.png)

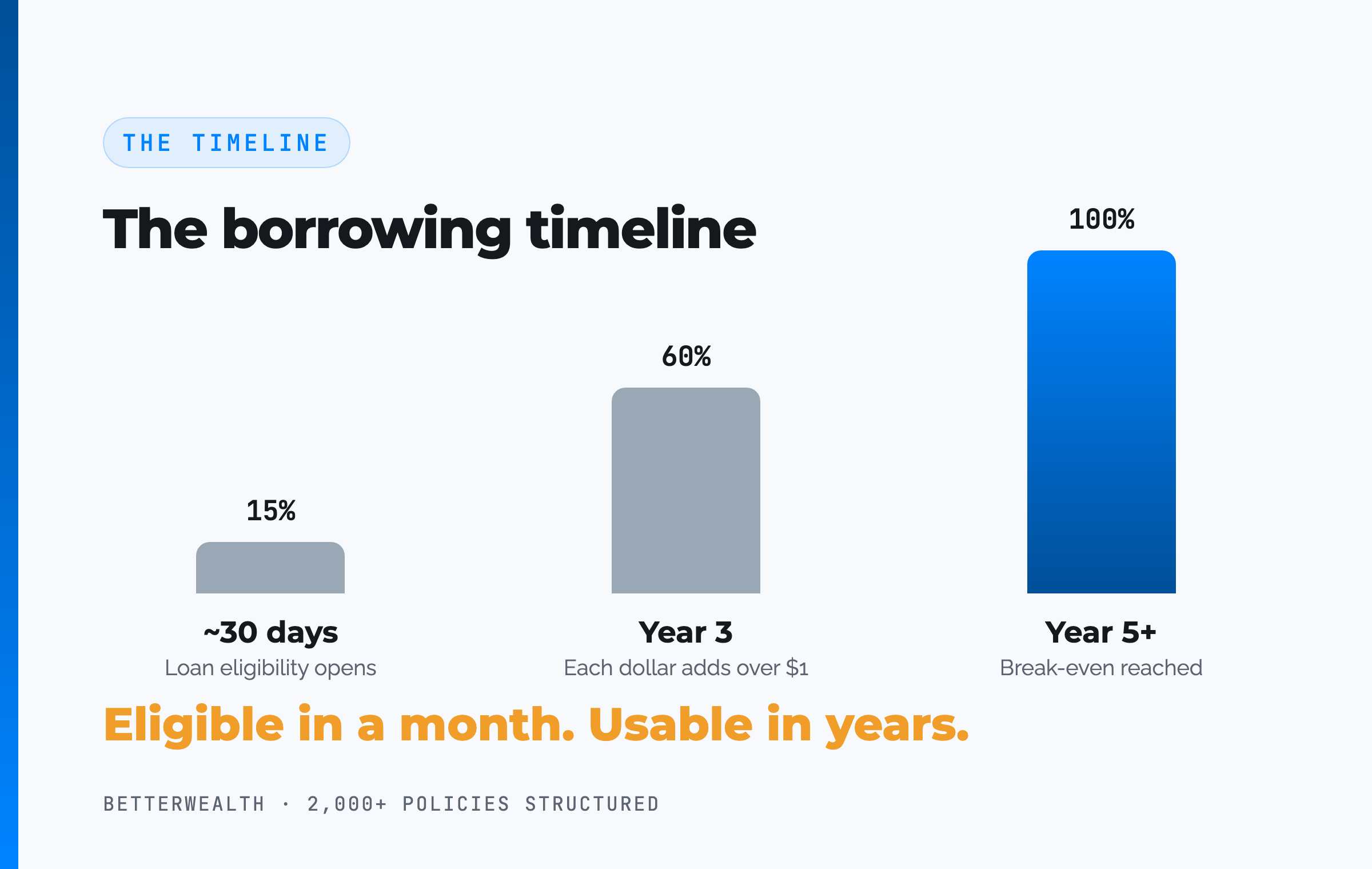

You can borrow against whole life insurance roughly 30 days after the policy is in force, once you have cash value to borrow against. The mechanical wait is short. The real timeline is about accumulation: cash value does not exceed cumulative contributions before year four, and break-even typically lands at year five or later for a healthy individual.

