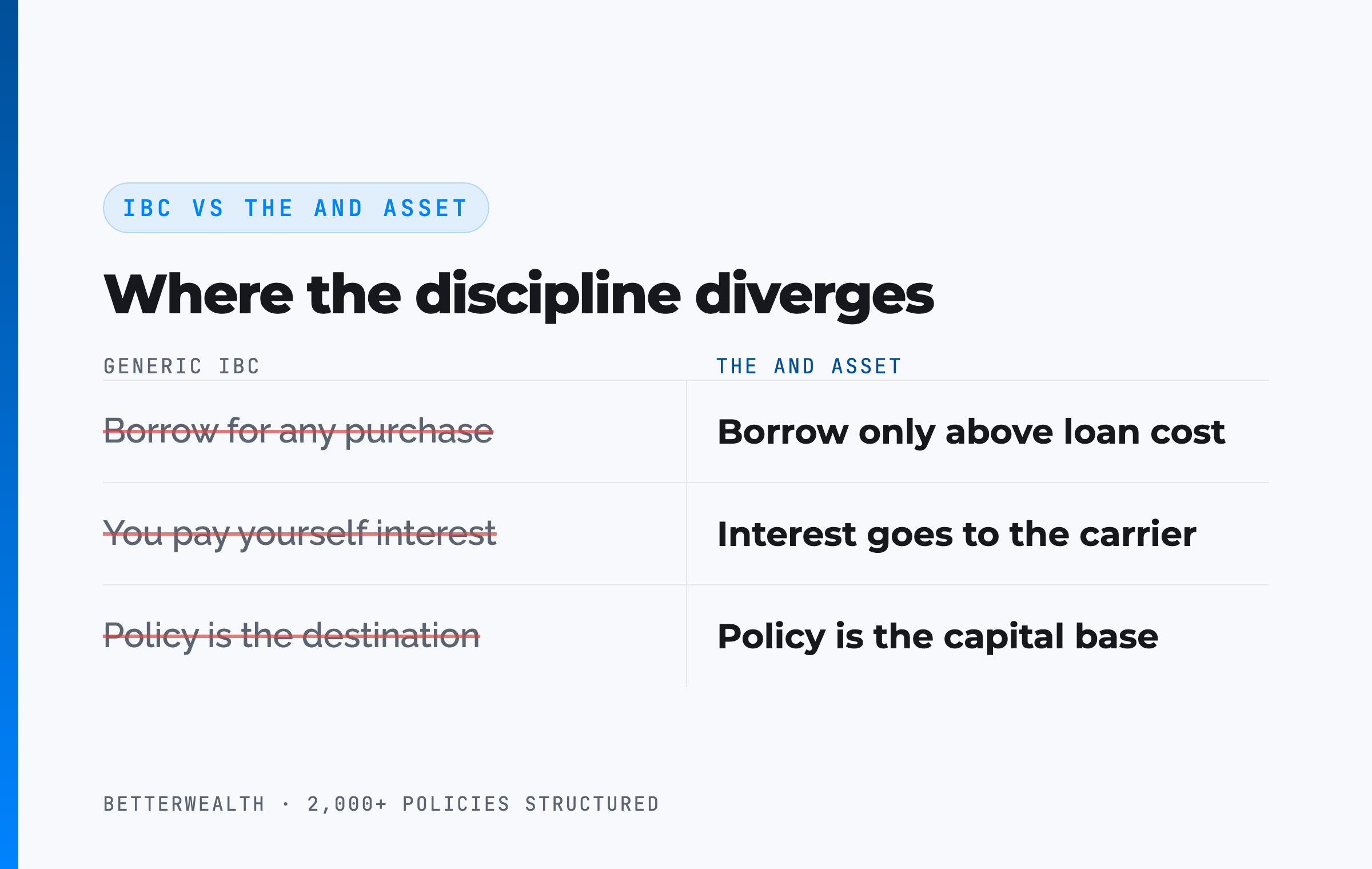

Infinite banking with any of these carriers means using a properly structured whole life policy as a capital base you borrow against, while the policy keeps compounding on its full value. That is the mechanical definition. The discipline layered on top is what we call The And Asset.

Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy compounds uninterrupted.

