The Performance of Whole Life Insurance VS High-Yield Savings Bonds

Welcome back to our series with Todd Langford, the founder of Truth Concept. Today, we're delving into a compelling discussion about whole life insurance and its understated yet significant role in financial planning. This calculator that we're exploring today deepened my conviction about whole life insurance more than any other tool. While the platform may seem familiar from my previous YouTube videos, this is, in fact, a refined 2.0 version, and I'm excited to have Todd here to walk us through it.

The Misunderstood Asset: Whole Life Insurance

Life insurance, particularly whole life insurance, often encounters skepticism, primarily due to misconceptions about its rate of return. Our focus today is on understanding the real rate of return and appreciating life insurance over a lifetime rather than just short-term gains. Much like the tortoise and the hare fable, what's slow and steady can prove to be beneficial in the long run.

Integrating Life Insurance in Financial Planning

- Asset Efficiency: Life insurance can serve as a cash vehicle, not just an investment portfolio. It’s important to use cash efficiently and maximize benefits.

- Diversification: Life insurance complements real estate investments by providing a stable cash reserve.

- Long-Term Perspective: It is critical to evaluate the lifetime benefits rather than just immediate returns.

Case Study Analysis

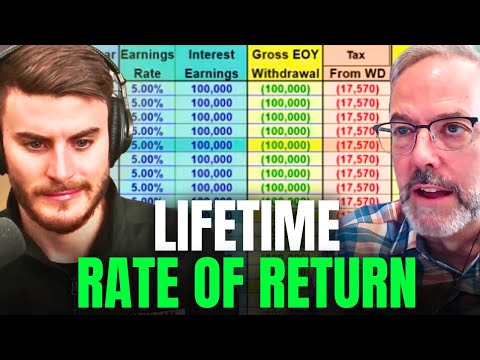

Consider a 35-year-old with a life insurance policy involving a $27,000 premium. Over a span of 35 years, predicted growth showcases an increase in cash value to nearly $3 million, with a rising death benefit reaching $3.3 million. Internal rate of return (IRR) can be perceived around 4.03%, integrating tax implications.

Exploring Alternate Accounts

Let's explore comparisons:

- Without whole life insurance, achieve equivalent savings using a 4.03% annual alternative.

- Consider tax implications and increased required rates over time.

The Cost of Term Insurance

Alternatively, providing a death benefit with term insurance incurs its own costs. An extended 30-year level term policy significantly hikes the costs after its initial duration, affecting overall calculations and outcomes.

Reflection of Economic Fluctuations

Life insurance returns displayed relative stability even amid historical interest rate changes. While short-term financial instruments might show rapid shifts, life insurance maintains slower, more consistent reactions, leveraging a substantial cash reserve.

Understanding High-Yield Alternatives

With current market dynamics, high-yield accounts might offer returns near competitive levels, presenting temporary opportunities. However, a long-term perspective reinforces whole life insurance's sustained value compared to fluctuating market interests.

Conclusion

As we continue this series, understanding life insurance as a multi-functional asset demonstrates its advantages beyond immediate returns. This strategic financial tool helps manage cash efficiently, providing protective benefits alongside insured reserves. As economic peaks and troughs come and go, whole life insurance retains its steadfast nature, serving as both a safety net and a strategic asset.

