Everything that we do needs to be represented on cash flow because whether it's our salary or income, future pension, social security, or future investment income, our world is based around cash flow. This whole model, this whole assessment is based around a cash flow ratio between how much money you're consuming and how much money you're saving.

Consumption vs. Savings

The consumption is based on any dollars that you lose, whether you lose it to paying taxes, buying a coffee, incurring a necessary business expense, or any time you lose, spend, or use a dollar. You don't just lose that dollar, but you lose what that dollar could earn you for the rest of your life.

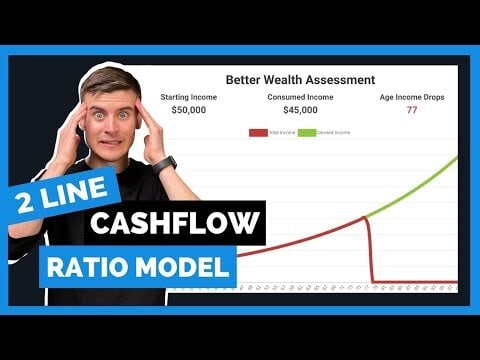

Understanding the Better Wealth Assessment

This is Better Wealth with Caleb Guilliams. Welcome to the first ever Better Wealth Assessment! I'm excited that you are here, and this assessment is ready to go live. I want to break down the philosophy and brilliance of how this model and the assessment were designed.

- It's not based on a strategy or theory; it's based on math.

- We want to give you a mirror to see how you're currently doing.

- Answer tough questions like how much money you need to be saving.

- Make key pivots for better financial management.

Graphical Representation of Cash Flow

I'm drawing a dollar sign, and this represents cash flow. Everything that we do needs to be represented on cash flow because, as stated, our world is based on cash flow.

Inflation and Its Impact

We need to understand inflation, which makes our dollars less valuable. For example, if a family was making $100,000, saving $10,000, and consuming $90,000: they need $90,000 now, but much more in the future to maintain the same lifestyle because of inflation.

Calculating Your Financial Future

We're assuming an inflation rate of 3%, a 7% investment return rate before retirement, and conservatism for post-retirement. Including Social Security, pensions, and other accounts help make this snapshot more accurate.

- Your initial savings and how much you save annually.

- Projected income increase by 3% annually.

- Expected retirement age and lifestyle maintenance costs.

The Red Line and Green Line

The concept is to keep the red line, representing necessary income, balanced with the green line, representing savings growth. Most people find a gap because of unseen factors like inflation, taxes, etc.

Tools and Recommendations

Factors like tax efficiency, money tracking, and growth strategies can help you align your financial future.

- Maximize current savings potential.

- Explore financial strategies for better ROI.

In Conclusion

This Better Wealth Assessment offers a snapshot of where you are and what needs to be changed to stay in balance. If this model seems off, remember: there are solutions, and working with someone skilled can help maximize your financial potential.

Thank you for listening to The Better Well Podcast. Hit subscribe, leave a review, and share with those you care about.

