.png)

Whole life insurance cash value is the living portion of a permanent policy you can access while alive. Part of every premium funds it, it grows from a guaranteed floor plus non-guaranteed dividends compounding net of mortality and expense charges, and you reach it mainly through a policy loan collateralized by the value.

Cash value is the most misunderstood number in personal finance, and the confusion is profitable for the people selling it. Buyers are shown a glossy illustration with a big year-thirty number, told the policy "compounds tax-free," and never walked through the mechanics underneath. Then year one arrives, the statement shows less cash value than premium paid, and trust evaporates. The problem was never the asset. The problem was that nobody explained how it works.

Cash value is not a savings balance and it is not the death benefit. It is a living capital base, built deliberately, that grows on a guaranteed floor and accrues non-guaranteed dividends net of the policy's internal costs. Understand that one sentence and most of the marketing noise around whole life insurance collapses.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and the single biggest gap we see is mechanical literacy. People argue about whether whole life is good or bad without understanding the engine inside it. This guide fixes that. We cover where cash value comes from, how dividends and paid-up additions drive it, the difference between the guaranteed and non-guaranteed columns, the realistic year-by-year timeline (no break-even before year four to five), and how you actually access the money through a policy loan.

- Cash value is the living asset inside a whole life policy, separate from the death benefit, that you can access while alive.

- It grows two ways: a guaranteed annual increase the carrier must credit, plus non-guaranteed dividends declared each year.

- Cash value compounds at the dividend rate net of mortality and expense charges, never at the gross dividend rate advertised.

- Paid-up additions are the rider that drives early cash value; without a heavy PUA design, growth is slow.

