.png)

Overfunded whole life insurance is a policy designed to hold the base premium low and pour extra money into a paid-up additions rider, so cash value builds far faster than a standard policy. You fund it as close to the IRS MEC limit as possible without crossing into a Modified Endowment Contract.

The word "overfunded" sounds like a mistake, as if you accidentally paid too much. It is the opposite. An overfunded policy is the only version of whole life insurance that functions as a capital tool, and a standard, fully-loaded death-benefit policy is the version most people get sold and later regret. The difference is not the carrier or the dividend rate. It is how the premium is split.

Overfunding is the single design decision that determines whether a whole life policy builds usable cash value or just buys an expensive death benefit. Most agents quote the dividend rate and skip the split entirely, because the split is where their commission shrinks. The smaller the base premium and the larger the paid-up additions, the less the agent earns and the more cash value you keep.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and almost every one is overfunded to a deliberate ratio. This piece covers what overfunding actually is, how paid-up additions outrun base premium, where the MEC limit defined by IRC Section 7702A caps you, what "maximum overfunded" really means, and the real cash value timeline (no break-even in year one, no matter what the illustration shows). We will also tell you when overfunding is the wrong move.

- Overfunding means a low base premium and a heavily loaded paid-up additions rider, often a 40/60 split or richer toward PUAs.

- A paid-up additions dollar is almost entirely cash value on day one; a base premium dollar is mostly death benefit cost early on.

- The MEC limit (IRC Section 7702A) is the ceiling: fund past it and policy loans become taxable income.

- "Maximum overfunded" means funded right up to the seven-pay MEC line and not a dollar over it.

