.png)

Whole life vs term insurance is not a contest between a good product and a bad one. Term is cheaper and right for a temporary death-benefit need. Whole life costs more and earns it only as a capital base you actually borrow against. Different jobs, different buyers.

The whole life versus term debate is usually staged as a morality play. One side calls whole life a ripoff sold by commissioned agents. The other side calls term a temporary fix that leaves you with nothing. Both sides are arguing about the wrong thing, because they are comparing two products that were built to do two different jobs.

Term and whole life are not competitors. They are different tools, and the right answer depends entirely on which problem you are trying to solve. Term insures a temporary obligation cheaply. A properly structured whole life policy builds a capital base you can use while you are alive. Forcing them into a single bracket and asking which one wins is how most people end up with the wrong policy and a story about why insurance is a scam.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and we sell term constantly. We tell people to buy term when term is the right answer, which is more often than the permanent-insurance industry likes to admit. This piece covers what each product actually does, when term clearly wins, when whole life clearly wins, the false binary that wrecks the comparison, and where our framework, The And Asset, fits into the decision.

- Term and whole life solve different problems, so "which is better" depends on whether your need is temporary or you intend to deploy capital.

- Term wins on cost and is the honest answer for a young family covering a mortgage and income over a fixed window.

- Whole life only earns its higher premium if you borrow against it for a return that beats the carrier's loan cost.

- Most online comparisons rig the matchup by pitting term against a death-benefit-heavy policy, not a cash-value design.

- Owning both is often the honest answer: term for the big temporary need, whole life as the capital base.

- Whole life cash value compounds net of mortality and expense charges, and break-even lands at year five or later, not year one.

01 / The setupWhat problem are you actually solving?

The whole life versus term question only has an answer once you name the problem, and almost nobody starts there. People start with the product. They read that term is "smart money" or that whole life is "becoming your own banker," then they shop for the product that matches the slogan they liked best.

There are two distinct problems, and they have two distinct answers. The first problem is temporary risk: if you died this year, who is left holding a mortgage, college tuition, or a decade of lost income? That is an insurance problem, and term is the efficient tool for it. The second problem is capital: you have money you want compounding, protected, and accessible to deploy without liquidating the asset. That is a capital structure problem, and a properly designed whole life policy is one tool for it.

Confusing the two is the original sin of this debate. You cannot buy a cheap product to solve an expensive problem, and you should not buy an expensive product to solve a cheap one.

The question is not "term or whole life." The question is "what job am I hiring this dollar to do," and then you pick the product that does that job best.

02 / Term, fairly statedWhat does term life insurance actually do well?

Term life insurance does one thing extremely well: it buys the largest possible death benefit for the lowest possible premium over a fixed period. That is the whole product, and it is a good product. We refuse to straw-man it, because the case for term is real.

You choose a term length, usually 10, 20, or 30 years, and a face amount. You pay a level premium for that window. If you die inside the window, your beneficiaries get the death benefit. If you outlive the window, the coverage ends and you walk away. There is no cash value, no loan feature, and no asset. There is a contract that pays if a specific risk shows up in a specific timeframe.

Where term clearly wins

Term wins anywhere the need is temporary and the budget is real. A 34-year-old with two kids, a thirty-year mortgage, and a single income does not need a capital base. They need to know that if they die, the house is paid and the family is funded until the kids are grown. A large term policy does that for the price of a few dinners out per month. Buying whole life instead, on a stretched budget, would mean buying far less coverage than the family actually needs. That is the trade that hurts people.

Big temporary need, tight budget. Buy term.

Term also has an underrated feature most buyers ignore: convertibility. Many term policies let you convert to permanent coverage later with no new medical exam. If your health changes or your financial picture grows into a life insurance strategy, that rider protects your insurability. A convertible term policy is a starting point, not a dead end.

03 / Whole life, fairly statedWhat does whole life insurance actually do well?

Whole life insurance does something term cannot: it builds a cash value that compounds for your entire life and gives you a permanent death benefit that never expires. The premium is higher because you are funding both the insurance and the asset at the same time.

