.png)

To structure an infinite banking policy for cash value, minimize the base death benefit, maximize the paid-up additions rider, and use a term rider to add PUA room without triggering a MEC. The base/PUA split is the single decision that determines early cash value. Most agents design the opposite, because commission is paid on base premium.

The carrier you choose is the question everyone obsesses over, and it is the wrong place to start. Two whole life policies issued by the same top mutual carrier, funded with the same premium, can produce cash value figures that differ by tens of thousands of dollars in the first five years. The variable is not the company. It is how the policy was built.

Policy design, specifically the base-to-PUA split, decides whether a whole life policy becomes a capital base or an expensive death benefit, and the default design serves the agent's commission before it serves the client. This is the single largest gap between how these policies should be structured and how they usually are.

Agent commission is paid on base premium. Paid-up additions pay the agent a fraction of that, sometimes nothing. So the structure that pays an agent the most is a high-base, low-PUA policy, which is also the structure that leaves a client with the least early cash value. The incentive and the client's interest point in opposite directions, and almost nobody says it out loud.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we have re-engineered plenty of policies that were built backwards. This guide covers the four design levers that actually matter: the base/PUA split, the paid-up additions rider, the term rider and the MEC limit, and where carrier choice fits. It also covers what to do if you already own a policy that was built for the wrong person.

