.png)

Infinite banking vs a 401(k) is not a winner-take-all choice, because the two tools solve different problems. A 401(k) is a tax-deferred retirement account with restricted access before 59 and a half. The And Asset is a capital base you can borrow against at any age, while it keeps compounding.

Most people frame this as a cage match. Whole life insurance against the 401(k), one strategy left standing. That framing is wrong, and it has cost a lot of entrepreneurs real money in both directions: people who dumped their match-funded 401(k) on the advice of an insurance agent, and people who let a six-figure capital opportunity pass because every dollar they had was locked behind a penalty wall until age 59 and a half.

A 401(k) and a properly structured whole life policy answer two different questions, and treating them as substitutes is how you get the answer wrong. One question is how to defer tax on income you will not touch for decades. The other is how to keep capital accessible and compounding so you can deploy it when an opportunity appears. The first is a retirement question. The second is a capital question.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the entrepreneurs who get the most out of this rarely choose one tool over the other. They capture the employer match, then they build a capital base on top. This piece compares the two on the four dimensions that decide life insurance strategy: access, tax treatment, control, and what we call the spendable-income lens. We will also be precise about how qualified plans actually work, because the loose version of that story is everywhere and it is wrong.

- A 401(k) defers tax and restricts access before 59 and a half; The And Asset keeps capital accessible at any age with no penalty.

- Capture the full employer match before funding any alternative. A match is an immediate return no policy beats early.

- Policy loans are generally not taxable income while the policy stays in force, under IRC Section 7702.

- A 401(k) loan removes money from the market; a policy loan leaves cash value compounding on its full value.