A whole life policy has guaranteed cash value growth, plus dividends when the carrier declares them. That cash value compounds at the dividend rate net of mortality and expense charges, which is the figure that actually grows inside the policy, not the gross dividend rate an agent might quote. You can borrow against the cash value through a policy loan, and the policy keeps compounding on its full value while the loan is outstanding. The death benefit pays whenever you die, not only if you die inside a window.

None of that makes whole life automatically worth the cost. It makes whole life a different category of tool. The question of whether whole life is worth the higher premium turns entirely on what you do with the capital it builds, which is the part marketers skip.

Whole life is not a good investment and it was never supposed to be one. It is a capital base. Comparing its growth to the stock market is comparing a foundation to a skyscraper.

04 / The frameworkWhere does The And Asset change the comparison?

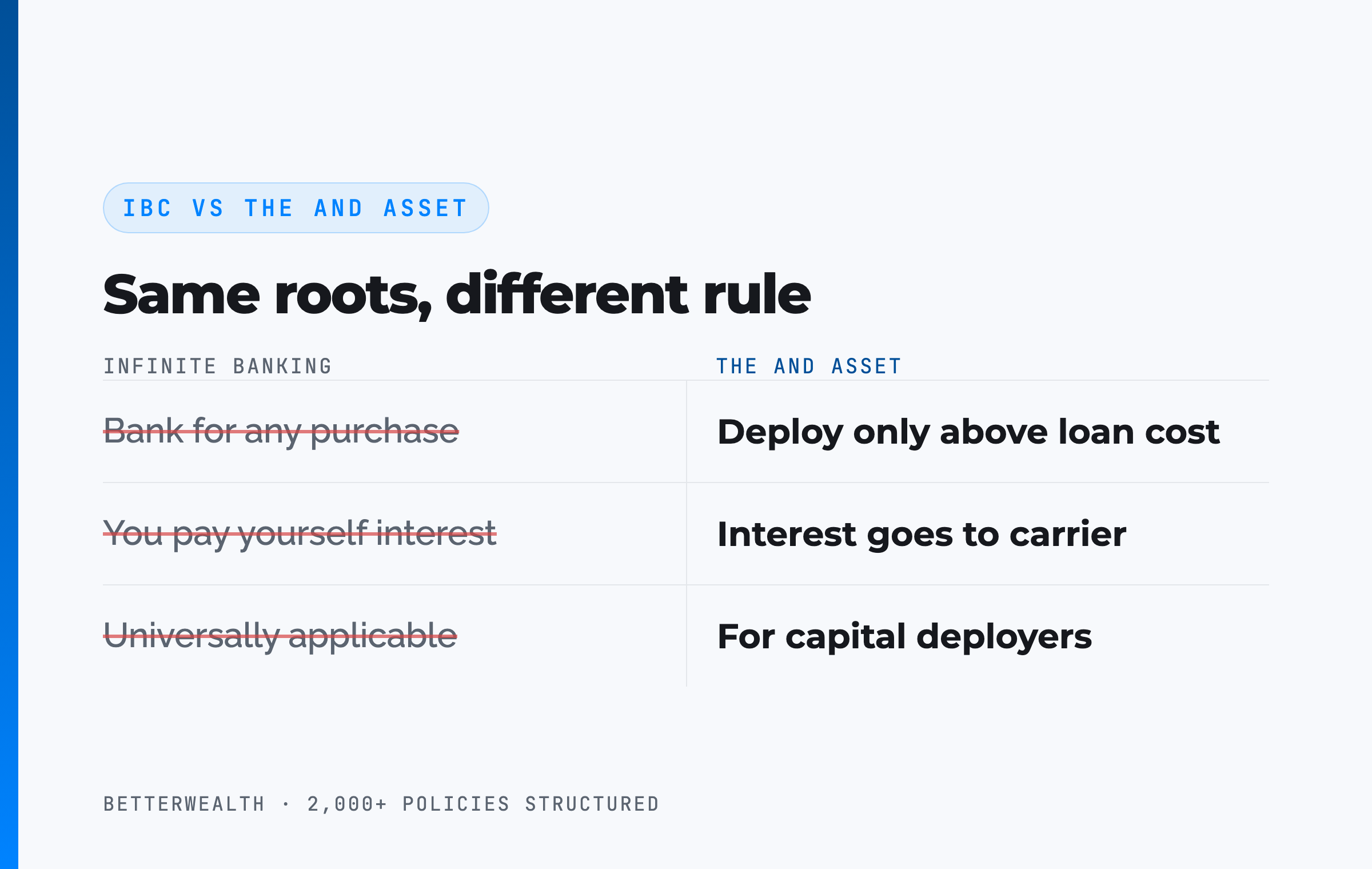

The And Asset changes the comparison by adding a discipline that decides whether whole life is worth owning at all. Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

Infinite banking says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers also say you are paying yourself interest. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy compounds uninterrupted.

This is exactly where the term comparison gets clarified. If you will never borrow against the policy to deploy capital into something that beats the loan cost, then whole life is not an And Asset for you. It is just an expensive death benefit, and term would have served you better. The framework is the filter.

If you cannot name the use, you do not need the policy.

The honest version of this strategy is for entrepreneurs and value creators, not savers. The And Asset shares roots with IBC but operates on different principles: the dollars have to beat the loan rate, or you do not borrow.

Term, whole life, or both? It depends on a specific person.

Whole life may fit if

- You have a long capital horizon (10+ years)

- You already deploy capital and understand IRR

- You can name a use that beats the loan cost

- You have maxed conventional tax-advantaged accounts

Term is the honest answer if

- Your need is temporary (mortgage, young kids)

- Your budget is tight and coverage is the priority

- You want a savings account, not a capital base