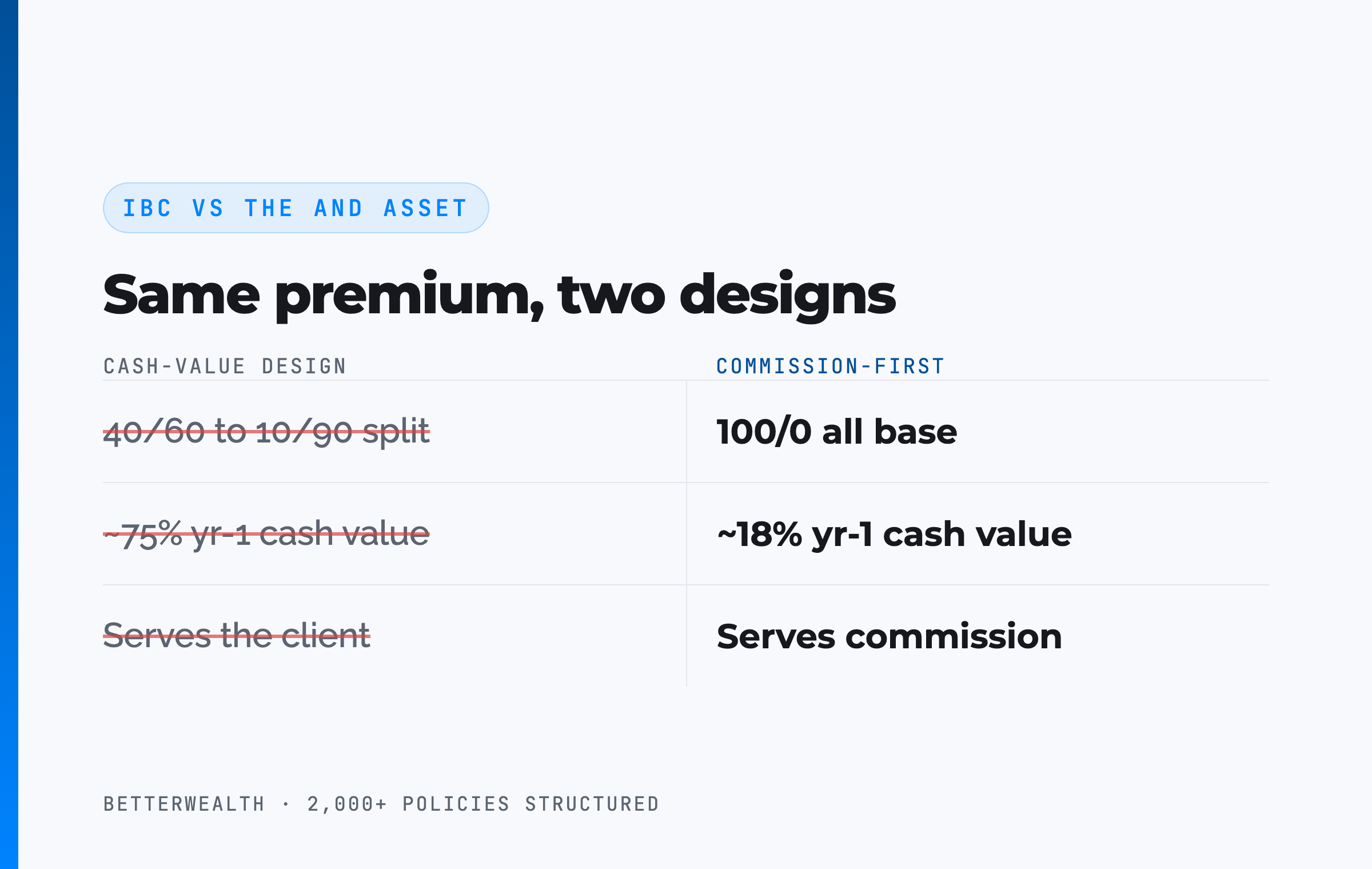

- The base/PUA split is the design decision that drives early cash value; a cash-value design runs roughly 40/60 to 10/90.

- Agent commission is paid on base premium, so a high-base policy pays the agent more and the client less.

- The paid-up additions rider is the engine; almost every PUA dollar becomes cash value immediately.

- A term rider creates room for more PUA premium without crossing the MEC limit and its tax consequences.

- Design matters more than the carrier or the dividend rate for whether a policy functions as a capital base.

- The And Asset rule still governs: only borrow when the deployed return clears the carrier's loan cost.

01 / The problemWhy two identical premiums produce different policies

The same premium can build two very different policies because the death benefit and the funding mix are design choices, not fixed features of the product. When an agent runs an illustration, they decide how much of your premium buys base whole life and how much buys paid-up additions. That single decision moves your first-year cash value by a wide margin.

A base-heavy policy buys a large death benefit and a small amount of early cash value. A PUA-heavy policy buys the smallest death benefit the IRS will permit for your premium and pushes the rest into cash value that is accessible almost immediately. Same carrier, same dollars, opposite outcomes.

This is why we say carrier choice is the least important variable in the decision. A worse carrier with a better design will out-perform a better carrier with a commission-first design for the purpose of building accessible capital. If you want the mechanics of how that cash value actually accumulates inside the contract, we walk through it in detail in how whole life insurance cash value works.

The carrier is the question everyone asks first. The design is the question that actually decides the outcome, and almost nobody asks it.

02 / The hidden leverWhy do most agents structure for commission instead of cash value?