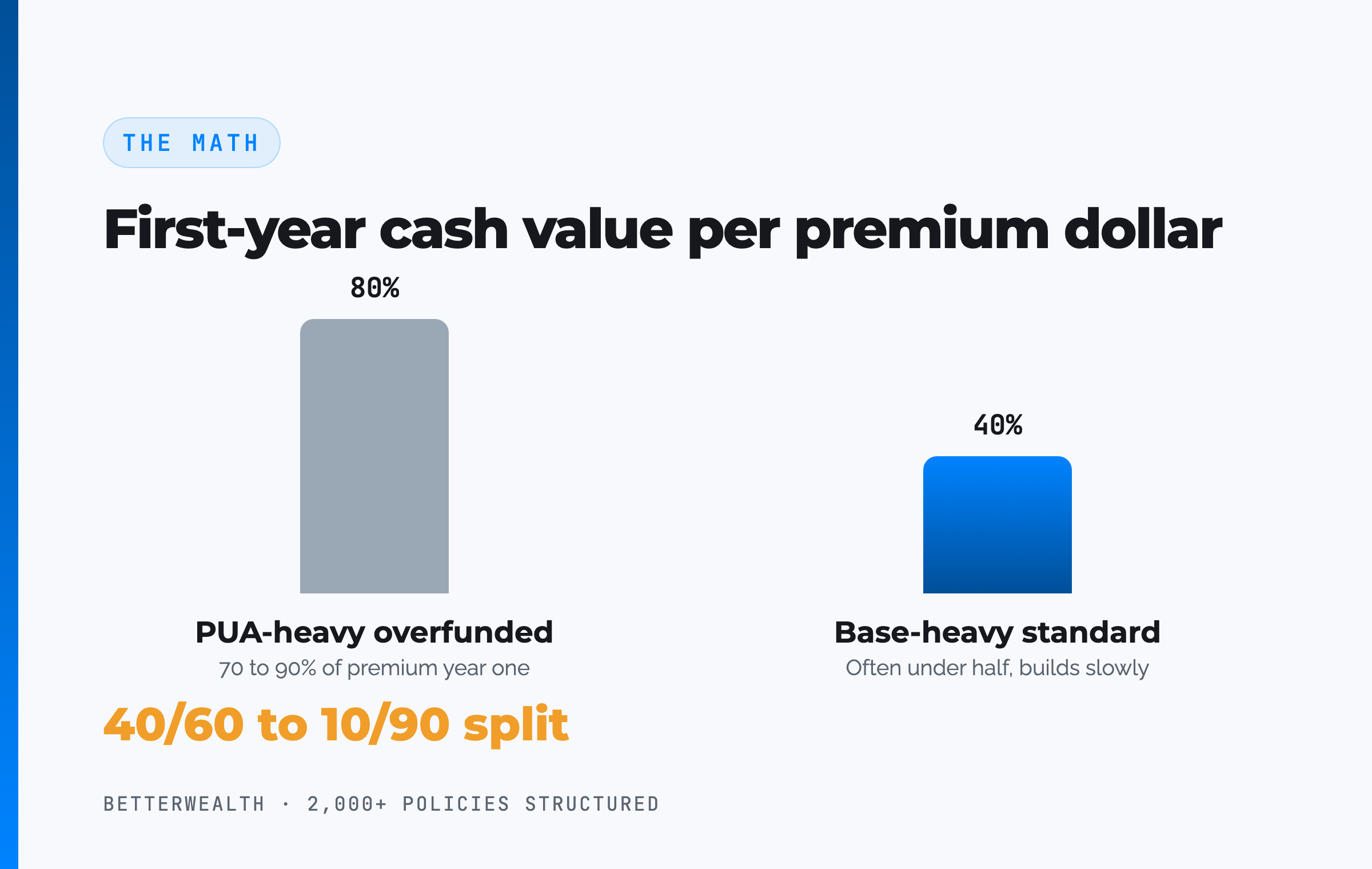

- Cash value grows net of mortality and expense charges and does not exceed contributions before year 4; break-even lands at year 5 or later.

- An overfunded policy is a capital base, not an investment; The And Asset rule still governs when you borrow.

01 / The problemWhy a standard whole life policy disappoints buyers

A standard whole life policy disappoints because it is built to maximize death benefit, which front-loads the cost and starves early cash value. The buyer was told whole life "builds cash value," funded it for three years, looked at the statement, and found less cash than they had paid in. They concluded whole life is a scam. They were half right. The product was sold wrong, not designed wrong.

The structural issue is the premium split. In a death-benefit-first policy, nearly every dollar goes to base premium, which carries the bulk of the policy's internal cost in the early years. Cash value crawls. Overfunding flips the ratio. It minimizes the base and routes the rest into paid-up additions, which is where this article spends most of its time.

Marketers have ruined how this strategy gets explained. A whole life policy that disappoints almost always failed at the design stage, on the base-to-PUA split, not at the carrier.

02 / Base vs PUAWhat is the difference between base premium and paid-up additions?

Base premium buys the permanent death benefit and carries most of the policy's cost in the early years; paid-up additions are extra deposits that each buy a small, fully paid-up block of insurance that is almost entirely cash value immediately. That is the whole mechanism in one sentence. Overfunding is the act of shrinking the first and enlarging the second.

Think of the base premium as the chassis and the paid-up additions rider as the engine. The chassis is required (you cannot have a policy without a base), but it does not move you forward fast. The PUA rider is what accelerates cash value, because a dollar of PUA buys a chunk of paid-up insurance whose cash value shows up almost in full, right away, rather than being consumed by first-year acquisition costs.

How the split is written

The split is written as a ratio, base to PUA. A 40/60 design sends 40% of target premium to base and 60% to paid-up additions. A 10/90 design pushes as much as possible into PUAs. The richer the PUA side, the more first-year cash value, up to the point where IRS rules stop you. Overfunding is not one setting. It is a dial, and where you set it depends on how much cash value you want working early versus how much death benefit you need.

This is also where overfunding accelerates the broader mechanism. If you want the full picture of how that cash value is built, grows net of mortality and expense charges, and is eventually accessed, we walk through it in how whole life insurance cash value works. Overfunding is the lever that speeds every stage of that timeline.

The base is the chassis. The PUA rider is the engine.

If an agent will not show you the base-to-PUA split on your illustration, you are not looking at an overfunded policy. You are looking at a commission.

03 / The MEC limitWhat is a MEC, and why does it cap overfunding?