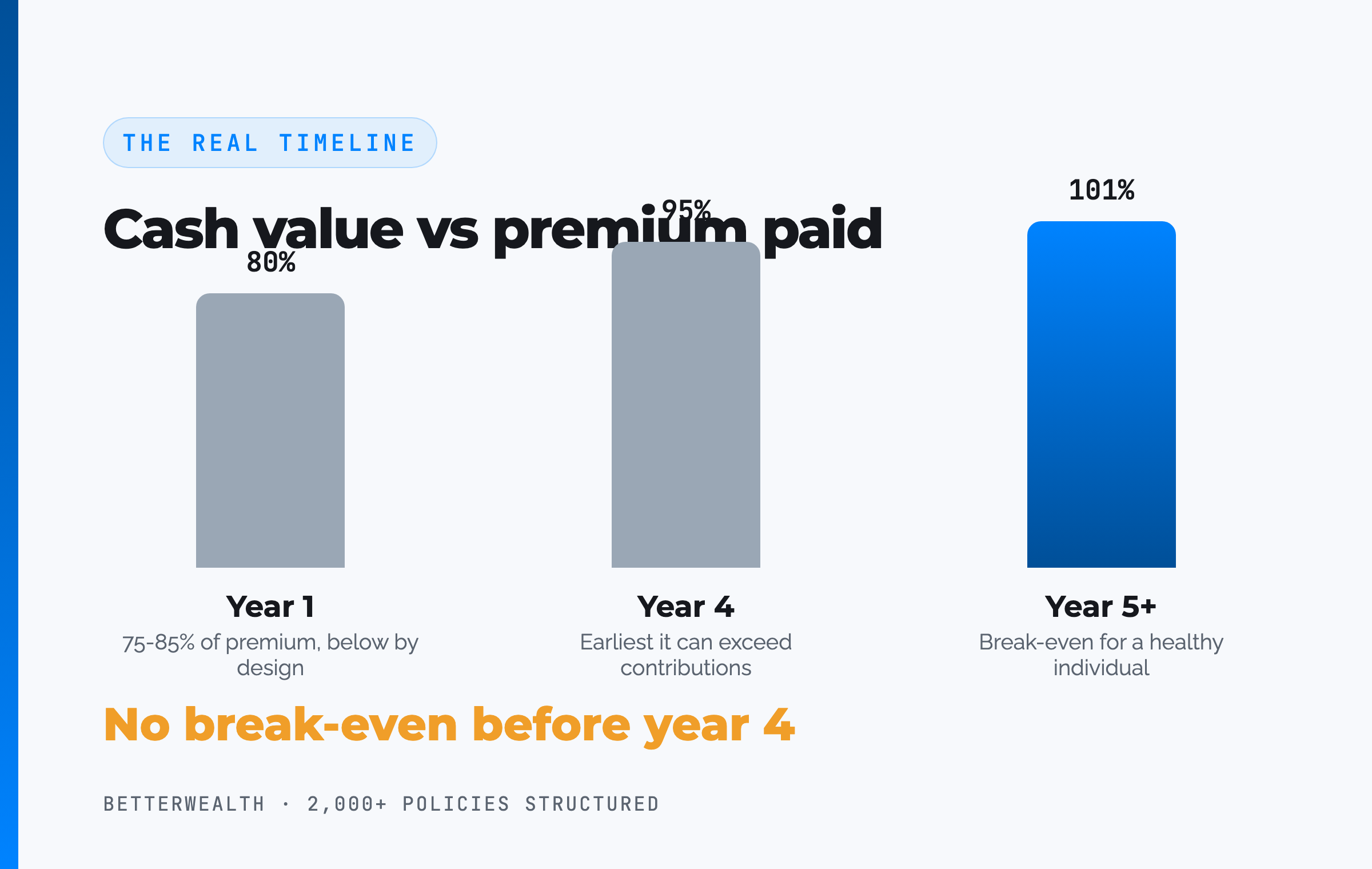

- A healthy, well-designed policy reaches break-even around year 5. Cash value does not exceed contributions before year 4.

- You access cash value mainly through a policy loan, which keeps the full value compounding while the loan is outstanding.

01 / The problemWhat cash value is actually supposed to solve

Cash value exists to give you access to capital without unwinding the asset that holds it. That is the structural problem it solves, and it is the problem conventional advice ignores. Money in a 401(k) is restricted until 59½ under rules set by Congress. Money in a brokerage account is liquid but taxed on gains every year you trade it. Money sitting in cash earns almost nothing and quietly loses the opportunity cost of not being deployed.

Whole life cash value sits in a different category. It compounds inside a tax-advantaged structure, and you can borrow against it without selling it, without a credit check, and without the lender being able to call the loan. For an entrepreneur or high-income earner whose capital is always spoken for, that combination is the point. The asset keeps growing while the capital it backs goes to work somewhere else.

The headline year-thirty number on an illustration is the least useful figure on the page. How the cash value behaves in years one through ten, and how you can use it, is what actually matters.

02 / DefinitionWhat is whole life insurance cash value?

Whole life insurance cash value is the portion of a permanent life insurance policy that builds up over time and that you can access while you are alive. A whole life policy has two values that live side by side. The death benefit pays your beneficiaries when you die. The cash value is the living asset you can borrow against, withdraw from, or eventually take as income. They are related, but they are not the same number, and confusing them is the root of most cash-value misunderstanding.

Here is the mechanical version. When you pay a whole life premium, the carrier allocates it across the cost of insurance, the policy's expenses, and the cash value account. In a traditional, agent-default policy, very little goes to cash value early on. In a policy designed for capital, the structure is flipped so that as much premium as the IRS allows funds cash value, without tipping the contract into a Modified Endowment Contract that would strip its tax treatment.

Why the design decides everything

The same carrier, the same insured, and the same premium can produce wildly different cash value depending on how the policy is built. A death-benefit-heavy design grows cash value slowly. A cash-value design front-loads the paid-up additions rider so the living asset is efficient from the start. This is why two people can own "whole life" and have completely different experiences of it. The product label is identical. The engineering is not.

The carrier matters. The design matters more.

03 / Growth mechanicsHow does whole life cash value grow?

Cash value grows in two layers, and keeping them separate is the difference between understanding the asset and being sold it. The first layer is guaranteed. The second is not.