The question behind the question is almost always about timing a deal. Someone funds a whole life policy, an opportunity shows up eight months later, and they want to know whether the capital is reachable yet. The marketing answer is "right away, it is your money." The practitioner answer is more useful, because it separates two things that get collapsed into one.

The ability to take a policy loan arrives fast. The cash value worth borrowing against arrives over years. Both are true at the same time, and confusing them is how people end up disappointed in a strategy that was never designed to deliver maximum liquidity in month one.

At BetterWealth, we have structured more than 2,000 policies across all 50 states, and this is one of the most common timing questions we field. The answer depends on how the policy was built, how it was funded, and what you intend to do with the money. This piece lays out the real timeline: the carrier waiting period, why early cash value sits below what you paid in, how a properly overfunded policy puts usable capital to work sooner, and the rule that decides whether you should borrow at all once you can.

- Most carriers allow a policy loan about 30 days after the policy is in force, with no credit check and no lender approval.

- A properly overfunded policy holds roughly 75 to 85% of first-year premium as cash value you can borrow against.

- Cash value does not exceed cumulative contributions before year four; break-even lands at year five or later for healthy individuals.

- Overfunding with paid-up additions speeds up usable cash value, but it does not produce a year-one break-even.

- The policy keeps compounding on its full value while a loan is outstanding, net of mortality and expense charges.

- The And Asset rule governs: only borrow when the deployed return clears the carrier's loan cost.

01 / The problemTwo different clocks people confuse

There are two separate clocks running on a new whole life policy, and conflating them is the source of nearly every frustration. The first clock is eligibility: when the carrier mechanically lets you take a loan. The second is accumulation: when there is enough cash value that borrowing actually moves the needle on a deal.

The eligibility clock is short. Most carriers open policy loans about 30 days after the policy is in force. The accumulation clock runs for years, because a whole life policy front-loads the cost of insurance and acquisition costs, and the cash value has to climb past those before it works as a serious capital base. Treat them as one number and you will either over-promise (the marketer's mistake) or write the strategy off as useless in year one (the skeptic's mistake). Both are wrong.

"It is your money, access it anytime" is half true and fully misleading. You can access a little almost immediately. You cannot access a lot for years, and no honest illustration pretends otherwise.

02 / EligibilityHow fast can you actually take a policy loan?

You can typically take a policy loan about 30 days after the policy is in force, and the process carries none of the friction of bank lending. Once the contract is issued and the first premium is paid, the cash value becomes collateral you can borrow against. There is no credit check, no income verification, and no approval committee, because you are not asking a lender for their money. You are requesting a loan against your own policy's value.

That is what makes the eligibility clock fast. The limiting factor is never your qualifications. It is the size of the cash value sitting behind the loan. Carriers generally let you borrow up to roughly 90 to 95% of available cash value, holding back a buffer so accruing interest does not erode the collateral. Early on, 90% of a small number is still a small number.

No approval needed. Just collateral.

03 / What you borrow againstWhy early cash value sits below what you paid in

Early cash value sits below your cumulative contributions because the first policy years absorb the cost of insurance and the costs of putting the policy on the books, and the cash value needs time to capitalize past them. This is not a flaw. It is how permanent insurance works, and any illustration showing a dollar in equals a dollar of cash value on day one is fiction.

Understanding what is actually accumulating helps here. The cash value is the living, accessible value inside the policy, and it grows as the dividend net of mortality and expense charges compounds on it year after year. If the mechanics of that accumulation are new to you, we walk through exactly how whole life insurance cash value works and why the early-year curve looks the way it does. That curve is the whole reason the borrowing timeline is what it is.

On a well-designed policy, the turn comes around year three, where each premium dollar begins adding more than a dollar of cash value. Break-even, where total cash value catches total contributions, lands at year five or later for a healthy individual. Before year four, cash value stays under what you have paid in. That is the realistic shape of it.

If an agent shows you year-one or year-two break-even, walk away. A healthy, properly funded policy does not catch its contributions until year five at the earliest. Anyone promising sooner is selling, not structuring.