A Modified Endowment Contract (MEC) is a life insurance policy funded faster than federal law allows, and it is the hard ceiling on how much you can overfund. The limit comes from IRC Section 7702A, which applies a "seven-pay test": roughly, the cumulative premium in the first seven years cannot exceed what would pay the policy up in seven level annual payments. Cross that line and the policy is a MEC for life.

The consequence is tax. A non-MEC policy lets you take policy loans that are not treated as taxable income. A MEC reverses the accounting. Distributions come out gains-first and are taxed as ordinary income, plus a 10% federal penalty on the gain if you are under 59 and a half. The death benefit stays income-tax-free, but the living-benefit access that makes overfunding useful is gone.

So overfunding has a natural governor built into the tax code. You want to pour in as much PUA as possible, because that maximizes early cash value, but the seven-pay limit stops you before the policy stops behaving like life insurance. Good design funds right up to that line.

Overfunding is not "more is always better." Past the MEC limit, every extra dollar costs you the tax treatment you bought the policy for in the first place.

04 / Maximum overfundedWhat does "maximum overfunded" actually mean?

Maximum overfunded means the policy is funded right up to the MEC limit and not a dollar over it, so you get the most cash value per premium dollar while keeping tax-free policy loans. It is the sweet spot, not the extreme. The phrase confuses people because "maximum" sounds like "as much as humanly possible." In policy design it means "as much as the IRS allows before the penalty box."

Reaching maximum overfunded is a design exercise, and the steps matter in order. Here is the sequence we use.

- Minimize the base premium. Set the base as low as the carrier permits for the death benefit you need. The base is the cost of the chassis, not the engine.

- Maximize the paid-up additions rider. Load the PUA rider as heavily as the carrier and the IRS allow. Each PUA dollar buys paid-up insurance that is almost all cash value on day one.

- Stay under the MEC limit. Keep total premium under the seven-pay limit. The designer runs the policy against Section 7702A so you fund up to the line and not over it. Maximum overfunded is exactly this line.

- Fund consistently. Use a level or front-loaded schedule. The optimal horizon for an overfunded design runs 7 to 25 years, long enough for compounding to do its work.

- Let cash value capitalize, then deploy. Allow the early years to capitalize. Break-even arrives at year 5 or later. After that, you borrow against the cash value only for an activity that out-earns the carrier's loan cost.

One nuance most buyers never hear: when you overfund heavily, the carrier sometimes has to increase the death benefit to keep the policy under the MEC limit. A bigger death benefit adds internal cost, which slightly lowers the long-term internal rate of return. That is the trade for funding aggressively. It is a real cost, and it is small relative to the liquidity you gain.

Maximum overfunded is a line, not a pile.

Overfunding fits a specific person doing specific things.

It fits you if

- You have a 7+ year capital horizon

- You want liquidity and control over day-one death benefit

- You can name a use for capital that beats the loan cost

- You will fund consistently for a decade or more

It does not fit you if

- You are early in building wealth and cash is tight

- You want a savings account, not a life insurance strategy

- You need the largest possible death benefit per dollar

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you what overfunded design fits your situation. If you are in the second, we will tell you that too.

Book a Discovery Call05 / The frameworkOverfunding is the structure. The And Asset is the discipline.

