Whole life insurance is a type of permanent life insurance that provides lifelong protection along with a savings component known as cash value. Unlike term life insurance, which only offers coverage for a set period, whole life insurance is designed to last your entire life—as long as premiums are paid. In this guide, we’ll explain how whole life insurance works, breaking down its key components, how cash value accumulates, and the tax benefits it offers. We’ll also reference a variety of reputable sources, including IRS guidelines and government resources, to give you a well-rounded understanding.

The Basics of Whole Life Insurance

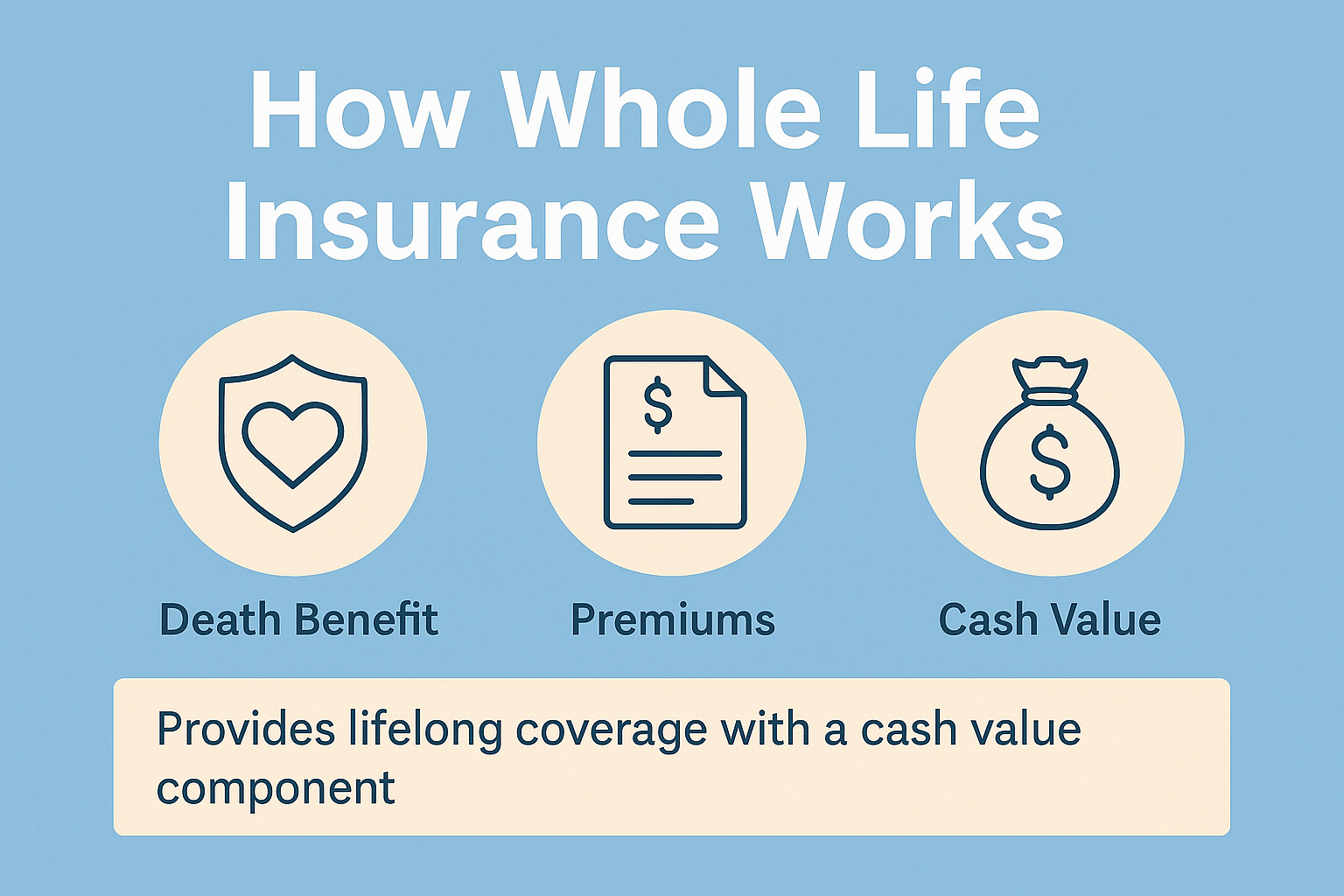

At its core, whole life insurance is a contract between you (the policyholder) and an insurance company. You agree to pay a fixed premium over your lifetime, and in return, the insurer promises to pay a death benefit to your beneficiaries upon your death. But whole life insurance does more than just provide a death benefit—it also builds cash value over time.