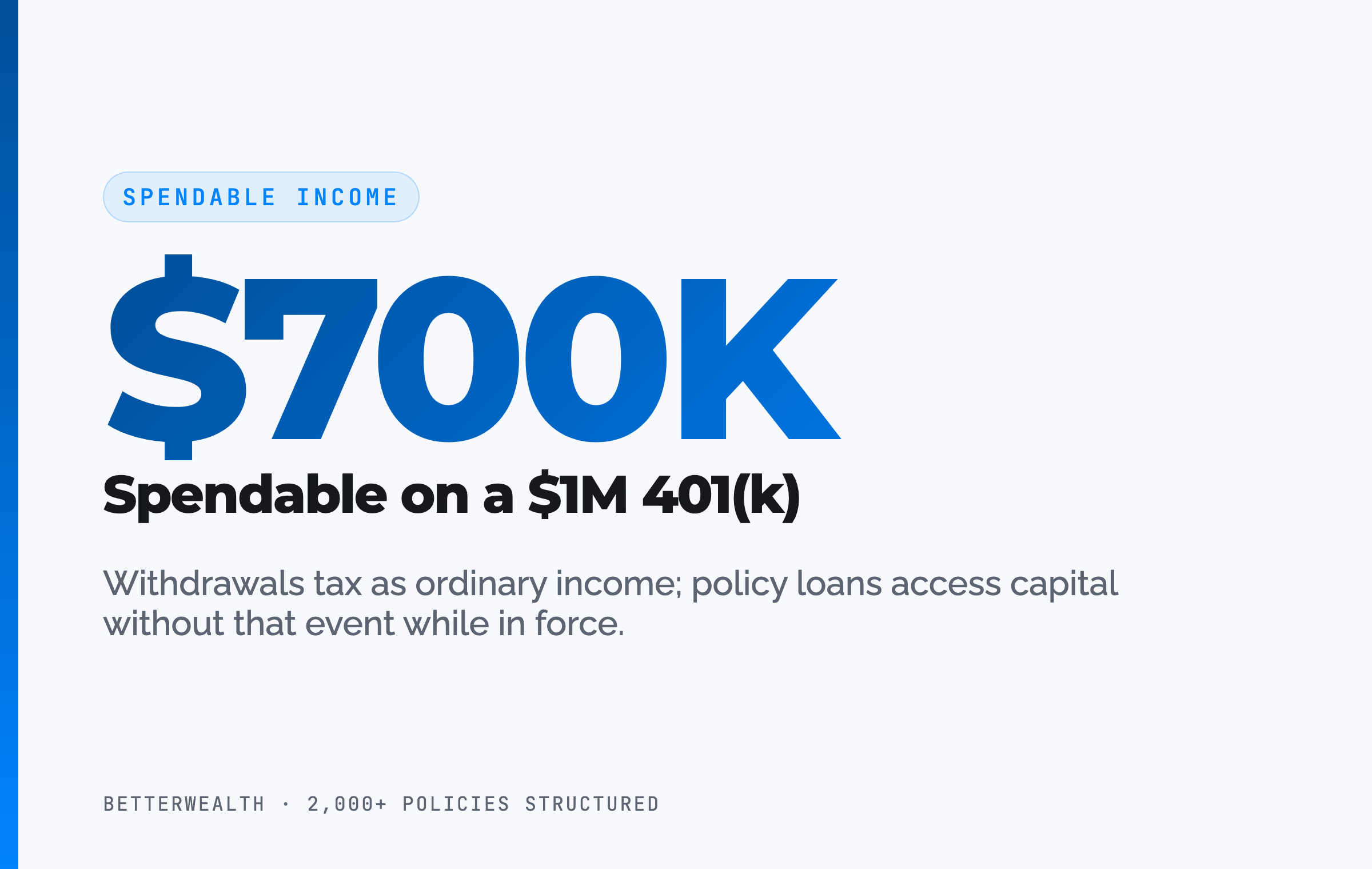

- The spendable-income lens matters: a $1,000,000 traditional 401(k) is not $1,000,000 you can spend.

- The And Asset complements qualified plans. It is not a 401(k) replacement, and we never sell it as one.

01 / The problemWhat conventional planning gets right, and where it leaves a gap

Conventional retirement planning gets the long horizon right and the accessibility question wrong. Maxing a 401(k), capturing the match, and letting it compound for thirty years is sound advice for the retirement-income job. The gap opens when an entrepreneur needs capital before retirement and discovers that the bulk of their net worth sits behind an age wall, a penalty, and a tax bill.

This is the lost-opportunity-cost problem Nelson Nash spent his career describing. You either pay interest to outside lenders to access capital, or you pay the opportunity cost of capital you cannot reach without a penalty. A 401(k) is structurally designed to be hard to touch early. That is a feature for retirement and a constraint for capital deployment. The constraint is the gap.

The problem is not that the 401(k) is bad. The problem is that it was sold to you as your whole strategy, when it was only ever built to do one job.

02 / The frameworkWhat does it mean to use a policy as a capital base instead of a 401(k)?

Using a policy as a capital base means treating a properly structured whole life policy as a pool of accessible capital you borrow against, while a 401(k) treats your contributions as restricted retirement savings you generally cannot touch until 59 and a half. That is the mechanical difference. The discipline layered on top is what we call The And Asset.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds. We respect that foundation. If the broader concept is new to you, our pillar guide on what infinite banking actually is walks through the mechanics before you weigh it against a qualified plan. The And Asset builds on Nash's foundation with one rule his broader teaching does not enforce.

