Estate Tax vs. Gift Tax: Understanding the Rules on Gifting Money to Family

Navigating taxes in estate planning can be complex, especially when you consider estate tax and gift tax. If you're thinking about gifting money to your family as part of your wealth transfer strategy, it’s crucial to understand these two tax concepts and how they differ. In this blog, I’ll break down exactly what you need to know about estate tax, gift tax, and the rules on gifting money to family to help you maximize your financial legacy.

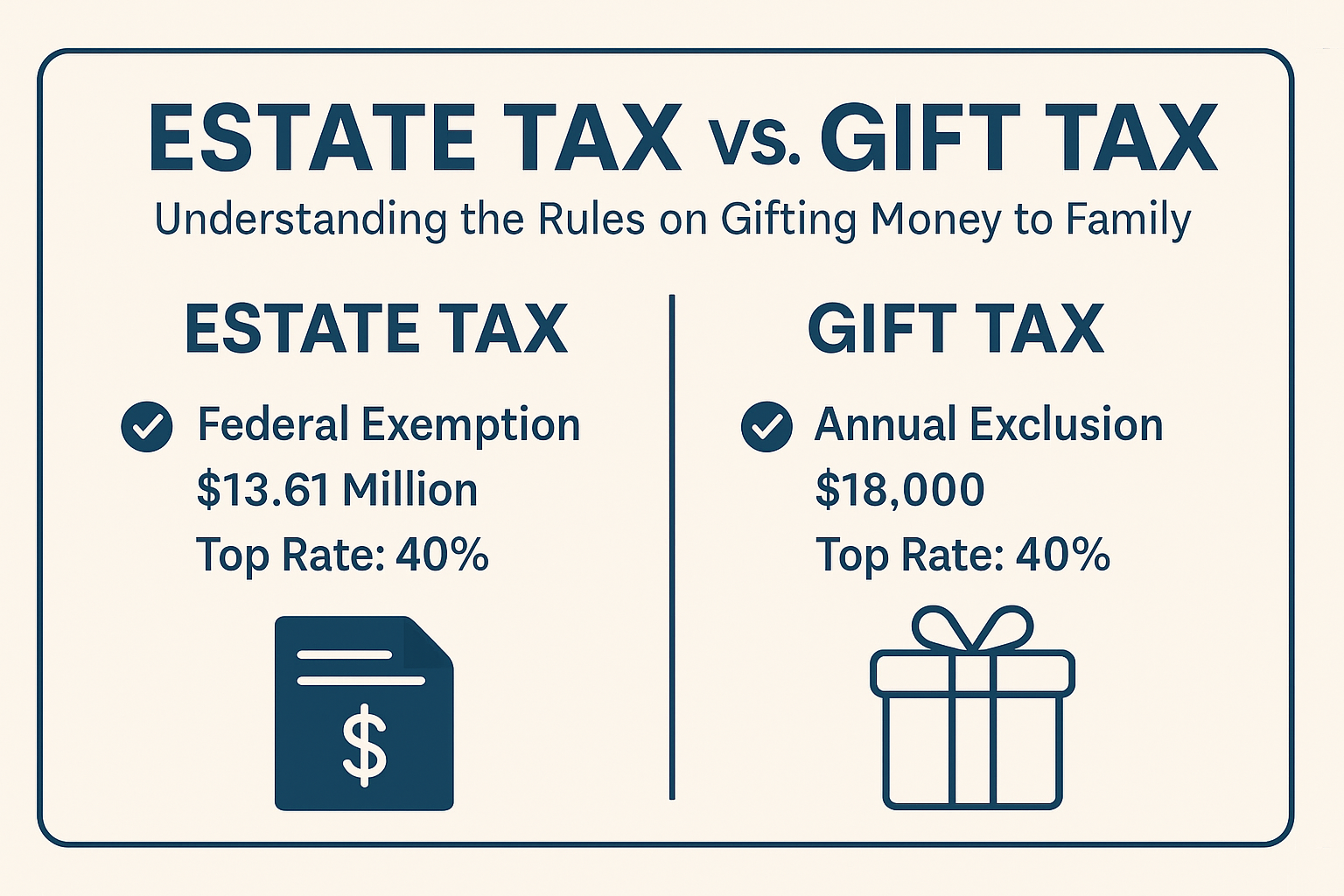

What Is Estate Tax?

The estate tax—sometimes called the "death tax"—is a tax imposed by the federal government (and sometimes states) on the transfer of a deceased individual's assets. The tax is calculated based on the estate's total value at the time of the individual’s death.

Currently, the federal estate tax exemption for 2024 is set at $13.61 million per individual ($27.22 million for married couples). Only estates valued above this amount owe federal estate tax, which currently has a top tax rate of 40%.

Estate Tax Highlights:

- Federal exemption (2024): $13.61 million per individual

- Top Federal Tax Rate: 40%

- Applicable assets: Cash, real estate, securities, insurance, businesses, trusts, and other property

State Estate Tax Considerations

Some states impose their own estate taxes with lower exemption thresholds than the federal government. States with estate taxes include Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington, among others. Always check local state rules to avoid unexpected taxes.