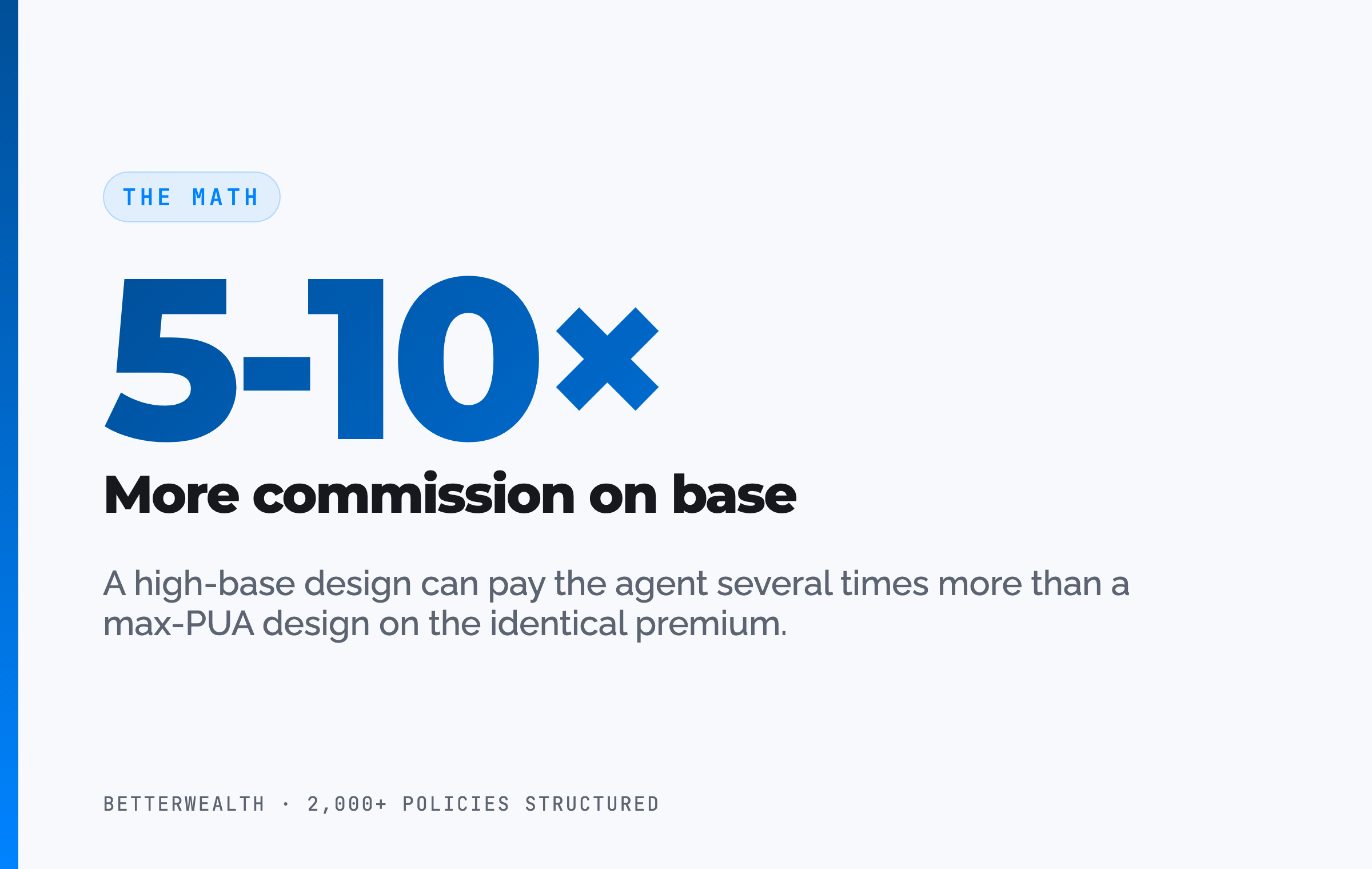

Most agents structure for commission because commission is paid on base premium and barely paid, if at all, on paid-up additions. The math is simple and the incentive is direct. A high-base policy can pay an agent several times more in the first year than a max-PUA design on the identical premium. The structure that pays the agent best is the structure that hands the client the least early cash value.

This is not a conspiracy. Most agents were trained to sell death benefit, were never taught cash-value design, and run the default illustration the carrier's software produces. The default is base-heavy. The result is the same whether the motive is incentive or ignorance: the client gets a policy built for the wrong job.

How to spot a commission-first design

A few tells show up fast. The illustration carries a large death benefit relative to the premium. There is little or no paid-up additions rider. The first-year cash value is a small fraction of what you paid in. And the agent leads with the death benefit and the dividend rate rather than the early cash value and the loan provisions. If your year-one cash value is 10 to 20% of premium, you are looking at a base-heavy policy. A cash-value design lands far higher.

Follow the incentive. It explains the design.

Marketers have ruined how this strategy gets explained. The same people then sell a structure that quietly pays them five times more and you tens of thousands less.

03 / The frameworkWhat are you actually designing the policy to do?

You are designing the policy to function as a capital base you can borrow against while it keeps compounding, which is a different goal than buying death benefit. That goal changes every design decision. Once the job is "build accessible capital," the base/PUA split, the riders, and the carrier all get chosen to serve it. The discipline layered on top is what we call The And Asset, our framework for using a properly structured policy as a capital base.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. The reason this matters for design is that a policy built for casual spending and a policy built as a disciplined capital base are structured for the same thing: maximum accessible cash value, minimum drag. The discipline decides whether the structure pays off.

Many IBC marketers say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what you deploy the capital into while the policy keeps compounding net of mortality and expense charges.

The math has to work. Every time.