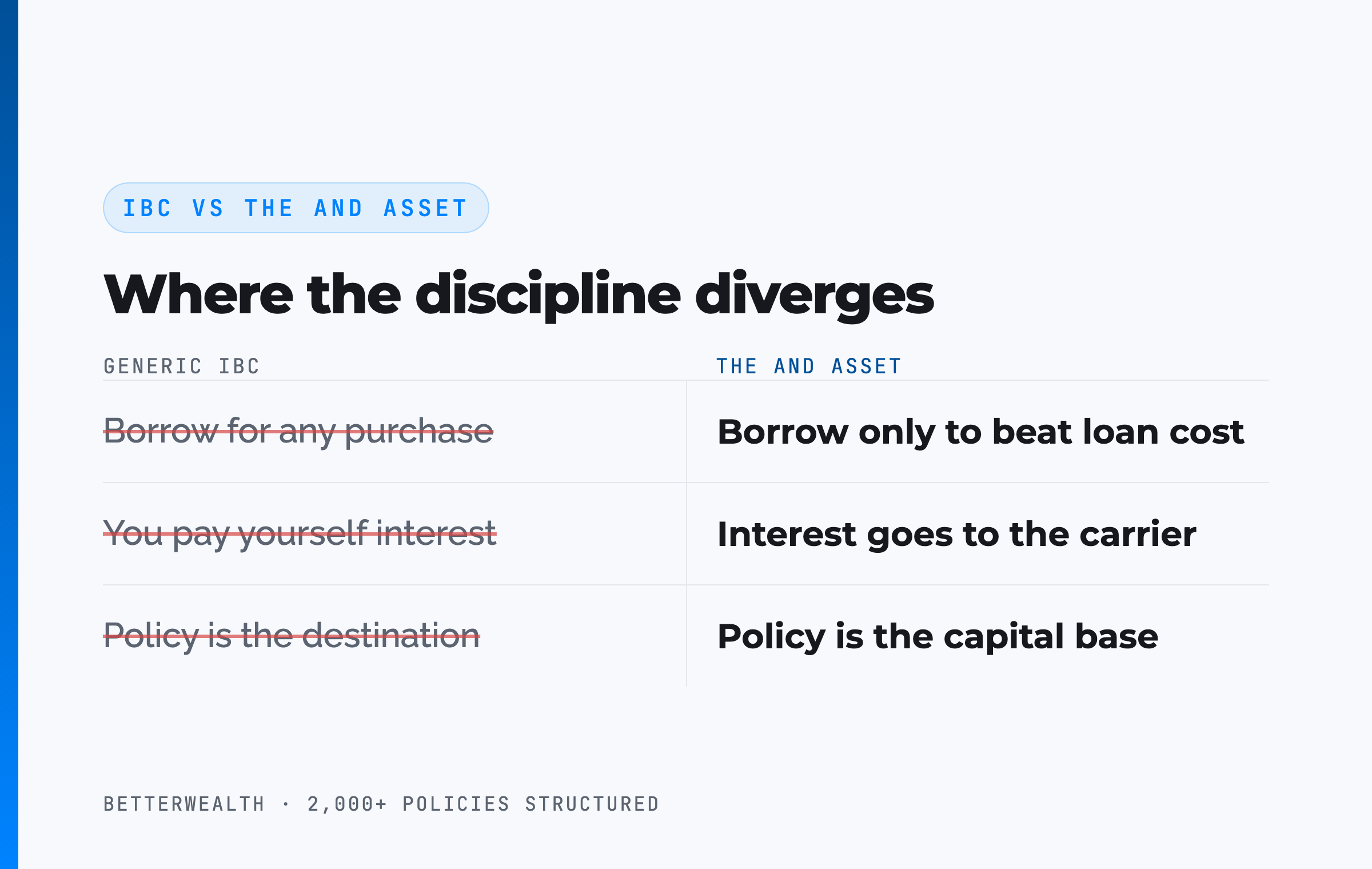

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase, including consumer spending you would have done anyway. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers also say you are paying yourself interest. You are not. The interest goes to the insurance company. Your return is what your deployed capital earns elsewhere while the policy compounds at the dividend rate net of mortality and expense charges.

This distinction matters more in a 401(k) comparison than almost anywhere else, because the lazy pitch is "be your own bank instead of using a 401(k)." That pitch fails the discipline test. The honest version is narrower and harder.

The math has to work. Every time.

Marketers have ruined how this gets explained. "Fire your 401(k) and be your own bank" is a slogan, not a strategy. If you cannot beat the loan cost, do not borrow.

03 / AccessWhy can you reach policy cash value when a 401(k) is locked?

You can reach policy cash value at any age because a policy loan is collateralized by an asset you own, not a withdrawal from a tax-advantaged account governed by distribution rules. A 401(k) restricts access before 59 and a half, and most early withdrawals carry a 10% penalty on top of ordinary income tax. The policy carries neither.

The contrast sharpens when you compare the two loan options directly. A 401(k) loan, where the plan allows one, removes money from the market, caps at the lesser of 50% of your vested balance or $50,000, and typically must be repaid within five years. Leave or lose your job and the outstanding balance often comes due fast, sometimes treated as a taxable distribution if unpaid. Your invested dollars stop compounding the moment you borrow them.

A policy loan works differently. The carrier lends against your cash value as collateral, so the full cash value keeps compounding while the loan is outstanding. There is no fixed repayment schedule the carrier imposes, no five-year clock, and the loan cannot be called. You set the repayment pace. The discipline of repayment is the strategy, and it is on you, not the lender.

A 401(k) loan pulls your money out of the market to lend it to you. A policy loan leaves your capital compounding and lends you someone else's. Same dollar, two very different mechanics.

04 / How it worksHow to weigh The And Asset against a 401(k), step by step

The decision runs in a fixed order, and the order is what keeps people out of trouble. This is the sequence we walk clients through before a single dollar moves.