Full Transcript

This calculator does such a good job. It really does elevate our view of where life insurance should be. This life insurance policy just continues to grow all the way out. Most wealthy people have a bit of whole life insurance in their investment portfolio. That's part of what they do. And it's the general public, unfortunately, that gets fooled by some of the rhetoric out there saying it has a terrible way to return. What are our long-term marathon dollars doing? And that's what's important about what's happening here. What have been some of the a-haws of people that maybe have been in the industry have sold life insurance, but then how would this enhance what they currently do? I think one of the other big mistakes that a lot of people made. Hey guys, welcome back. We're in a series with Todd Langford, the founder of Truth Concept. And we're going through calculators. And this next calculator that we are going through is new and approved. But this one for me made me a grew my conviction of whole life insurance probably more than any other tool period. I have a couple videos on YouTube and it might look a little different because again, this is like a 2.0 version. And so we're having Todd back. He's going to walk through what's called the funding calculator. I'm going to hand it over to you Todd, but I would really encourage the people at home to listen, maybe rewatch this. And like always, like subscribing and commenting questions helps us. No, no kind of where your mind sets at. And Todd is willing to do a whole series with us. You enjoy this content buckle up because there's more to come. So without further ado, Todd, I'm going to hand it over to you and I'm taking notes as well. Great, Caleb, thanks. So life insurance, whole life insurance is probably one of the most misunderstood things out there really. And so one of the primary things that gets commented on is it has a terrible rate of return. And so what we're going to look at is what the real rate of return is. And we're also talking about time. It's not about just today. If it is about just today, then this is really the wrong tool to be using. If we're talking about over a lifetime, that's a whole different picture. And we have to look at it over a lifetime and not what's going on just in the first year or the second year or the third year or the tenth year. It needs to be out there forever. And so that's really what we need to look at and put it in perspective. So you know, kind of like the tortoise on the hare, those things that maybe start slow may end up winning the race if we understand how they work over time. And so that's a big piece of what we're going to look at here. And the other thing is so often people want to compare life insurance to their investment portfolio or their real estate or other places. The life insurance policy is really a cash vehicle, right? It's a savings vehicle, not an investment vehicle. And so whenever we have as an example, if we've got real estate and we're real estate investors, we're not talking about taking money away from real estate investing. What we're talking about is there's cash that needs to be on hand all the time to handle capital losses, a storm coming through vacancies, those kind of things. But where's that cash sitting? You know, if it's sitting in a checkered account, those are the dollars that we're talking about that maybe could be more efficient and provide additional benefits. And so that's a big piece of what happens when we start to look in a really efficient idea of a strategy for our finances. What we need to understand is that we want assets that can do more than one job, ideally, right? They can cover more than one place. So we're going to look at that and just see what this looks like. But those are just some upfront things to be wary of. And so when we look at this, so here I've got just a 35 year old, we're going to look out 35 years with this life insurance policy that has a 27,000 dollar premium. It's got cash value that over this time frame estimated based on what the company is currently doing to grow out to $2,000,000,000,000,000 over the 35 years. And it's also got a death benefit that's increasing, that starts a little over a million dollars. And ends up at $3.3 million over this time frame, if death were to occur along the way, it would be potentially any of these other numbers depending on how that growth occurred over time. So if we look at the rate of return here, so let's look at that first. So we see that this has a 4.03% internal rate of return. And what that means is if we put $27,000 a year in to get $2,000,000,000 at the end, it would take the equivalent of 4.03% every single year. Now life insurance policy doesn't work like that. And if we look at the RORs on an annual basis, so what we see is up front on the life insurance policy, it's going to have some negatives, right? If we judge this by what happens here versus the long run, we're going to miss out on really the full picture. But we can see that we've got negatives up front on this policy. So it's earning well less than the 4.03%. So how can we get to a place where it actually earns 4.03 the whole time frame? Well, what happens is at the policy ages, as it gets older and longer in the books, it earns a lot more than 4.03 so that it does the equivalent of that. And that's pretty confusing. It's hard for a lot of people to get their head around it, but let's look at it like this. What if we chose not to put this $27,184 in life insurance, but put it in