The carrier choice does not change that rule. It only changes how efficiently the capital base is built and accessed. Pick the wrong carrier and you lose a few points of efficiency. Skip the discipline and you lose the whole strategy.

The math has to work. The carrier is secondary.

03 / Financial strengthHow do you compare carrier strength for a 30-year strategy?

You compare strength with two rating systems, because a banking system you plan to hold for decades has to outlive the rate environment that created it. AM Best is the most recognized independent rating. COMDEX is a percentile score from 0 to 100 that blends the major agencies, so a 100 means the top 1% of insurers and an 83 means the top 17%.

We target carriers in the top 10% on COMDEX, and most of this group clears that bar. Guardian and New York Life are the powerhouses, both at COMDEX 100 and AM Best A++. Penn Mutual carries a distinction no other carrier in the industry can claim: an AM Best rating of A or better for 98 consecutive years.

Strength is not just a vanity badge. When you partner your protection with a carrier for thirty years, its staying power is the foundation everything else sits on. Look up the COMDEX score of whoever writes your auto and home insurance. You may be surprised how far below these mutuals it sits.

04 / The dividend trapWhy doesn't the highest dividend rate win?

The highest dividend rate does not win because the dividend interest rate is a gross number, not your growth rate. The carrier announces a rate, then subtracts mortality charges and expenses before anything compounds inside your policy. Two carriers can post identical dividend rates and deliver very different cash value.

MassMutual makes the point. It posts the highest 2026 dividend rate in the group at 6.6%, yet it does not have the best long-term cash value growth. Penn Mutual posts a lower 6.1% dividend rate and still leads on internal rate of return, because it runs lean in other areas and that shows up in the projections.

Any agent who tells you "MassMutual pays 6.6%, so your policy compounds at 6.6% tax-free" is either careless or selling. That is not how it works. The figure that matters is the internal rate of return on cash value, which reflects the dividend after the carrier's internal costs. The dividend rate is one of the least useful pages in the entire comparison.

The dividend rate is the most overhyped number in this industry. A 6.6% dividend does not mean 6.6% growth. Mortality and expense charges come out first. Compare internal rate of return, not headline rates.

05 / RecognitionIs direct or non-direct recognition better for infinite banking?

Neither is categorically better, and the infinite banking community has spent twenty years overstating how much it matters. The reason is simple: insurance companies do not lose on loans. Over a long horizon, whether they directly recognize the loan or charge a full variable rate, it largely comes out in the wash.

Direct recognition means the dividend paid on the loaned, collateralized portion of cash value can move up or down depending on the rate environment. Guardian and Penn Mutual are the two direct-recognition names here, plus Pan-American, with Ameritas letting you choose per loan. Non-direct recognition keeps the dividend unchanged when you borrow, which is simpler and more predictable. Lafayette Life, MassMutual, New York Life, OneAmerica, and Security Mutual sit here.

When each one actually helps

Direct recognition shines in two spots. In a rising-rate environment, the dividend on loaned values can be pulled up faster. And in the distribution phase, a known spread makes retirement income math cleaner. Guardian gives real estate investors a fixed 5% loan rate for the first 10 years, then a choice of fixed or variable. Penn Mutual guarantees a 0.65% spread between loan rate and dividend rate in years 1 through 10, then flattens it to a 0% spread from year 11 on, which is built for taking income later.

Non-direct recognition shines when you want simplicity and predictability, and historically in falling-rate environments, where dividends can stay elevated for two to three years after rates drop. That lag is where the old "arbitrage" claim came from. It was real in specific windows of the last 25 to 30 years, and it is not the rule. In today's rate environment, arbitrage does not exist at any carrier, because loan rates sit well above policy internal rates of return.

One more reason not to obsess over this: third-party lenders erase the conversation entirely. You pledge your cash value and death benefit as collateral, get faster and often cheaper access, and the recognition type stops mattering. Many of our more sophisticated clients borrow this way, partly because it can make loan-interest deductibility cleaner for business use.

Pick the carrier on early cash value and design, not the recognition label.

This strategy fits a specific person doing specific things.

It fits you if

- You deploy capital and understand IRR and opportunity cost

- You have a long horizon and can fund consistently

- You can name a use for capital that beats the loan cost

- You want control and flexibility, not the highest day-one number alone

It does not fit you if

- You want a savings account or a 401(k) replacement

- You are early in building wealth and starting from zero

- You need a quick fix for high-interest debt

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you which carrier and design fit your situation. If you are in the second, we will tell you that too.