- Max the match first. Capture the full employer 401(k) match before you consider any alternative. A match is an immediate, guaranteed return no whole life policy can replicate in the early years. Leaving it on the table to fund a policy is a mistake, and we will tell you so.

- Separate retirement from capital. Decide what money is genuinely for retirement income decades out, and what money you want accessible for deployment now. These are different jobs and they call for different tools.

- Structure the policy for cash value. Design an overfunded whole life policy that minimizes base premium and maximizes the paid-up additions rider, building accessible cash value without crossing the MEC limit. Our guide to overfunding a policy covers the design that makes this work.

- Let the early years capitalize. Do not expect day-one liquidity. Cash value trails cumulative contributions through the first few years and reaches break-even at year five or later for a healthy individual. Any illustration showing earlier break-even is fiction.

- Borrow and deploy. Take a policy loan and deploy it only into an activity that beats the carrier's loan cost. Repay from the cash flow that activity generates. The policy compounds on its full value the entire time.

Match first. Capital base second. Always in that order.

This is for a specific person doing specific things with capital.

It fits you if

- You already capture your full employer match

- You deploy capital and understand IRR and opportunity cost

- You want capital accessible before 59 and a half

- You can name a use that beats the loan cost

It does not fit you if

- You would skip the match to fund it

- You want a savings account, not a life insurance strategy

- You are early in building wealth with no capital to deploy

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will show you whether The And Asset adds anything to what you already do. If you are in the second, we will tell you that, too.

Book a Discovery Call05 / Tax treatmentHow does the tax treatment actually compare?

The tax treatment differs in when the tax is paid and whether access creates a taxable event. A traditional 401(k) and traditional IRA defer tax now and tax withdrawals later as ordinary income, at whatever rate applies in the year you withdraw. A Roth defers nothing now and delivers tax-free qualified withdrawals later, if the rules are met. The And Asset sits in a different category: policy loans are generally not taxable income while the policy stays in force, under the tax treatment of life insurance in IRC Section 7702.

That is the structural point people miss. Pulling capital out of a traditional 401(k) before retirement is a taxable distribution, often with a penalty. Borrowing against policy cash value is not a distribution at all, so it does not create the same income-tax event while the contract is in force. The death benefit also passes to beneficiaries income-tax-free in most cases, which a 401(k) balance does not.

There is a constraint, and we state it plainly. A policy that lapses or is surrendered with an outstanding loan can trigger tax on the gain, sometimes a painful one. The tax treatment is a feature of a policy that stays in force and is managed. It is not a magic wand, and "tax-free" only holds inside those guardrails.

Your 401(k) is not "the government's money" and it is not "trapped by the IRS." You own it. It is regulated, access is restricted before 59 and a half, and growth is tax-deferred, not stolen. Precision is the credibility.

06 / ControlWho actually controls the money in each case?

You own a 401(k) balance, but Congress and the IRS control the terms of access, and that is the distinction that matters for life insurance strategy. Contribution limits, the 59-and-a-half age wall, the 10% early-withdrawal penalty, and required minimum distributions starting at age 73 are all set by statute and can change. You decide how much to contribute and how it is invested within the plan menu. You do not decide when you can take it out without penalty, or when you are forced to start taking it out.

With a properly structured policy, you control the timing. You decide when to borrow, how much, what to deploy it into, and the pace of repayment. The carrier cannot call the loan or freeze access the way a bank can freeze a HELOC, which is a comparison we cover in depth in infinite banking vs a HELOC. Control is the entire reason an entrepreneur builds a capital base outside qualified plans in the first place.

The spendable-income lens

The most underused way to compare these tools is to ask what you can actually spend, not what the statement says. A $1,000,000 traditional 401(k) is not $1,000,000 of spendable income. Withdraw it and you owe ordinary income tax at an unknown future rate, so your spendable number might be $700,000, or less if rates rise. Account balances are quoted gross. Spendable income is what survives the tax. Policy loans are accessed without that income-tax event while the policy is in force, which is why the spendable-income lens often flatters the policy in the distribution years even when the raw account balance does not.

Statements lie a little. Spendable income tells the truth.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to model a policy against a 401(k), an IRA, and a taxable account, including the spendable-income math. Free, email-gated, no spam.

Open the Vault07 / The mathDoes the deployed return clear the loan cost?