What Is Gift Tax?

The gift tax is a federal tax levied on the transfer of property or cash from one individual to another without receiving equal value in return. The IRS imposes gift tax to prevent individuals from avoiding estate taxes by giving away their wealth during their lifetime.

Key Gift Tax Highlights:

- Annual Exclusion (2024): $18,000 per recipient per year

- Lifetime Gift Tax Exemption (2024): Unified with estate tax at $13.61 million

- Top Federal Gift Tax Rate: 40%

This means you can gift up to $18,000 each year to as many individuals as you like without triggering the gift tax. Married couples can combine their annual exclusions, giving up to $36,000 per recipient annually without gift-tax consequences.

Estate Tax vs. Gift Tax: Key Differences

Understanding these key differences will help you leverage both estate planning tools effectively:

|

Factor |

Estate Tax |

Gift Tax |

|

When applied? |

After death (on estate value) |

During lifetime (on gifts given) |

|

Who pays? |

Estate before distribution |

Donor (person giving the gift) |

|

Exemption (2024) |

$13.61 million per person |

$13.61 million lifetime exemption |

|

Annual exclusion |

N/A |

$18,000 per recipient per year |

|

Tax rate |

Top rate of 40% |

Top rate of 40% |

Rules on Gifting Money to Family: A Practical Guide

Annual Gift Tax Exclusion

One of the easiest ways to minimize estate and gift taxes is to take advantage of the annual gift tax exclusion, which currently stands at $18,000 per recipient for 2024. This exclusion is per donor, meaning that you and your spouse can jointly give up to $36,000 annually per recipient without triggering any tax consequences.

Example:

- A couple with three adult children can gift up to $108,000 annually ($36,000 to each child) without owing gift taxes or utilizing their lifetime exemption.

Direct Payment Exemption

You can bypass gift tax entirely by directly paying medical and educational expenses for family members. These payments must be made directly to the medical institution or educational provider—not to the individual—to qualify for this exemption.

Lifetime Gift and Estate Tax Exemption

The lifetime exemption of $13.61 million (as of 2024) is unified between gift and estate taxes. This means each dollar gifted above the annual exclusion reduces your remaining estate tax exemption.

Example:

- If you gift your child $118,000 in one year, you surpass the annual exclusion ($18,000) by $100,000. This $100,000 will reduce your lifetime exemption from $13.61 million to $13.51 million.

How Gifting Can Minimize Estate Taxes

Strategically gifting money to family members can significantly reduce the value of your taxable estate, thus lowering potential estate tax liability.

Consider the following strategies:

1. Annual Gifts Within the Exclusion Limit

Giving consistently within the annual exclusion limits each year can substantially reduce the taxable value of your estate over time.

2. Utilize Trusts for Larger Gifts

For larger gifts, using irrevocable trusts can protect assets from estate taxes. Once placed in an irrevocable trust, these assets are no longer part of your estate for tax purposes.

For more details, see my blog post: Revocable vs. Irrevocable Trust: Understanding the Key Differences

3. Educational and Medical Expenses

Directly paying tuition and medical bills provides immediate benefit to your beneficiaries while avoiding gift tax implications altogether.

Common Misconceptions About Gift and Estate Taxes

Misconception #1: "You Can't Gift More Than the Annual Limit"

You can give more than the annual exclusion. However, gifts above this amount reduce your lifetime exemption, potentially affecting estate tax liability.

Misconception #2: "Gift Tax Is Always Owed by the Recipient"

The gift tax is typically the responsibility of the donor (the giver), not the recipient.

Misconception #3: "All Gifts to Spouses Are Taxable"

Transfers between spouses are generally exempt from gift and estate taxes due to the unlimited marital deduction.

Actionable Steps to Maximize Gifting Strategies

Here's what you can do immediately to optimize your gifting and reduce estate and gift tax exposure:

- Assess Your Estate Size: Evaluate your assets to understand your potential estate tax liability clearly.

- Plan Annual Gifting: Create a gifting plan leveraging annual exclusions to minimize taxable estate value.

- Consider Direct Payments: Directly pay for family members' educational and medical expenses.

- Explore Trust Structures: Evaluate irrevocable trusts as vehicles for larger transfers to safeguard your assets.

- Seek Professional Advice: Consult with an estate planning professional to structure your gifting effectively.

Final Thoughts: Secure Your Family’s Financial Future

Understanding the rules on gifting money to family—and how estate and gift taxes apply—can make a significant difference in preserving your family’s wealth. With careful planning, you can effectively pass on assets to your loved ones while minimizing or entirely avoiding unnecessary taxes.

At BetterWealth, we’re here to help you navigate these complexities and craft an estate plan tailored specifically to your financial goals.

Schedule a consultation with our team today to start creating a tax-efficient gifting strategy that protects your family's financial future.