04 / How it worksHow to structure the policy, step by step

A cash-value policy gets built in five decisions, and the order matters. The product is a participating whole life policy from a mutual carrier, designed for maximum cash value rather than maximum death benefit. Here is the sequence we use.

- Set the death benefit to the MEC floor. Size the base death benefit as low as the carrier and the IRS allow for your target premium. A smaller death benefit means lower insurance cost, which means more of every dollar can become cash value. The base premium is the floor, not the goal.

- Maximize the paid-up additions rider. Load the PUA rider as heavily as the design permits. This is the engine. Almost every PUA dollar converts to cash value immediately, which is what produces accessible capital in the early years.

- Add a term rider to buy MEC room. A term insurance rider raises the death benefit just enough to let you pour more PUA premium in without crossing the MEC limit. The term burns off over time. It is scaffolding, not the structure.

- Choose the carrier for mechanics, not the dividend. Select a mutual carrier on loan provisions, PUA flexibility, financial strength, and recognition type. The dividend rate is one input and the least decisive one.

- Fund consistently and let it capitalize. Fund on a level or front-load schedule and let the early years build. A healthy policy reaches break-even around year 5, then cash value begins to exceed cumulative contributions.

A well-designed policy reaches the capitalization point, where each premium dollar adds more than a dollar of cash value, around year three. Break-even, where total cash value catches total contributions, typically lands at year five for a healthy individual. Any illustration that shows break-even in year one or two is fiction.

The base/PUA split, written plainly

The split is the ratio of base premium to paid-up additions premium, and it is always written with a slash. A 40/60 split sends 40% of premium to base and 60% to PUAs. A 10/90 split is more aggressive on cash value. A 100/0 policy is all base, which is the commission-first default. The right split depends on the carrier, your health, and how much you can fund, but the direction is constant: more to PUAs, more early cash value. If you want the deeper mechanics of the rider itself, the paid-up additions explainer covers how each PUA dollar behaves inside the contract.

The split is the strategy. The carrier is a detail.

A cash-value design fits a specific person doing specific things.

It fits you if

- You want a capital base, not a death benefit

- You can fund consistently for 10+ years

- You can name a use for capital that beats the loan cost

- You want to see the commission and the design, not just the pitch

It does not fit you if

- You are early in building wealth and need cash flow elsewhere

- You want a savings account, not a life insurance strategy

- You cannot identify a productive use for borrowed dollars

- You want the largest possible death benefit for the lowest premium

If you are in the first column, a 30-minute conversation will show you the design and the commission side by side. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The engineWhy the paid-up additions rider does the heavy lifting

The paid-up additions rider is what turns a slow-building death benefit into a fast-building capital base. A PUA is a small chunk of fully paid-up whole life insurance you buy on top of the base policy. Because it is paid-up, almost the entire dollar becomes cash value right away, and it carries its own death benefit and earns dividends. Stack enough of them and the early cash value climbs to a useful level years before a base-only policy would.

A base-premium dollar in year one is mostly consumed by the cost of insurance and the carrier's acquisition expense. A PUA dollar is mostly cash value. That contrast is the entire reason design matters. The flexibility of the rider also matters: better carriers let you fund the PUA in varying amounts within IRS limits, so the policy can flex with a business owner's uneven cash flow.

PUAs are the engine. Base is the chassis.

A whole life policy without a heavy PUA rider is just a whole life policy. The rider is the difference between a death benefit and a capital base.

06 / The guardrailWhat is a MEC, and why does it shape the design?

A Modified Endowment Contract is a life insurance policy funded faster than IRS limits allow, and crossing that line costs you the tax treatment that makes this strategy work. Once a policy becomes a MEC, loans and withdrawals are taxed like a retirement account distribution, with last-in-first-out ordering and a possible penalty before 59½. The favorable access disappears.

Good design funds the policy right up to the edge of the MEC limit without crossing it, because that is where cash value is maximized while the tax treatment stays intact. The term rider exists to widen that edge. By adding death benefit, the term rider raises the MEC limit, which lets you pour in more PUA premium before you hit the line. The term is temporary by design and falls away as the paid-up additions take over the death benefit.