The guaranteed layer

Every whole life contract specifies a guaranteed cash value schedule. The carrier is contractually obligated to credit at least this amount each year, regardless of how its investments perform or what it declares in dividends. This is the floor. It is conservative on purpose, and a sound policy stands on this column alone. If a policy only works on the optimistic projection, it is not a policy, it is a bet.

The non-guaranteed layer: dividends

Mutual carriers are owned by policyholders, and when the company performs well, it returns a portion of the surplus as an annual dividend. Dividends are declared by the board each year and are not guaranteed. You can take them as cash, use them to reduce premium, or, in a cash-value design, direct them to buy paid-up additions that compound. Over decades the dividend is where most of the policy's growth above the guaranteed floor comes from.

Here is the precision that marketers skip. The carrier advertises a dividend interest rate, often in the 5 to 6% range at the time of writing, and an agent will sometimes quote that figure as your growth rate. It is not. Your cash value grows at the dividend rate net of mortality and expense charges. The gross rate is applied inside a structure that carries the cost of insurance and the policy's expenses, so the figure that actually compounds in your cash value is lower than the headline. Any illustration treating the gross dividend rate as your return is either careless or selling.

Your cash value does not grow at the dividend rate. It grows at the dividend net of the policy's internal costs. The gross number on the brochure is not your return.

04 / The engineWhat are paid-up additions, and why do they matter?

Paid-up additions are the single design feature that determines how fast your cash value builds in the early years. A paid-up addition is a small piece of fully paid-up whole life insurance you purchase through a rider. Each one is immediately efficient: it adds death benefit and cash value with almost no new sales load, and it earns dividends of its own from day one. The PUA rider is the engine of a cash-value policy. Without it, you own an expensive death benefit that happens to have some cash value attached.

The structural decision is the base-to-PUA ratio. A policy heavily weighted toward the paid-up additions rider, something like a 40/60 or even 10/90 split depending on the design and carrier limits, pushes far more of each premium dollar into efficient cash value. The IRS caps how much you can stuff into a PUA rider before the contract becomes a Modified Endowment Contract and loses its loan tax treatment, so the design walks right up to that line without crossing it.

This is exactly the mechanic that makes the broader strategy work. A policy built with a heavy PUA rider is what gives you usable capital early enough to do something with it, which is the entire premise of using a policy as a capital base. We go deep on what that capital is actually for in our explainer on What Is Infinite Banking? The And Asset Guide, because building cash value is only half the equation. Deploying it intelligently is the other half.

No PUA rider, no early cash value. It is that simple.

05 / Step by stepHow cash value is built and accessed, in order

Cash value is built through a sequence of five steps, and the order is not optional. This is the mechanical path every well-designed policy follows, from the first premium to the first loan.

- Structure for cash value. Minimize the base premium and load the paid-up additions rider as heavily as the IRS allows. The base/PUA split is the design decision that determines early cash value. Get this wrong and nothing downstream recovers.

- Fund consistently. Each premium buys base coverage plus, through the rider, immediate paid-up insurance that carries its own cash value and earns its own dividends. Consistency is what compounds. A policy funded erratically performs erratically.

- Let early years capitalize. First-year cash value on a cashflow design lands roughly in the 75 to 85% of premium range. It is below premium on purpose, because early premium also covers the cost of insurance and acquisition costs. Do not expect day-one break-even. You will not get it, and any illustration that shows it is fiction.

- Cross break-even. Around year three, each premium dollar starts adding more than a dollar of cash value. Around year five for a healthy individual, total cash value catches total contributions. Cash value does not exceed cumulative contributions before year four.

- Access through a policy loan. Once the cash value is meaningful, you borrow against it. The loan is collateralized by the policy, not withdrawn from it, so the full cash value keeps compounding. Under IRC Section 7702, the loan proceeds are not taxable income.

That last step is where the asset stops being theoretical and starts being capital. It is also where the discipline that defines our approach comes in, which is the next section.