another account that was earning 4.03% every year. Now remember this $2,000,000,000, we have down at the end in cash value. And we'll just make a note of it just so we can keep track of it might make it a little easier. So the cash value is estimated to be $2,994,794 at the end of this time frame of the company performs like it does this year all the way out to 35 years. It could be higher or lower than this, right? Now let's look at an alternate account, another option, and turn on the alternate account. And what I want to do is earn 4.03% every single year. Turn off the term insurance. Okay, so here at the 4.03, if we right-click there and let's earn that on this $27,000 every single year. So if we could put the $27,000 in account, earning 4.03 every single year, look what we see at the bottom of this time frame, the same $2,994,000. So while the life insurance policy didn't earn 4.03% every year, it has some negatives up front and earn more than that on the back. It earned over this time frame the same as an account that earn 4.03% every year. And that's the way an internal rate of retiring calculation works. And so it's important to understand that, even though it may not do that every year, that's the equivalent of what it would have done to get to that number of things. It's time frame. So it's an important piece. All right, so let's go back and think about this for a minute. With life insurance, we have a safe liquid asset, right? It's protected, it's got reserves, and we have access to those dollars. They're not locked up, right? What other asset really fits in that class? How do you say an account? That's about it. A bank account, so we have some FDIC insurance around it, maybe that's part of the protection there, right? And again, liquid, yeah, money market, sort of, checking accounts, CDs, depending on what our lock is on that kind of. But all those assets are actually tax on the earnings every year, right? Correct. And so we have to consider that piece. And so if we look at this and we look at taxes, say, in a 22% tax bracket, then what we see now is it would actually take 5.16% every year to get to our $2,494,000, because we can see right now if we just are in the 4.03 in the other account, and we had to take taxes out of that earnings, we only end up with a million seven. So let's see what happens if we are in 5.16 every year on this account to be able to pay the taxes. Ah, there's our $2,494,000. So now if we understand that an equivalent asset is going to be a bank asset that we have to pay taxes on, now we see, well, we would have to actually earn 5.16% on an alternate account to end up in the same place that we have with our life insurance policy. And that's not to say that life insurance policy is earned in 5.16. But we are saying is to have an equivalent taxable account, we would have to earn that to match what happens in that life insurance policy. Now, the life insurance policy also comes with a death benefit. And let's say that we wanted to use a different account, but we still wanted to provide a death benefit for our family. How would we do that? We have to have to have insurance, wouldn't we? Yeah. Yeah. Yeah. So we bought a million dollar term insurance policy. Then we would have the term insurance expenses. And what's interesting with a level term policy, if we scroll down on this policy, what we see is it's $1820. This was a 30 year level term policy, but when we get to the 31st year, that premium is going to jump to $36,000. So for a lot of people, that's going to force them to cancel the term insurance. Now, that's not by design. It's just that the insurance company did an actuarial calculation on the likelihood of death in these first 30 years. And now we're extended past that. And it means they undercharge that whole time. So they have to charge a lot more to catch up and get them back on the proper actuarial curve. And for a lot of people, it just means life insurance is going to is going to disappear at that point. So we're going to assume that we're going to cancel the insurance at age 64. And now, even with canceling it there, to have that extra term cost that's actually built into the whole life side, it would cause us to have to earn 5.55 to get back to our $2 million. All right, I don't know anywhere where anything that's safe is earning that kind of money, right? And so all of a sudden, we see that the life insurance, when we look at equivalent yields, has got a pretty good yield and it incorporates multiple pieces. We have the death benefit, along with our savings vehicle access to the cash and being able to use those dollars along the way to maybe even do more than this, right? It's not locked up in a particular area. Todd, I want to mention that at the time of this recording, there are certain high yield savings accounts that aren't at the 5.5, but they potentially are 5 or 4.5. And I would love to hear your thoughts on this because this is like a short term flash in the pan that we've experienced. And it's fair to say, and you can say it, but if interest rates were going to stay this high, it would be fair to say that we would also see an increase in the life insurance yields. What has been your experience about the rate of return in a whole life insurance policy over 30 years compared to a high yield savings account over 30 years, if you take that average? I want to interrupt real quick and invite you to an in-person and asset mastermind that we are hosting for the financial professional. This is for the person that literally