Key Components

- Death Benefit:

This is the lump-sum payment that your beneficiaries receive upon your death. It provides financial security to your loved ones and is typically paid out tax-free under current IRS rules (see IRS Topic 404 for more details). - Premiums:

Premiums for whole life insurance are generally fixed, meaning you pay the same amount each period regardless of changes in your age or health. These premiums cover the cost of insurance (risk coverage) and contribute to building the policy’s cash value. - Cash Value:

A portion of your premium goes into a cash value account. This cash value grows over time on a tax-deferred basis, meaning you don’t pay taxes on the gains as they accumulate, similar to retirement accounts. The cash value is guaranteed to grow at a set rate, and in some cases, the insurer may also pay dividends, which can further enhance growth. You can borrow against this cash value or even withdraw funds under certain conditions, providing you with financial flexibility during your lifetime.

The Insurance Information Institute (III) explains that whole life insurance is “a type of permanent life insurance that not only provides a death benefit but also accumulates cash value, which grows on a tax-deferred basis.”

How Cash Value Accumulation Works

One of the distinctive features of whole life insurance is its cash value component. Here’s how it works:

- Premium Allocation:

Your fixed premium is divided into two parts. One part covers the cost of insurance (the base) while the remainder contributes to the cash value. This cash value begins to grow from the first day of the policy. - Compound Interest:

The cash value grows over time by earning interest on both the principal amount and the accumulated interest from previous periods—a process known as compound interest. For example, even a modest guaranteed interest rate, typically between 2% and 3.25%, can lead to significant growth over decades. This growth is tax-deferred, as explained in IRS Publication 525 on taxable and nontaxable income (IRS Publication 525). - Dividends:

Many whole life policies from mutual insurance companies may also pay dividends if the company performs well. Although dividends are not guaranteed, when they are paid, they can be used to purchase additional paid-up insurance or to reduce your premium payments, further boosting your policy’s cash value.

Tax Advantages of Whole Life Insurance

One of the key benefits of whole life insurance is its tax efficiency:

- Tax-Deferred Growth:

The cash value grows tax-deferred, which means you don’t pay taxes on the gains each year. This allows for the power of compound interest to work without interference from annual tax liabilities. The IRS provides guidelines on the tax-deferred nature of such growth in various publications available on their website. - Tax-Free Death Benefit:

Generally, the death benefit paid out is not considered taxable income for your beneficiaries, ensuring that they receive the full benefit of your policy. This tax-free treatment is a major reason why whole life insurance is an attractive component of estate planning.

For detailed IRS information on the tax treatment of life insurance, visit the IRS Life Insurance Overview page.

Advantages and Considerations

Advantages

- Lifetime Coverage:

Whole life insurance guarantees lifelong protection, so your beneficiaries are assured a payout regardless of when you pass away. - Stable Premiums:

With fixed premiums, you have predictability in your long-term financial planning. This stability helps in budgeting and managing your finances over the long term. - Cash Value as an Asset:

The cash value component can act as a savings vehicle, offering flexibility in accessing funds for emergencies, opportunities, or supplementing retirement income. This dual-purpose nature makes whole life insurance unique.

Considerations

- Higher Cost:

Whole life insurance premiums are higher than those for term life insurance. For individuals who primarily need temporary coverage, this might represent an unnecessary expense. - Complexity:

Understanding the mechanics of cash value growth, dividends, and policy loans can be complex. It’s important to review your policy documents and consult with a financial advisor who can help you navigate these details. - Moderate Returns:

While whole life insurance provides a guaranteed rate of return, it typically does not match the potential returns of higher-risk investments. Its primary strength lies in stability and predictability rather than aggressive growth.

Conclusion

Whole life insurance works by providing lifelong protection combined with a savings component that grows over time through compound interest. With fixed premiums, a guaranteed death benefit, and a cash value that accumulates tax-deferred, it offers a unique blend of security and long-term financial growth. This makes it an invaluable tool for estate planning, financial stability, and even strategies like infinite banking.

To further explore how whole life insurance can fit into your financial plan, consider reviewing resources from the Insurance Information Institute, the American Council of Life Insurers, and IRS publications on taxable income and compound interest, such as IRS Publication 525.

By understanding how whole life insurance works and weighing its benefits against your financial goals, you can decide whether it’s the right tool to secure your family’s future and build a lasting legacy.

Whole life insurance is more than just a safety net—it’s a foundational financial tool that offers lifelong protection and steady, compound interest-driven growth. With the right strategy and expert guidance, it can become a cornerstone of your long-term financial plan.