04 / The timelineHow to get to a usable policy loan, step by step

Getting to a usable policy loan follows five steps, and the order is fixed because the cash value has to build before borrowing means anything. Here is the sequence as we structure it.

- Fund the policy. Make the first premium and let the policy go in force. Cash value exists from year one, but on a properly funded policy it starts below your cumulative contributions. That is expected.

- Clear the carrier waiting period. Most carriers open policy loans roughly 30 days after the policy is in force. The mechanical ability to borrow shows up almost immediately. Having enough cash value to matter does not.

- Let early cash value capitalize. On a well-designed overfunded policy, each premium dollar starts adding more than a dollar of cash value around year three. Do not expect to break even before year four. You will not.

- Reach break-even. Total cash value catches total contributions at year five or later for a healthy individual. From here the policy is net-positive against everything you have paid in, and the accessible balance is large enough to fund real activity.

- Borrow and deploy. Take a policy loan collateralized by cash value, deploy it into an activity that returns more than the carrier's loan rate, and repay from the cash flow that activity generates. The policy compounds on its full value the entire time.

Eligible in a month. Powerful in a few years.

05 / OverfundingDoes overfunding let you borrow sooner?

Overfunding does let you borrow meaningfully sooner, because it changes how much of every premium dollar lands in cash value in the early years. A policy built mostly on base premium buys a large death benefit and accumulates cash value slowly. A policy built to be overfunded minimizes base premium and loads the paid-up additions rider, pushing cash value to the IRS limit without tipping the contract into a Modified Endowment Contract.

The base/PUA split is the single design decision that determines early cash value. A heavily weighted PUA design, something like a 10/90 split, puts roughly 75 to 85% of first-year premium into accessible cash value. A base-heavy design might leave almost nothing usable in year one. Same carrier, same dividend rate, radically different borrowing timeline.

What overfunding does not do

Overfunding accelerates the curve. It does not rewrite the laws of the curve. Even a maximally overfunded policy does not break even before year four, because the cost of insurance and acquisition costs still have to be absorbed. What overfunding buys you is more usable capital sooner inside that realistic timeline, not a year-one miracle. Anyone implying otherwise has misunderstood the mechanics, or is hoping you do.

Design moves the timeline. It does not break physics.

The borrowing timeline fits a specific kind of plan.

It fits you if

- You have a multi-year capital horizon, not a 60-day need

- You want a policy designed for early cash value access

- You can name a use for capital that beats the loan cost

- You value access that cannot be frozen or called

It does not fit you if

- You need maximum liquidity in the first few months

- You are solving an immediate high-interest debt crunch

- You want a savings account, not a capital base

- You cannot identify a productive use for borrowed dollars

If you are in the first column, a 30-minute conversation will tell you how to design for the access you need. If you are in the second, we will tell you that too.

Book a Discovery Call06 / The frameworkJust because you can borrow does not mean you should