helps clients use these strategies. And if that's you and you want to meet me and so many amazing other people in person, we're going to be hosting an event June 27th and 28th in Denver, Colorado. It's my third time hosting this and the whole purpose is to connect, connect, connect, connect. You have amazing people, connect you with amazing ideas, connect you with amazing strategies that can elevate your business. Garrett Gunnerson is going to be present. Tom Wall, we have Welk Nation, Denzel Rodriguez, Christopher Patrick, Ryan Lee, Todd, Langford from Truth Concepts, David Anderson from Life, I'm in Compossess and so many more people. It's going to be an incredible room. And if you will, again, are in this profession, in this space, you won't want to miss. Go to andsit.com to check out more information and hope to see you in June. Sure. And so one of the things that's driven the life insurance returns down, I would say, in that 4.03 percent internal rate return range is the fact that interest rates have been down for so long. If we start to see, we've got to like say a little blip that's happened where we all of a sudden see a little bit of a jump in interest rates. Most likely they're going to drop back down into that what we've been used to for the previous, you know, 25 plus years and that being down in the 0 to 2 percent range, right? If that doesn't happen, just like you're saying, then in all likelihood, it's going to push the returns up on the life insurance policies as well. The life insurance is always going to be slower to react. So what we see in the marketplace, we might see short bursts of fluctuations up and down and the life insurance policies just going to slowly go up, slowly go down. It's just not going to have those quick reactions. And it's because of the amount of cash that they have sitting on hand at the insurance companies and other pieces and parts about it. And so those those immediate quick blips just don't impact the life insurance as quickly. And so what we're assuming here is the life insurance policy never got better due to those ups and downs. And yet it's still performing at this level. So that's that's pretty amazing. Yeah. And we get the additional benefits along the way as well. You know, it's it's hard to see what's going to happen. And people look back and we see the last 30 years, the truth of the matter is, the policy that you had 30 years ago would have done way more than this because it would have taken advantage of some of that stuff that we saw 30 years ago in the nine plus range on the dividends, right? Yeah. That that dropped back. And so, you know, I would rather stay on the conservative side knowing that where we really are right now. Totally. On the low on probably the lowest dividend time we've ever seen. Right. Right. And yet look out for forms. Right. I love that. Yeah. We can continue. Yeah. All right. So, so let's let's look at this a little differently. And you know, some people might look at it as, okay, what if we did bonds, you know, for a lot of people in their portfolio, they've got bonds that are supposed to be the certainty side of the risk to balance off the equities, right? And life insurance policies, I mean, life insurance company has a lot of bonds. That's a big part of their portfolio. But if we think about it in terms of those bonds for just a minute and using this as a bond replacement, the bonds are also going to have another aspect. They're going to have fees, right? And so, if we look at a point and a half management fee, now you'd have to earn 7.62 to keep up with what the life insurance policy is doing. And so while the life insurance policy has a bad rap, and a lot of it's because of the short sightedness of looking at the front end, right? Those first four or five years are not looking at it over time. You really miss the opportunity that actually, you know, the wealthy have known for a long time, right? Most wealthy people have a bit of whole life insurance in their investment portfolio. That's part of what they do. And it's the general public, unfortunately, that gets fooled by some of the rhetoric out there saying it has a terrible rate of return. Yeah. Yeah. This has been again, so eye opening because again, you could look at even the 7.6% and we're not saying that life insurance gets that. In fact, the internal rate of return got a little over 4% in your example. But we are saying that that doesn't show the whole picture. And when you add in taxes, when you add in the cost of insurance, when you add in other scenarios like potential management fee, now you're increasing the borrowing old life insurance to you, you need an alternative account to earn far greater than that 4% just to compete with the life insurance. But what this, what this calculator doesn't even do a full job is articulate all the other benefits that you get in life insurance. And so what I love about it is it sets a stage, but there's other valuable things that you get by having whole life, insurance as a part of your portfolio, that we're not even able to articulate right now. Right. And, you know, just to add to that, what we're really doing is talking about a product right now and not necessarily a strategy. The beauty is of when that fits into an overall strategy. And I think what happens for a lot of people is they see the idea of the death benefit. And most people would like to have a death benefit to protect their family. Most people don't want to pay for it. Right. And so what we see is this idea that somehow