The tax framework here is real and worth stating precisely. Section 7702 defined the tax treatment of cash value in 1984, and the MEC rules arrived in 1988 under TAMRA. These are guardrails, not loopholes. A policy designed to the limit and held inside it keeps policy loans out of taxable income.

Fund to the line. Never over it.

07 / The mathDoes the design pay off only if the deployment beats the loan cost?

A well-structured policy creates the capacity to borrow cheaply, but the structure pays off only when the deployed return clears the carrier's loan cost. Design and discipline are two separate things, and the cleanest policy in the world loses money if you borrow against it to buy something that earns less than the loan rate.

Here is the test. You borrow at the carrier's loan rate. The policy keeps compounding on its full cash value, net of mortality and expense charges, even while the loan is outstanding. Your deployed capital earns its own return. If that return is higher than the loan cost, the dollar has done two jobs and you are ahead on the spread. If it is lower, you have borrowed money to lose money slowly. Loan rates vary by carrier and rate environment. At the time of writing many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify, not a constant.

If the deal does not clear the loan rate, do not borrow.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the design frameworks and calculators we use to compare a commission-first illustration against a cash-value design, line by line. Free, email-gated, no spam.

Open the Vault08 / The tradeoffsThe honest cost of a cash-value design

A cash-value design has real tradeoffs, and pretending it does not is how agents lose trust. Here they are, plainly.

First, less death benefit per premium dollar. If your primary goal is the largest possible payout for your family at the lowest cost, term insurance does that job better, and we will say so. Second, you still do not break even on day one. Even a perfect design trails cumulative contributions through the first few years, with break-even at year five or later for a healthy individual. Anyone promising faster is selling. Third, it requires consistent funding. A policy built to be funded heavily for a decade and then under-funded will not perform as illustrated. Fourth, the cheaper commission means some agents will not build it this way, so finding the right design can take more effort than accepting the default.

Against those costs sits the payoff: accessible capital that compounds uninterrupted while you borrow against it, with tax treatment you keep as long as you stay inside the MEC limit. The early-cash-value gap and the lower death benefit are the price of admission for that.

Lower death benefit. Higher early cash value. That is the trade.

This is not for everyone. If maximum death benefit at minimum cost is your goal, buy term and skip the rest of this article.

09 / The fixCan you repair a policy that was built backwards?

Sometimes you can repair a commission-first policy, and sometimes the better move is to start clean. It depends on how old the policy is. If it is recent, the design may carry an existing PUA rider you can begin maximizing, or a 1035 exchange into a properly designed policy may make sense and preserve the tax basis. If you are several years in, the heavy first-year commission cost is already sunk, and abandoning the policy can mean walking away from value that is finally starting to compound.

The decision turns on your specific numbers: the current cash value, the surrender charges, the rider room, and your health today versus when you bought it. This is exactly the kind of question worth a second opinion from someone whose commission does not depend on the answer.

10 / Head to headCommission-first design versus a cash-value design

Compared side by side, a commission-first policy and a cash-value policy can carry the same premium and the same carrier while behaving like two different products. The table sets them against each other on the four design dimensions that decide whether a policy works as a capital base.

| Design dimension | Cash-value design (The And Asset) | Commission-first design (default) |

|---|---|---|

| Base/PUA split | Roughly 40/60 to 10/90, weighted to paid-up additions | Close to 100/0, all base premium |

| Death benefit | Set to the MEC floor for the premium | Large relative to premium |

| Year-1 cash value | A high share of premium, accessible early | A small fraction of premium |

| Who it serves first | The client building a capital base | The agent's first-year commission |

The split. Everything flows from the base/PUA ratio. A design weighted to paid-up additions converts most of each dollar to cash value early. An all-base design buys death benefit the client may not need and starves the cash value.

The death benefit. Setting the death benefit to the MEC floor minimizes insurance cost. A commission-first design does the reverse, because more base means more death benefit and more commission, not more capital for you.

Who it serves. The clearest test is the first-year cash value. A cash-value design hands you a high share of your premium back as accessible capital. A commission-first design hands the agent a larger check and you a smaller balance.

A composite: same premium, two designs

Consider a 43-year-old business owner, preferred non-tobacco, funding $52,000 per year. This is a representative composite, not a single named client, and it mirrors a pattern we see often when someone brings us an existing policy for a second opinion.