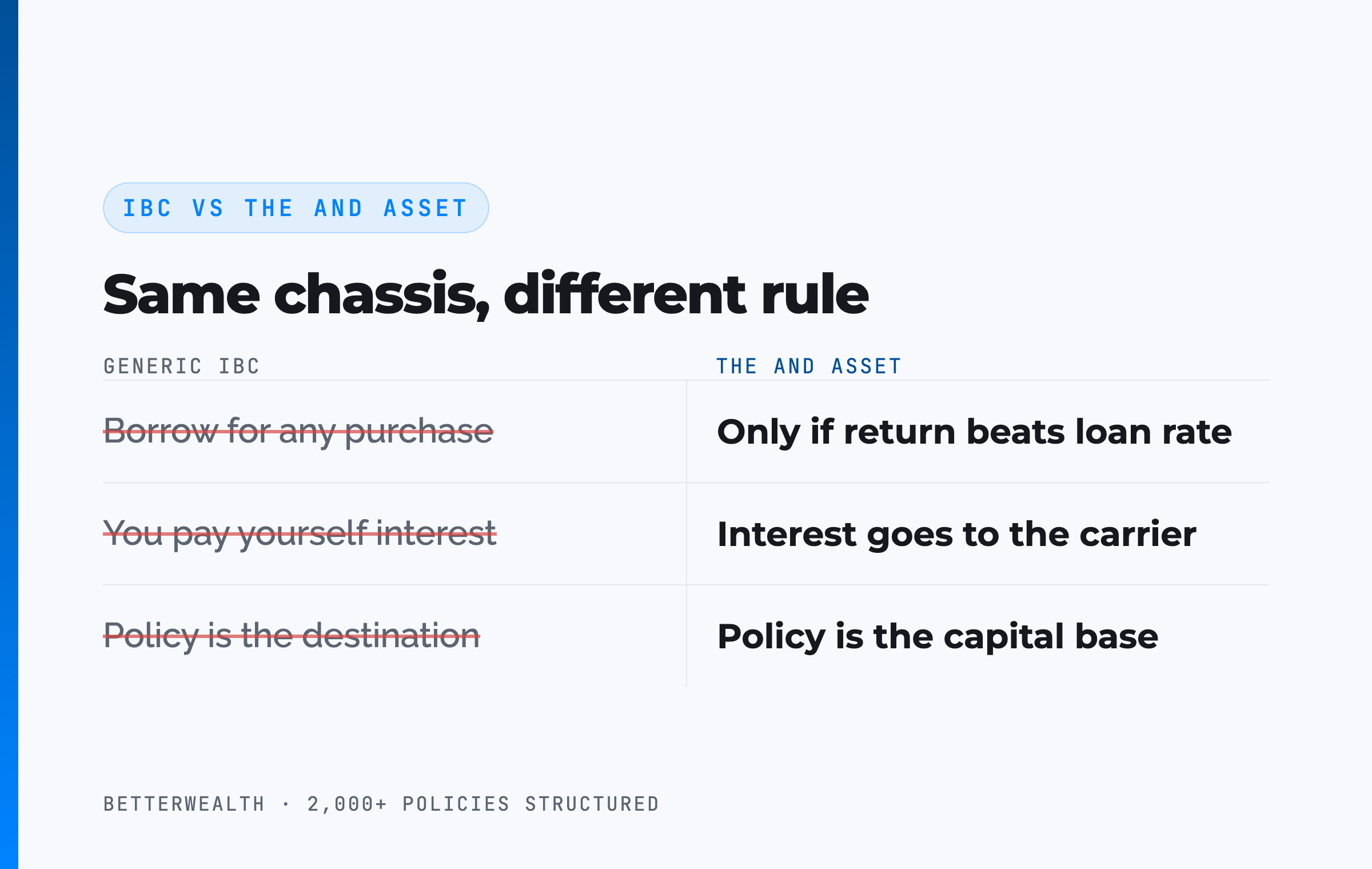

Overfunding builds the capital base. What you do with that capital is where the value is created or destroyed, and that is what we call The And Asset. Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker, and an overfunded policy is the chassis his concept requires. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers say you are paying yourself interest when you repay the loan. You are not. The interest goes to the insurance company. Your return is what the deployed capital earns elsewhere while the policy keeps compounding net of its internal charges.

The distinction matters most for an overfunded policy, because overfunding hands you a large, accessible pool of cash early. The temptation to borrow against it for anything is real. The discipline is the whole strategy. It is built on Nash's foundation but operates on different principles.

An overfunded policy with no plan for the capital is just a slow, expensive savings account. The structure does not create the value. The deployment does.

06 / The mathDoes the return clear the carrier's loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or you should not borrow against the policy. This is the entire test, and it does not change because the policy is overfunded. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with the carrier, not a constant.