- You cannot identify a productive use for borrowed dollars

If you are not sure which column you are in, a 30-minute conversation will tell you honestly. We sell term, whole life, and the combination, so we have no reason to push you toward the expensive answer.

Book a Discovery Call05 / The false binaryWhy is "buy term and invest the difference" usually a rigged comparison?

Buy term and invest the difference is good advice for a specific person, and a rigged comparison for everyone else. The slogan assumes two things that frequently are not true: that you will actually invest the difference every month for thirty years, and that the whole life policy in the comparison was designed for cash value in the first place.

Start with the behavior. The math of investing the difference only works if the difference gets invested, consistently, through every market drop and every tempting purchase, for decades. Most people spend it. That is not a moral failing, it is human behavior, and a comparison that assumes flawless discipline is comparing a spreadsheet to real life.

Now the product. Most "whole life loses" comparisons quietly use a death-benefit-heavy policy with a small or nonexistent paid-up additions rider, which is the worst possible design for cash value. Comparing that to term plus an index fund is a setup. A policy structured for The And Asset, with a heavy paid-up additions rider and minimized base premium, behaves nothing like the strawman in those charts.

The comparison that is actually fair

A fair comparison puts term plus a disciplined, actually-executed investment plan against a properly structured whole life policy used as a capital base. Run on those terms, the answer stops being universal. For a disciplined investor with no use for borrowable, protected capital, term plus investing often wins outright. For an entrepreneur who will deploy capital into deals that beat the loan cost, the And Asset adds something term plus investing cannot replicate: the same dollar working in two places at once.

Compare the real product to the real behavior, or do not compare at all.

06 / The mathDoes whole life's extra cost ever clear the bar?

Whole life's extra cost clears the bar only when the capital it builds gets deployed at a return above the carrier's loan cost. This is the entire test, and it is the same test we apply to every And Asset decision. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6 percent range, but treat the specific number as a variable to verify with the carrier, not a constant.