Book a Discovery Call06 / FlexibilityWhich carrier has the most flexible paid-up additions rider?

Penn Mutual has the most flexible paid-up additions rider of the group, and PUA flexibility is the most underrated metric in this entire comparison. The paid-up additions rider is the engine that drives early cash value, and how it behaves when life does not go to plan is where carriers separate.

Flexibility does not show up in an IRR number. It shows up the year your business has a bad stretch and you cannot fund the rider, or the year you have a windfall and want to backfill what you missed. Some carriers let you catch up. Others give you a flat no.

How the riders actually differ

Penn Mutual leads with anytime payments, a full catch-up provision for a missed prior year, and only a requirement to pay half of one year's maximum within any 5-year rolling period to keep the rider active. OneAmerica ranks second, with anytime payments up to 3x base premium and only a $120 annual minimum, though its funding capacity is lower. Lafayette Life and Pan-American offer strong anytime flexibility with limited or no catch-up.

MassMutual sits at the bottom. Its riders can be all-or-nothing on the policy anniversary, cap you at three payments a year, and cancel the rider if you skip more than two years. That is by design. MassMutual has publicly said it does not want infinite banking business, and an inflexible rider is them backing up what they say. It is a strong carrier with strong financials. It just is not built for this.

Flexibility is the make-or-break you cannot see in a spreadsheet.

"Flexibility does not show up in cash value IRR. IRR shows one or two benefits, but life insurance is multi-beneficial, and life happens. That flexibility can be the make or break.", Caleb Guilliams

The full 10-carrier data, plus the frameworks behind 2,000+ policies.

The And Asset Vault holds the carrier comparison data, the COMDEX scores, the design frameworks, and the calculators we use when we match a carrier to a client. Free, email-gated, no spam.

Open the Vault07 / The numbersHow the carriers actually performed, cashflow vs front-load

The numbers come from real illustrations on all 10 carriers, modeled on a 40-year-old male, one rating above standard non-tobacco, at $50,000 per year. We ran two designs: a cashflow design funded 20 years at level premium, and a front-load design funded heavier in year one. Every carrier has an optimal way to be built, so a single apples-to-apples build flatters some and penalizes others. Treat these as directional, not gospel.