Here is the structure of the decision. You borrow at the carrier's loan rate. The policy keeps compounding on its full cash value, including the borrowed portion, net of mortality and expense charges. Your deployed capital earns its own return. If that return is higher than the loan cost, you are ahead on the spread, and the same dollar has done two jobs. If it is lower, you have borrowed money to lose money slowly. Overfunding gives you more dollars to deploy. It does not change whether deploying them is smart.

If the deal does not clear the loan rate, do not borrow.

07 / Where people get this wrongThe four mistakes that wreck an overfunded policy

Most overfunded policies that underperform were wrecked by one of four mistakes, and all four are avoidable. None of them are the carrier's fault.

First, too little PUA. A policy sold as "overfunded" with a 70/30 base-heavy split is barely overfunded at all. The cash value lags and the buyer never sees the benefit. Second, accidentally tripping the MEC limit by overpaying, which turns tax-free loans into taxable distributions. Third, expecting day-one break-even and panicking in year two when cash value still trails contributions. Real policies do not break even before year 4, and break-even at year 5 or later is healthy, not broken. Fourth, treating the policy as an investment and comparing its internal rate of return to the S&P 500. That is the wrong comparison. It is a capital tool, judged by liquidity, control, and what you deploy into, not by beating the market.

The carrier is rarely the problem. The design and the discipline are.

Comparing an overfunded policy's IRR to the stock market is a category error. One is a capital base you borrow against. The other is a place you park money and hope.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the design frameworks and calculators we use to set base-to-PUA ratios, test against the MEC limit, and decide how aggressively to overfund. Free, email-gated, no spam.

Open the Vault08 / Benefits and tradeoffsWhat overfunding gives you, and what it costs

Overfunding gives you fast-building, accessible cash value with favorable tax treatment, and it costs you a smaller death benefit per premium dollar plus a slightly lower long-term internal rate of return. Both halves are real, and any explanation that skips the second half is a sales pitch.

On the benefit side: cash value that builds in the first years instead of the second decade, policy loans that are not taxable income under Section 7702, a loan that cannot be called by the carrier, and uninterrupted compounding on the full cash value even while you borrow against it. On the cost side: you buy less death benefit per dollar than a death-benefit-first policy, the heavier PUA load means the carrier may raise the death benefit to dodge the MEC limit (adding internal cost), and the early years still trail your contributions. Overfunding is the right move when you value the capital function. It is the wrong move when you primarily need the largest possible death benefit.

More usable cash early. Slightly less death benefit and IRR. That is the trade.

09 / Head to headOverfunded vs minimally-funded whole life

Compared to a minimally-funded, death-benefit-first whole life policy, an overfunded policy trades maximum death benefit for early liquidity and capital efficiency. The table sets the two designs side by side on the four dimensions that decide whether a policy works as a capital tool.

| Dimension | Overfunded (high PUA) | Minimally funded (base-heavy) |

|---|---|---|

| Base-to-PUA split | Low base, heavy PUA rider (e.g. 40/60 to 10/90) | Mostly base premium, little or no PUA |

| Early cash value | Roughly 70 to 90% of premium in year one; capitalizes fast | Often well under half of premium early; slow to build |

| Death benefit per dollar | Lower per premium dollar; the chassis, not the goal | Higher per premium dollar; the whole point of the design |

| Function | Capital base you borrow against (The And Asset) | Pure protection; weak as a living-benefit tool |

The split. Everything starts with the base-to-PUA ratio. An overfunded design routes the majority of premium into paid-up additions; a minimally funded design barely uses the PUA rider, if at all. This one choice cascades into every other row.

Early cash value. The overfunded policy is built so a dollar in becomes most of a dollar of cash value quickly. The base-heavy policy spends the early years covering acquisition cost, which is exactly why so many buyers feel misled.

Death benefit and function. If your only goal is the largest death benefit per dollar, minimally funded wins, and overfunding is the wrong tool. If you want a capital base you can borrow against and deploy, overfunding is the only design that delivers it.

A composite: the contractor who overfunded to the line

Consider a 43-year-old contractor, preferred non-tobacco, funding an overfunded whole life policy at $47,000 per year on a roughly 25/75 base-to-PUA split, designed to sit just under the MEC limit. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real overfunded policy should. By year three, each premium dollar adds more than a dollar of cash value, because the heavy PUA load has cleared most of the early acquisition cost. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction.