Same carrier, same premium, same health class. The commission-first illustration ran roughly 100/0 and returned about $9,400 of accessible cash value in year one. The cash-value design ran near 15/85 with a term rider holding it under the MEC limit, and returned roughly $38,900 in year one, more than four times as much accessible capital from the identical dollars.

Through the first three years, even the cash-value design trails cumulative contributions, exactly as a real policy should. By year three each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions at $268,300 against $260,000 paid in. No earlier.

In year six, with accessible cash value built up, the owner borrows $94,500 against the policy to fund a revenue-producing project that returns an estimated 13.6% IRR against an illustrative loan cost near 6%. The spread works in the owner's favor by more than seven points, the policy keeps compounding on its full value the entire time, and repayment runs on a 29-month schedule funded by the project's own cash flow.

One dollar. Two jobs. That is the And.

See your design and the commission side by side.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner shows you what a cash-value design looks like for your numbers and what the default would have cost you. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on policy structure.

Book a Discovery CallFAQPolicy structure questions

How do you structure a whole life policy for infinite banking?

You structure it for cash value by minimizing the base death benefit, maximizing the paid-up additions rider, and using a term rider to add PUA room without triggering a MEC. The base/PUA split is the single design decision that determines early cash value. A commission-first design does the opposite, loading base premium and leaving the client with little early cash value.

What is a good base to PUA ratio for infinite banking?

A cash-value-focused design typically runs a base/PUA split somewhere between 40/60 and 10/90, depending on the carrier and your funding ability. More premium flowing to paid-up additions means higher early cash value. A 100/0 all-base policy is a commission-first design, not a capital base.

Why do agents structure policies for commission instead of cash value?

Agent commission is paid on base premium, not on paid-up additions. A high-base, low-PUA policy pays the agent several times more while leaving the client with far less first-year cash value. The structure that pays the agent best is usually the structure that serves the client worst, whether the cause is incentive or training.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

What is a paid-up additions rider?

A paid-up additions rider lets you buy small chunks of fully paid-up whole life insurance on top of the base policy. Almost all of a PUA dollar becomes cash value immediately, which is why a heavy PUA rider is the engine behind early cash value in a well-designed policy.

What is a MEC and why does it matter for policy design?

A Modified Endowment Contract is a life insurance policy funded faster than IRS limits allow. Once a policy becomes a MEC, loans and withdrawals lose their favorable tax treatment and are taxed on a last-in-first-out basis. Good design pushes premium to the edge of the MEC limit without crossing it, which is why a term rider is often used to create room.

Does the carrier or the design matter more?

Design matters more than carrier. Two policies from the same top mutual carrier can differ by tens of thousands of dollars in early cash value purely based on the base/PUA split. The dividend rate is one input and the least decisive one for whether a policy will function as a capital base.

How long until a properly structured policy breaks even?

A well-designed, cash-value-focused policy typically reaches break-even, where total cash value catches total contributions, around year 5 for a healthy individual. The capitalization point, where each premium dollar adds more than a dollar of cash value, arrives around year 3. Any illustration showing break-even in year one or two is marketing fiction.

Can I fix a poorly structured policy I already own?

Sometimes. If the policy is recent, an existing PUA rider can be maximized or a 1035 exchange into a better-designed policy may make sense and preserve the tax basis. If you are years in, the early commission cost is already sunk, and the better move depends on your current cash value, surrender charges, and health. This is worth a second opinion from someone whose commission does not depend on the answer.

What is a term rider doing in a cash-value policy?

A term rider adds temporary death benefit, which raises the MEC limit and lets you fund more paid-up additions without crossing it. The term burns off over time as the paid-up additions take over the death benefit. It is scaffolding that lets you maximize early cash value while staying inside the IRS limits.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the 1984 provision defining the tax treatment of life insurance cash value.

- IRC Section 7702A (Cornell Law), the Modified Endowment Contract rules added under TAMRA in 1988.

- LIMRA, life insurance industry data, including persistency and product design benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, and we have re-engineered plenty that were built for the agent instead of the client. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether your policy is designed right, book a discovery call. We will tell you if it is not.