Cash value is a tool for a specific person doing specific things.

It fits you if

- You have a long capital horizon (10+ years)

- You already deploy capital and think in terms of return

- You can name a use for borrowed dollars that beats the loan cost

- You want access to capital without unwinding the asset

It does not fit you if

- You need maximum liquidity in year one

- You are early in building wealth and have higher-priority steps

- You want a savings account, not a capital base

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you whether a properly designed policy fits. If you are in the second, we will tell you that too.

Book a Discovery Call06 / The mathWhat is the cash value actually for?

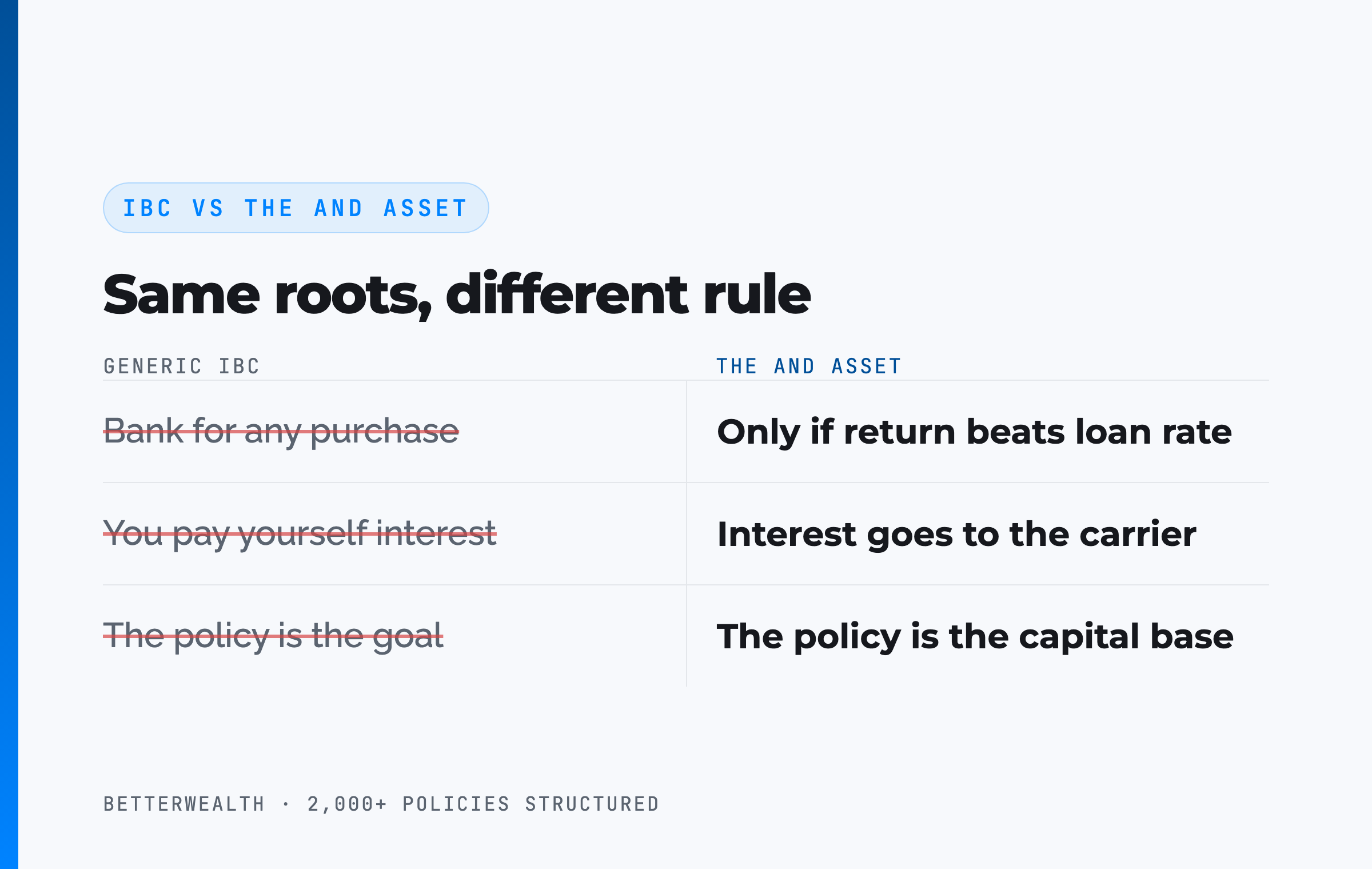

The cash value is capital you can put to work, and what you do with it is what creates the value, not the policy by itself. This is where BetterWealth diverges from how most people teach this. We call our framework The And Asset. It is built on Nelson Nash's foundation and it operates on a different principle.

Nelson Nash pioneered the idea of using whole life insurance as a personal banking system in Becoming Your Own Banker. His core insight holds: you either lose money paying interest to outside lenders, or you lose money to the opportunity cost of capital sitting idle. We respect that foundation. The And Asset adds one rule Nash's broader teaching does not enforce.

IBC says you can use the cash value as a personal bank for any purchase. The And Asset says you only borrow against the cash value when the deployed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many IBC marketers also say you are paying yourself interest when you repay a policy loan. You are not. The interest goes to the insurance company. Your return is what the borrowed capital earns elsewhere while the policy keeps compounding on its full value.

The math is a single test. You borrow at the carrier's loan rate, which varies by carrier and rate environment and often sits in the 5 to 6% range at the time of writing. Your policy keeps compounding on its full cash value. Your deployed capital earns its own return. If that return clears the loan cost, the same dollar has done two jobs, and you are ahead on the spread. If it does not, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

The cash value is the capital base. The value is created in what you deploy it into. If you cannot identify a use that beats the loan cost, the right move is to leave it compounding and not borrow at all.