Cashflow design: who leads early, who leads late

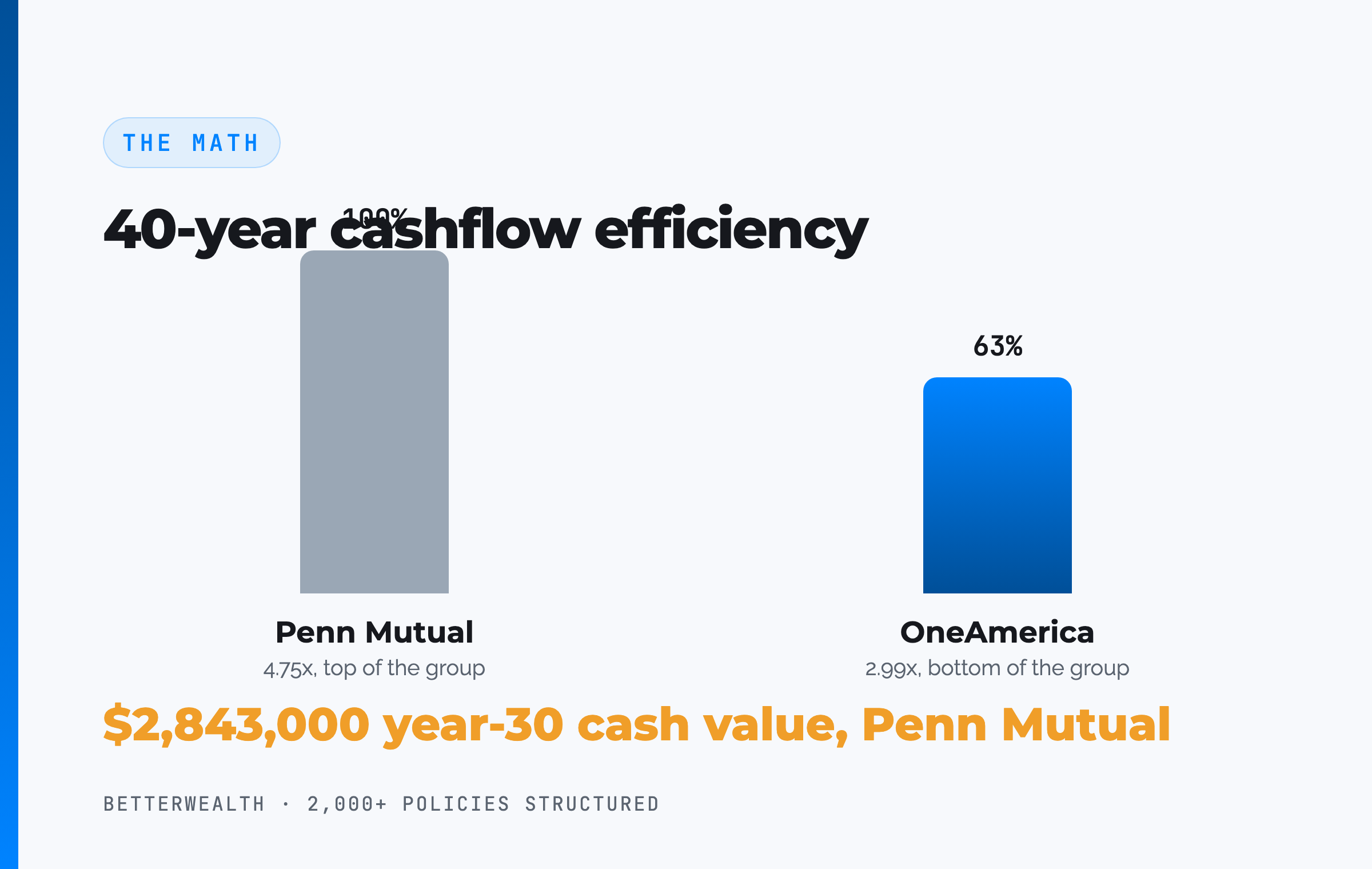

Out of the gate, Foresters posts the highest year-one cash value at $46,716, with Lafayette Life and Pan-American close behind near $45,000, and Ameritas at the low end around $33,000. The picture inverts over time. By year 30, Penn Mutual leads the projections at $2,843,000, with MassMutual the runner-up near $2.6 million and OneAmerica at $2,092,000. Penn Mutual's 40-year efficiency ratio of 4.75x tops the group; OneAmerica's 2.99x sits at the bottom.

Break-even, where total cash value catches total contributions, averages around year five for this group. Lafayette Life is fastest at year four. Ameritas, built outside its optimal funding window here, breaks even at year ten. No carrier is the leader in every column.

Front-load design: early access changes the order

On a front-load, Foresters again leads year one at over 94% first-year cash value, while Penn Mutual lands last at about $82,000, because front-loading is not what Penn is built for. Lafayette Life is the standout: number two in year one, then green through year ten, which is why it is a go-to front-load carrier. Long term, Penn Mutual still wins the efficiency ratio at 5.74x, with MassMutual and New York Life close behind.

The lesson across both designs is consistent. If you want to borrow in the first few years, weight early cash value and look at Guardian, Lafayette Life, Pan-American, or Foresters. If you are building for decades, Penn Mutual's long-term efficiency is hard to beat. Lafayette Life is often the best of both worlds.

For the carrier-by-carrier deep dives behind these summary numbers, the full IBC series breaks down each company one at a time:

08 / Where people get this wrongThe marketing traps to ignore

The biggest mistake people make is choosing a carrier on the single metric a marketer told them to care about. The dividend rate, the recognition type, the brand name. Each one gets oversold, and each one leads to the wrong company for the wrong reason.

The "only work with non-direct recognition carriers" rule is a sales pitch, not a principle. The "you pay yourself interest" line is factually wrong, because the interest goes to the carrier. The "highest dividend means best policy" claim ignores that the dividend is gross. And the "this one company is the best for everyone" promise ignores your state, your health, and your funding style. We have rescued policies where the client could no longer fund the PUA rider and had no idea, because no one explained the product they bought.