our wealth accumulation and our protection are actually on two opposing or perpendicular paths. If we have the right tools in the right strategy, those can be on the same parallel path. Right. And that's what we're going to see here. Okay. So we'll take this a little bit further. Hopefully I haven't lost anybody too far yet. And like Caleb said earlier, watch it again. And see, but let's take this out a little bit. And let's go back and let's knock this down on the fixed right here on this account. Let's take off the management fees. And let's go back to a more normal 2% safe savings rate that we've seen over the last, you know, 25 plus years. And let's see how these compare to each other. So what we see is here. And let's turn off the right of returns. And the RORs. So we can just focus on this. So putting in the same amount of money each year. This first one shows the alternate account earning 2% and having taxes and term insurance to have to pay for to match what we have with the life insurance. We can see that savings account is actually ahead of the life insurance policy. In this case, with this particular product for about 11 years. And at one point, the life insurance policy is behind by as much as about a premium and a quarter right there on the fifth year as the most. And then what happens over this time frame, there's $900,000 more plus a death benefit that doesn't go away like it did with the term insurance. Yeah. So let's look at the term and all right, let's look at the legacy for just a minute as well in this picture. Go ahead and click it again. Look at this. So we have $900,000 more in cash. And we have $2 million more in legacy or death benefit across that time frame. And I know it's difficult looking at numbers when you're not used to just a bunch of raw numbers, but let's put it in a graphical format that's a little easier to understand. Okay, so here is the cash. Right. So this is the cash curve. The blue line represents the cash value of the whole life insurance policy. The gold line here is our 2% account. And what we see is that blue line in that first 10 years falls just below the gold line. It's a little bit behind across this time frame. And then there from the like 11th year on, the difference is double. There's twice as much money in the cash value as there is in that savings account. And this red, these red bars represent the amount that we put in and we can see in both scenarios exactly the same. So both of them are paying the same amount of money over this time frame. And this is the difference in the way the cash grows across this time frame. Little behind on the front end, the idea of the tortoise and the hare, right? And this is what it provides. And if our goal is only five years out, we need to be looking at something else. What are our long term marathon dollars doing? And that's what's important about what's happening here. Now what we said earlier was most people look at protection as something that costs us in our wealth accumulation. Let's now switch gears and look at the legacy or death benefit side of this. And so we're going to turn on the legacy and turn off the cash. And what we see here is the purple line represents the death benefit of the whole life policy. The goal line enters the death benefit or legacy of our choice to buy term insurance and have our savings account. So really what makes up the death benefit on the alternate choice is the term insurance death benefit plus whatever that account grows to. And that's why when we see here at age 65, we see this big drop. That's when we become totally self-insured, right? And at that point in time, now our legacy is only what we have in cash. And so this life insurance policy, just like we saw in the cash continues to grow all the way out. Yeah. And if we turn off the alternate account and turn on the cash, here's what happens on that parallel path. We see both the death benefit, that legacy piece, and our cash growing. They're not fighting each other and work an opposite. And yet the way a lot of people ensure themselves, the lot of way a lot of people set up their financial strategy, there are things that contradict and are perpendicular to their path. But with the right tools and the right strategy, which is the biggest piece in place, those can be on the same path and help each other get to that end result. Yeah, that's amazing. And Kim, if you can show the other one, I know that there's a lot of lines, but I think it's powerful if you could compare it to if you just see, so not only the legacy part is greater from the very, pretty much from the very beginning and on, but the cash, the cash account, you can just see that blue line after, you know, after that 11, 12 years just continues to pull away. And again, this is this is representing the death benefit and cash, but there's other benefits that you get with a life insurance. And that's where you talk about where this is just looking at the product. Now, we're not looking at strategy and how this plays a role, but this is just powerful to look at a life insurance policy where most people kind of dog on like, oh, this is horrible, rate of return. And all if you compare it to a like asset, which this this calculator does such a good job with, it really does elevate our view of where life insurance should be. You're right. And I think what you said is a critical, critical piece that I should have commented on earlier. And yes, this is behind up front from a cash standpoint, but look what it did with the death benefit. See, it's