The return on whatever you deploy borrowed capital into must exceed the carrier's loan cost, or you should not borrow. This is the entire test, and it is the test a 401(k) never makes you run because you usually cannot deploy that capital at all before retirement. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify, not a constant.

Here is the structure. You borrow at the carrier's loan rate. Your policy keeps compounding on its full cash value, net of internal costs, including the borrowed portion. Your deployed capital earns its own return. If that return clears the loan cost, you are ahead on the spread, and the same dollar has done two jobs: it backs the policy and it funds the deal. If the return does not clear the loan cost, you have borrowed money to lose money slowly, and the disciplined answer is not to borrow.

If the deal does not clear the loan rate, leave the capital where it is.

08 / The tradeoffsBenefits and the honest tradeoffs against a 401(k)

The policy's advantages come with tradeoffs that disqualify it for some people, and pretending otherwise is how agents lose trust. Here they are, plainly.

First, no employer match. A 401(k) match is free money the policy cannot replicate, which is why the match always comes first. Second, low early cash value. A policy trails its contributions for the first several years, while a market-invested 401(k) can be up in year one. If you need liquidity immediately, this is a real reason to wait. Third, the policy requires discipline and management. A lapsed policy with a loan can create a tax bill, and the strategy only works if you actually deploy capital into returns above the loan cost. Fourth, no question this is more complex than checking a contribution box on a benefits portal.

Against those tradeoffs sits the structural benefit: capital that is accessible at any age, compounding while borrowed against, with tax treatment and control you keep. The 401(k) wins on simplicity, the match, and early growth. The policy wins on access, control, and the spendable-income picture later. Most of our clients want both, which is the point. For the full unfiltered case in both directions, we wrote an honest assessment of the pros and cons.

If skipping your match is the only way you can fund a policy, you are not ready for a policy. Fix the cash flow first. We have turned people away for exactly this reason.

09 / The fitWho should use both, and who should just keep the 401(k)?

Use both if you are an entrepreneur or high-income earner who already captures the match, deploys capital, and wants accessibility and tax diversification on top of a qualified plan. That profile gets the retirement-income job done inside the 401(k) and the capital job done inside the policy. It is the most common shape we see across 2,000-plus policies, and it is rarely an either-or.

Keep just the 401(k) if you are early in building wealth, have no capital to deploy, want simplicity above all, or cannot fund a policy without sacrificing the match. There is no shame in that answer. For many people, maxing the match and a Roth is the right and complete strategy, and a policy would only add cost and complexity. If you cannot name an activity that beats the loan cost, no policy changes that math.

10 / Head to headThe And Asset against the 401(k), IRA, and taxable account

Compared to the accounts most high earners already hold, The And Asset trades early simplicity and the employer match for access, control, and tax treatment you keep. The table sets it against a traditional 401(k), a traditional IRA, and a taxable brokerage account on the four dimensions that decide life insurance strategy.

| Dimension | The And Asset | Traditional 401(k) | Traditional IRA | Taxable Brokerage |

|---|---|---|---|---|

| Access before 59½ | Policy loan at any age, no penalty | Restricted; 10% penalty plus tax on most early withdrawals | Restricted; same 10% penalty plus tax, limited exceptions | Fully accessible anytime |

| Growth while borrowed | Compounds on full cash value, net of internal costs, even while borrowed against | A 401(k) loan removes the money from the market; it stops compounding | No loan feature; a withdrawal ends compounding on that money | No leverage feature built in; selling ends compounding |

| Tax treatment | Loans not taxable income under IRC 7702 while in force | Deferred now, taxed as ordinary income later; RMDs at 73 | Deferred now, taxed as ordinary income later; RMDs at 73 | Capital gains and dividends taxed yearly |

| Control | You set timing and repayment; loan cannot be called | Contribution, access, and RMD rules set by Congress | Same statutory rules; you choose investments | Full control, taxed on every realized gain |

Access. The defining gap is age. A 401(k) and a traditional IRA both wall off your capital until 59 and a half under most circumstances, with a penalty for breaking in early. A policy loan carries no age rule, which is the whole reason an entrepreneur wants a capital base outside the plan.

Growth and control. A 401(k) loan is the closest qualified-plan analog, and it is structurally weaker: the borrowed money leaves the market and stops compounding, the cap is low, and the clock is short. The policy keeps compounding on its full value while you borrow, and the carrier cannot call the loan.