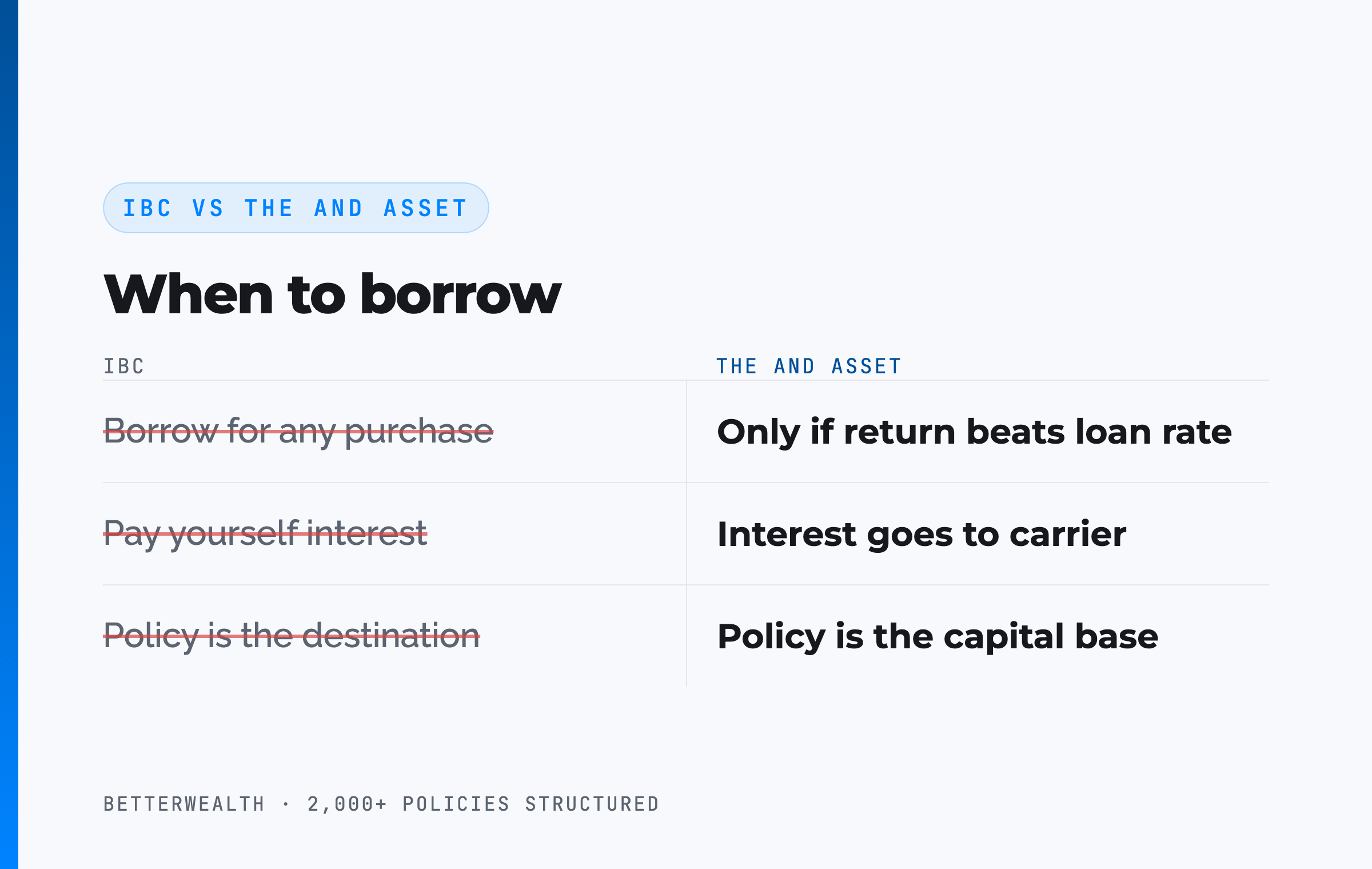

The right time to borrow is not "as soon as the carrier allows it." The right time is when you have an activity that returns more than the carrier's loan cost. This is where The And Asset departs from how most people teach infinite banking, and the distinction matters most precisely at the moment you first become eligible to borrow.

Nelson Nash pioneered using whole life insurance as a personal banking system in Becoming Your Own Banker. His insight holds: you either lose money paying interest to outside lenders, or you lose it to the opportunity cost of idle capital. We respect that foundation. The And Asset builds on it with one rule Nash's broader teaching does not enforce.

Where IBC ends and The And Asset begins

IBC says you can use a whole life policy as a personal banking system for any purchase. The And Asset says you only deploy capital from the policy when the borrowed dollars will produce a return greater than the carrier's loan cost. Anything less is an expensive way to spend money. Many marketers say you are paying yourself interest when you borrow. You are not. The interest goes to the carrier. Your return is what the deployed capital earns elsewhere while the policy keeps compounding uninterrupted.

So the timeline question has a second half nobody asks. Not just "how soon can I borrow," but "how soon will I have a use for the capital that clears the loan rate." If the answer to the second is "not yet," then the answer to the first does not matter. Leave the cash value compounding until the math works.

The math has to work. Every time.

Being able to borrow early is not a reason to borrow early. The discipline of waiting for a use that beats the loan cost is the strategy, not a limitation on it.