07 / Guaranteed vs non-guaranteedWhich numbers on the illustration can you trust?

Trust the guaranteed column and treat the non-guaranteed column as upside, not a plan. Every whole life illustration shows two sets of values side by side, and the gap between them is the source of most disappointment and most overselling. The guaranteed column is what the carrier must deliver. The non-guaranteed column layers projected dividends on top, and dividends are declared annually and can change.

A responsible policy is evaluated on its guaranteed performance first. If the guaranteed column makes the strategy work, the dividends are a bonus. If the strategy only works on the projected column, you are planning your capital around a number nobody promised you. Mutual carriers with long dividend histories have paid dividends consistently for decades, including through recessions, which is meaningful context. It is not a guarantee, and the contract is careful to say so.

This is also why dividend-rate comparisons between carriers are close to useless on their own. A higher gross dividend rate inside a less efficient policy structure can produce lower cash value than a lower rate inside an efficient one. The rate is one input. The design, the internal costs, and the guaranteed floor decide the outcome.

08 / AccessHow do you actually get the cash value out?

You access cash value through one of two routes, and the route you choose has real consequences. The first is a withdrawal. The second is a policy loan. For a life insurance strategy, the loan is almost always the right tool.

Withdrawals

A withdrawal pulls money directly out of the cash value and permanently reduces it, along with the death benefit. Withdrawals are tax-free up to your cost basis, the total premium you have paid, but anything above basis can be taxable. A withdrawal also stops that money from ever compounding again. It is a one-way door, useful in narrow situations and rarely the move for an entrepreneur using the policy as a capital base.

Policy loans

A policy loan is the workhorse. You borrow from the carrier using your cash value as collateral. The cash value is not removed, it stays in the policy and keeps compounding on its full value, which is the structural feature that lets the same dollar do two jobs. The carrier charges interest on the loan, and you set the repayment terms. The loan cannot be called as long as the policy stays in force, and under IRC Section 7702 the loan proceeds are not taxable income.