Full Transcript

Everything that we do needs to be represented on cash flow because whether it's our salary or income, future pension, social security, future investment income, like our world is based around cash flow. And so this whole model, this whole assessment is based around a cash flow ratio between how much money you're consuming and how much money you're saving. Now, the consumption is based off of any dollars that you lose, whether you lose it to paying taxes, whether you lose it to going and getting a coffee, whether you lose it to a necessary business expense or anytime you lose or spend or use a dollar, you don't just lose that dollar, but you lose with that dollar to earn you the rest of your life. This is Better Well with Caleb Gullium. Hey everybody, welcome to the first ever Better Well Assessment. I'm so excited that you're here and I'm so excited that this assessment is ready to go live. And what I want to do is break down this quick video so that you understand the philosophy and really the brilliance of how this model was designed, the assessment was designed, and really so that you understand that this is not based on a strategy, this is not based on a some philosophy or theory, but this is based around math and it makes a ton of sense and what we wanted to do as a company is give you a mirror so that you could see how you're currently doing answer tough questions like how much money you need to be saving so that you can make some key pivots and really understand that there are better ways to approach this whole money thing than just the typical way. So what I'm going to do is I'm going to draw my computer and I'm going to put myself in the corner here and give you the philosophy of how this tool is built. So essentially I'm drawing a dollar sign and this represents cash flow. Everything that we do needs to be represented on cash flow because whether it's our salary or income, future pensions, social security, future investment income like our world is based around cash flow. And so this whole model, this whole assessment is based around a cash flow ratio between how much money you're consuming and how much money you're saving. Now the consumption is based off of any dollars that you lose, whether you lose it to paying taxes, whether you lose it to going and getting a coffee, whether you lose it to a necessary business expense or anytime you lose or spend or use a dollar, you don't just lose that dollar but you lose with that dollar to earn you the rest of your life. And what we find is a lot of people, their number, this number right here is represents your consumption. It also ultimately represents the cost of you living life. And then the other number is the savings and this is money that you are saving for a future date. Now the assumption that we're making is this dollars, you're not just saving for like a car or a refrigerator or some short term consumption, you're saving for a future date. You're saving for the future retirement or your future legacy and the assumption that we're going to make is these dollars need to be working for you over time and the hope is that they can grow, the hope is that you can control and maximize the use of those savings. So just real quick, you have money coming in, your money can either go to places, it can be consumed or it could be saved. And the question that we want to be able to answer is what you're currently doing, how much money do you need to save, what needs to happen in your model so that you can maintain your current lifestyle. Now how I draw this out is I'm drawing of just a little graph. And what we have to understand is this thing called inflation, inflation pretty much is making our dollars less valuable. In other words, it takes more money to maintain what we're currently used to living. So if let's say for example, we just to make this this simple, we were making $100,000 as a family, we were saving $10,000 and we were consuming $90,000. So when it comes to taxes, when it comes to the cost of living, we spent $90,000 and it's gone forever and $10,000 is working for us. So the assumption that we can make is $90,000, I'm going to do 90K, is what we're currently used to living and to just to maintain that, it's not just going to be a linear because inflation means we this line needs to be in in crease because in 20 years, we need a whole lot more money to spend just to keep up with the current lifestyle that we're used to living. I hope that makes sense. It's inflation is making everything more expensive. So when I draw this little retirement right here, what we need is a lot more than $90,000 at retirement just to maintain what we're currently used to spending. And so out here it may be, we can see on the tool what that looks like, but we need a whole lot more. And so the question is, is the money that we're saving and how it performs and the couple factors that go into it that I can show you in a second, will that give us enough money to last our entire life? We go all the way to age 100 just because people are living longer and we want to be conservative. And so the question is, is the red line going to stay on the green line? And if that's the case, are we are financially in balance at least to maintain our current lifestyle? And for many of you, we want to do more than just maintain. And so this is not like saying that you're financially successful. This is just saying that you're balanced at where you're currently used to living. But what happens for most people is their red line stays on their green line. And then when they hit retirement a couple of years after some people less longer than others, it ends up dropping now. So security pensions might kick in. But what you find is this gap, it gets greater and greater from what your your current lifestyle would would be just to maintain where you're currently at and where your reality is. And then you get this massive gap. And this gap becomes a big issue. And again, there's not there's not let it many tools. There's not a lot of people talking about this. And as a result, they're not able to show you what's actually going on based on math versus based on some philosophy. So what I'm going to do is I'm just going to quickly pull up the tool just just so I can walk you through how this works. And so this is representing how what you're what when you would like to retire. So let's say 65. But let's all put 67. And then this is your initial money saved. And so let's say this person, this is you, let's say you have $100,000 saved up. You could have zero money. You could have a lot more, but you put that in. And let's say that this person saving $10,000 a year because that's what our example said. And we're assuming a 3% inflation rate, meaning that every year that the our current lifestyle needs increased by 3% just to keep can maintain what we're currently used to. We're going to assume that we can earn 7% in investments before retirement. And then obviously we're going to be a little bit more conservative after retirement, just to just to play it safe. And this is our salary, where we make $100,000 a year. We're also including that we can our our income is going to increase by 3% each year. And we are 30 in this example. And we're going to work till 67. Okay. What I'm also going to do is I'm also going to add Social Security. This is something that a lot of people miss. And for this example, you can always look these numbers up. But I'm just going to put 35,000. We're going to say it's going to increase at 2%. You're going to start at age 67. And it's going to go to age 100. And this is where you can put pension accounts. This is where you can put other details as really as that, you know, as it relates to this assessment. So this green line again represents early on, you need $90,000. When you hit 60 67, you need 268,000. Just to main just to currently consume what you're used to, you know, spending when you were 30 years old. That just shows you the power of inflation. Now if we calculate, you'll see that this model works and this assessment works all the way till age 84. And then drops off all the way down to 49,000. And you could see this gap. And so the question that we can mess around with is we can say how much money do I need to say? Is it $15,000 a year? That gets you to 92. Is it $17,000 a year? It's mean to 95. I might we might want to work longer. And so what we could do is we could work till 70. And that gets me that gets me there. Age 100, just right. Let's or I could work. I'm going to drop this down to 67 or I can maybe take a higher rate of return. And and now this this gets me there. So essentially the goal is to just see what it would look like to be in balance. And for most cases, trying to factor in a model of getting your getting a rate of return at 9% every single year. For a lot of people that might be risky and stressful. So so in many cases, what we need to do is how do we through efficiency find ways that you can find money, whether you're overpaying on taxes, whether you're missing money due to lack of tracking or there's so many ways that we can be in be more efficient and get your money to work for you in multiple areas. So in summary, this better wealth assessment is just to show you a good snapshot of where you're at and what you may need to do to get to where you are to go and to stay in balance. And I will say this don't get too depressed if you see this model being so out of whack and you and you lose hope. There are a lot of solutions. There's a lot of ways that we can tweak and really help you. And that's that's why this is just a basic model. There's a lot going behind the scenes. And actually as a company, we want to help people that are not in balance and in balance, there's different ways that we can help you. But really, it's just an area to see where you're at. And then the goal is to work with someone that can help you maximize what you're currently doing so that you can live a more intentional life. Thank you so much for listening to The Better Well Podcast. It would mean the world to me if you could hit subscribe, leave a review and share this with the people that you know and love.