07 / The mathDoes the return clear the loan cost?

The return on whatever you deploy must exceed the carrier's loan cost, or borrowing destroys value instead of creating it. This single test governs every loan decision, regardless of how soon you are eligible. Policy loan rates vary by carrier and rate environment. At the time of writing, many carriers fall in the 5 to 6% range, but treat the specific number as a variable to verify with your carrier, not a constant.

The structure of the decision is simple. You borrow at the carrier's loan rate. The policy keeps compounding on its full cash value, including the borrowed portion, adjusted by the carrier's recognition spread. Your deployed capital earns its own return. If that return beats the loan cost, you are ahead on the spread and one dollar has done two jobs. If it does not, you have borrowed money to lose money slowly.

If the deal does not clear the loan rate, do not borrow.

The frameworks behind 2,000+ policies, in one place.

The And Asset Vault holds the calculators, design frameworks, and structuring decisions we use to build policies for early cash value access and to test whether a deal clears the loan cost. Free, email-gated, no spam.

Open the Vault08 / Head to headPolicy loan access versus the alternatives

Compared to the capital tools entrepreneurs actually use, a policy loan trades fast initial access for control, tax treatment, and uninterrupted compounding. The table sets the And Asset policy loan against a HELOC, a 401(k) loan, and a brokerage margin loan on the dimensions that decide a life insurance strategy.

| Dimension | And Asset policy loan | HELOC | 401(k) loan | Brokerage margin |

|---|---|---|---|---|

| Time to first access | ~30 days to eligibility, but meaningful balance builds over years | Weeks to set up; fast to draw once open | Days, but capped at $50K or 50% of balance | Fast once the account is funded |

| Approval | None; you borrow against your own cash value | Credit check, appraisal, income docs | Plan rules; no credit check | Margin agreement; subject to maintenance rules |

| Can it be frozen or called? | No; the loan cannot be called and access does not freeze | Yes; lines have been frozen and reduced | Loan accelerates if you leave the employer | Yes; a margin call can force liquidation |

| Does the base keep growing? | Yes; the policy compounds on full cash value while borrowed | No; home equity is not a compounding asset | You sell units; growth pauses on the borrowed portion | Holdings keep moving, but margin risk cuts both ways |

Time to first access. A HELOC or margin loan can deliver cash faster than a young policy can, and we say so plainly. The policy's edge is not speed in month one. It is that the access does not disappear when conditions tighten.

Frozen or called. A HELOC can be frozen exactly when you need it, as thousands of investors learned in 2020. A margin call can force a sale at the worst moment. A policy loan cannot be called, and you set the repayment terms.

Compounding base. The policy keeps compounding on its full value while you borrow, net of internal costs. A credit line is not an asset, and a 401(k) loan pulls money out of the market. That uninterrupted compounding is the structural feature that lets one dollar do two jobs.

A composite: the investor who waited for the right year

Consider a 39-year-old real estate investor, preferred non-tobacco, funding an overfunded whole life policy at $42,000 per year on a heavily weighted PUA design. This is a representative composite, not a single named client.

In month two, the investor was already eligible to borrow against roughly $33,600 of first-year cash value. He did not. There was no deal on the table that cleared the loan cost, so the disciplined move was to let the policy keep compounding. Through the first three years, cash value trailed cumulative contributions, exactly as a real policy should. By year three, each premium dollar was adding more than a dollar of cash value. At year five, total cash value crossed total contributions. No earlier.

In year six, with roughly $268,000 of accessible cash value, a value-add property came together. He borrowed $164,000 against the policy for the down payment and renovation budget. The stabilized deal returned an estimated 13.2% IRR against an illustrative loan cost near 6%, a spread of more than seven points in his favor. The policy kept compounding on its full value the entire time. Repayment ran on a 44-month schedule funded by the property's own cash flow.

One dollar. Two jobs. That is the And.

The honest 30 minutes about your timeline.

We have structured more than 2,000 policies across all 50 states. On a discovery call, a practitioner looks at your situation and tells you how soon a policy could give you usable capital, how to design for it, and whether the strategy fits at all. If you would rather learn first, the The And Asset and BetterWealth YouTube channels go deep on the math.