One technical point worth knowing. Carriers handle loans under either direct or non-direct recognition. Under direct recognition, the carrier adjusts the dividend on the borrowed portion of cash value by a fixed, known spread. Under non-direct recognition, it does not. Neither is universally better. What matters is that under both, the policy keeps working while you have a loan outstanding, which is the entire reason this is different from draining a savings account.

A loan borrows against the value. It does not spend it.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators and design frameworks we use to structure cash value, compare carrier illustrations, and pressure-test whether borrowing makes sense. Free, email-gated, no spam.

Open the Vault09 / Where people get this wrongThe cash value mistakes that cost the most

The most expensive cash value mistakes come from believing the marketing instead of the mechanics. Four show up constantly across the policies we review.

First, expecting early break-even. Cash value runs below premium in the first years on every honest design. People who were promised day-one liquidity feel cheated, when the real problem was the promise. Second, quoting the gross dividend rate as the growth rate. The cash value grows net of mortality and expense charges, always lower than the headline. Third, buying a death-benefit-heavy policy and expecting cash-value performance. Without a heavy paid-up additions rider, the living asset builds slowly no matter how good the carrier is. Fourth, borrowing without a plan. A policy loan against cash value to fund consumption that returns nothing is just an expensive way to spend money, which is the exact behavior The And Asset rule exists to prevent.

There is also a fair question underneath all of this: given the early timeline and the internal costs, does the cash value justify owning the policy at all? That deserves an honest answer rather than a pitch, and we gave it one in Is Whole Life Insurance Worth It? An Honest Answer. The short version is that it depends entirely on whether you are the person who will use the capital with discipline.

Marketers have ruined how this gets explained. The mechanics are sound. The overselling is the problem, and it is why so many people own policies that do not fit them.

10 / Head to headCash value against the alternatives

Compared to the capital tools entrepreneurs actually use, whole life cash value trades the highest possible day-one liquidity for control, tax treatment, and uninterrupted compounding. The table sets it against a high-yield savings account, a HELOC, and a 401(k) on the dimensions that matter when you think of money as capital, not storage.

| Dimension | Whole Life Cash Value | HY Savings | HELOC | 401(k) |

|---|---|---|---|---|

| Growth | Guaranteed floor plus dividends, net of costs; compounds even while borrowed against | Interest only; taxed annually; no compounding while spent | None (a credit line, not an asset) | Market growth, tax-deferred |

| Access while alive | Policy loan against the value; cannot be called while in force | Immediate, but spending it removes it | Fast once approved, but can be frozen or called | Restricted before 59½ (penalty plus tax) |

| Tax treatment | Loans not taxable income under IRC 7702; growth tax-advantaged | Interest taxed as ordinary income yearly | Interest deductible only in limited cases | Deferred now, taxed as ordinary income later |

| Early liquidity | Below premium in year one; meaningful by years 4-5 | Full and immediate | High once the line is open | Locked without penalty |

Growth. Cash value keeps compounding on its full value while you borrow against it, which neither a savings account nor a HELOC can do, because spent savings stop compounding and a credit line is not an asset at all. That uninterrupted compounding is what makes the same dollar do two jobs.

Access and control. A HELOC is faster on paper, but it can be frozen exactly when you need it, as many investors learned in 2020. A policy loan against cash value cannot be called while the policy is in force. The 30-day initial wait and lower early liquidity are the price of access that does not disappear in a downturn.

Tax and timeline. Policy loans are not taxable income under Section 7702, and a 401(k) restricts access until 59½ under rules set by Congress. Cash value trades the highest possible early liquidity for control and tax treatment you keep. If you need cash this month, savings wins. If you are building a multi-decade capital base, this is a different instrument entirely.

A composite: the cash value behind a real deployment

Consider a 43-year-old business owner, preferred non-tobacco, funding a cash-value-designed whole life policy at $48,000 per year on a heavy paid-up additions rider. This is a representative composite, not a single named client.