Here is the structure. You pay the higher whole life premium. The cash value compounds, net of internal costs, including on the portion you have borrowed against. You borrow at the carrier's loan rate and deploy that capital into an activity. If the activity returns more than the loan cost, you are ahead on the spread and the policy has done two jobs with one dollar. If it returns less, you have paid a premium for a feature you are using to lose money slowly. In that case, term would have been the cheaper and more honest choice.

This is why the term-versus-whole-life answer is not a number you can look up. It is a function of what you will actually do with capital. The product cannot supply the discipline. You do.

No deployment, no spread. No spread, no reason to pay the premium.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to decide between term, whole life, and the combination, including the loan-cost math that determines whether a policy earns its premium. Free, email-gated, no spam.

Open the Vault07 / The both answerWhy owning term and whole life together is often the honest play

For many entrepreneurs and high-income earners, the right answer is not term or whole life but a deliberate combination of both. This is the option the slogans never mention, because it does not make a clean argument for either side.

The logic is simple. Your large temporary obligation, the mortgage and the income-replacement years, gets covered by term, which is the cheapest way to insure it. Separately, a smaller whole life policy gets structured as a capital base you fund consistently and borrow against over decades. The term handles the risk. The whole life handles the capital. Neither product is asked to do the job it does poorly.

We structure this combination often. A business owner might carry a large convertible term policy for pure protection while funding a whole life policy at a level they can sustain for thirty years. As the term need fades, the children grow up, the mortgage gets paid, the capital base remains and keeps compounding. The convertibility rider on the term means part of it can become permanent later if the situation warrants.

This is not a binary. The most defensible plan we build often uses term for the risk you want to cover cheaply and whole life for the capital you intend to use.

08 / The fitWho should buy which, plainly stated

Term is right for the person with a temporary, definable obligation and a budget that makes coverage the priority. Young families, new mortgage holders, anyone replacing income over a fixed window, and anyone who cannot yet name a productive use for borrowed capital. For that person, term is the smart, honest answer, and a properly sized term policy beats an undersized whole life policy every time.

Whole life is right for the entrepreneur, business owner, or high-income earner with a long horizon who will actually deploy capital. The value creator who funds consistently for a decade or more, who has maxed conventional tax-advantaged accounts, who understands IRR and opportunity cost, and who can identify activities that beat the loan cost. For that person, a properly structured And Asset does a job term cannot.

The combination is right for the person who has both problems at once, which describes a large share of the entrepreneurs we work with. If you cannot name an activity that beats the loan cost, no whole life policy is right for you yet, and that is not an insult. It is the discipline working as intended.

09 / Head to headTerm vs whole life vs the And Asset, side by side

Compared directly, term and whole life diverge on cost, duration, cash value, and what the policy can do while you are alive. The table sets pure term against a death-benefit-heavy whole life policy and against a whole life policy structured as an And Asset, because those last two are not the same thing.

| Dimension | Term Life | Whole Life (death-benefit design) | Whole Life as an And Asset |

|---|---|---|---|

| Cost | Lowest premium for the largest death benefit | High premium, most of it funding the death benefit | High premium, structured to maximize cash value |

| Duration | Fixed window (10-30 yrs), then expires | Permanent, lasts your whole life | Permanent, lasts your whole life |

| Cash value | None | Slow to build, small relative to premium | Heavy PUA rider builds cash value toward year-5 break-even |

| Living use | None; pure protection | Borrowable, but the design fights you | Borrow against full value while it compounds; deploy above loan cost |

Cost. Term is the clear winner on price, and that is not a weakness, it is the point. If coverage is the goal and the budget is finite, term buys more protection per dollar than any permanent product.

Cash value and living use. A death-benefit-heavy whole life policy and an And Asset policy share a category but behave differently. The base/PUA split is the design decision that separates a policy you can actually use from one that mostly funds a death benefit. Most online comparisons use the former and pretend it represents the latter.

The honest read. Term beats both whole life columns for anyone whose need is temporary or who will not deploy capital. The And Asset column only pulls ahead for the disciplined capital deployer, and only when the deployed return clears the loan cost.