In year six, with roughly $312,000 of accessible cash value, the contractor borrows $156,000 against the policy to buy a used grading machine that lets the crew take on a class of jobs they had been subcontracting out. The added margin returns an estimated 13.6% IRR. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by more than seven points. The policy keeps compounding on its full value the entire time. Repayment runs on a 43-month schedule funded by the machine's own billings.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether overfunding fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your situation and tells you what base-to-PUA split, what funding schedule, and what carrier (or no policy at all) belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQOverfunded whole life insurance questions

What is overfunded whole life insurance?

Overfunded whole life insurance is a policy designed to hold the base premium low and pour extra money into a paid-up additions rider, so cash value builds far faster than a standard policy. You fund it as close to the IRS MEC limit as possible without crossing it, which is what gives it the early liquidity that makes it useful as a capital tool.

What does maximum overfunded mean?

Maximum overfunded means the policy is funded right up to the seven-pay MEC limit set by IRC Section 7702A and not a dollar over it. At that line you get the most cash value per premium dollar while keeping tax-free policy loans. Cross it and the policy becomes a Modified Endowment Contract and loses that tax treatment.

What is the difference between base premium and paid-up additions?

Base premium buys the permanent whole life death benefit and carries most of the policy's internal cost in the early years. Paid-up additions are extra deposits that each buy a small chunk of fully paid-up insurance, and almost all of a PUA dollar becomes cash value immediately. Overfunding means a high PUA-to-base ratio, often 40/60 or richer toward the PUA side.

What is a MEC and why does it matter?

A Modified Endowment Contract (MEC) is a life insurance policy funded faster than IRC Section 7702A allows. Once a policy becomes a MEC, loans and withdrawals are taxed as ordinary income on gains first, plus a 10% penalty before age 59 and a half. Overfunding correctly means funding up to, but never past, the MEC limit.

Does overfunding a policy avoid mortality and expense charges?

No. An overfunded policy still carries mortality and expense charges. Overfunding shrinks the base premium and adds paid-up additions, which means fewer charges relative to the dollars going in, so cash value grows net of those charges more efficiently. The charges do not disappear, and any cash value figure you see is already net of them.

How fast does an overfunded policy build cash value?

An overfunded whole life policy commonly shows first-year cash value of roughly 70 to 90% of premium, depending on design and carrier. Cash value does not exceed cumulative contributions before year 4, and break-even typically lands at year 5 or later for a healthy individual. Any illustration showing year-one or year-two break-even is not realistic.

Is overfunded whole life insurance a good investment?

Overfunded whole life is a capital tool, not a market investment, and comparing its internal rate of return to the stock market is the wrong comparison. Its value is liquidity, control, and tax treatment on a capital base you borrow against. It only creates real value when you deploy borrowed capital into something that out-earns the carrier's loan cost.

Can you overfund a term life policy?

No. Term life insurance has no cash value component and no paid-up additions rider, so there is nothing to overfund. Overfunding applies to permanent cash value policies, primarily participating whole life from a mutual carrier such as Penn Mutual, MassMutual, or Guardian.

How aggressively can you overfund a policy?

You can overfund up to the MEC limit, which in practice supports base-to-PUA splits as rich as roughly 10/90 on many designs. The exact ceiling depends on your age, health, death benefit, and the carrier's product. A designer runs the policy against the seven-pay test to find the most aggressive split that stays a non-MEC.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured, overfunded whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The overfunded policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

- IRC Section 7702A (Cornell Law), the Modified Endowment Contract definition and the seven-pay test that caps overfunding.

- IRC Section 7702 (Cornell Law), the federal definition of life insurance that overfunding operates within.

- Nelson Nash, Becoming Your Own Banker, the origin of using whole life as a personal banking system.

- LIMRA, life insurance industry data, including cash value and persistency benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states, almost all of them overfunded to a deliberate base-to-PUA ratio. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether an overfunded policy fits your plan, book a discovery call. We will tell you if it does not.