Complexity is its own trap. The larger the carrier, the more complex the products tend to be, and complexity means more ways to get the design wrong. MassMutual scores highest on product complexity in this group; Pan-American is the simplest. Complexity is not bad if you and your agent understand it. It is dangerous when you do not.

The recognition type, the dividend rate, the brand. Each gets oversold as the deciding factor. None of them is. Policy design, funding discipline, and early cash value decide the outcome.

09 / The fitWho is each carrier right for?

Each carrier is right for a specific profile, and matching the two is the whole job. The long-term wealth builder who will fund for decades and values flexibility leans Penn Mutual. The person who needs maximum cash in years one through five for an imminent deal leans Guardian, Lafayette Life, Pan-American, or Foresters. The buyer who prioritizes brand and balance-sheet safety above all leans Guardian or New York Life.

The variable-income earner who needs to skip and catch up leans Penn Mutual or OneAmerica. The New York resident is limited to Ameritas, Guardian, MassMutual, New York Life, or Security Mutual, and among those Guardian and New York Life are the strongest. And the buyer who wants strong performance with reasonable early access and good support lands on Penn Mutual or Lafayette Life. If you cannot name an activity that beats the loan cost, no carrier on this list is right for you yet.

10 / Head to headThe category winners, side by side

Compared across the four dimensions that decide a capital strategy, the carriers sort into clear category leaders rather than one overall champion. The table below is the liftable summary: who leads, the headline figure, and the tradeoff that comes with it.

| Category | Leader | Headline figure | The tradeoff |

|---|---|---|---|

| Long-term performance | Penn Mutual | ~4.75x cashflow efficiency at 40 yrs; ~8 to 21% ahead over 20 to 30 yrs | Early cash value runs 7 to 12% lower in years 1 to 5 |

| Early cash value | Guardian / Lafayette Life | Front-load year one in the mid-80s to mid-90s % of premium | Long-term growth can lag the performance leaders |

| Financial strength | Guardian / New York Life | COMDEX 100, AM Best A++ | Less competitive products for max cash value designs |

| PUA flexibility | Penn Mutual / OneAmerica | Anytime payments, full catch-up; 50% of max within any 5 yrs | OneAmerica has lower funding capacity; base stays 25%+ of premium |

Long-term performance. Penn Mutual's projected internal rate of return leads the group, with a 4.75x cashflow efficiency ratio at 40 years and a $2,843,000 year-30 cash value projection in the model. The cost of that result is lower early cash value, which is why Penn fits a long horizon, not a first-year borrow.

Early cash value. Guardian and Lafayette Life lead on front-load year-one access, with Pan-American and Foresters close. Lafayette Life is the rare carrier that holds competitive cash value long term too, breaking even by year four in the cashflow model, which makes it a frequent pick for clients who want both.

Strength and flexibility. Guardian and New York Life sit at COMDEX 100 for the safety-first buyer. Penn Mutual and OneAmerica lead flexibility for the variable-income funder. The right combination depends on your goal, not on any single carrier being best at everything.

A composite: matching the carrier to the goal

Consider a 43-year-old business owner, preferred non-tobacco, funding $50,000 per year. This is a representative composite, not a single named client. The point is how the goal, not the brand, picks the carrier.

Because his horizon is 25-plus years and he plans to take policy income later, we model Penn Mutual for its long-term efficiency and its 0% loan-to-dividend spread from year 11 on. Through the first three years, cash value trails cumulative contributions, exactly as a healthy policy should. At year five, total cash value crosses total contributions. No earlier. Any illustration showing a year-two break-even is marketing fiction.

In year eight, with roughly $408,000 of accessible cash value, he borrows $215,000 against the policy to fund the down payment on a small rental portfolio. The properties return an estimated 13.8% IRR. The loan cost is illustrative at about 6%, so the spread runs nearly eight points in his favor, and the policy keeps compounding on its full value the entire time. Repayment runs on a 44-month schedule funded by the rental cash flow.

Had his goal been to borrow in year one instead, we would have modeled Lafayette Life or Guardian for the early cash value, and accepted slightly lower long-term efficiency. Same strategy. Different carrier. The goal decided it.

One dollar. Two jobs. That is the And.

The honest 30 minutes about which carrier fits you.