Tax. Both qualified plans defer tax and force taxable distributions at 73. The policy's loans are not taxable income while it stays in force, and the strategy adds tax diversification rather than replacing the deferral a 401(k) provides. The right mix depends on your situation, not on a slogan.

A composite: the founder who kept the match and built a capital base

Consider a 43-year-old business owner, preferred non-tobacco, already contributing enough to a 401(k) to capture the full employer match. She directs an additional $47,500 per year of discretionary capital into an overfunded whole life policy on a cashflow design. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction, and we throw those out.

In year six, with roughly $312,000 of accessible cash value, she borrows $164,000 against the policy to fund a buildout that expands her business's billable capacity. The 401(k) stays untouched and keeps compounding for retirement. The expansion returns an estimated 13.6% IRR, against an illustrative loan cost of around 6%, so the spread runs more than seven points in her favor. The policy compounds on its full value the entire time. Repayment runs on a 38-month schedule funded by the new revenue.

One dollar. Two jobs. The 401(k) never had to move.

The honest 30 minutes about whether this fits next to your 401(k).

We have structured more than 2,000 policies across all 50 states, and we have seen this strategy work exactly as designed and seen it fail. On a discovery call, a practitioner looks at your specific situation and tells you whether a policy belongs alongside your qualified plans, or whether you should just keep maxing the match. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQInfinite banking vs 401(k) questions

Is infinite banking better than a 401(k)?

Neither is better in the abstract, because they do different jobs. A 401(k) is a tax-deferred retirement account with restricted access before 59 and a half. The And Asset is a capital base you can borrow against at any age for deployment. Most entrepreneurs use both: the match-funded 401(k) for retirement and the policy for accessible capital.

Should I stop my 401(k) to fund infinite banking?

No, not before capturing your full employer match. An employer match is an immediate return no whole life policy can match in the early years. The And Asset is funded with discretionary capital after the match, not as a replacement for it. We turn people away who would skip the match to fund a policy.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Does the government own my 401(k)?

No. You own your 401(k) balance. The account is regulated by Congress and the IRS, which set contribution limits, withdrawal rules, and required minimum distributions. Access is restricted before age 59 and a half, and most withdrawals are taxed as ordinary income, but the assets are yours.

Can I access my money before 59 and a half with The And Asset?

Yes. Policy loans against cash value carry no age restriction and no early-withdrawal penalty. A 401(k) generally restricts access before 59 and a half, with a 10% penalty plus ordinary income tax on most early withdrawals. Access at any age is the core structural difference.

How is a policy loan different from a 401(k) loan?

A 401(k) loan removes money from the market, caps at the lesser of 50% of vested balance or $50,000, and usually must be repaid within five years or on a short timeline if you leave your job. A policy loan is collateralized by cash value that keeps compounding, has no fixed repayment schedule, and cannot be called by the carrier.

Are policy loans taxable like 401(k) withdrawals?

Policy loans are generally not taxable income while the policy stays in force, under the tax treatment of life insurance in IRC Section 7702. A 401(k) withdrawal is taxed as ordinary income, and Roth withdrawals are tax-free only if rules are met. A lapsed or surrendered policy can trigger tax on gains, so the policy must be managed.

What is the spendable-income lens?

The spendable-income lens asks how much you can actually spend after tax, not how large the account statement reads. A $1,000,000 traditional 401(k) is not $1,000,000 of spendable income, because withdrawals are taxed as ordinary income at an unknown future rate. Policy loans are accessed without that tax event while the policy is in force.

Can I use both a 401(k) and The And Asset?

Yes, and most of the entrepreneurs we work with do. Capture the full 401(k) match, then use discretionary capital to fund a policy that gives you accessible capital and tax diversification. The And Asset complements qualified plans rather than replacing them.

What about a Roth IRA versus The And Asset?

A Roth IRA delivers tax-free qualified withdrawals but still restricts access to earnings before 59 and a half and caps contributions tightly. The And Asset has no contribution cap tied to income limits and allows access at any age through loans. They are complementary tax buckets, and high earners often use both for diversification.

- Nelson Nash, Becoming Your Own Banker, the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law), the tax code provision behind the tax treatment of life insurance cash value and loans.

- IRS, 401(k) contribution limits, current employee deferral limits, which adjust annually.

- IRS, Required Minimum Distributions, the rules forcing taxable withdrawals from qualified plans.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a policy belongs next to your 401(k), book a discovery call. We will tell you if it does not.