kind of a trade off in that cost in those other early years. It's got a much higher death benefit across that timeframe. And then eventually, both of them surpass all of it. Yeah. Yeah. And so something that's given a bad rap is having a terrible rate of return is very short-sighted unfortunately. And when we really get some of the pieces in there, we can see for the type of asset it is, there's really not anything else out there that has that kind of return. Now, return alone is not what we're looking for. And as you said earlier, you know, it has to be in the right strategy. We need to see a full picture to know how everything fits in the right place. And, you know, so often people like said earlier want to compare life insurance to their investment portfolio. What if those work together? Right. As an and asset. Yeah. And what we see is this is just the front half, but when we get into the distribution phase, wow, it really shines even more so in that piece because those other assets, those alternative accounts that we're talking about, those other investments, life insurance is going to make them way more spendable during that distribution phase. Yeah. I love love love that. And what I just want to say is if you are an advisor, if you help if you help people with money, if you're like, I want to get my hands on these calculators so that I can be better what I do and be able to understand how these numbers work. We'll have a link down below where you can get access to two truth concepts. And again, if you're like, I want to learn more about life insurance, just to see if this would be a good fit for for me. And what when I'm trying to accomplish, we'll also have a link where you can learn more about that. Todd, I'm excited to go through this series with you because, you know, you kind of hinted at a future future video to as it relates to looking at the distribution. What have been some of the a-haws that you've seen people that have gone through this at your your workshops and all? Like what have been some of the a-haws of people that maybe have been in the industry have sold, you know, life insurance, but then like how does this enhance what they currently do? Like I'm just curious what some of the things that you hear because again, I've seen many people use this and this has really increased their conviction for life insurance. Yeah, what unfortunately there's not a lot of good training in the industry. And so, you know, people in the industry a lot of times people that are helping clients, they do the best they can with what they have. And there are a lot of gimmicks out there in the financial world, right? There just are that aren't completely true. And I think a lot of advisors are amazed that if we can just get this to where it's understandable that people can really see how it can impact their lives just for what it is without any of the extra pieces and parts. It's just, it's it's really very simple and yeah, at the same time it's it's complicated. It can be complicated, right? Because there's so much misinformation out there that has to kind of be undone. And so, when we have clients that are really willing to look at what do the numbers say? And then let's step back from that and see how that fits into a into a bigger picture. But I've seen advisors that have been in the industry 30 plus years at training. They say, why is nobody ever told me this? Yeah, and I can't answer that question. But challenge me, you know, what we want to do more than anything is get to the absolute truth. And if there's something that's ever said that's not, we want to make sure that it's right. And and the numbers, you know, there's no gray in math. Right? It's right. It's what it is. Any any final thoughts before we land the plan here? You know, I think one thing that and maybe it's not for this conversation, but I think what's important, one of the things that I said about how it's going to help during the distribution phase, I think one of the other big mistakes that a lot of people make is focusing on net worth. And and I think that's one of the big detractors on good financial decisions is what's the net worth between this decision and another decision. And unfortunately net worth doesn't pay the bills. And so piling up money and something that's not spendable is not really helpful. And so that strategy that we look at out there in the future really needs to shift to what are my cash flow options based on, you know, what I'm putting together in my financial portfolio and how's that spendable because what we might find is that having smaller assets in the presence of whole life insurance might actually give us more cash flow causing those assets to act like much bigger assets than what they are. Hey, it's Caleb Williams here. I'm just interrupting this video quickly to invite you to check out our Ann Desset Vault. You may have been there. We've actually revamping it. And if you are somebody that wants to learn more about is life insurance right fit for me, does this end asset makes sense? Like does this actually help me be more efficient? We've put together a 10 minute documentary style video and I can test a really really good job giving the history why the end asset, different setups and designs that we use. And then we have an Ann Desset Vault that gives case studies, calculators, handbooks and so much more. We are here to serve you whether it's a conversation, whether it's education or the video. So make sure to go check out and Desset.com, Sush Bolt, learn more.