We have structured more than 2,000 policies across all 50 states and we represent every carrier in this guide. On a discovery call, a practitioner looks at your goal, your state, and your funding style, then tells you which carrier and design fit, or whether none do. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQBest company for infinite banking questions

What is the best life insurance company for infinite banking in 2026?

There is no single best company. The best carrier depends on what you value. Penn Mutual leads long-term performance, Guardian and Lafayette Life lead early cash value, Guardian and New York Life lead financial strength, and Penn Mutual leads funding flexibility. All 10 carriers reviewed sit in the top 1 to 2% of US insurers for this strategy.

Which is better for infinite banking, direct or non-direct recognition?

Neither is categorically better. Over a long horizon it comes out in the wash, because carriers price loans so they do not lose. Direct recognition can help in rising-rate and distribution years, and non-direct is simpler and keeps the dividend unchanged when you borrow. Policy design and early cash value matter more than the recognition type.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does the dividend interest rate tell you which company is best?

No. The dividend interest rate is the most overhyped metric in the industry. It is a gross figure before the carrier subtracts mortality and expense charges. MassMutual posts the highest 2026 dividend rate at 6.6% yet does not have the best long-term cash value growth. Internal rate of return on cash value is a far more accurate comparison.

Which life insurance companies work in New York for infinite banking?

Five of the carriers reviewed sell their core whole life products in New York: Ameritas, Guardian, MassMutual, New York Life, and Security Mutual. Penn Mutual, Lafayette Life, OneAmerica, and Pan-American do not operate in New York. Among the New York options, Guardian and New York Life offer the strongest combination of strength and flexibility.

Which carrier has the most flexible paid-up additions rider?

Penn Mutual ranks first for paid-up additions flexibility, with anytime payments, a full catch-up provision, and only a requirement to pay half of one year's maximum within any 5-year period. OneAmerica ranks second. MassMutual is the least flexible of the carriers reviewed.

Why does Penn Mutual rank highest for long-term performance?

Penn Mutual posts the strongest projected internal rate of return among the carriers reviewed, roughly 8 to 21% higher than much of the competition over 20 to 30 years. Its tradeoff is lower early cash value, running 7 to 12% below some competitors in the first five years, so it fits a long capital horizon. Cash value grows at the dividend net of mortality and expense charges, not the gross rate.

Which carrier is best for early cash value?

For early cash value, Guardian, Lafayette Life, Pan-American, and Foresters lead. On a front-load design, first-year cash value can reach the low to mid 90% range. Lafayette Life is often the best of both worlds, with strong early access and competitive long-term growth.

Is MassMutual good for infinite banking?

MassMutual is a strong, highly rated carrier, but it has publicly stated it does not want infinite banking business, and its paid-up additions riders are the least flexible of the group. It fits a disciplined funder who will hit premiums reliably, less so someone who needs to skip and catch up. Penn Mutual is a two-n spelling; MassMutual is direct in some legacy products but non-direct on its current line.

Does the carrier matter more than the policy design?

No. Among top mutual carriers, the policy design, your funding strategy, and your discipline in using the policy matter far more than which company you choose. The carrier choice refines the result. It does not determine success.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- AM Best, financial strength ratings for all carriers referenced, including Penn Mutual's 98-consecutive-year A-or-better record.

- LIMRA, life insurance industry data, including lapse and persistency benchmarks.

- Society of Actuaries, mortality and policy-performance data used to estimate undisclosed dividend rates.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

Built the 10-carrier comparison data, ran the illustrations, and walks the cash value and death benefit numbers on screen in the source video. He specializes in policy structure and carrier comparisons across the IBC series.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on which carrier fits your goal, book a discovery call. We will tell you which one, or whether none fits yet.

1. "What Is Infinite Banking?" (Pillar / Blog 1) → wire from the framework section (H2 02) anchor "The And Asset."

2. "Penn Mutual Infinite Banking 2026" (Carrier Review) → wire from the first mention of Penn Mutual in the intro and from H2 07.

3. "How to Structure an And Asset Policy" (Blog 8) → wire from the design discussion (H2 02 / H2 08).

4. "Infinite Banking Pros and Cons" (Blog 10) → wire from the tradeoffs and "where people get this wrong" section (H2 08).

5. Pillar (Blog 1) must appear on every blog — included above.