Through the first three years, cash value trails cumulative contributions, exactly as a real policy should. By year three, each premium dollar adds more than a dollar of cash value. At year five, total cash value crosses total contributions. No earlier. Any illustration showing year-two break-even is marketing fiction, and we have watched buyers get burned believing one.

In year six, with roughly $312,000 of accessible cash value, the owner borrows $164,500 against the policy to fund a bulk inventory purchase at a supplier discount. The discount and resale margin return an estimated 13.8% IRR. The loan cost is illustrative at around 6%, so the spread works in the owner's favor by nearly eight points. The cash value keeps compounding on its full value the entire time. Repayment runs on a 29-month schedule funded by the inventory turnover itself.

One dollar. Two jobs. That is the And.

The honest 30 minutes about whether cash value fits you.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your specific situation and tells you whether a properly designed cash value policy, or no policy at all, belongs in your plan. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQWhole life cash value questions

What is whole life insurance cash value?

Whole life insurance cash value is the living portion of a permanent policy that you can access while alive. A part of every premium funds it, it grows from a guaranteed floor plus non-guaranteed dividends, and you reach it through withdrawals or, more often, a policy loan collateralized by the value. It is separate from the death benefit.

How does whole life insurance cash value grow?

Cash value grows two ways. A contractually guaranteed amount increases every year, and a mutual carrier may credit a non-guaranteed annual dividend on top. That dividend compounds at the dividend rate net of mortality and expense charges, which is why your cash value does not grow at the gross dividend rate the carrier advertises.

When does whole life cash value break even?

For a healthy individual with a well-designed, PUA-heavy policy, total cash value typically catches total contributions around year 5. Cash value does not exceed cumulative contributions before year 4. Any illustration showing year-one or year-two break-even is marketing fiction.

What are paid-up additions?

Paid-up additions are small chunks of fully paid-up whole life insurance you buy through a rider. Each one is immediately efficient, adding cash value and death benefit with almost no new sales load and earning its own dividends. The PUA rider is the single design feature that drives early cash value in a policy built for capital.

What is the difference between guaranteed and non-guaranteed cash value?

Guaranteed cash value is the contractual floor the carrier must credit regardless of performance. Non-guaranteed cash value comes from annual dividends, which are declared by the board each year and are not promised. A sound policy stands on the guaranteed column; the dividend is upside, not a number to plan your capital around.

How do you access cash value from a whole life policy?

The two routes are a withdrawal and a policy loan. Most strategies use a loan: you borrow against the cash value, the policy keeps compounding on its full value, and the loan is not taxable income under IRC Section 7702. A withdrawal permanently reduces the policy and can become taxable above your cost basis.

Does the policy keep growing when you borrow against the cash value?

Yes. A policy loan is collateralized by the cash value, not withdrawn from it, so the full cash value continues to compound while the loan is outstanding. Under direct recognition the carrier adjusts the dividend on the borrowed portion by a fixed spread; under non-direct recognition it does not. Either way the policy keeps working.

Is cash value the same as the death benefit?

No. The death benefit is what beneficiaries receive when you die. Cash value is the living asset you can access while alive. In a traditional policy the two converge over time; in a cash-value-designed policy the early gap between premium paid and cash value is much smaller because of the paid-up additions rider.

Why is my first-year cash value less than I paid in premium?

Early premium covers the cost of insurance and the policy's acquisition costs, so first-year cash value runs below premium even on an efficient design. On a well-structured cashflow policy, first-year cash value lands roughly in the 75 to 85% of premium range, then climbs until it crosses contributions around year 5.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against the cash value for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed cash value when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

- Nelson Nash, Becoming Your Own Banker. The origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law). The tax code provision governing cash value accumulation and the tax treatment of policy loans.

- IRC Section 7702A (Cornell Law). The Modified Endowment Contract rules that cap how much cash value a policy can hold.

- LIMRA. Life insurance industry data, including dividend and persistency benchmarks.

- NAIC. Regulatory guidance on life insurance illustrations and disclosures.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on whether a cash value policy fits your plan, book a discovery call. We will tell you if it does not.