A composite: the founder who needed both

Consider a 39-year-old business owner, preferred non-tobacco, married with two young children and a $612,000 mortgage. This is a representative composite, not a single named client.

The temporary problem was obvious: if he died, the family needed the mortgage gone and income replaced for years. We covered that with a large, inexpensive convertible term policy. Stretching to cover that need with whole life would have meant buying a fraction of the coverage the family actually required. That would have been the wrong trade.

Separately, he funded a whole life policy designed with a heavy paid-up additions rider. Through the first three years, cash value trailed cumulative contributions, exactly as a real policy should. Break-even arrived at year five, with cash value crossing total contributions, not before. Any illustration showing a year-two break-even is marketing fiction.

In year seven, with accessible cash value of roughly $214,500, he borrowed $138,000 against the policy to fund inventory for a second location. The expansion returned an estimated 13.6 percent IRR against an illustrative loan cost near 6 percent, so the spread worked in his favor by more than seven points. The policy kept compounding on its full value the entire time, and repayment ran on a 44-month schedule funded by the new location's cash flow. The term covered the risk. The whole life did the capital work. Neither was asked to do the other's job.

One dollar. Two jobs. That is the And.

The honest 30 minutes about which one fits you.

We have structured more than 2,000 policies across all 50 states, term and whole life both. On a discovery call, a practitioner looks at your specific situation and tells you whether term, a properly designed whole life policy, the combination, or none of it belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQWhole life vs term insurance questions

Is whole life or term insurance better?

Neither is better in the abstract. Term is better when you need a large death benefit for a fixed window at the lowest cost. Whole life is better when you want a capital base you can borrow against while living and will actually deploy that capital. They solve different problems, so the right answer depends on which problem you have.

Why is whole life insurance so much more expensive than term?

Whole life costs more because you are funding two things at once: a death benefit that never expires and a cash value that compounds net of mortality and expense charges. Term funds only a temporary death benefit, so for the same coverage the premium can be roughly ten times lower in the early years.

Is buy term and invest the difference a good strategy?

Buy term and invest the difference works well for disciplined investors who actually invest the difference every month for decades and never need that money to be liquid and protected at the same time. It fails for people who spend the difference, or who need uninterrupted compounding and capital they can borrow against without liquidating the asset.

Does term life insurance ever pay out?

Most term policies never pay a death benefit because the insured outlives the level term period or lets the policy lapse. Industry persistency data shows only a small percentage of term policies result in a claim. That is by design: term is built to cover a temporary need cheaply, not to guarantee a payout.

Can you convert term insurance to whole life?

Many term policies include a conversion rider that lets you convert to permanent coverage with no new medical exam, usually before a stated age or within a set number of years. This protects insurability if your health changes. It is one reason a convertible term policy can be a reasonable starting point rather than a dead end.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Is whole life insurance a good investment?

Whole life is not an investment and comparing its cash value growth to the stock market is the wrong frame. It is a capital structure tool. Its value comes from uninterrupted compounding, tax treatment, and the ability to borrow against it for an activity that beats the loan cost. Judged as a standalone return, it underperforms equities. Judged as a capital base, it does a job equities cannot.

When does term insurance make more sense than whole life?

Term makes more sense when your need is temporary, your budget is tight, or you cannot identify a productive use for borrowed capital. A young family covering a thirty-year mortgage and income replacement is the textbook case. Term insures that obligation for a fraction of the cost of permanent coverage.

Can you own both whole life and term insurance?

Yes, and for many entrepreneurs that combination is the honest answer. Term covers the large temporary obligation cheaply while a smaller, properly structured whole life policy builds the capital base. This stacks the two jobs each product does best rather than forcing one product to do both.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of permanent life insurance cash value and loans.

- LIMRA, life insurance ownership, persistency, and lapse benchmarks.

- NAIC, consumer guidance on term versus permanent life insurance.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, term and whole life both. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether term, whole life, or the combination fits your plan, book a discovery call. We will tell you if neither does.