Book a Discovery CallFAQBorrowing against whole life questions

How soon can I borrow against whole life insurance?

Most carriers let you take a policy loan roughly 30 days after the policy is in force, so the mechanical ability to borrow comes within the first month. The practical question is different: a properly overfunded policy has meaningful cash value to borrow against in the first few years, but cash value does not exceed cumulative contributions before year four, and break-even typically lands at year five or later for a healthy individual.

Can I borrow against my whole life policy in the first year?

Often yes, mechanically, but the amount is small. A properly overfunded policy on a cashflow design holds roughly 75 to 85% of the first-year premium as cash value, and you can borrow against most of that after the carrier's short waiting period. A policy built mostly on base premium may show little to no usable first-year cash value.

Why is my whole life cash value lower than what I paid in?

Early cash value sits below cumulative contributions because the first years cover the cost of insurance and acquisition costs, and the policy needs time to capitalize. On a well-designed overfunded policy each premium dollar starts adding more than a dollar of cash value around year three, and total cash value catches total contributions at year five or later.

What is the waiting period to take a policy loan?

Most carriers allow a policy loan about 30 days after the policy is in force, once the contract has been issued and the first premium is paid. The exact timing varies by carrier, so confirm it with your carrier before you count on it for a specific deadline.

How does overfunding speed up access to cash value?

Overfunding loads the paid-up additions rider and minimizes base premium, which pushes more of every dollar into cash value in the early years without triggering a Modified Endowment Contract. A properly overfunded policy reaches usable cash value sooner than a base-heavy policy, though it still does not break even before year four.

What is The And Asset?

The And Asset is BetterWealth's framework for using a properly structured whole life policy as a capital base. You only borrow against it for an activity that produces a return greater than the carrier's loan cost, so your dollars do two jobs at once: the policy keeps compounding while the deployed capital earns its own return.

How is The And Asset different from infinite banking?

Infinite banking, as Nelson Nash taught it, frames a whole life policy as a personal banking system for any purchase. The And Asset adds a discipline: you only deploy borrowed capital when the return clears the carrier's loan cost. The policy is the capital base, not the destination. It is built on Nash's foundation but operates on different principles.

Do I have to qualify or get approved to borrow against my policy?

No. A policy loan requires no credit check, no income verification, and no lender approval, because you are borrowing against your own cash value as collateral. There is no underwriting on the loan itself. The only constraint is how much cash value you have accumulated.

How much of my cash value can I borrow?

Carriers typically allow you to borrow up to roughly 90 to 95% of your available cash value. The remainder stays as a buffer so the loan plus accruing interest does not erode the collateral. The exact percentage varies by carrier and policy.

Does borrowing against my policy stop it from growing?

No. The policy continues to compound on its full cash value while a loan is outstanding, because you are borrowing against the cash value rather than withdrawing it. Growth is the dividend net of mortality and expense charges, and a direct recognition carrier may adjust the dividend on the borrowed portion by a fixed spread.

Should I borrow against my policy as soon as I can?

Only if you have an activity that returns more than the carrier's loan cost. The ability to borrow early is not a reason to borrow early. If you cannot identify a productive use for the capital that beats the loan rate, leaving the cash value to compound is the better decision.

- Nelson Nash, Becoming Your Own Banker: the origin of the infinite banking concept.

- IRC Section 7702 (Cornell Law): the tax code provision behind the tax treatment of life insurance cash value and loans.

- IRC Section 7702A (Cornell Law): the Modified Endowment Contract rules that cap how much a policy can be overfunded.

- LIMRA: life insurance industry data, including persistency and policy-loan benchmarks.

- BetterWealth resources: The And Asset book, the The And Asset YouTube channel, and the BetterWealth YouTube channel.

I founded BetterWealth to treat life insurance as the wealth and capital tool it actually is, not the product most people get sold. Our team has structured more than 2,000 policies across all 50 states. I wrote The And Asset and host the BetterWealth and The And Asset YouTube channels. If you want an honest read on how soon a policy could give you usable capital, book a discovery call. We will tell you if it does not fit.